Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.93 Trillion |

| Market Size (2031) | USD 1.13 Trillion |

| Growth Rate (2026 - 2031) | 3.97% CAGR |

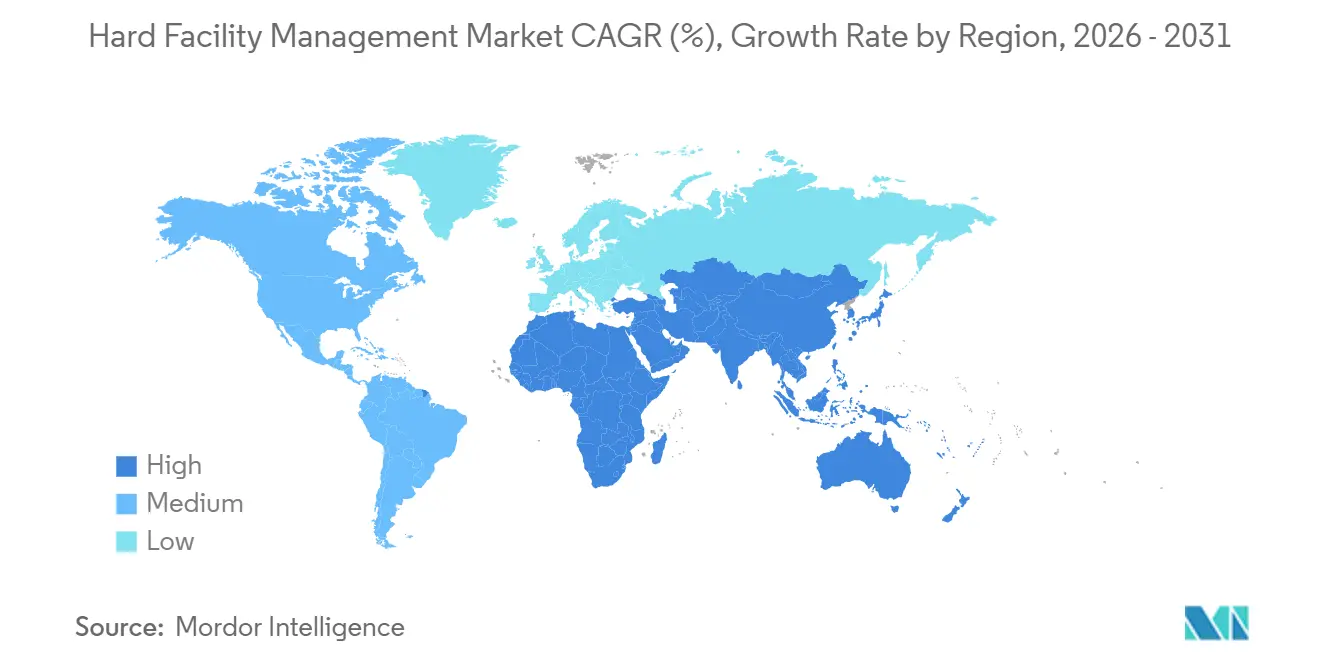

| Fastest Growing Market | Middle East |

| Largest Market | North America |

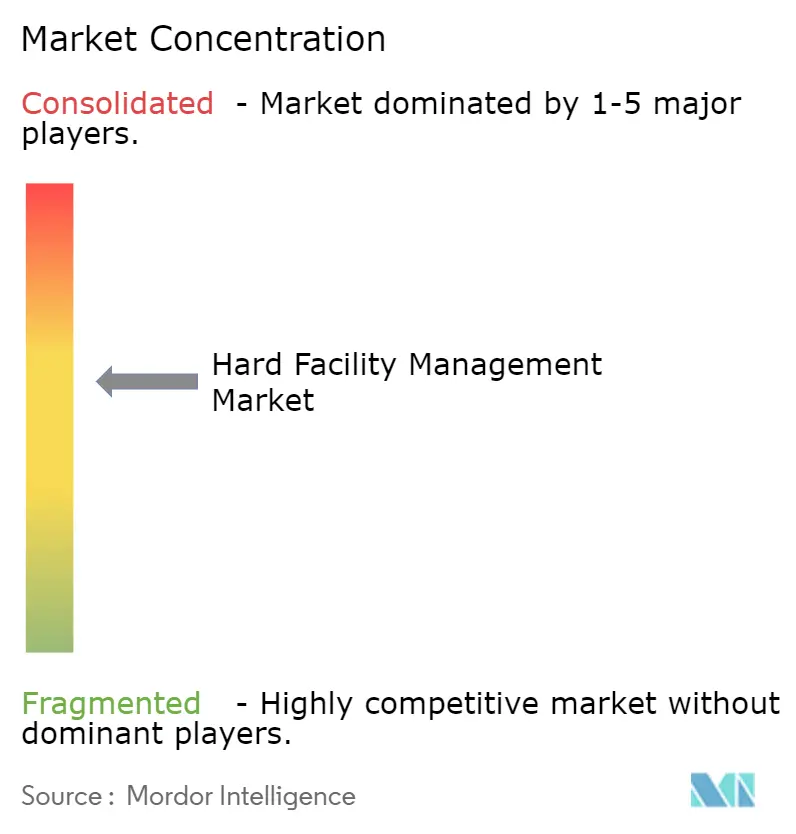

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hard Facility Management Market Analysis by Mordor Intelligence

The hard facility management market size is expected to increase from USD 890 billion in 2025 to USD 930 billion in 2026 and reach USD 1.13 trillion by 2031, growing at a CAGR of 3.97% over 2026-2031. Rapid migration from reactive toward predictive maintenance, expanding decarbonization mandates, and the rise of integrated outsourcing are reshaping cost structures and service mixes. Spending is shifting toward data-rich asset stewardship that merges building-automation data with cloud analytics, while multi-year contracts hedge labor‐cost volatility and guarantee uptime for mission-critical facilities. Private-equity roll-ups are injecting capital for digital platforms, accelerating adoption of AI-powered work-order routing, and widening the gap between technology-enabled leaders and single-trade specialists. Uptime guarantees in data centers exceeding 99.982% are redefining service quality thresholds and pressuring generalist contractors to deepen engineering capabilities.

Key Report Takeaways

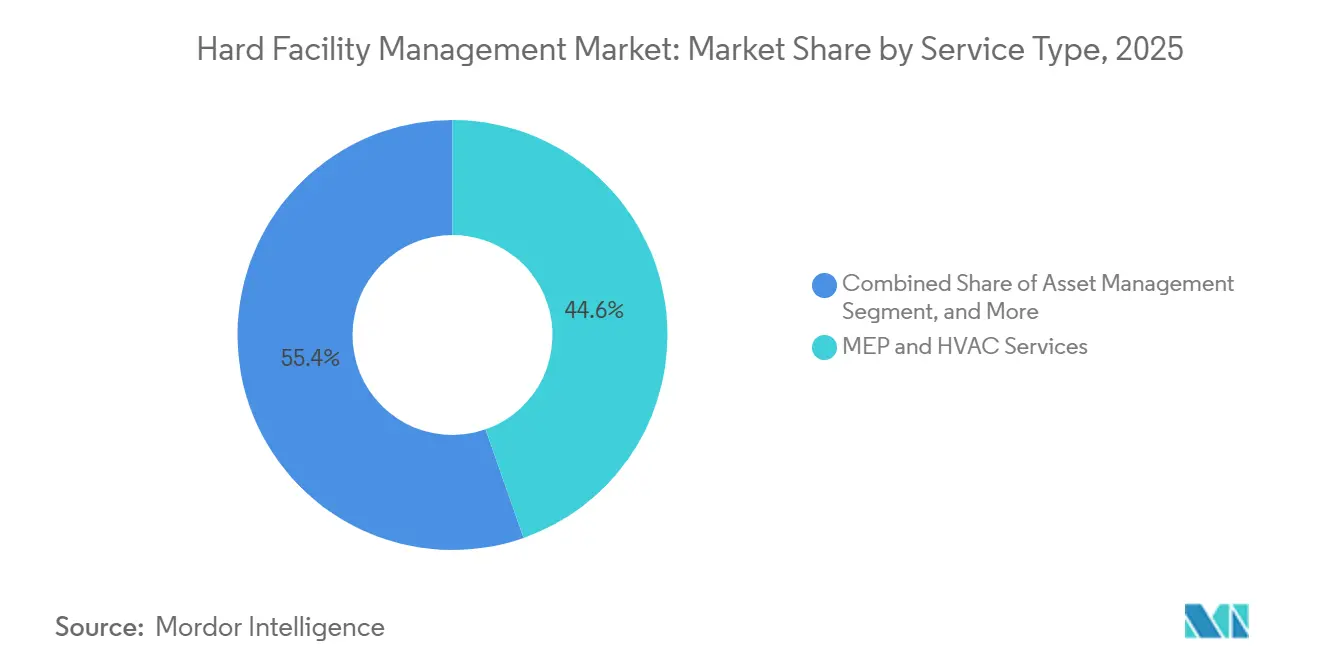

- By service type, MEP and HVAC services led with 44.63% of the hard facility management market share in 2025.

- By service type, asset management is projected to advance at a 4.32% CAGR through 2031.

- By offering type, outsourced delivery models held 58.71% of 2025 revenue and are forecast to expand at a 4.19% CAGR to 2031.

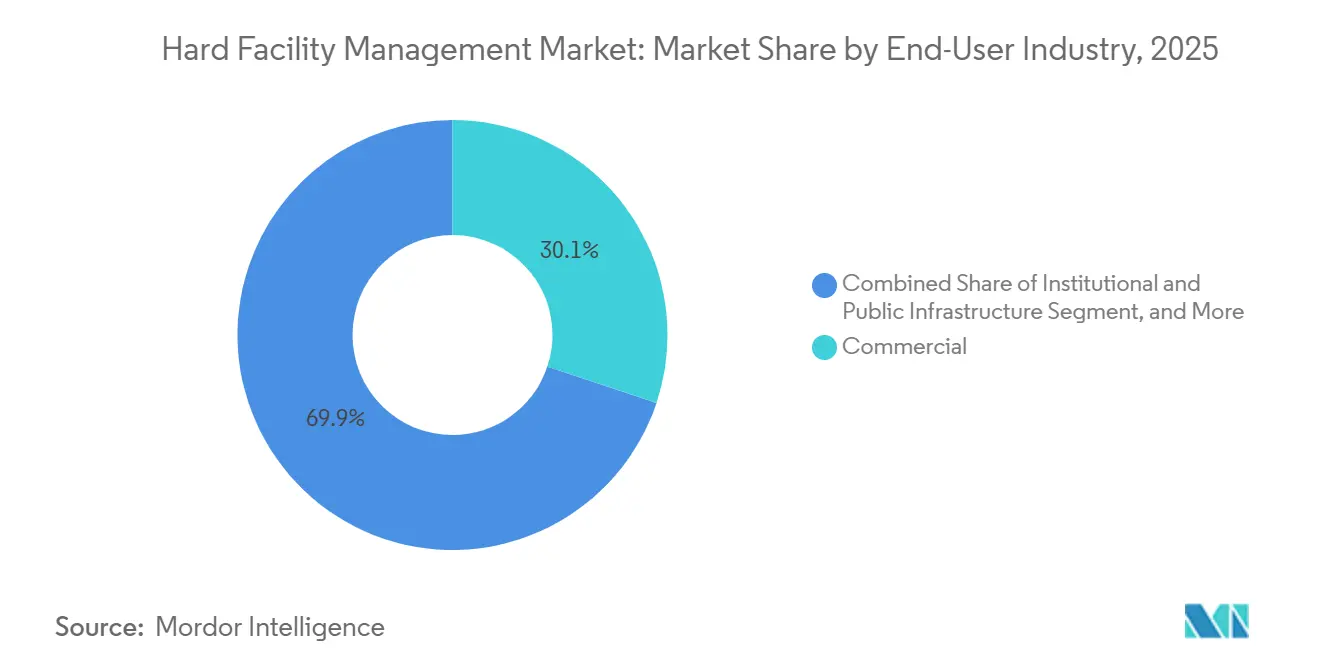

- By end-user, commercial real estate commanded 30.12% demand in 2025, while healthcare is set to grow at a 5.07% CAGR through 2031.

- By geography, North America accounted for 37.28% revenue in 2025; the Middle East is positioned for the fastest regional growth at 5.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hard Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Enabled Predictive Maintenance Platforms | +0.9% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Decarbonization Mandates Driving HVAC and Energy Retrofits | +1.2% | Europe and North America, spreading to Asia-Pacific | Long term (≥4 years) |

| Integrated Hard-Soft FM Outsourcing to Reduce Lifecycle Cost | +0.7% | Global, strong in commercial and healthcare sectors | Medium term (2-4 years) |

| Data-Driven FM Procurement and Cost-Inflation Hedging | +0.5% | Global, notably North America and Europe | Short term (≤2 years) |

| Resilience Upgrades for Climate-Related Extreme Weather Events | +0.6% | North America, Middle East, Asia-Pacific coastal | Long term (≥4 years) |

| Private-Equity Roll-Ups Accelerating Hard-FM Tech Adoption | +0.4% | North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Predictive Maintenance Platforms Drive Operational Transformation

Machine-learning models now analyze vibration, temperature, and power-draw data from HVAC chillers, boilers, and switchgear to flag anomalies weeks before a failure occurs, converting unplanned downtime into scheduled interventions. ABM Industries deployed the approach at an Ingredion site in 2025, avoiding compressor outages and saving USD 1.2 million annually.[1]ABM Industries, “Predictive Maintenance Use Case,” abm.com Building owners are embedding uptime clauses in service agreements, pushing providers to invest in sensor networks and data scientists. The shift favors large, capital-rich operators that can absorb upfront digital costs, accelerating consolidation. Predictive contracts also tighten supplier relationships because analytics platforms benchmark asset health against manufacturer data, compelling joint optimization of parts inventory and warranty coverage. As a result, the hard facility management market is moving toward outcome-based pricing tied to mean-time-between-failure metrics.

Decarbonization Mandates Accelerate HVAC and Energy Retrofit Investments

California’s 2025 code now requires heat pumps in new commercial builds, and the EU’s revised directive mandates zero-emission status for new structures by 2030, forcing rapid electrification of heating and ventilation.[2]European Commission, “Revised Energy Performance of Buildings Directive,” ec.europa.eu Demand has spiked for variable-refrigerant-flow systems, ground-source heat pumps, and high-performance façades that cut thermal bridging. Facility managers wrestle with securing retrofit capital that may exceed traditional contract horizons, amplifying interest in energy-service-company style agreements that spread repayment over savings. Procurement teams face lengthy lead times for compressors and inverters, a bottleneck that expands the role of integrated FM providers with sourcing leverage. Compliance frameworks such as ISO 50001 are now prerequisites for public tenders, raising entry barriers for smaller contractors and increasing the strategic importance of decarbonization credentials within the hard facility management market.

Integrated Hard-Soft FM Outsourcing Reduces Lifecycle Costs

Companies are bundling MEP, fire safety, and structural repairs with cleaning, security, and catering to secure end-to-end accountability. ISS reported 5.8% organic revenue growth in Q3-2025 due to integrated deals that cross-sell technical trades into its legacy soft-service base.[3]ISS World, “Q3-2025 Results,” issworld.com Bundling lets owners negotiate lifecycle guarantees rather than task-level rates, transferring risk to providers that must harmonize disparate labor pools and technology stacks. The model is thriving in healthcare, where infection control depends on synchronized asset performance and environmental services. Providers scaling too quickly face integration risk, highlighted by rising churn where labor scheduling systems and computerized maintenance management systems are not fully aligned. Nonetheless, the trend continues to expand the hard facility management market because integrated contracts often extend to seven-year tenures, encouraging deeper capital investment in predictive tools.

Data-Driven FM Procurement Enables Cost-Inflation Hedging Strategies

SourceBlue’s Q3-2025 MEP Cost Index reached 233, underlining spare-parts price hikes that have spurred data-centric procurement.[4]SourceBlue, “MEP Cost Index Q3-2025,” sourceblue.com Large providers aggregate spend across portfolios, using predictive models to time buy-outs for switchgear and chillers before commodity run-ups. Contracts now feature escalation caps tied to producer-price indices, transferring inflation risk to suppliers. Analytics also expose duplicate vendors, enabling strategic sourcing and volume rebates. Regional contractors lacking scale find themselves squeezed because they cannot leverage similar buying power or hedging instruments. Performance-based agreements that share energy-savings gains with providers are proliferating, further aligning incentives and embedding data analytics deep within the hard facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Trades Labor Shortages and Aging Workforce | -0.8% | Global, acute in North America and Europe | Long term (≥4 years) |

| Volatile Input Prices for Critical MEP Spare Parts | -0.6% | Global, regional supply-chain dependencies | Medium term (2-4 years) |

| Cyber-Security Vulnerabilities in Connected BMS | -0.3% | Global, digitally advanced markets | Short term (≤2 years) |

| Short Contract Tenures Limiting ROI on Hard-FM Capex | -0.4% | Global, especially commercial real estate | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Trades Labor Shortages Constrain Service Delivery Capacity

The Associated General Contractors of America revealed a 439,000-worker shortfall in the United States for 2025 projects, with 68% of technicians aged 45 plus and retirement outpacing apprenticeship intake. Wage inflation passed 6% annually, eroding fixed-price margins. Specialized roles in building-automation programming and fire-alarm integration face the steepest gaps because certification pathways are lengthy and vendor-specific. Immigration curbs intensify the squeeze in North America and Europe. Higher pay alone has not resolved the scarcity, prompting providers to invest in augmented-reality training and remote expert support to stretch scarce talent. Persistent shortages limit the capacity of the hard facility management market to absorb surging retrofit demand.

Volatile Input Prices for Critical MEP Spare Parts Increase Operational Costs

The International Energy Agency reported transformer costs climbed 75% between 2019 and 2025 on copper and steel inflation. Lead times for specialized switchgear now exceed 52 weeks, obliging providers to stock costly inventory or negotiate consignment deals. Fixed-price contracts signed prior to 2024 are underwater as suppliers refuse mid-term repricing. Some operators have adopted index-linked clauses, but clients often resist, leading to contract terminations. Commodity hedging is emerging as a core competency, and multi-regional sourcing strategies are spreading risk across suppliers. Elevated replacement costs compress profit margins and slow project schedules across the hard facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: MEP Dominance Meets Asset-Management Disruption

MEP and HVAC services claimed 44.63% of 2025 revenue, underscoring their role as the backbone of the hard facility management market size at facility level. Data-center power densities jumping toward 100 kW per rack accelerate demand for liquid cooling, redundant feeds, and precision controls. Quarterly inspections mandated by Joint Commission in healthcare sustain fire-safety work, while façade and structural repair volumes are event-driven, rising after climate events.

The rise of computerized maintenance management systems is elevating asset management, the fastest-growing service line at 4.32% CAGR. Platforms capture run-time data from chillers, pumps, and emergency power systems, calculate remaining useful life, and auto-schedule tasks. This convergence blurs distinctions between trades because analytics pull MEP telemetry into strategic planning. Smaller HVAC-only shops face consolidation pressure as owners pursue integrated bundles that cut administrative effort. Wireless smoke detectors and cloud alarms, recognized in NFPA 72-2025, further digitize inspection routines. Overall, the segment’s transition from break-fix to outcome-oriented service is a defining current for the hard facility management market.

By Offering Type: Outsourcing Gains as Capex Constraints Mount

Outsourced models held 58.71% of 2025 revenue, confirming that organizations prefer variable expense structures and specialist expertise. Integrated facility management contracts dominate healthcare and institutional bidding because they guarantee lifecycle cost ceilings. Bundled hard-FM agreements appeal to commercial landlords operating multisite portfolios that require service uniformity.

In-house teams, representing 41.29% in 2025, struggle to recruit trades, making external providers more attractive when contracts stretch to seven years and cover capital upgrades. Private-equity backed platforms court in-house operators with hybrid staff-placement models that blend onsite control with centralized procurement muscle. As a result, the hard facility management market size tied to outsourcing is set to widen its advantage through 2031. Performance-based clauses that align provider remuneration with uptime or energy savings deepen collaboration and anchor long-term partnerships.

By End-User Industry: Healthcare Outpaces Aging Commercial Stock

Commercial real estate delivered 30.12% of 2025 spending, led by office, retail, and mixed-use properties requesting standardized MEP and façade care. Yet healthcare is accelerating at a 5.07% CAGR, steered by demographic aging and infection-control imperatives that boost HVAC filtration and asset redundancy. Predictive sensors in operating suites now monitor particulate loads and temperature drift, triggering proactive filter changes that avoid surgical delays.

Institutional investors flood data centers, logistics warehouses, and senior-living facilities, each imposing distinct service intensity. Public infrastructure, constrained by budgets, anchors baseline demand through compliance frameworks such as ISO 14001. Vendors with clinical engineering capabilities are expanding fastest, while hospitality contractors pivot toward guest-experience metrics that embed FM ratings into customer satisfaction dashboards. These diverse needs reinforce segmentation depth within the hard facility management market, opening niches for specialist entrants even as integrated majors scale.

Geography Analysis

North America retained 37.28% of 2025 revenue because of vast legacy building stock and regulatory momentum around electrification. Federal incentives and state codes encourage retrofit cycles, especially in California where compulsory heat pumps now set design baselines. U.S. data-center clusters in Virginia and Texas amplify demand for high-density power and water-efficient cooling. Canada’s infrastructure renewals concur with P3 models that embed FM guarantees, binding long-term revenue.

Europe’s trajectory is dominated by the revised directive setting zero-emission goals for new buildings by 2030, which channels capital into HVAC electrification and envelope upgrades. Germany earmarked EUR 14 billion (USD 15.9 billion) for energy efficiency, subsidizing FM-led retrofits. Compliance with EPC classes A and B is reshaping procurement criteria, shunting preference toward providers with decarbonization roadmaps verified under ISO 50001.

The Middle East carries the fastest CAGR at 5.81% as Saudi Vision 2030 mega projects including NEOM and the Red Sea resort city demand climate-adapted HVAC and energy management. UAE directives under the Dubai 2040 master plan push smart-building integration and LEED Gold certifications. High ambient temperatures necessitate chiller plants with thermal storage and materials rated for 50 °C summers, intensifying per-square-foot spend. Asia-Pacific growth is propelled by China’s automation mandate for large commercial builds and India’s Smart Cities Mission, while South America and Africa progress in pockets as urbanization lures multinational occupiers. Across regions, regulatory energy targets, climatic extremes, and smart-city programs expand addressable volumes within the hard facility management market.

Competitive Landscape

The hard facility management market exhibits moderate concentration: the ten largest providers command roughly 35-40% of global revenue, leaving a fragmented field of regional and single-trade firms. Private-equity sponsors such as Blackstone, KKR, and Apollo spent 2025 aggregating mid-market operators and funding digital upgrades. CBRE posted USD 8.7 billion Q3-2025 revenue, citing Global Workplace Solutions as its growth engine after embedding predictive analytics and occupancy sensing. ISS, registering 5.8% organic expansion, leveraged integrated contracts to cross-sell hard FM into its soft portfolio. Sodexo’s onsite services contributed EUR 22.6 billion (USD 25.5 billion) in fiscal 2025, with hard FM near 30% of mix.

Data-center specialism constitutes a profit pool because liquid cooling and 99.982% uptime exceed the competences of generalist firms. New SaaS entrants offering asset-management portals can disintermediate full-service providers by letting owners orchestrate multiple contractors in-house. Cyber-security credentials now influence bids, especially where IEC 62443 compliance is stipulated; suppliers presenting third-party audits gain edge in healthcare and government verticals.

Patent filings for predictive-maintenance algorithms and digital-twin environments are rising, yet interoperability challenges hinder lock-in. Culture clashes during roll-up integrations risk service quality dips, giving incumbents a differentiation opportunity through proven global processes. Margin pressure from labor costs sparks innovation in mobile workforce management and augmented reality support, a critical lever as the hard facility management market scales digital intensity.

Hard Facility Management Industry Leaders

CB Richard Ellis (CBRE.)

Sodexo Facilities Management Services

Jones Lang LaSalle Incorporated

Johnson Controls International plc.

Cushman & Wakefield

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: CBRE partnered with Siemens Smart Infrastructure to roll out AI-driven building analytics across its Global Workplace Solutions portfolio, targeting 20% energy-cost savings.

- December 2025: ISS acquired a UAE technical FM specialist, adding 1,200 extreme-heat HVAC and fire-safety technicians to capture Saudi Vision 2030 projects.

- November 2025: EMCOR secured a USD 450 million, five-year contract covering 8 million ft² of North American data-center space with 99.99% uptime guarantees.

- October 2025: Mitie invested GBP 50 million (USD 63 million) in an in-house IoT platform to predict failures across 500,000 assets and support U.K. public-sector net-zero goals.

Global Hard Facility Management Market Report Scope

Hard facility management (HFM) services involve managing the people, technology, systems, and equipment that make up a company's physical structure.

The Hard Facility Management Report is Segmented by Service Type (Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard FM Services), Offering Type (In-House FM, Outsourced FM), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process Sector, Other End-User Industries), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Asset Management |

| MEP and HVAC Services |

| Fire Systems and Safety |

| Other Hard FM Services |

By Offering Type

| In-House FM | |

| Outsourced FM | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Asset Management | |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| By Offering Type | In-House FM | |

| Outsourced FM | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value for global hard facility management spending by 2031?

The hard facility management market is projected to reach USD 1.13 trillion by 2031.

Which service category currently generates the largest revenue?

MEP and HVAC services led with 44.63% of 2025 revenue.

Why is healthcare the fastest-growing end-user segment?

Aging demographics and stringent infection-control standards drive a 5.07% CAGR for healthcare through 2031.

How fast is the Middle East market expanding?

Fueled by mega projects under Saudi Vision 2030, the region is advancing at a 5.81% CAGR to 2031.

What role do predictive analytics play in facility management contracts?

Predictive platforms enable uptime guarantees, shift risk to providers, and underpin outcome-based pricing models.

Page last updated on: