Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

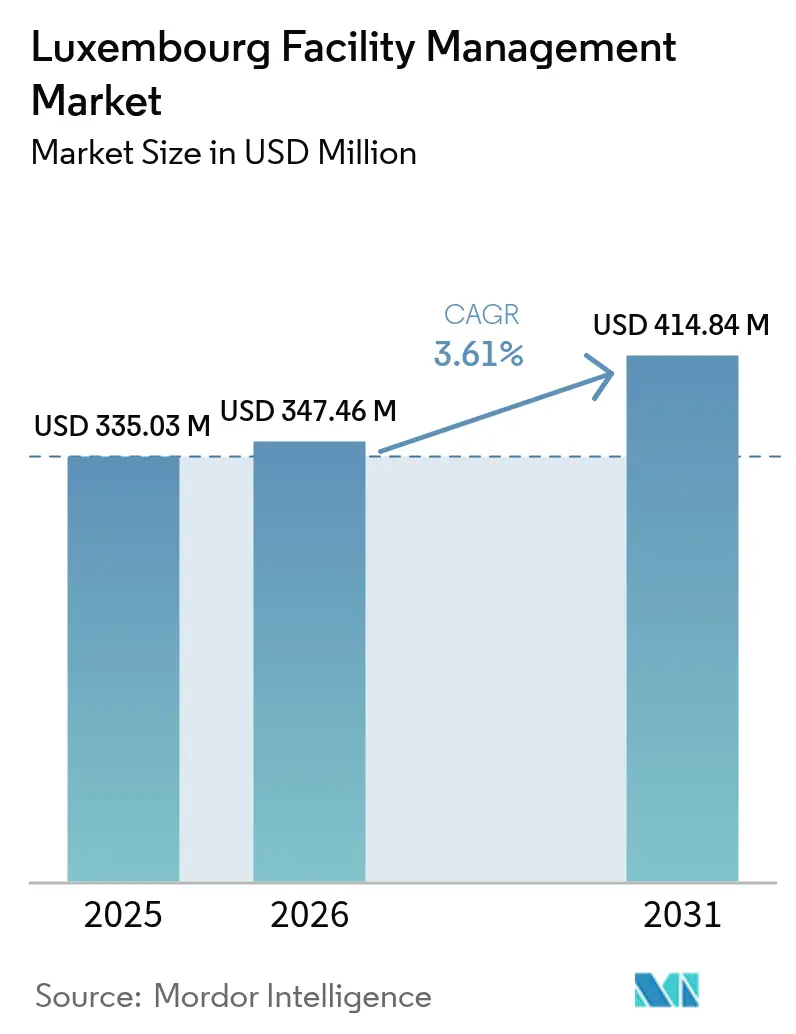

| Base Year Market Size (2025) | USD 335.03 Million |

| Market Size (2026) | USD 347.46 Million |

| Market Size (2031) | USD 414.84 Million |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxembourg Facility Management Market Analysis by Mordor Intelligence

The Luxembourg facility management market size is expected to increase from USD 335.03 million in 2025 to USD 347.46 million in 2026 and reach USD 414.84 million by 2031, growing at a CAGR of 3.61% over 2026-2031. Demand is tilting toward integrated contracts that weave cyber-physical security into building-management systems, reflecting the early impact of the Digital Operational Resilience Act and the EU Taxonomy Regulation. Hard services continue to anchor revenue as landlords retrofit mechanical, electrical and plumbing assets to meet stricter energy-performance thresholds, while soft-service growth benefits from a swelling data-center footprint and hospitality rebound. Outsourcing gains momentum because commercial owners want variable cost structures and turnkey ESG reporting, yet a persistent skills gap and inflation-driven cost pressures curb faster expansion. Competitive differentiation increasingly rests on digital twins, predictive analytics and carbon-accounting modules that reinforce client stickiness within the Luxembourg facility management market.

Key Report Takeaways

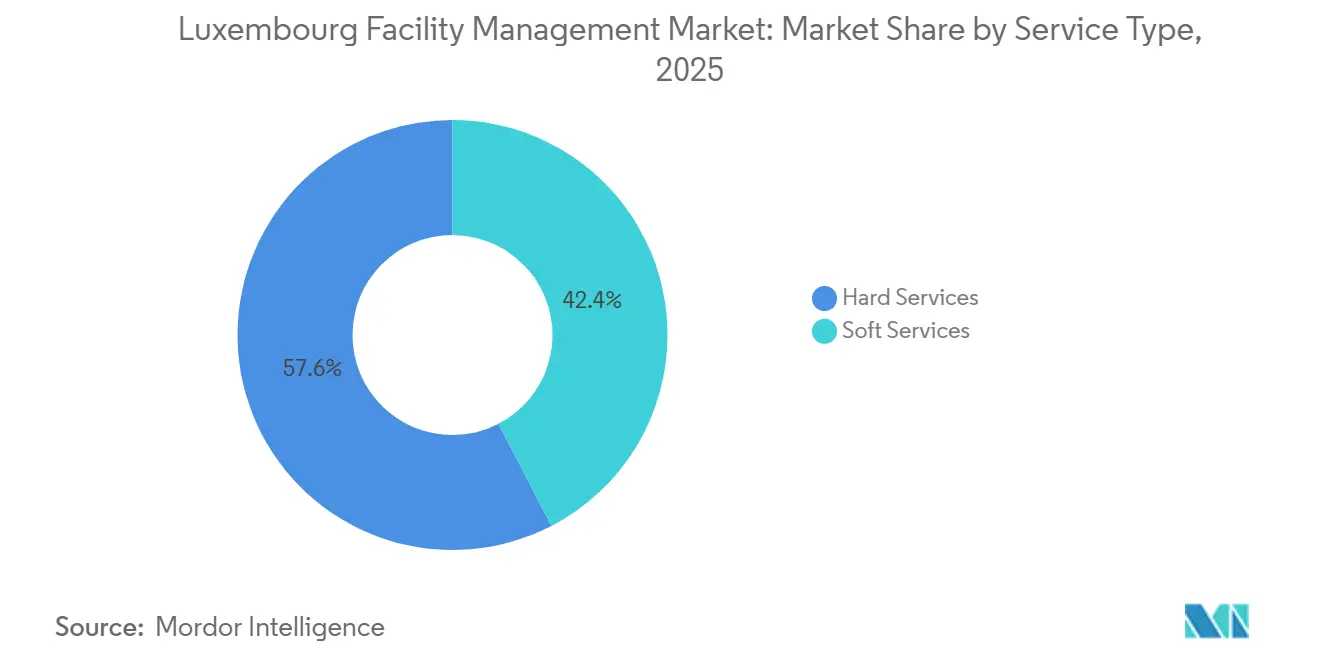

- By service type, hard services commanded 57.61% of the Luxembourg facility management market share in 2025, whereas soft services are projected to expand at a 4.23% CAGR through 2031.

- By delivery model, in-house management held 54.13% of the Luxembourg facility management market in 2025; outsourced contracts are forecast to grow at a 4.04% CAGR over 2026-2031.

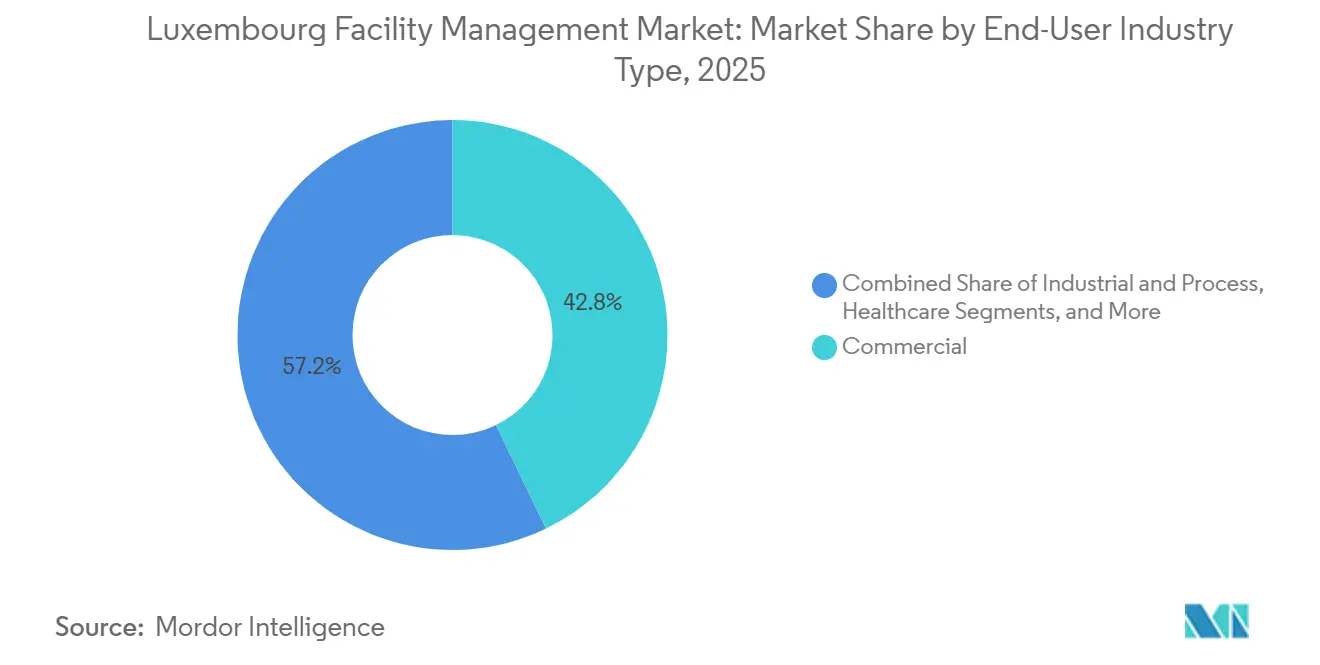

- By end-user industry, the commercial segment accounted for 42.84% of revenue in 2025 and is advancing at a 3.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Luxembourg Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technology-Led Integrated Facility Management Adoption | +1.2% | National, especially Kirchberg and Cloche d'Or | Medium term (2-4 years) |

| ESG Compliance Reshapes Service-Delivery Models | +0.9% | National, aligned with EU Taxonomy and CSRD | Long term (≥ 4 years) |

| Digital Operational Resilience Act Enhances ICT Risk Management | +0.7% | Financial-services corridor | Short term (≤ 2 years) |

| Data-Center Build-Out Fuels Critical-Environment FM Demand | +0.6% | Bettembourg and Betzdorf logistics zones | Medium term (2-4 years) |

| Workforce Transformation Lifts Soft-Services Expansion | +0.5% | National cross-border labor markets | Medium term (2-4 years) |

| Green-Building Incentives Accelerate Sustainable FM Uptake | +0.4% | National PRIMe House and LENOZ programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technology-Led Integrated Facility Management Drives Market Evolution

Integrated building-management platforms that connect HVAC, lighting, access control and occupancy sensors over a single IP backbone are now standard for Grade A offices in the Luxembourg facility management market. Providers embed artificial-intelligence algorithms that predict chiller failures up to 72 hours ahead, trimming unplanned downtime by 30% and delaying capital-equipment spend.[1]Siemens Smart Infrastructure, “Predictive Maintenance in Buildings,” SIEMENS.COM Dussmann tested a digital twin in late 2025 for a 15,000 m² mixed-use asset, pulling real-time data from 400 IoT points to fine-tune air-handling schedules and defer a rooftop-unit replacement by 18 months.[2]Dussmann Group, “Digital Twin Deployment,” DUSSMANN.DE Tenants favor these capabilities because they must benchmark energy-use intensity under the EU Level(s) framework, while landlords chase the 2030 near-zero-energy target. As government policy phases out fossil-fuel heating in public buildings by 2029, suppliers able to document quantifiable energy savings capture premium fees and longer contracts.

ESG Compliance Reshapes Service-Delivery Models

The EU Taxonomy Regulation requires primary energy demand at least 10% below nearly zero-energy thresholds, inserting sustainability clauses into bid specifications. Contracts now stipulate EU Ecolabel cleaning chemicals, sourcing of catering ingredients within 150 km and monthly waste-diversion reporting. Sodexo’s circular-economy kitchen model diverted 92% of organic waste to anaerobic digestion, earning GRESB 5-Star status in 2025.[3]Sodexo Group, “Circular Economy Catering,” SODEXO.COM Bonus-malus payment schemes tied to carbon-intensity reductions convert ESG compliance into revenue upside for providers that invest in low-emission equipment. The Corporate Sustainability Reporting Directive extends Scope 3 disclosure to companies with more than 250 employees in 2026, accelerating demand for auditable facility-level data streams that the Luxembourg facility management market now supplies.

Digital Operational Resilience Act Transforms ICT Risk Management

In force since January 2025, DORA obliges banks and insurers to prove ICT resilience, elevating the physical layer of data protection. Facility partners must guarantee biometric access accuracy, CCTV uptime and redundant power, or risk triggering reportable incidents. Vinci Facilities secured a three-year extension with a Tier 3 data center by integrating building-access logs into the client’s security-information and event-management platform and demonstrating ISO/IEC 27001 conformity.[4]Vinci Energies, “ISO/IEC 27001 Compliance Services,” VINCI-ENERGIES.COM Because DORA forces entities to audit third-party concentration risk, providers advertising operational independence and diversified supply chains win share in the Luxembourg facility management market.

Data-Center Build-Out Fuels Critical-Environment FM Demand

Installed data-center capacity surpassed 60 MW in 2025, positioning Luxembourg as a secondary FLAP-D hub and widening the addressable pool for critical-environment services. Atalian formed a specialised division in 2025, hiring Certified Data Centre Management Professionals and deploying Schneider Electric’s EcoStruxure platform across colocation sites. Hyperscale plans, such as Google’s proposed Bissen campus, will need 15-20 full-time facility staff versed in hot-aisle containment. Grid-capacity constraints could delay some projects, yet the segment’s high service intensity underpins above-market growth for the Luxembourg facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic Volatility Constrains Market Expansion | -0.6% | National, Eurozone spillover | Short term (≤ 2 years) |

| Technical Skills Gap Limits Service Sophistication | -0.4% | National cross-border labor markets | Medium term (2-4 years) |

| Fragmented Municipal Regulations Complicate Multi-Site Contracts | -0.3% | 102 communes | Long term (≥ 4 years) |

| Slow Uptake of Performance-Based Contracts Curbs Revenue Scalability | -0.2% | Commercial and institutional sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Volatility Constrains Market Expansion

Construction-cost inflation averaged 4.2% in 2024, forcing clients to delay discretionary upgrades while the European Central Bank kept its policy rate near 3.0% into 2026. Wage growth outpaced consumer inflation, squeezing margins for labor-heavy soft services, and some mid-tier providers exited unprofitable accounts. Hospitality operators, still operating below 2019 occupancy, renegotiated contracts with reduced service frequencies, clipping potential revenue for the Luxembourg facility management market.

Technical Skills Gap Limits Service Sophistication

The sector adds roughly 300-350 new technical posts each year, yet training programs graduate fewer than 200 qualified candidates, leaving a structural shortfall. Cross-border recruits face equivalency hurdles; French HVAC technicians must complete a 40-hour course to comply with Luxembourg safety rules. WISAG reported a 90-day average time-to-fill for building-automation roles in 2025, double that of cleaning staff, slowing the rollout of integrated contracts. Data-center certifications are even scarcer, inflating wage premiums and restraining the Luxembourg facility management market’s move up the value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Revenue, Soft Services Accelerate

Hard services held 57.61% of the Luxembourg facility management market in 2025, reflecting the capital intensity of MEP, HVAC and life-safety systems. Soft services are projected to expand at a 4.23% CAGR, outpacing overall growth as data centers and flexible workspaces demand higher cleaning and security frequencies. Within hard services, MEP and HVAC dominate because the F-Gas phase-down is driving an equipment-replacement wave. Fire-safety work benefits from stricter EN 54 false-alarm thresholds, compelling annual third-party smoke-detector testing.

Older building stock pushes envelope retrofits and HVAC upgrades, yet co-working hubs inflate daily cleaning and reception needs. Infection-control protocols triggered adoption of electrostatic disinfection and UV-C air purification, boosting specialized cleaning revenue. Food-cost inflation pressured catering margins, prompting plant-based menus that trim ingredient spend while pleasing ESG-minded tenants. These twin currents position soft services as the fastest-growing slice of the Luxembourg facility management market size through 2031.

By Offering Type: Outsourcing Gains as Clients Seek Risk Transfer

In-house teams managed 54.13% of facilities in 2025, mostly within government and critical-infrastructure owners who value direct control. Outsourced contracts will rise at a 4.04% CAGR as commercial landlords convert fixed labor costs to variable line items and rely on vendors for ESG data. Integrated agreements, about one-fifth of outsourced volume, gain favor by erasing hand-offs between hard and soft services. Bundled contracts suit mid-sized enterprises, while single-service deals persist in hospitality and healthcare.

Labor-transfer rules oblige new vendors to absorb incumbent staff at equivalent terms, limiting cost savings and reinforcing vendor selection on quality and retention. ISS reported 12% staff attrition in 2025, well below the 18% sector average, a statistic that helped it secure new multi-year awards. Stable workforces and auditable data pipelines underpin the competitive edge needed to grow share in the Luxembourg facility management market.

By End-User Industry: Commercial Segment Leads Growth Trajectory

Commercial real estate captured 42.84% of 2025 revenue and will maintain the strongest trajectory with a 3.74% CAGR, thanks to new Grade A completions in Kirchberg and Cloche d'Or. Institutional and public infrastructure contribute roughly one-fifth of sales, characterized by long contracts and prescriptive SLAs. Hospitality accounts for about 13% after lodging demand neared pre-pandemic levels, reviving housekeeping and F&B support.

Healthcare adds roughly 11%, where mandatory daily terminal cleaning inflates service intensity. Industrial users, though a smaller absolute base, pay premium rates for cleanroom upkeep and cold-chain monitoring. Financial services underpin commercial demand: they occupy 26% of office stock and drive above-average euros-per-square-meter spending. This tenant mix cements the commercial segment as the anchor of the Luxembourg facility management market size.

Geography Analysis

The Luxembourg facility management market concentrates within a 30 km corridor stretching from Luxembourg City to Esch-sur-Alzette and Differdange, an area that houses 75% of commercial floor space. Kirchberg commands the highest spending density, with annual outlays of EUR 180-220 (USD 203-248) per m². Cloche d'Or added three BREEAM Excellent towers in 2024-2025, each tendering integrated service packages that blend energy management, security and tenant amenities.

Esch-sur-Alzette is redeveloping metallurgical brownfields into creative campuses, spurring adaptive-reuse service needs. Northern cantons such as Clervaux and Vianden represent less than 5% of demand because their building stock skews residential. Cross-border labor dynamics shape supply; 45% of facility workers commute daily from France, Belgium and Germany, exposing operations to rail or fuel disruptions.

Regulation is national, but enforcement varies across 102 communes. The capital mandates quarterly fire-alarm tests, while some rural areas accept semi-annual cycles, forcing multi-site vendors to juggle disparate checklists. Government decentralization aims to divert 20% of new public-office builds to regional hubs by 2030, potentially diffusing opportunity beyond the city core. Even so, high per-capita GDP and a dense multinational tenant base keep the central corridor pivotal to the Luxembourg facility management market.

Competitive Landscape

The Luxembourg facility management market remains moderately concentrated: ISS, Sodexo, Dussmann, Vinci Facilities and Atalian control roughly 60%-65% of 2025 revenue. ISS and Sodexo invest heavily in proprietary platforms that give clients live dashboards for space use, service compliance and carbon footprints, extending average contract terms beyond three years. Dussmann and Vinci target high-spec environments such as data centers and pharma cleanrooms, leveraging ISO 14644 expertise and 24/7 critical monitoring.

Atalian and WISAG compete on cost and agility, focusing on mid-market landlords through streamlined bundles. Smaller firms like Wagner Facility Management carve niches by offering hyper-local response and multilingual support, valuable in a market where 48% of tenants are foreign-owned. IoT sensors and AI analytics raise the capital bar for new entrants yet strengthen incumbents’ moats. Lack of a dominant domestic champion opens the door to cross-border consolidation, although linguistic and labor protections raise integration friction.

White-space opportunities include outcome-based contracts pegged to energy savings, circular-economy waste monetization and management of micro-mobility assets as the city expands bike-share networks. Vendors able to combine technical depth, ESG metrics and digital transparency are best placed to widen their share of the Luxembourg facility management market.

Luxembourg Facility Management Industry Leaders

Sodexo SA

P. Dussmann Serv Romania S.R.L.

ISS Facility Services

Vinci facilities

Atalian Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sodexo Luxembourg rolled out a carbon-accounting module inside its catering and workplace services, letting clients track Scope 3 emissions at meal level. The solution piloted with three financial-services firms managing over 50,000 m² of offices.

- December 2025: Dussmann Luxembourg activated a digital twin for a 15,000 m² mixed-use complex in Cloche d'Or, optimizing HVAC schedules and extending equipment life by 18 months.

- November 2025: ISS Luxembourg won a five-year integrated contract for a 12,000 m² financial headquarters in Kirchberg, bundling predictive maintenance, IoT space analytics and ISO 14001 waste management.

- September 2025: Vinci Facilities Luxembourg renewed a three-year deal with a Tier 3 data-center operator after aligning with ISO/IEC 27001 and DORA reporting.

Luxembourg Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through their responsibility for maintaining what is often an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

The Luxembourg Facility Management Market Report is Segmented by Service Type (Hard Services: Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Services; Soft Services: Office Support and Security, Cleaning Services, Catering Services, Other Soft Services), Offering Type (In-House, Outsourced: Single, Bundled, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography (Luxembourg). The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-House | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-House | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is driving demand for integrated contracts in the Luxembourg facility management market?

New EU regulations on digital resilience and sustainability are pushing landlords and tenants to seek single-provider solutions that bundle cyber-physical security and ESG reporting.

How large will the Luxembourg facility management market size be by 2031?

It is projected to reach USD 414.84 million by 2031, expanding at a 3.61% CAGR from 2026.

Which service type is growing fastest in the Luxembourg facility management industry?

Soft services, notably security and cleaning, are forecast to rise at a 4.23% CAGR through 2031.

Why are outsourced models gaining share?

Commercial owners want variable cost structures and turnkey compliance data, prompting a 4.04% CAGR for outsourced contracts.

What segments hold the highest Luxembourg facility management market share today?

Hard services command 57.61% of revenue, while the commercial end-user segment leads with 42.84%.

How concentrated is competition?

The top five vendors control about 60%-65% of revenue, reflecting moderate concentration with room for niche specialists.

Page last updated on: