3D Printed Unmanned Aerial Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

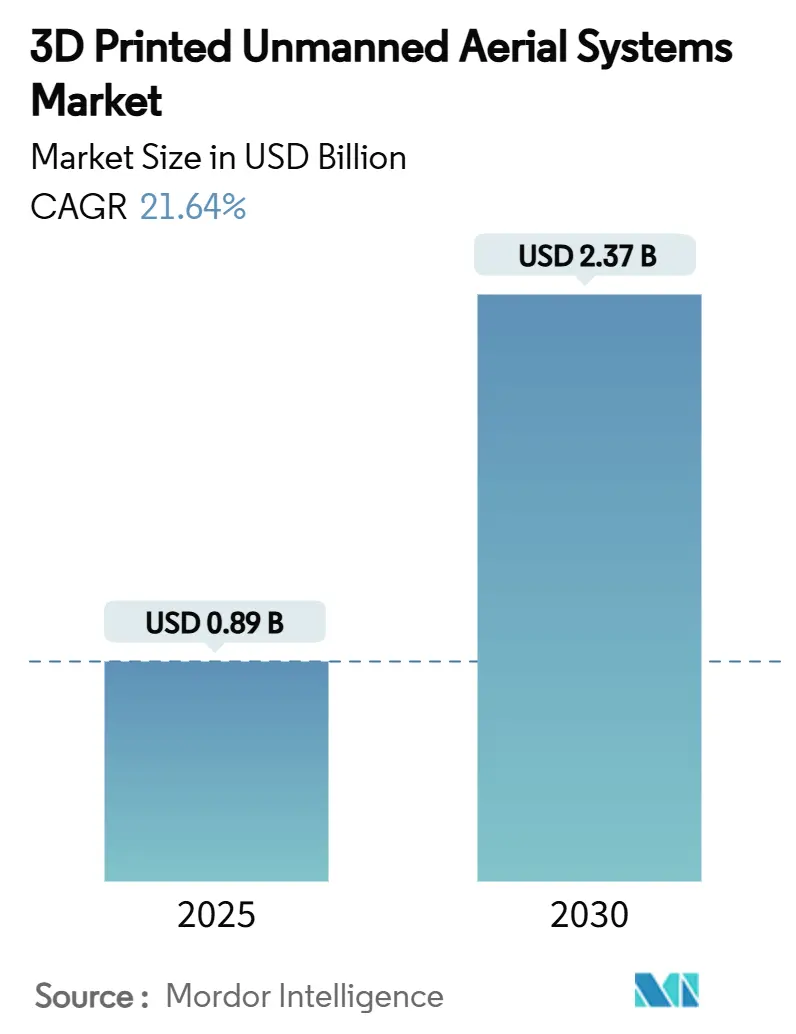

| Market Size (2025) | USD 0.89 Billion |

| Market Size (2030) | USD 2.37 Billion |

| Growth Rate (2025 - 2030) | 21.64% CAGR |

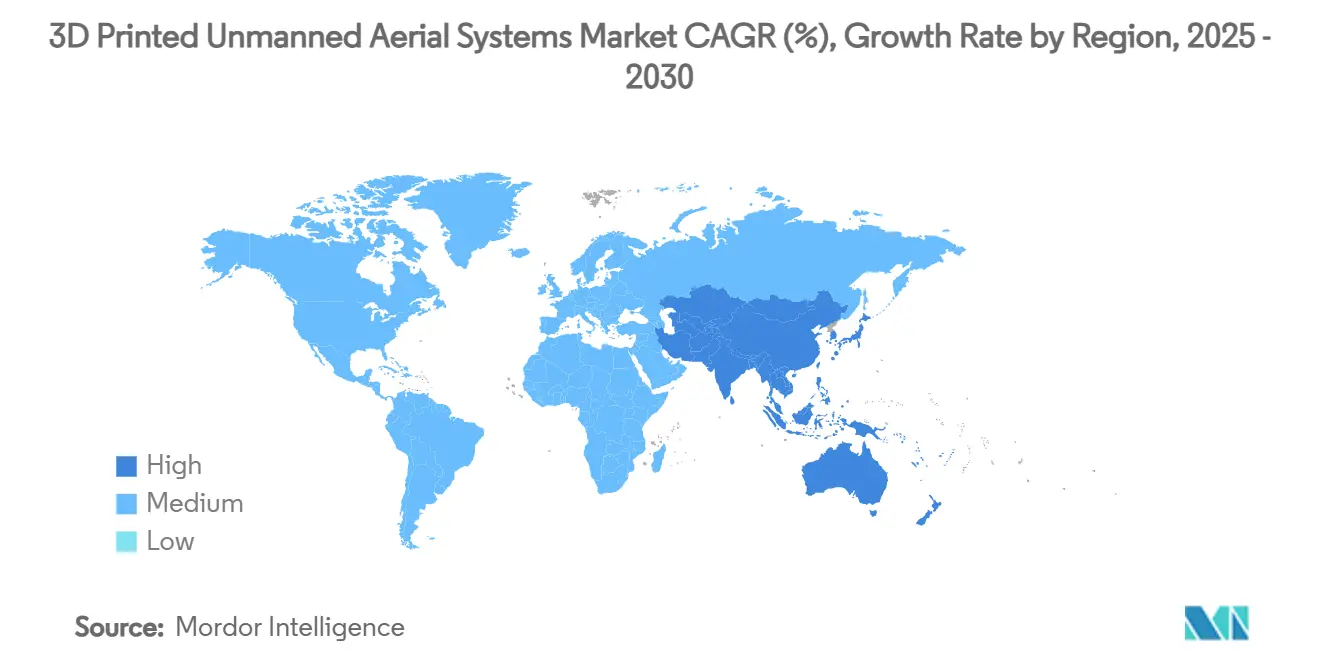

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

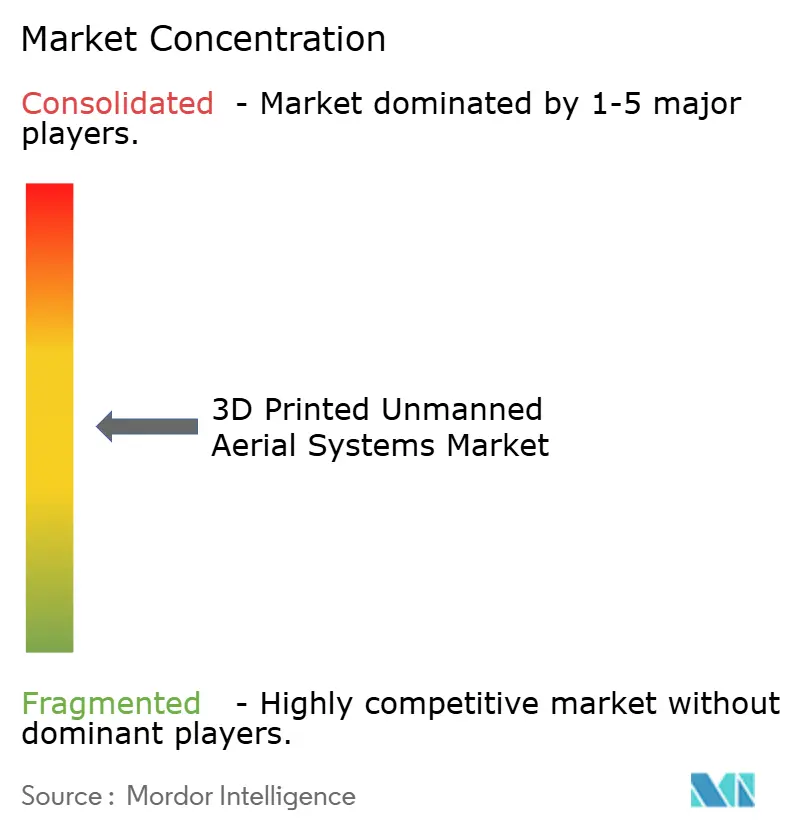

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Printed Unmanned Aerial Systems Market Analysis by Mordor Intelligence

The 3D-printed unmanned aerial systems (UAS) market size stands at USD 0.89 billion in 2025, is forecasted to reach USD 2.37 billion by 2030, and is projected to expand at a 21.64% CAGR over the period. This sharp growth trajectory reflects defense-driven demand for rapid prototyping, the rising volume of commercial UAS deployments, and the proven reliability of aerospace-grade additive manufacturing processes. The combination of field-deployable printers, increasingly mature regulatory guidance, and a widening portfolio of qualified metal and composite materials positions 3D printing as a mainstream production option rather than a niche prototyping tool. Military procurement plans now specify digital manufacturing workflows that allow components to be produced at the point of need, while commercial operators in agriculture, energy, and infrastructure inspection value the ability to commission low-volume, mission-specific airframes. Established aerospace primes are therefore integrating additive manufacturing lines into legacy facilities, and a new generation of vertically integrated start-ups is building entire airframes and propulsion systems around design freedoms that only additive processes can deliver.

Key Report Takeaways

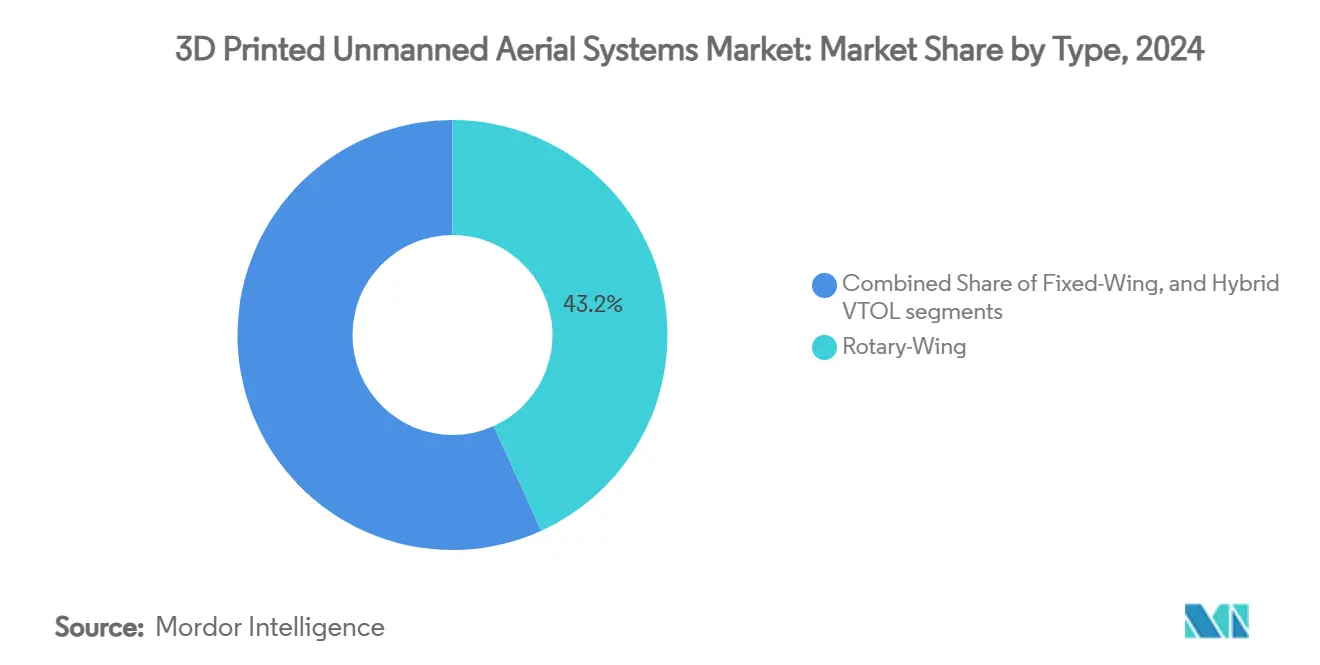

- By type, rotary-wing platforms led with a 43.22% share of the 3D-printed UAS market in 2024, while hybrid VTOL aircraft recorded the quickest expansion at a 27.35% CAGR to 2030.

- By manufacturing technique, material extrusion captured 47.28% of the 3D-printed UAS market in 2024, and power bed fusion is expected to advance at a 24.11% CAGR through 2030.

- By material, polymers commanded 51.90% of the 3D-printed UAS market share in 2024, whereas composite materials are set to register a 23.67% CAGR between 2025 and 2030.

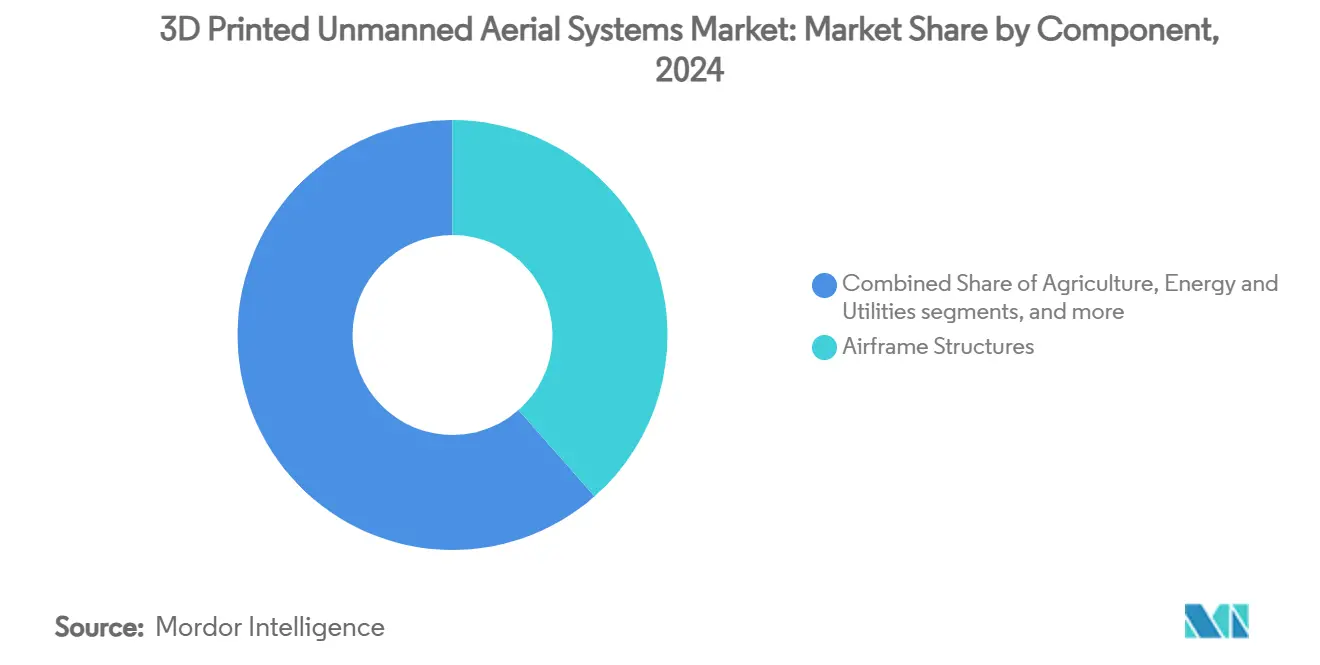

- By component, airframe structures accounted for 38.51% of the 3D-printed UAS market size in 2024, while payloads and sensors are projected to grow at a 25.76% CAGR through 2030.

- By end-use industry, military and security represented 46.85% of the 3D-printed UAS market in 2024; logistics and last-mile delivery are poised for a 23.81% CAGR to 2030.

- By geography, North America dominated with 42.67% of 2024 revenue, and Asia-Pacific is anticipated to post the fastest 25.95% CAGR over the forecast period.

Global 3D Printed Unmanned Aerial Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for lightweight and customizable airframes | +4.3% | North America, Europe, global spill-over | Medium term (2-4 years) |

| Reduced production costs and lead times enabled by additive manufacturing | +3.9% | Asia-Pacific hubs, global applicability | Short term (≤ 2 years) |

| Advancements in composite and continuous-fiber 3D printing technologies | +3.5% | North America, Europe, extending into APAC | Long term (≥ 4 years) |

| Increased investment in scalable and swarm-capable fleet production | +3.2% | North America, China, allied nations | Medium term (2-4 years) |

| Deployment of mobile 3D printing units for on-demand manufacturing in field environments | +2.6% | Conflict zones worldwide | Short term (≤ 2 years) |

| Emerging digital certification methods reducing regulatory hurdles for 3D-printed parts | +2.2% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lightweight and Customizable Unmanned Aerial Systems Airframes

Operators now expect mission-specific airframes delivered in days rather than months. The US Army’s mobile micro-factory initiative shows how field teams can print unique components overnight, reducing supply-chain exposure and cutting mass by up to 40% through lattice structures that conventional machining cannot achieve. Weight savings extend endurance, a critical metric for intelligence and surveillance sorties where battery improvements lag payload growth. French forces have validated the concept in active deployments, highlighting additive manufacturing’s shift from laboratory to battlefield acceptance. Therefore, the 3D-printed UAS market benefits directly from each new requirement for bespoke geometry and rapid turnaround.

Reduced Production Costs and Lead Times Enabled by Additive Manufacturing

Conventional tooling and minimum-order constraints once made small drone batches uneconomic. Beehive Industries’ propulsion program illustrates the reversal, shrinking engine part counts from 2,000 to 14 printed components and compressing build schedules from years to months.[1]Stephanie Hendrixson, “Beehive Industries Is Going Big on Small-Scale Engines,” Additive Manufacturing Media, additivemanufacturing.media Civil operators also capitalize: precision farming firms order seasonal nozzle configurations that classic injection molds cannot justify. Crucially, spare-part overhead drops when airframes and housings can be printed on demand, removing large inventory write-offs—an attractive proposition as fleets diversify.

Advancements in Composite and Continuous-Fiber 3D Printing Technologies

Thermoplastics alone rarely satisfy aerospace load cases. Continuous-fiber reinforcement allows printers to place carbon strands along specific stress paths, generating single-piece structures with joint-free integrity and weight parity versus legacy carbon lay-up. HP’s Windform family, qualified for wind-tunnel and flight articles, underpins this step-change. Regulatory progress follows: revised FAA guidance in 2025 references digital material pedigrees, signalling growing acceptance of composite additive solutions in critical parts.

Increased Investment in Scalable and Swarm-Capable Unmanned Aerial Systems Fleet Production

Distributed warfare concepts require hundreds of low-cost aircraft rather than a few exquisite platforms. The Pentagon’s Replicator program targets large volumes within 24 months, a timeline ideally matched to additive workflows that scale without bespoke tooling. Venture capital mirrors defense priorities by funding start-ups that combine autonomous software with vertically integrated printing facilities, aiming to produce diverse airframes from common digital baselines. Commercial sectors follow the template: multi-drone agricultural fleets rely on low-unit-cost custom designs that additive techniques readily supply.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of standardized aerospace certification for 3D-printed components | –1.7% | North America, Europe | Long term (≥ 4 years) |

| High material costs and limited print speed for mass-scale drone production | –1.5% | Global | Medium term (2-4 years) |

| Technical risks related to electromagnetic interference from embedded printed electronics | –1.1% | Global | Medium term (2-4 years) |

| Fragmented intellectual property environment limiting collaborative design innovation | –0.9% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardized Aerospace Certification for 3D-Printed Components

The US Federal Aviation Administration still requires part-by-part qualification for flight-critical components, offsetting the speed gains of additive fabrication. European regulators offer structured pathways, yet remain cautious around unfamiliar alloys and composites. Defense acquisition rules add further layers of testing, often extending full-rate production decisions by years. Manufacturers invest heavily in bespoke qualification regimes, a cost that smaller firms find prohibitive. Until harmonized test protocols and digital assurance schemes are firmly established, this restraint subtracts momentum from the otherwise fast-moving 3D-printed UAS market.

High Material Costs and Limited Print Speed for Mass-Scale Production

Aerospace-grade metal powders and advanced polymers can cost three to five times more than their conventionally processed equivalents, and high-quality power bed fusion cycles remain slower than machining for simple geometries. Post-processing—heat treatment, support removal, and surface finishing—adds labor and lead time. Although multi-laser architectures and in-process metrology have begun to narrow throughput gaps, the economic breakeven for massive production runs still favors casting or molding in many cases. Material supply chains are also immature, with limited qualified vendors controlling pricing power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hybrid VTOL Drives Next-Generation Capabilities

Rotary-wing models retained 43.22% of 2024 revenue owing to maneuverability in confined spaces and simple mechanical architectures well suited to additive build volumes. Fixed-wing UAS can command endurance-oriented civilian tasks such as farm mapping and pipeline inspection. The hybrid VTOL class, however, is on course for a 27.35% CAGR through 2030, reflecting the combined need for runway-free launches and long cruise ranges. 3D printing eliminates previous weight penalties by integrating tilt-mechanism housings, ducted fans, and complex transition structures in single builds. GE Aerospace’s hybrid-electric propulsion demonstrations highlight how additive heat exchangers and cable channels create efficient, structurally integrated nacelles. A consumer-grade VTOL prototype achieving a 130-mile range underscores the widening performance envelope now feasible for non-military buyers.[2]Kapil Kajal, “Beginner Develops 3D-Printed Drone,” Interesting Engineering, interestingengineering.com

Mission planners value hybrid VTOL platforms for ship-borne reconnaissance, mountain supply drops, and tactical resupply missions formerly reserved for helicopters. Precise thermal-management channels for batteries and power electronics are printed directly into airframes, removing heavy radiators. The resulting fuel or energy savings translate into longer endurance, enabling the same payload to travel farther without scaling up motors or cells. Service operators benefit from simplified maintenance because removable, additively produced nacelle shells house lift and cruise propellers, allowing rapid in-field replacement.

By Manufacturing Technique: Power Bed Fusion Gains Aerospace Acceptance

Due to inexpensive printers and an extensive polymer library, material extrusion dominated with 47.28% of 2024 sales. Its role as the workhorse of prototyping remains secure, especially for low-stress housings and jigs. Power bed fusion’s 24.11% forecast CAGR stems from defense and high-performance civil applications that require metallic strength at minimal mass. 3D Systems’ PSLA 270 and SLS 380 machines demonstrate cycle-time gains through multi-laser arrays and closed-loop powder management.

Print-once, fly-forever concepts gain traction as operators couple powder bed fusion with predictive digital inspection. Internal lattices tuned for specific vibration modes improve fatigue life, and conformal fuel channels free up external surfaces for payloads. Because multiple metal parts can be nested within one build chamber, procurement officers can order day-one spares without incurring additional tool changes, reducing per-unit cost curves. Combined with automated depowdering and heat treatment cells, powder bed fusion moves closer to series production economics for specialized fleets.

By Material: Composites Enable Aerospace-Grade Performance

Polymers led 2024 with a 51.90% share, due to ease of processing and cost efficiency. Composite grades, however, are forecast to grow at 23.67% CAGR as military and commercial buyers demand higher stiffness-to-weight ratios and embedded functional gradients. Continuous-fiber systems such as Windform allow single-piece wing skins that withstand battlefield loads while trimming fastener counts. CRP Technology’s work in carbon-fiber polyamide exemplifies this leap.

Metals address thermal and electromagnetic constraints, especially propulsion casings or shielded electronics bays. Advances in alloys optimized for low-temperature sintering reduce energy input, making aluminum-based powders viable for lightweight airframe skeletons. Bio-derived polymers gain European attention where end-of-life recyclability influences procurement, though limited mechanical performance confines them to low-stress pods. Designers will co-locate metallic inserts inside composite shells as multi-material printheads mature, delivering structural grounding for antennas without separate assembly steps.

By Component: Payloads Drive Integration Innovation

Airframe structures formed the cornerstone of 2024 revenue at 38.51%, reflecting the immediate weight and design gains unlocked by additive techniques. Propulsion benefited from complex internal cooling passages that boost thrust-to-weight ratios. Yet payloads and sensors will advance at a 25.76% CAGR during the forecast period. GA-ASI’s partnership with Divergent shows how integrated aero-structures reduce fasteners by 95% and simplify sensor mount alignments.

Multi-material deposition lets engineers build vibration isolators, EMI shields, and cooling ducts around optical or RF payloads within the same print cycle. Environmental-monitoring unmanned aerial systems take advantage of chemical detection chambers being embedded directly into wing roots, saving space for larger batteries. On the commercial front, last-mile delivery firms print customized cargo pods that match retailer packaging dimensions, avoiding the aerodynamic penalties of generic boxes. Such component-level innovations sustain premium pricing even as overall airframe prices trend down.

By End-Use Industry: Logistics Transforms Commercial Applications

Defense remained the principal buyer with 46.85% of 2024 spending, using additive manufacturing to replenish parts in austere theatres and to iterate prototypes well ahead of formal milestones. Agriculture applies remote-sensing unmanned aerial systems with 3D-printed spray-nozzle arrays that vary droplet size by crop species. Infrastructure inspection draws on corrosion-resistant housings and sensor gimbals tuned to bridge or wind-turbine geometries. Logistics, however, is positioned to disrupt volume dynamics through a 23.81% CAGR during the forecast period.

Retail and medical couriers test citywide unmanned aerial systems lanes, printing aerodynamic capsule shapes optimized for each payload profile. Regulatory advances that enable beyond-visual-line-of-sight flights accelerate these pilots, pushing demand for ultralight airframes. Consumer and prosumer segments feed innovation by refining open-source flight-controller housings and camera mounts that migrate into commercial offerings. Environmental agencies order purpose-built sensor arrays printed in weather-resistant composites, illustrating how bespoke design overcomes harsh field conditions.

Geography Analysis

North America generated 42.67% of 2024 revenue, underpinned by Pentagon budgets, NASA additive research programs, and a deep supplier ecosystem. The Replicator initiative sets multiyear demand for swarm-class unmanned systems, and partnerships such as GE Aerospace with Kratos on affordable small engines cement the region’s leadership. Mobile printer deployments aboard naval vessels and forward operating bases further mainstream the concept of in-theatre manufacturing. Canada’s Arctic surveillance UAS draw on cold-rated polymer blends, while Mexican assembly hubs integrate printed subcomponents into cost-competitive export models.

Asia-Pacific is the fastest climber with a 25.95% CAGR. China leads civilian unit volumes and invests in indigenous metal-powder supply chains to reduce import dependence. Japan and South Korea leverage precision robotics and material-science prowess to qualify high-temperature composites. India’s Make-in-India defense policy funds locally printed reconnaissance UAS, while Australia tailors modular sensor pods for mining-site mapping. Cost advantages and expanding technical capability allow APAC firms to challenge Western incumbents, broadening the global 3D-printed UAS market.

Europe holds a significant share through its mature aerospace cluster and clear regulatory roadmap. EASA’s structured framework attracts investment into certified polymer and metal lines. Germany fuses automotive and aerospace additive competencies, the United Kingdom pushes hybrid-electric VTOL demonstrators, and France field-tests portable battlefront printers. Environmental mandates encourage bio-based feedstocks and energy-efficient print cells, providing a sustainability angle that differentiates European offerings in government tenders.

Competitive Landscape

The 3D-printed UAS market shows moderate concentration. The Boeing Company, Airbus SE, and Lockheed Martin Corporation each operate in-house additive centers while partnering with material and printer specialists such as Stratasys and 3D Systems to accelerate throughput. These collaborations let incumbents protect core intellectual property while outsourcing rapid iteration. Stratasys Ltd. positions its high-temperature FDM line for aerospace tooling, whereas 3D Systems tailors SLA resins for wind-tunnel scale models showcased at RAPID + TCT 2025.

Beehive Industries exemplifies the vertically integrated disruptor, unveiling jet engines composed of 14 printed parts that lower acquisition cost for expendable UAS.[3]Beehive Industries, “Beehive Industries Introduces Frenzy Engine Family,” Beehive Industries, beehive-industries.com Divergent Technologies supplies AI-driven topology optimization and adaptive production systems, forming fully assembled tail-booms and wing structures in hours. Smaller entrants target niche payload solutions, merging sensor development, additive manufacturing, and data analytics services into turnkey packages for environmental agencies or smart-city operators.

Intellectual-property fragmentation shapes strategic moves. Primes acquire material startups to lock down supply and certification data, while independent bureaus form patent pools to negotiate cross-licenses. The result is a dynamic landscape where technology and design rights influence merger-and-acquisition timing as much as revenue multiples.

3D Printed Unmanned Aerial Systems Industry Leaders

General Atomics

The Boeing Company

AeroVironment, Inc.

Parrot Drones SAS

Stratasys, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Firestorm Labs secured a USD 100 million five-year Indefinite Delivery, Indefinite Quantity (IDIQ) contract with the US Air Force. The company will accelerate the development and production of modular, cost-effective 3D printed UAS, enabling flexible deployment for military operations in critical environments.

- October 2024: The US Air Force awarded Beehive Industries a USD 12.4 million contract to produce engines for UAS. The company will execute this contract with the University of Dayton Research Institute (UDRI).

Global 3D Printed Unmanned Aerial Systems Market Report Scope

| Fixed-Wing |

| Rotary-Wing |

| Hybrid VTOL |

| Material Extrusion |

| Polymerization |

| Power Bed Fusion |

| Others |

| Polymers |

| Metals |

| Composites |

| Others |

| Airframe Structures |

| Propulsion Systems |

| Payloads and Sensors |

| Control Electronics |

| Spare Parts and Accessories |

| Defense and Security |

| Agriculture |

| Logistics and Last-Mile Delivery |

| Construction and Infrastructure Inspection |

| Energy and Utilities |

| Environmental Monitoring |

| Consumer and Prosumer |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Fixed-Wing | ||

| Rotary-Wing | |||

| Hybrid VTOL | |||

| By Manufacturing Technique | Material Extrusion | ||

| Polymerization | |||

| Power Bed Fusion | |||

| Others | |||

| By Material | Polymers | ||

| Metals | |||

| Composites | |||

| Others | |||

| By Component | Airframe Structures | ||

| Propulsion Systems | |||

| Payloads and Sensors | |||

| Control Electronics | |||

| Spare Parts and Accessories | |||

| By End-Use Industry | Defense and Security | ||

| Agriculture | |||

| Logistics and Last-Mile Delivery | |||

| Construction and Infrastructure Inspection | |||

| Energy and Utilities | |||

| Environmental Monitoring | |||

| Consumer and Prosumer | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected CAGR for the 3D Printed Unmanned Aerial Systems market between 2025 and 2030?

The market is forecasted to grow at a 21.64% CAGR over the forecast period.

Which Unmanned Aerial Systems type is expanding the fastest?

Hybrid VTOL platforms are set to advance at a 27.35% CAGR through 2030, outpacing rotary- and fixed-wing categories.

Why is Asia-Pacific the highest-growth region?

China’s large civilian UAS base, regional military modernization, and expanding additive manufacturing supply chains push Asia-Pacific toward a highest-growth region.

What manufacturing technique is gaining aerospace acceptance?

Power bed fusion is moving rapidly into certified production, projected to rise at a 24.11% CAGR owing to its ability to deliver metal parts with near-wrought properties.

How are propulsion systems benefiting from 3D printing?

Companies such as Beehive Industries have reduced jet-engine part counts by over 95%, delivering lighter, cheaper, and faster-to-produce engines suitable for expendable UAVs.

What is the main regulatory hurdle for additive-manufactured Unmanned Aerial Systems parts?

A lack of standardized aerospace certification requires component-specific qualification, extending approval timelines especially for flight-critical metallic structures.

Page last updated on: