Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

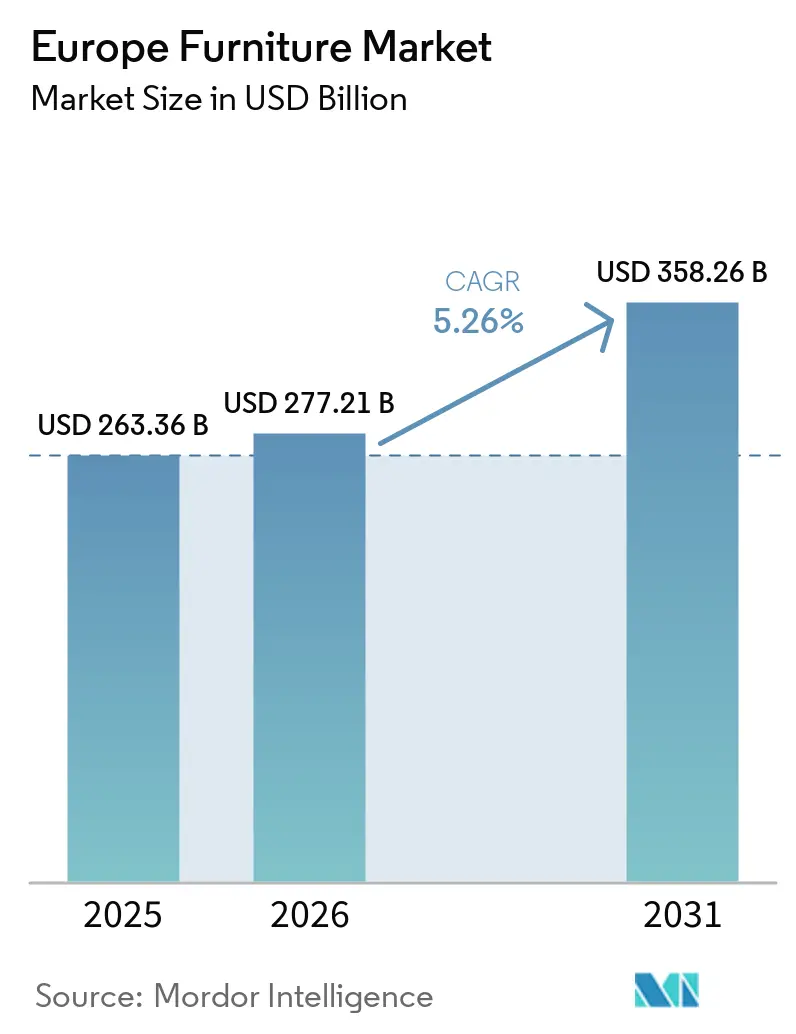

| Base Year Market Size (2025) | USD 263.36 Billion |

| Market Size (2026) | USD 277.21 Billion |

| Market Size (2031) | USD 358.26 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Furniture Market Analysis by Mordor Intelligence

Europe furniture market size was valued at USD 263.36 billion in 2025 and is estimated to grow from USD 277.21 billion in 2026 to reach USD 358.26 billion by 2031, at a CAGR of 5.26% during the forecast period (2026-2031). The growth outlook reflects persistent tailwinds from EU renovation programs, hybrid work normalization, and demographic demand for ergonomic solutions that support aging populations. Western Europe remains the centre of gravity, and Germany continues to anchor value pools even as its share faces pressure from import penetration and a housing downturn. Spain is emerging as a growth leader with robust housing activity and tourism-driven hotel refurbishment cycles that elevate hospitality-related demand. Digitalization of retail and the One-Stop-Shop VAT regime are improving cross-border e-commerce operations and reinforcing omnichannel growth, particularly for mid-range sellers that can scale logistics and customer service efficiently.

Key Report Takeaways

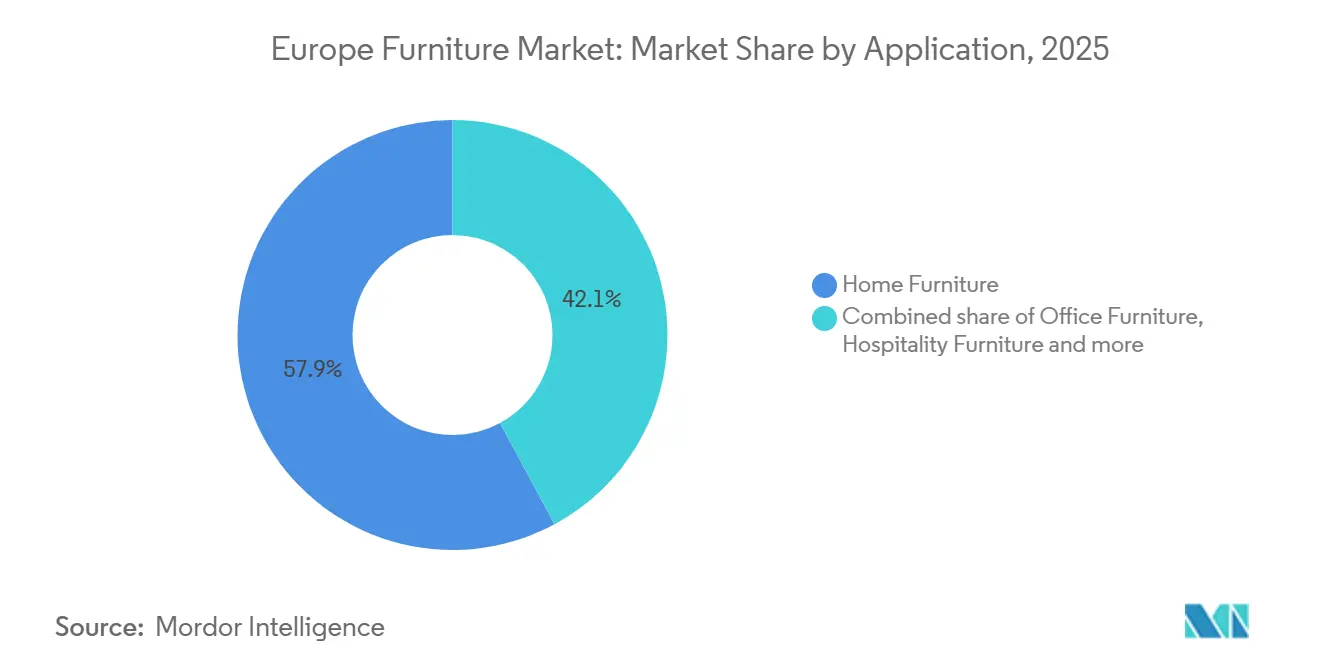

- By application, home furniture led with 57.87% of the European furniture market size in 2025. Office furniture is forecast to expand at a 6.72% CAGR through 2031.

- By material, wood furniture held 51.87% of the European furniture market share in 2025. Plastic and polymer furniture is expected to grow at a 6.38% CAGR through 2031.

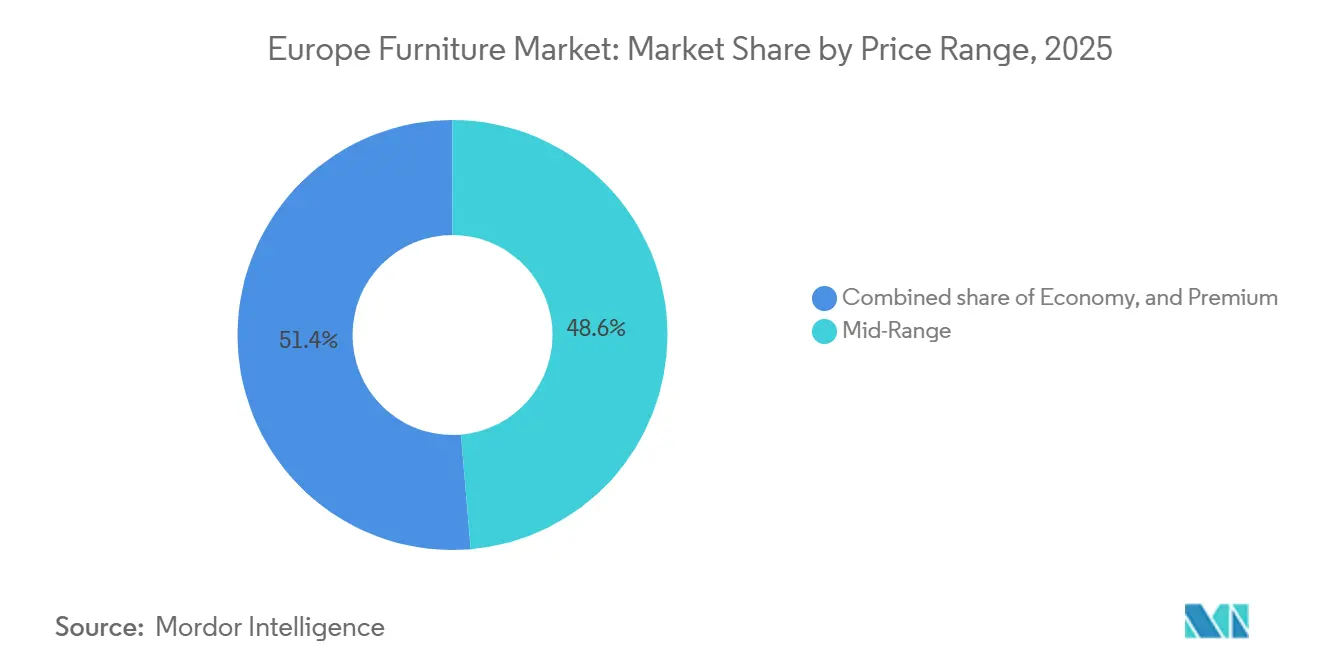

- By price range, mid-range accounted for 48.64% of the European furniture market share in 2025. Premium offerings are projected to expand at a 5.83% CAGR through 2031.

- By distribution channel, B2C or retail held 74.35% of the European furniture market share in 2025. B2C is set to advance at a 7.33% CAGR through 2031.

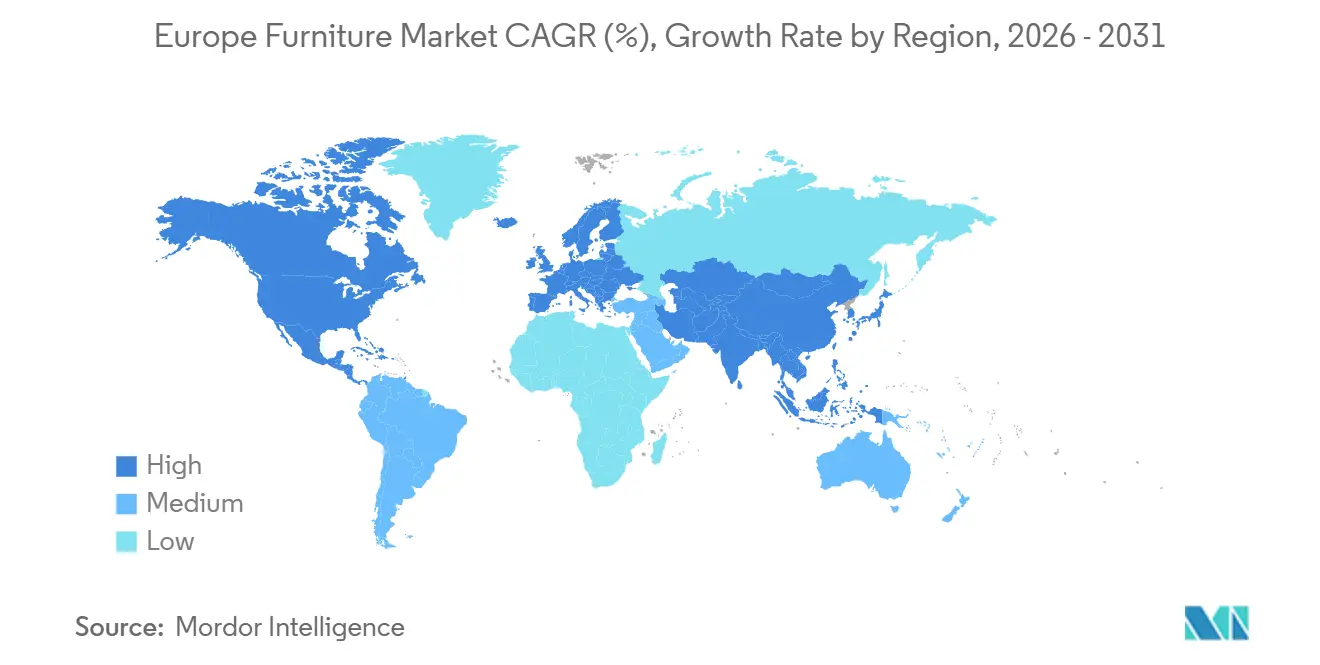

- By geography, Germany held 19.39% of the European furniture market share in 2025. Spain is projected to grow at a 6.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Furniture Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU renovation grants and energy retrofits drive replacement cycles | +1.2% | Western Europe, with gains in Northern Europe | Medium term (2-4 years) |

| Net household formation via build-to-rent and micro-housing | +0.9% | Western Europe and major urban hubs | Medium term (2-4 years) |

| Aging demographics increase spending on ergonomic and assisted-living solutions | +0.7% | Western Europe, with high shares in Germany, Italy, and France | Long term (≥ 4 years) |

| Hybrid work normalizes demand for home office and modular workspaces | +1.1% | Western Europe and Northern Europe | Short term (≤ 2 years) |

| Tourism revival and hotel pipeline expansion lift hospitality demand | +0.8% | Southern Europe, with strong Spain and Italy exposure | Medium term (2-4 years) |

| Cross-border e-commerce, BNPL, and OSS VAT expand access | +0.6% | EU-27 with digitally mature Northern and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Renovation Grants and Energy Retrofits Driving Large-Scale Furniture Replacement

EU renovation policy aims to double renovation rates by 2030 and retrofit 35 million buildings, which increases replacement cycles for kitchens, living spaces, and work areas aligned to modern performance and safety standards. National programs and local funding channels complement EU-level goals and contribute to retrofits getting pulled forward as property owners address insulation, ventilation, and layout improvements. Renovated homes often require integrated storage, modular seating, and cabinetry that can accommodate efficient appliances and better air quality standards. The share of residents in dwellings with efficiency improvements rose in recent years, which supports steady furniture refresh activity as owners complete multi-year projects. These policy actions intersect with tightening chemical emissions rules for components and coatings, prompting shifts to lower emissions in materials and finishes across the supply base. Manufacturers operating in Northern Europe reported facility and process adjustments, including wider use of water-based coatings and steps to trim VOC emissions, that align with emerging compliance thresholds.

Hybrid Work Normalization Sustaining Demand for Home Office and Modular Workspace Furniture

Hybrid work settled into long-run usage levels, which keep home office equipment and compact workstations relevant for both B2C and project channels. France-based surveys show sustained interest in remote work options and continued fit-out and reconfiguration projects as employers reshape space for collaboration and shared desks. Occupiers reduced enclosed offices and expanded collaborative areas, prompting purchases of ergonomic chairs, height-adjustable desks, and acoustic solutions that raise per-employee specification levels even as total desk counts per head decline. This creates a shift in purchasing from traditional distribution to project-based procurement for shop and contract use, which partially offsets softer order books in classic office lines. The expansion of second-hand and refurbished office furniture gained momentum as sellers highlight lower cost and verified carbon reductions compared with new products. Retailers and refurbishers emphasize omnichannel merchandising, in-store configuration tools, and after-sales services to capture hybrid-driven demand that moves between home and workplace settings.

Cross-Border E-Commerce, BNPL, and OSS VAT Regime Broadening Access

The EU's One-Stop-Shop (OSS) VAT regime, implemented on July 1, 2021, under EU Directive 2017/2455, streamlined cross-border e-commerce VAT compliance by allowing sellers to remit VAT in a single member state for all intra-EU distance sales, eliminating the need for multiple VAT registrations. This administrative simplification particularly benefited mid-range furniture sellers and marketplaces, enabling IKEA's online share to reach 30% of sales (up 2 percentage points) in FY2025, while Wayfair's international segment (Canada, UK) grew 10% year-over-year in Q2 2025; the company exited Germany in January 2025. BNPL usage remains limited in furniture compared to cards and cash, yet it has expanded the addressable base for mid-priced goods in several markets. Some sellers favor consolidation of VAT and compliance within the OSS framework to control back-office costs and speed up market entries in adjacent EU geographies. International online specialists showed mixed results in continental competition, and exits in Germany underlined the challenge of scaling profitably against entrenched physical-first incumbents.

Aging Demographics Increasing Spend on Ergonomic and Assisted-Living Solutions

Europe's ageing population is reshaping furniture demand curves, with the 65-74 age cohort spending more than the average on home furnishings and routine household management, according to the Swiss Federal Statistical Office's 2018-2019 Household Budget Survey. However, France's Think Tank Matières Grises and public agency ANAP revealed in September 2024 that the average age for starting home adaptation work is 84 years, far too late to prevent fall-related injuries that cause over 10,000 annual deaths among French seniors aged 65+, with 75% of fatal falls occurring in those 75 and over. Policy programs to finance home adaptations can accelerate timely investments that favor furniture designed for limited mobility and compact spaces in senior residences. The expansion of assisted-living and seniors’ serviced apartments increases demand for compact ergonomic solutions with durable materials and modular layouts that ease maintenance and reconfiguration. Constrained public budgets and varying occupational therapy capacity influence uptake, yet the need is persistent and growing across regions with high 65+ shares. Household financial stress still weighs on purchase decisions in several member states, but the functional value and safety gains of adaptive furnishings are rising in priority within older age cohorts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent inflation and real-wage pressure are delaying big-ticket purchases | -1.3% | Southern and Eastern Europe with broader global exposure | Short term (≤ 2 years) |

| Volatile certified timber, foam, and metal prices squeeze margins | -0.9% | Europe with upstream sensitivity in Nordics and Baltics | Medium term (2-4 years) |

| Mature Western European markets extend replacement cycles | -0.8% | Western Europe's core markets | Long term (≥ 4 years) |

| Strict REACH and fire-safety standards raise compliance costs | -0.5% | Pan-European, with highest impact on upholstery and foam-based furniture manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Inflation and Real-Wage Pressure Delaying Big-Ticket Purchases

Headline inflation moderated across the euro area in 2025 compared with the 2022 peak, yet wage and price dynamics kept real household purchasing power under pressure. Survey data indicate a rise in the share of EU residents who could not afford to replace worn-out furniture in 2024, with the 50-64 cohort reporting the highest constraint levels. Housing cost overburden remains acute among the lowest income quintile, limiting discretionary budgets available for large purchases such as sofas, dining sets, and fitted storage. Germany’s price trends showed year-over-year declines in several furniture categories in early 2025, a sign of demand weakness that forced markdowns even as headline CPI rose. The Netherlands recorded a negative contribution from furnishings and household equipment to inflation in 2024 compared with a positive contribution a year earlier, underscoring subdued category demand[1]Statistics Netherlands, “Inflation Rate 3.3 Percent in 2024,” Statistics Netherlands, cbs.nl. This backdrop supports value-seeking behavior and elongated decision cycles, which dampen order intake and stretch conversion timelines for retailers and manufacturers.

Volatile Certified Timber, Foam, and Metal Prices Squeezing Margins

Cost volatility in core inputs such as sawlogs, foam feedstocks, and metals constrained margins and drove consolidation in the European sawn timber segment in 2024 and 2025. Elevated log prices in key supplying regions weighed on sawmills, while energy inputs added further pressure for energy-intensive fabrication processes. Global commodity views projected aluminum price declines in 2025 with some relief on material costs, yet higher European natural gas prices kept energy bills elevated through 2025, shaping tactical pricing. Compliance with traceability rules for wood products entering EU markets increased system costs, and companies raised concerns about readiness and documentation burdens. Import realignments following changes in third-country policies, reshaped flows, and reinforced the relative cost advantage of efficient producers across the Baltic states. Category-specific import declines for tropical sawnwood in 2024 also reflected regulatory effects and sourcing adjustments within supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Home Furniture Dominates While Office Lines Rebound Behind Hybrid Workplace

Home furniture held the largest market share at 57.87% in 2025, while office furniture is projected to grow at a 6.72% CAGR through 2031. Employers standardizing hybrid schedules and retrofitting spaces for collaboration drive this growth. Hybrid routines blur living and working zones, sustaining demand for multiuse sofas, dynamic storage, and compact desks for apartments and small homes. Kitchen cabinetry trends in 2024 varied by country, highlighting the role of housing market momentum in big-ticket installed furniture. Wardrobes and bedroom furniture remained resilient as consumers prioritized personal storage and sleep comfort, offsetting declines in other subcategories. Bathroom furniture benefited from small-space renovations tied to micro-housing programs and urban densification projects, emphasizing compactness and functionality.

Office furniture’s recovery is shaped by return-to-office measures and a shift to project-based procurement for contract applications, altering order flows. Germany’s midyear data in 2025 showed declining traditional office volumes but improving shop or contract activity, indicating a move toward broader project-based layouts. In France, sealed private offices gave way to shared and collaborative spaces, boosting demand for acoustic pods and adjustable desks with integrated power and charging.

Hospitality furniture gained traction with tourism recovery and hotel renovation projects in Southern Europe, with Spain’s island destinations leading. France’s reuse quotas in public procurement are fostering repair and refurbishment ecosystems, extending institutional furniture life cycles.

By Material: Wood Retains the Majority, While Plastics and Polymers Scale on Circular Rules

Wood held a 51.87% share in the market in 2025, supported by certification, consumer preference for natural finishes, and reliable supply in European regions. Compliance costs and upstream volatility remain challenges, but certified wood and recycled content in panels and boards are scaling in production. Circular material choices are increasingly integrated into product development, with higher recovery rates from wood waste and a growing share of recycled wood in board inputs reported by industry associations. Metal frames and components are essential in office seating, outdoor environments, and contract applications requiring durability and structural integrity. Energy conditions for metals and fabrication influence pricing and margins, with the net effect depending on the balance between lower commodity prices and higher energy costs.

Plastics and polymers are expected to grow fastest at a 6.38% CAGR through 2031, driven by circular design and recyclability mandates. Prototypes and product lines using post-consumer and post-industrial inputs demonstrate compliance with technical standards and viable performance in emerging applications. Large retailers are retooling packaging and small component choices to reduce plastics and support recyclability goals. Paints and coatings are adapting to stricter emissions standards, with producers advancing alternative chemistries aligned with indoor air quality targets. Polymer-based parts and recycled composites are expanding into seating shells, tabletops, and decorative elements at scale.

By Price Range: Mid-Range Anchors Volume While Premium Defies Affordability Headwinds

The mid-range segment held a 48.64% market share in 2025, driven by its balance of design, durability, and price. Large-format retailers significantly influenced this segment, with pricing strategies in 2024 and 2025 reducing average customer prices year over year to defend market share. Based on 2024 data, the lower-priced economy segment faced challenges in Germany, while the premium segment showed growth, reflecting resilience among high-income consumers. The average kitchen price in Germany reached a new high in 2024, despite a decline in total volumes, indicating a polarization in the purchase mix. Category leaders focused on omnichannel strategies and price adjustments to sustain basket sizes and repeat purchases in a cautious consumption environment.

The premium furniture segment is expected to grow at a 5.83% CAGR through 2031, supported by high-net-worth consumers investing in signature pieces, bespoke upholstery, and coordinated designs. Luxury brands in Italy and France expanded showrooms, collaborations, and diversified into mobility and hospitality categories to enhance visibility among affluent travelers. Select Italian brands reported multi-year growth and expanded retail footprints in the Middle East and Asia, boosting exports alongside European sales. Circular and ecological furniture categories in Spain and other markets command price premiums, appealing to affluent customers. Secondary market activity increased as budget-conscious households opted for refurbished goods, redistributing volumes across price tiers without affecting premium segment growth[2]World Bank, “Commodity Markets Outlook, April 2025,” World Bank, worldbank.org.

By Distribution Channel: Physical Retail Leads While E-Commerce Drives Momentum

B2C and retail channels held a 74.35% share in 2025 and are forecast to grow at a 7.33% CAGR through 2031, supported by omnichannel integration and reduced frictions in cross-border selling. National breakdowns confirm that big-box home centers and specialist stores retain a leading role in category sales, complemented by smaller DIY and lifestyle outlets. Online shares climbed in Germany, Italy, and Spain in 2024, and ROPO behavior adds another layer of digitally influenced purchases that finalize in stores. Global platform players reported mixed international performance in 2025, with exits in Germany that highlight the structural advantage of entrenched physical networks. Leading retailers increased the online portion of sales and invested in price accessibility to stabilize quantities sold in 2025 against a softer macro backdrop.

B2B and project channels concentrated on contract spending in hospitality, healthcare, education, and corporate fit-outs as tenants reconfigure holdings and landlords refresh assets. Spain’s distribution mix indicates a rising share of direct sales to final customers within the contract pathway, reflecting the importance of design-to-install service bundles. Germany’s contract segment delivered modest growth in the first half of 2025 while traditional office moved lower, a sign that capital plans favored shopfitting and retail environments. Showrooms in major cities across Europe added trade and contract teams, visualization services, and project management capacity to accelerate conversions. The European furniture industry is channeling capability toward service-heavy projects as retailers and brands aim to defend share in a complex demand environment.

Geography Analysis

Germany accounted for 19.39% of the 2025 revenue, maintaining the largest country exposure in the region as the European furniture market aligns with Western European income levels and household structures. Production and retail performance in 2024 and the first half of 2025 showed declines due to weak housing completions and tightening household budgets. Import penetration reached record levels, with shipments from China and Poland displacing domestic output, intensifying price competition, and straining capacities. Stability appears dependent on easing inflation and renovation-driven replacements rather than a recovery in new housing construction, given the current pipeline outlook. The share of the European furniture market linked to German demand is expected to decline before stabilizing at more sustainable levels later in the forecast period[3]VDM/VHK, “Umsatz der deutschen Möbelindustrie liegt im ersten Halbjahr um 5 Prozent unter dem Vorjahresniveau,” Verbände der deutschen Möbelindustrie, moebelindustrie.de.

France and Italy experienced softer market conditions in 2024 and early 2025, though the underlying drivers and sector compositions differ. Total sales and production in France declined year over year, with the export coverage rate falling as imports increased, highlighting the challenge of competing at scale in a market with significant import exposure. Italy furniture sector faced a second consecutive year of turnover decline in 2024, though exports to the Gulf and Spain partially offset weaker flows to key European partners. Purchasing constraints and higher financing costs dampened replacement cycles. Despite these challenges, Italian brand leaders advanced premium product lines and expanded store openings in strategic international locations. Renovation-related spending and senior adaptation programs are expected to support recovery, alongside targeted domestic industrial initiatives.

Spain is projected to achieve a 6.98% CAGR through 2031, driven by tourism-led hotel renovations, increased household purchasing intent, and a favorable retail mix. Retail trade grew in 2024, with notable increases in kitchen furniture and office lines, while production totals showed slight growth alongside stable employment levels. Imports outpaced exports in early 2025, widening the trade deficit but reflecting strong domestic demand for design-focused and mid-range products. Consumer intent and average transaction values rose in 2025, indicating improved discretionary spending and growing interest in furniture categories among younger households. Spain’s island regions demonstrated the fastest hospitality growth in the country, bolstering contract demand throughout the forecast period.

Competitive Landscape

The European furniture market is moderately to highly fragmented, with the largest five players accounting for a small minority of total regional revenue. This leaves a significant presence of national and regional producers. In 2025, category leaders focused on affordability, accessibility, and sustainability, including price adjustments to maintain unit volumes and expand online market share. Retailers adopted new store formats and smaller urban locations to increase visitation and improve service density in city centers, supporting repeat customer visits amid tight budgets. Vertically integrated models provided cost control and margin stability through improved energy sourcing and logistics, offering a competitive edge during economic downturns. Market dynamics also reflected ongoing import competition from Asia and strengthening regional supply chains in Poland and the Baltics.

In December 2025, consolidation reshaped the contract office furniture segment with a major transaction creating a leading entity with an enhanced platform across North American and international markets. The combined company targeted synergies and deleveraging goals over a multi-year period, with rating agencies maintaining a stable outlook for its capital structure. Product launches in late 2025 emphasized ergonomic innovations for workstation seating and collaborative environments. Dealer networks and project channels linked European enterprise demand with international contract brands. Competitive strategies among European mid-sized manufacturers included specialization, circular economy services, and streamlining low-margin product lines.

Retailers with pan-European operations accelerated store openings and concept upgrades, entering new markets while enhancing digital capabilities. In 2025, expansion initiatives included new store launches across Europe and Africa, IT investments to improve merchandising and logistics, and flagship refurbishments serving as design and trade hubs. Luxury and premium brands expanded in the Middle East and Asia and strengthened positions in contract interiors for high-end hospitality and aviation. Recycling and materials investments aligned with circular economy targets for 2030 supported packaging transitions and mattress recycling capacity. The industry balanced affordability, innovation, and sustainability amid constrained household budgets.

Europe Furniture Industry Leaders

IKEA

Natuzzi S.p.A.

Poltrona Frau Group

Roche Bobois SA

BoConcept Holding A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: HNI Corporation completed its USD 2.20 billion acquisition of Steelcase Inc., creating a combined entity with USD 5.80 billion in pro-form annual revenue and USD 120 million run-rate cost. Collaboration at maturity, and S&P Global Ratings assigned a BB+ issuer credit rating with a stable outlook.

- November 2025: Ingka Group reported FY2025 retail sales of EUR 39 billion(USD 45.87 billion), with store visitation up 1.3% and online share rising to 30%, and the group committed over EUR 4.2 billion(USD 4.94 billion) toward a EUR 7.5 billion(USD 8.82 billion) renewable energy target by 2030.

- September 2025: JYSK posted a record turnover of DKK 46.3 billion(USD 7.29 billion) with 148 new stores opened across Europe and Africa, and 303 store activities to update to the latest concept, bringing the network to 3,500+ stores in 50 countries.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European furniture market as all movable articles meant for residential, commercial, and institutional use that are sold new within Europe, measured in manufacturer-level revenue (USD). Items range from ready-to-assemble wardrobes to contract-grade seating and workstations; the scope mirrors the harmonized CN94 customs codes and Eurostat PRODCOM classes to ensure exhaustive coverage.

Scope Exclusion: Built-in cabinetry and other fixtures permanently integrated during construction are not included.

Segmentation Overview

- Market Size & Growth Forecasts (Value)

- By Application

- Home Furniture

- Chairs

- Tables (side tables, coffee tables, dressing tables, etc.)

- Beds

- Wardrobes

- Sofas

- Dining Tables/Dining Sets

- Kitchen Cabinets

- Other Home Furniture (bathroom furniture, outdoor furniture, etc.)

- Office Furniture

- Chairs

- Tables

- Storage Cabinets

- Desks

- Sofas and Other Soft Seating

- Other Office Furniture

- Hospitality Furniture

- Educational Furniture

- Healthcare Furniture

- Other Applications (educational furniture, medical and non-medical furniture, public places, retail malls, etc.)

- Home Furniture

- By Material

- Wood Furniture

- Metal Furniture

- Plastic & Polymer Furniture

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B /Project

- B2C/Retail

- By Geography

- Germany

- France

- Italy

- Spain

- United Kingdom

- BENELUX

- NORDICS

- Rest of Europe

- By Application

Detailed Research Methodology and Data Validation

Primary Research

Interviews and online surveys with furniture producers, channel buyers, design consultants, and logistics specialists across Germany, Italy, Spain, the Nordics, and CEE markets helped validate discount structures, average selling prices, e-commerce mix shifts, and post-COVID renovation demand patterns, ensuring that desk-based findings aligned with on-ground realities.

Desk Research

We first built a foundational dataset from freely accessible tier-1 sources such as Eurostat PRODCOM unit shipments, EU Construction Output Index, UN Comtrade trade flows, and the European Federation of Furniture Manufacturers' production bulletins. National statistics offices, ECB household-spending tables, and industry journals like Wood Furniture Europe provided price trends and raw-material cost curves. To profile company financials and screen press releases, D&B Hoovers and Dow Jones Factiva, two of Mordor's paid repositories, were tapped. This multi-source canvas enabled us to map apparent consumption, benchmark import penetration, and flag anomalies. The sources cited here are illustrative; many additional publications, databases, and regulatory filings informed our desk work.

Market-Sizing & Forecasting

A top-down "apparent consumption" model (production + imports - exports) set the 2024 baseline, which was then cross-checked through selective bottom-up supplier roll-ups of sampled ASP times volume for key product families. Core drivers, housing completions, renovation outlays, office vacancy rates, household real income, and EU timber and steel price indices feed a multivariate regression that projects value through 2030. Where bottom-up gaps emerged (e.g. sparse data for micro-brands), interpolation followed by expert review bridged the variance.

Data Validation & Update Cycle

Outputs pass dual-analyst reviews; variance thresholds trigger re-checks against external series, and any deviation above +/-4 % prompts respondent call-backs. Reports refresh annually; interim updates occur after material events such as sudden tariff shifts or major building permit revisions.

Why Mordor's Europe Furniture Baseline Commands Credibility in Europe

Published figures often diverge because each firm tweaks market boundaries, applies different ASP ladders, or freezes currency rates at varying points. By anchoring estimates to Eurostat production codes and reconciling them with live trade and price signals before layering scenario assumptions, Mordor Intelligence delivers a middle-path baseline that boards can replicate and trust.

Taken together, the comparison shows that scope breadth, refresh cadence, and triangulation depth drive the spread; Mordor's disciplined blend of harmonized codes, timely primary checks, and balanced forecasting keeps our number both transparent and dependable for strategic planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 262.0 B (2025) | Mordor Intelligence | - |

| USD 222.0 B (2024) | Global Consultancy A | Excludes contract furniture, relies on household spend surveys only |

| USD 174.9 B (2022) | Industry Advisory B | Older base year, inflation adjustments absent, omits online-only sellers |

| EUR 165.0 B (2024) | Trade Journal C | Retail sales focus; excludes factory gate values and B2B project orders |

Taken together, the comparison shows that scope breadth, refresh cadence, and triangulation depth drive the spread; Mordor's disciplined blend of harmonized codes, timely primary checks, and balanced forecasting keeps our number both transparent and dependable for strategic planning.

Key Questions Answered in the Report

What is the size and growth outlook of the European furniture market?

The European furniture market size is projected to grow from USD 277.21 billion in 2026 to USD 358.26 billion by 2031 at a 5.26% CAGR, supported by renovation programs, hybrid work, and demographic demand.

Which applications are leading and which are growing fastest in Europe?

Home furniture led with a 57.87% share in 2025, and office furniture is the fastest-growing application with a 6.72% CAGR through 2031 as firms redesign for hybrid work.

Which materials will gain the most momentum in Europe by 2031?

Wood remains the largest material with a 51.87% share in 2025, while plastics and polymers are expected to grow fastest at a 6.38% CAGR due to circular design mandates.

How are channels shifting across the region?

B2C or retail remains dominant with a 74.35% share in 2025 and a 7.33% CAGR outlook, while omnichannel and OSS VAT simplify cross-border e-commerce and improve online shares in major markets.

Which country is expanding the fastest in Europe?

Spain is the fastest-growing geography with a projected 6.98% CAGR through 2031, driven by housing activity and tourism-led hotel renovations.

How concentrated is competition in European furniture?

The market is fragmented with a long tail of regional producers, and leaders focus on affordability, omnichannel capabilities, and sustainability-led investments to defend share.

Page last updated on: