Hardwood Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.18 Trillion |

| Market Size (2031) | USD 1.46 Trillion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hardwood Market Analysis by Mordor Intelligence

The Hardwood Market size is projected to expand from USD 1.12 trillion in 2025 and USD 1.18 trillion in 2026 to USD 1.46 trillion by 2031, registering a CAGR of 4.35% between 2026 and 2031. Expansion is being fueled by renovation cycles in the United States and Europe and by green-building programs that favor certified hardwood in mass-timber and interior scopes. Competitive pressure from resilient formats has pushed leading brands to enhance engineered hardwood with improved moisture performance, modern locking systems, and upgraded factory finishes to protect mid-tier demand. Design preferences are moving toward natural looks, with white oak anchoring specifications and walnut gaining traction in premium furniture and millwork as buyers seek darker tones and authentic grain. Producers are investing in densification and thermal modification to improve durability and installation speed while positioning around evolving trade and traceability requirements. Regionally, North America remains a major revenue base tied to remodeling cycles, and Asia-Pacific continues to expand on export furniture platforms in China and Vietnam, with rising consumption in India.

Key Report Takeaways

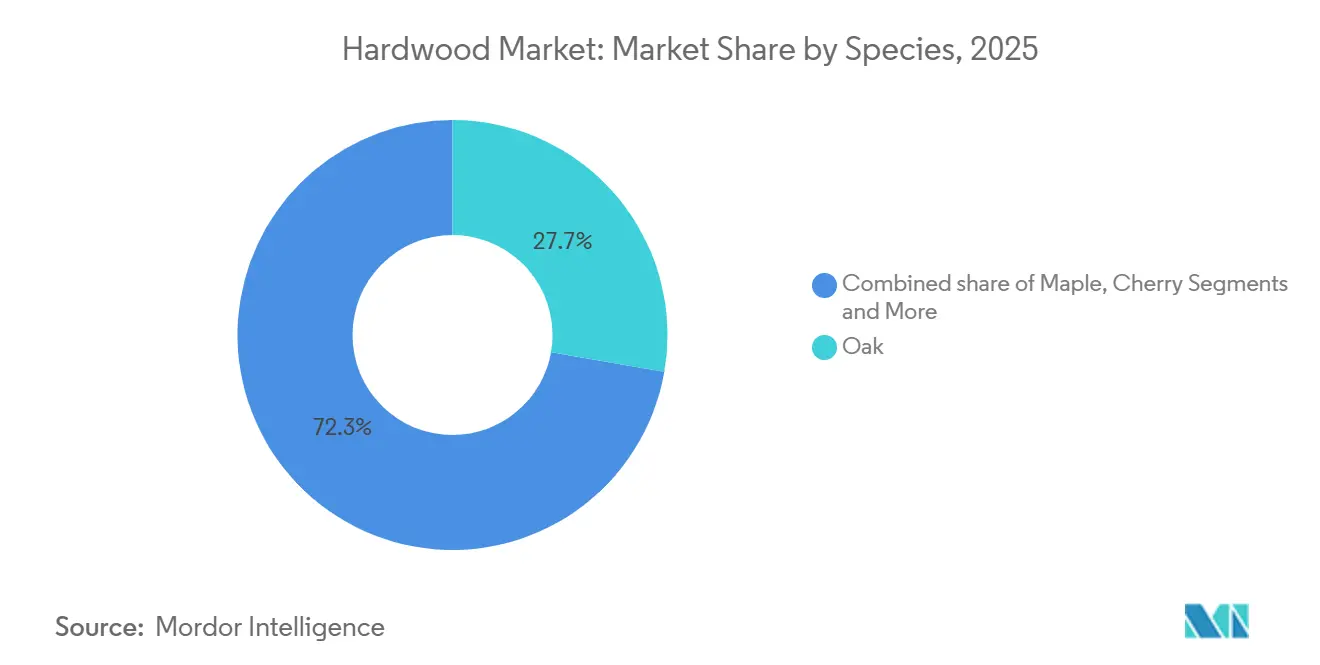

- By species, white oak led with 27.74% share in 2025 in the hardwood industry, while walnut is projected to expand at 5.71% CAGR through 2031.

- By application, flooring accounted for a 34.61% share in 2025 in the hardwood market, while construction recorded the highest projected CAGR at 4.83% through 2031.

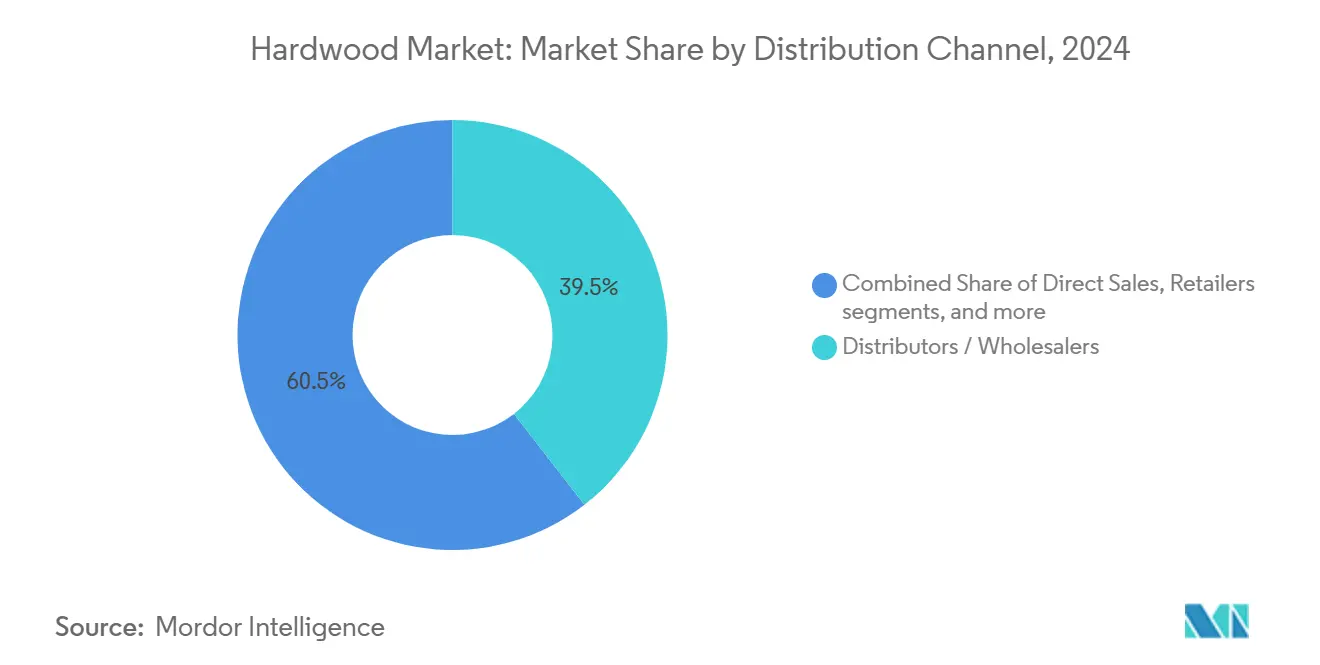

- By distribution channel, distributors and wholesalers held a 39.48% share in 2025 in the hardwood market, while retailers are projected to grow at 5.12% CAGR through 2031.

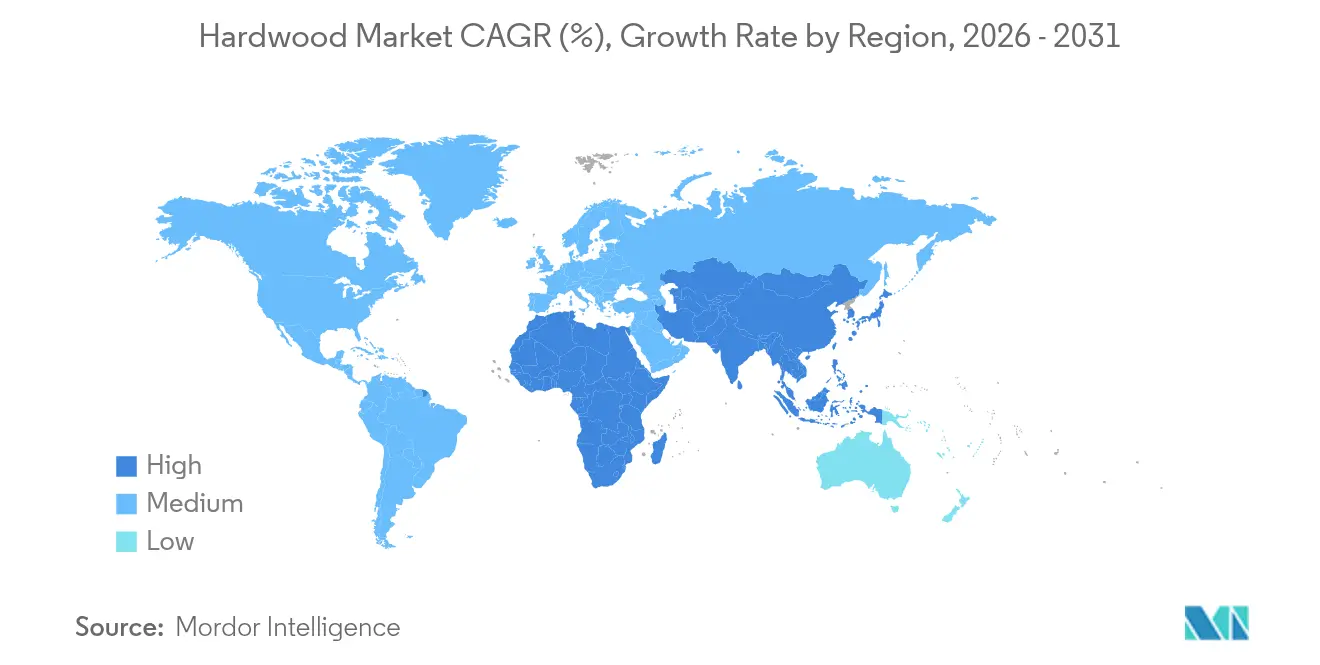

- By geography, North America captured a 36.55% share in 2025 in the hardwood industry, while Asia-Pacific is forecast to advance at a 5.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Hardwood Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation-led replacement cycles in residential and commercial interiors | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Premiumization toward natural hardwood aesthetics and durability | +0.9% | North America, Europe, and the Asia-Pacific urban centers | Long term (≥ 4 years) |

| Asia-Pacific furniture and joinery export engine pulling temperate hardwood demand | +0.8% | China, Vietnam, and India, with spillover to global trade | Medium term (2-4 years) |

| Thermally modified hardwoods expand into exterior applications | +0.6% | Europe and North America | Long term (≥ 4 years) |

| Green building programs broaden acceptance of certified hardwood | +0.5% | Europe, North America | Long term (≥ 4 years) |

| EUDR-ready traceability and low deforestation-risk temperate hardwoods | +0.4% | European Union markets, indirect United States and Canadian supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renovation-led replacement cycles in residential and commercial interiors

Residential remodeling in the United States stabilized after a slower 2024 and is expected to lift as interest-rate cuts improve affordability, with over 60% of National Wood Flooring Association members anticipating sales gains as deferred kitchen and flooring work resumes[1]National Wood Flooring Association, “Contractor and Retailer Outlook 2025,” Hardwood Floors Magazine, hardwoodfloorsmag.com. The replacement-on-ownership-transfer pattern remains an important catalyst, and the hardwood market benefits when existing-home transactions normalize since these projects carry larger ticket sizes than routine refresh cycles. Commercial interiors are adding demand through tenant improvement programs tied to office reconfigurations and return-to-work policies, with healthcare and education projects favoring easy-to-clean, durable finishes that align with post-pandemic standards. Installation practices also shape product choices since prefinished engineered lines shorten job timelines and reduce site disruption, which supports further mix shift toward factory-finished products in multi-family and commercial settings. Cycle length differs by property type, with hospitality refreshes running faster than typical residential lifecycles, so sustained growth depends on broad project coverage rather than a single category upswing.

Premiumization toward natural hardwood aesthetics and durability

Price signals in 2025 reflect a pivot to higher-end looks and species, with black walnut stumpage in Kentucky showing strong gains for medium-grade logs as furniture and millwork brands diversify away from a white-oak-dominant palette. Rift-sawn and quarter-sawn white oak command retail premiums versus commodity grades due to uniform grain and visual consistency valued in architecture and custom millwork. Engineered hybrids with 3-4 mm veneers seek the look of solid planks at lower weight and improved moisture stability, and upgrades such as drop-lock systems and extended wet-resistance warranties aim to limit substitution by rigid-core products. Buyers now research Janka hardness, finish chemistry, and grain patterns before purchase, which benefits species with clear performance narratives and distinctive aesthetics, and rewards brands that communicate provenance and refinishability. Regulatory pressures from formaldehyde emission rules and EPA testing support a premium for domestic production that advertises low-VOC finishes and compliance transparency in the hardwood industry.

Asia-Pacific furniture and joinery export engine pulling temperate hardwood demand

China and Vietnam continue to pull temperate hardwoods into export-oriented furniture and joinery supply chains, with United States and European species used in frames, faces, and veneers for goods shipped to North America and Europe. Shifts in trade rules and phytosanitary restrictions are changing routes rather than destroying demand as Vietnamese sawmills increased re-exports to China in 2025 to serve buyers managing around a Chinese log-import ban. India is adding a long-term pull with hardwood imports rising over two decades and domestic furniture consumption projected to grow at double-digit rates through the late 2020s, which supports diversified sourcing and product tailoring for Indian urban households. Shipping disruptions in the Red Sea in late 2023 and early 2024 led to opportunistic volume shifts, with some North American suppliers gaining where European routes faced higher costs and delays. Export flows to China fluctuated in 2025, but absorption from Vietnam and India illustrates the region’s resilience and its ability to rebalance volumes within the hardwood market during periods of policy stress.

Thermally modified hardwoods expand into exterior applications

Thermally modified hardwoods are increasingly adopted in exterior applications such as decking, cladding, and outdoor structures due to enhanced durability, dimensional stability, and resistance to moisture, decay, and insects. Their ability to replace tropical hardwoods and chemical-treated wood supports sustainable construction, driving demand across global hardwood markets. These treatments open exterior applications such as decking, cladding, and outdoor furniture for temperate species by improving dimensional stability and rot resistance, which expands addressable demand for hardwood producers. Adoption is visible in European facade projects and in North American decking channels where installers cite predictable movement and extended service-life claims as key decision factors. Policy constraints on legacy preservatives provide a favorable backdrop, and marketing of “chemical-free” wood supports premium positioning in commercial and high-end residential projects. Processing adds cost, and penetration is concentrated in premium tiers, but scale, automation, and kiln efficiency gains are improving the economics over time for the hardwood industry.

Restraints Impact Analysis of Hardwood Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution from LVT/SPC/resilient flooring and laminates | -1.1% | Global, most acute in mid-price residential segments | Medium term (2-4 years) |

| Pest- and climate-driven species availability shocks (e.g., ash/EAB) | -0.7% | North America with wider spread of risk | Long term (≥ 4 years) |

| Compliance costs and documentation burden (EUDR, Lacey Act) | -0.5% | European Union importers, United States exporters | Short term (≤ 2 years) |

| Trade policy shocks and import bans/tariffs disrupt flows | -0.4% | United States-China-Vietnam corridors, Canada-United States disputes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Compliance costs and documentation burden (EUDR, Lacey Act)

The European Union Deforestation Regulation requires geolocation down to plot level for each harvest entering European Union markets by December 30, 2026, for large operators, which is a major challenge for the United States hardwood supply due to fragmented ownership across millions of parcels[2]Wisconsin Department of Natural Resources, “EUDR Requirements and U.S. Hardwood Sector Readiness,” Wisconsin DNR, dnr.wisconsin.gov. The TRACES system expects polygon or points coordinates for all sources included in a shipment, which is a larger administrative lift than Lacey Act declarations and collides with aggregated sourcing that characterizes many United States consignments. The American Hardwood Export Council’s American Hardwood Assured platform uses satellite imagery and risk models to deliver state-level assessments as a practical workaround, and independent audits have verified negligible risk for a wide set of states. The European Commission is scheduled to review simplification in April 2026, including potential acceptance of state-based risk assessments for low-risk determinations, which would reduce documentation friction if adopted. Penalties for non-compliance can go up to 4% of European Union turnover and include seizure and exclusion, which is prompting mills to adopt traceability tools ahead of final rule clarity and to test digital systems for chain of custody in the hardwood market.

Substitution from LVT/SPC/resilient flooring and laminates

Hardwood is ceding volume to rigid-core and resilient formats in mid-price residential segments such as SPC, and enhanced wear layers offer perceived waterproof and scratch-resistant advantages in rooms with moisture and pets. SPC products now dominate the LVP category by volume and keep improving visuals with digital printing, which narrows the aesthetic gap with real wood and limits upsell conversion for commodity hardwood lines. Industry surveys show a large share of wood-flooring professionals view wood-look products as the largest threat to real-wood sales, underscoring the importance of product education on refinishing and long-life performance. Major brands have diversified capacity into resilient to hedge exposure, which creates internal competition for capital and shelf space within companies that also sell hardwood. Counter-messaging in the hardwood market emphasizes provenance, refinishability, and indoor-air-quality advantages, but these attributes resonate most with design-conscious and higher-income buyers, keeping the mid-tier under pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Hardwood Market Segment Analysis

By Species:

Oak Commands Premiums, Walnut Gains MomentumOak led 2025 volumes with a 27.74% share, supported by demand for staves and by design preferences that favor tight grain and neutral tones in high-end interiors, which places white oak at the core of specification lists across flooring and architectural millwork. Walnut is the fastest-growing species with a 5.71% CAGR expected through 2031 as buyers embrace darker, rustic aesthetics in luxury furniture and whole-home statements, aided by improved finishing systems that preserve color fidelity. These two poles shape the hardwood market as project buyers compare solid and engineered options, weigh refinishability against moisture tolerance, and calibrate plank widths to room scale and lighting. Rift- and quarter-sawn cuts of white oak continue to earn premiums for visual uniformity, while character-grade looks support value engineering on larger surfaces without sacrificing natural appeal [3]. Maple and cherry retain distinct roles in cabinet and furniture lines where light palettes or warm tones are desired, even as incremental share accrues to white oak and walnut in visible applications.

Walnut’s growth vector is closely tied to premium price realization in furniture and tailored millwork that calls for consistent color and grain, which is prompting mills to increase veneer recovery for select logs and to focus on grade yield improvements. The hardwood market size for walnuts is projected to expand at 5.71% CAGR through 2031, which keeps the species central to product launches that target affluent remodels and boutique hospitality. White oak’s leadership is reinforced by broad application fit across flooring, cabinetry accents, and architectural features, and by a robust export position to markets that prioritize certified temperate species under strict procurement rules. Ash volumes remain constrained by pest pressure, which steers substitution toward oak variants or engineered faces that maintain a similar look, while buyers monitor price and availability before committing to new ash-heavy programs. Across species, the hardwood industry is aligning grade mix, slicing strategies, and drying protocols to serve both premium aesthetics and consistent factory performance in engineered formats.

By Application:

Construction Outpaces Flooring on Infrastructure PullFlooring accounted for 34.61% of 2025 consumption as remodeling and tenant improvements sustained replacement cycles, and as prefinished engineered formats captured more project scope because they reduce install time and job-site variability. Within floors, white oak dominates in narrow to wide planks and in patterned configurations such as herringbone and chevron for high-end spaces, with product lines adding water-tolerant cores to minimize callbacks in kitchens and entries. The segment’s maturity is visible in the rising share of factory-finished products, and in the way warranties and mechanical locking systems feature in buyer decisions at the upper mid-tier. Furniture remains a steady outlet, with Asia-Pacific export programs pulling temperate species, and with domestic brands using walnuts and oak to anchor premium catalogs. Decorative interior applications, including panels and accent millwork, highlight thermally modified options where exterior cladding is in play and where material health narratives support specification.

Construction is the fastest-growing application with a 4.83% CAGR projected through 2031 as mass-timber frame systems pair with certified hardwood for millwork and select structural elements in commercial and civic projects. The hardwood market size tied to construction benefits from LEED v5 and BREEAM pathways that reward chain-of-custody wood, which embeds certified hardwood into standard submittals for new builds and major retrofits. Industrial packaging and pallets offer a base load for lower-grade outputs that do not meet appearance specs, and they stabilize sawmill economics during slow periods for higher-value uses. Millwork such as trims, stair parts, and rails keeps poplar and red oak relevant in painted or utilitarian roles at value-engineered price points. As construction ramps up under climate targets and public procurement standards, the hardwood industry attracts specifiers who seek natural materials with audited origins and long service lives.

By Distribution Channel:

Retailers Gain Share as E-Commerce ExpandsDistributors and wholesalers held 39.48% share in 2025 as they aggregate output from fragmented mills and buffer inventory for contractors and OEMs, yet their dominance is tested as mills scale direct programs and as retailers expand digital assortments. Specialty flooring showrooms and big-box chains are increasing product education and sample access to support in-store conversion, while selecting e-commerce platforms build curated SKUs for smaller projects and tighter timelines. The hardwood market is also seeing mills deepen relationships with large furniture brands that buy multi-container lots directly to manage price and continuity in Asia-Pacific hubs. Channel conflict emerges when manufacturers run direct-to-builder or direct-to-consumer programs that undercut distributor paths for identical or closely related SKUs, which pressures traditional relationships. Specialty retailers that focus on reclaimed, certified, or exotic provenance maintain high margins by solving documentation needs and by curating aesthetics that align with sustainability stories.

Retailers are projected to grow at 5.12% CAGR through 2031 as omnichannel strategies blend physical showrooms with digital discovery and sample logistics, including delivered sample kits and AR tools that help visualize plank widths and finishes. The hardwood market size implications favor brands that provide complete room solutions with trims and transitions, bundled services, and post-installation care, which improves attachment rates and loyalty. Distributors will continue to play a vital role in regional inventory and in servicing smaller contractors, but differentiation will hinge on value-added services such as moisture testing, job-site consultation, and training. For mills, channel mix strategy now sits alongside species and product strategy as a key driver of margin stability across cycles. The hardwood industry is evolving its go-to-market approach to balance reach, speed, and unit economics amid rising compliance and logistics complexity.

Geography Analysis

North America Hardwood Market

North America captured 36.55% of 2025 hardwood revenue and remains anchored by the United States remodeling cycles, bourbon-barrel stave demand, and Canada’s export-oriented sawmill base that feeds both domestic and overseas buyers. Interest-rate paths influence the timing of remodeling upswings, and industry surveys signal improving expectations for 2026 as rates stabilize. Tariffs implemented in October 2025 on selecting softwood and finished wood products altered sourcing and pricing, which led some retailers to build inventory early and diversify supplier lists. Canadian exporters face EUDR documentation challenges like those of their United States peers when accessing European Union markets, and certified wood can earn premiums in risk-sensitive channels. The region is also active in innovation and capacity upgrades supported by public programs, including grants to large hardwood producers to install equipment that raises throughput while enabling more efficient forest management[4]U.S. Forest Service, “Wood Innovations Program 2025 Awards,” U.S. Forest Service, fs.usda.gov. The hardwood market in North America is therefore characterized by strong domestic demand, complex policy exposure, and steady moves to higher-value engineered product share.

Europe Hardwood Market

Europe is expanding certified hardwood use despite slower housing starts, with BREEAM and national procurement rules placing chain-of-custody near the center of project specifications for commercial and institutional buildings. The United Kingdom increased purchases of United States hardwood in early 2025 under stable trade relations, and London functions as an entry point for high-end engineered planks that move onward to continental buyers. The European Union’s April 2026 simplification review for EUDR will shape the documentation burden for United States and Canadian suppliers, which is why many exporters are testing state-level risk documentation aligned with association platforms. European brands with long engineering heritage continue to command premiums in the hardwood industry by pairing wider planks with brushed textures and by promoting certified sourcing. These specifications and brand strategies help sustain mid-to-high-tier demand even when new-build volumes are modest.

APAC Hardwood Market

Asia-Pacific is the fastest-growing region at 5.42% CAGR through 2031 as export furniture platforms in China and Vietnam absorb temperate species, and as Indian demand expands due to urbanization and income growth. China’s log-import policies and wider tariff dynamics have driven re-routing through Vietnam, where mills boosted hardwood re-exports to serve Chinese buyers managing compliance. India continues to scale imports and downstream processing for domestic and export markets, and buyers there face higher documentation demands from European customers that require Lacey and EUTR-style assurances. Southeast Asian mills differentiate with formaldehyde compliance and chain-of-custody credentials, which support access to higher-value orders. The hardwood market share tied to Asia-Pacific furniture and joinery programs remains sensitive to freight conditions and policy, yet the region shows the agility to keep material flowing to demand centers.

Competitive Landscape

Market structure in the hardwood market is highly fragmented. Producers have concentrated on densified and engineered properties that address scratch resistance and moisture tolerance while preserving natural appeal, which aligns with premiumization trends. AHF Products invested USD 30 million in 2024 to enhance densification technology and scanning systems, while also increasing control over domestic log supply through sawmill acquisitions. Mohawk advanced installation speed and water-tolerance features with its TecWood Enhanced line, and Shaw upgraded facilities aimed at premium visuals while broadening sourcing options to reduce tariff risk. These moves recognize the need to protect shares against resilient formats and to serve the upper mid-tier with tangible performance gains.

Traceability solutions are an expanding white space as EUDR and other policies increase documentation friction, and the American Hardwood Export Council’s risk platform offers state-level assessments to lower entry costs for mills that cannot build bespoke systems. Digital platforms that standardize geolocation capture and automate due-diligence statements are also moving into commercial use to compress compliance timelines for mid-sized mills. Producers with FSC or PEFC certifications are seeing premiums tighten as certification becomes a baseline requirement in public and private tenders, which raises barriers for non-certified entrants but compresses margins for incumbents. The hardwood market increasingly differentiates on verified provenance, third-party audits, and lifecycle impact claims that align with LEED v5 and BREEAM.

Public funding, M&A in adjacencies, and capacity localization also shape competition. United States Forest Service grants awarded in 2025 helped major hardwood companies add or upgrade equipment to increase recovery and reduce emissions, which supports regional jobs and healthier forest management. Flooring manufacturers have acquired rigid-core capacity and introduced broader accessory portfolios to offer complete room solutions, which improves attachment rates at retail and in builder programs. These strategies lead firms to balance cyclical headwinds and to maintain relevance in the hardwood market despite substitution pressures.

Hardwood Industry Leaders

NWH (Northwest Hardwoods)

Baillie Lumber / The Baillie Group

Danzer

Pollmeier Massivholz

Interholco (IFO)

- *Disclaimer: Major Players sorted in no particular order

Hardwood Market Companies Covered in this Report

- NWH (Northwest Hardwoods)

- Baillie Lumber / The Baillie Group

- Danzer

- Pollmeier Massivholz

- Interholco (IFO)

- Rougier Afrique International

- Precious Woods (CEB, Gabon)

- JAF Group

- James Latham plc

- Timbmet

- Bingaman & Son Lumber

- AHF Products

- Kährs Group

- Bauwerk Group / BOEN

- Indusparquet

- Power Dekor Group

- Mohawk Industries

- Shaw Industries

- Sumitomo Forestry

- Derr Flooring Co.

Recent Industry Developments in Hardwood Market

- February 2026: AHF Products introduced a select-grade, premium Hartco offering at Surfaces 2026, manufactured in Turney, Tennessee, featuring 7.5-inch-wide formats with 3mm top layers targeting high-end clientele seeking American-made engineered hardwood, and simultaneously launched Bruce Natural Reflections, a 5/16-inch-thick, 3.25-inch-wide plank exclusive to AHF.

- February 2026: Kährs expanded its Canvas collection with eight new colors and upgraded to a 7.375-inch-wide format, while enhancing its engineered Life Authentic line with longer planks, wire brushing, and herringbone availability.

- January 2026: Cali unveiled First Press, a premium European white oak collection completing the “Cali Hardwoods Trilogy,” aimed at affluent buyers who value curated aesthetics and story-driven assortments.

- October 2025: AHF Products acquired a rigid-core factory in Cartersville, Georgia, expanding its footprint beyond traditional hardwood into hybrid and resilient categories.

Global Hardwood Market Report Scope

Hardwood is derived from angiosperm trees, which are typically broad-leaved deciduous species. These trees are characterized by their slower growth rate, resulting in denser wood with more complex cell structures than softwoods.

The Hardwood Market is segmented by species, application, distribution channel, and geography. By species, the market is divided into oak, maple, cherry, walnut, mahogany, and others. By application, the market is categorized into flooring, furniture, construction, interior design & decoration, industrial packaging & pallets, millwork, and other applications. By distribution channel, the market is segmented into direct sales, distributors/wholesalers, and retailers (offline and online). Geographically, the market analysis covers North America, South America, Europe, Asia-Pacific, and the Middle East & Africa. In North America, the market includes the United States, Canada, and Mexico. In South America, the market covers Brazil, Peru, Chile, Argentina, and the Rest of South America. In Europe, the market includes the United Kingdom, Germany, France, Spain, Italy, BENELUX (Belgium, Netherlands, Luxembourg), NORDICS (Denmark, Finland, Iceland, Norway, Sweden), and the Rest of Europe. In the Asia-Pacific region, the market covers India, China, Japan, Australia, South Korea, Southeast Asia, and the Rest of the Asia-Pacific region. In the Middle East & Africa, the market includes the United Arab Emirates, Saudi Arabia, South Africa, Nigeria, and the Rest of the Middle East & Africa. The report provides market size and forecasts for the hardwood market in value (USD) across all the above segments.

Segmentation Overview

| Oak |

| Maple |

| Cherry |

| Walnut |

| Cherry |

| Mahogany |

| Others |

| Flooring |

| Furniture |

| Construction |

| Interior Design & Decoration |

| Industrial Packaging & Pallets |

| Millwork |

| Other Applications |

| Direct Sales |

| Distributors/Wholesalers |

| Retailers (Offline and Online) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Species | Oak | |

| Maple | ||

| Cherry | ||

| Walnut | ||

| Cherry | ||

| Mahogany | ||

| Others | ||

| By Application | Flooring | |

| Furniture | ||

| Construction | ||

| Interior Design & Decoration | ||

| Industrial Packaging & Pallets | ||

| Millwork | ||

| Other Applications | ||

| By Distribution Channel | Direct Sales | |

| Distributors/Wholesalers | ||

| Retailers (Offline and Online) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the hardwood market size in 2025, and how fast is it growing to 2031?

The hardwood market size is expected to grow from USD 1.12 trillion in 2025 to USD 1.18 trillion in 2026 and is forecast to reach USD 1.46 trillion by 2031 at a 4.35% CAGR over 2026-2031.

Which species are leading to growth, and why?

White oak led 2025 volumes with 27.74% share, while walnut is the fastest-growing at 5.71% CAGR through 2031 due to premiumization and preference for darker aesthetics in furniture and interiors.

What applications are most important for demand today?

Flooring holds the largest 2025 share at 34.61%, supported by remodeling and tenant improvements, while construction-linked use cases are growing faster on mass-timber adoption and green-building credits.

Which regions are growing fastest in hardwood consumption?

Asia-Pacific is the fastest-growing region at 5.42% CAGR to 2031 on strong furniture export platforms and rising domestic consumption, while North America remains the largest with 36.55% of 2025 revenue.

What policy or regulatory issues pose the highest near-term risk?

EUDR plot-level geolocation and documentation requirements by late 2026 are the most immediate risk for exporters to the European Union, and companies are adopting association-led risk platforms to navigate compliance.

How is the substitute from resilient flooring affecting hardwood demand?

Rigid-core products like SPC are compressing mid-price hardwood share due to waterproof and scratch-resistant claims, prompting hardwood brands to advance engineered performance features and provenance messaging.

Page last updated on: