Inflation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

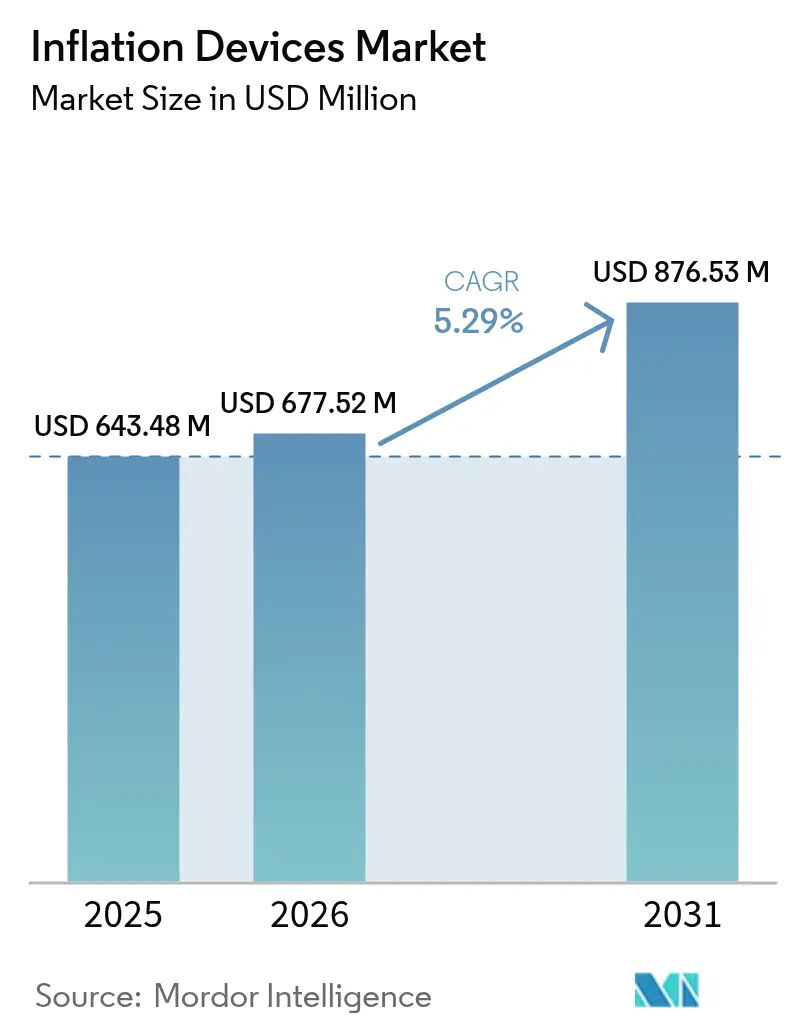

| Market Size (2026) | USD 677.52 Million |

| Market Size (2031) | USD 876.53 Million |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

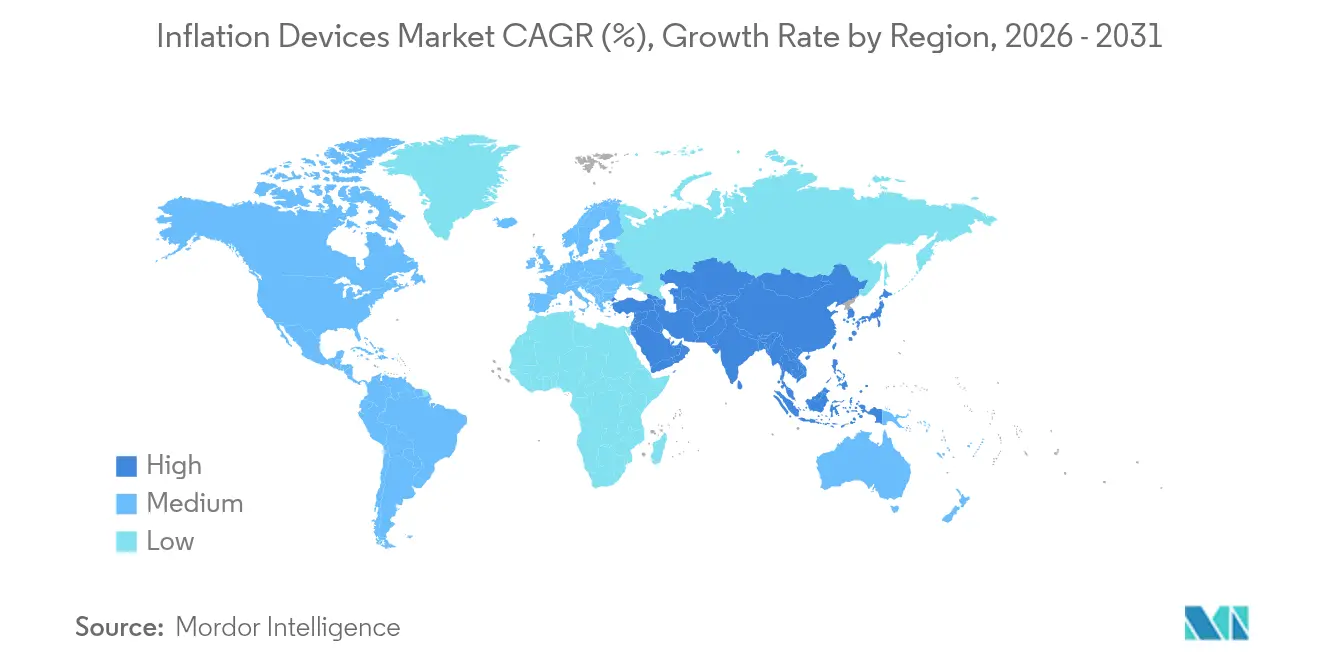

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inflation Devices Market Analysis by Mordor Intelligence

The Inflation devices market size is expected to grow from USD 643.48 million in 2025 to USD 677.52 million in 2026 and is forecast to reach USD 876.53 million by 2031 at 5.29% CAGR over 2026-2031. This outlook demonstrates the ability of the Inflation devices market to adapt to aging-population pressures, a heavier cardiovascular disease burden, and the rapid shift of catheter procedures into outpatient settings. Persistently high shipping, labor, and raw-material expenses—exacerbated by geopolitical tensions—compel manufacturers to re-engineer logistics footprints and invest 3–5% of revenue in supply-chain services. At the same time, digital pressure-sensing consoles are moving from optional add-ons to mandatory procurement criteria as providers chase data for quality metrics, while ambulatory surgical centers (ASCs) expand procedure volumes on the back of Medicare's USD 6.8 billion spend in 2023, representing an 11.5% increase from the previous year's USD 6.1 billion Medicare Payment Advisory Commission.

Key Report Takeaways

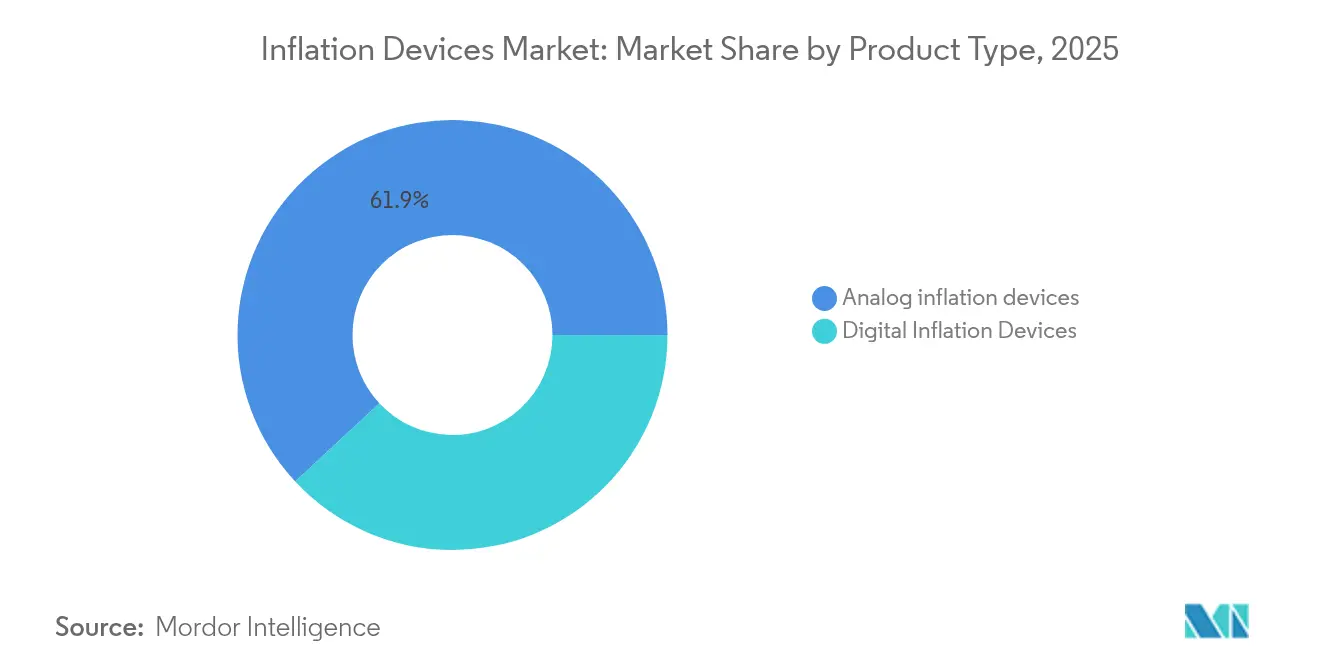

- By product type, analog inflation devices held 61.94% of Inflation devices market share in 2025; digital inflation devices are advancing at a 6.15% CAGR through 2031.

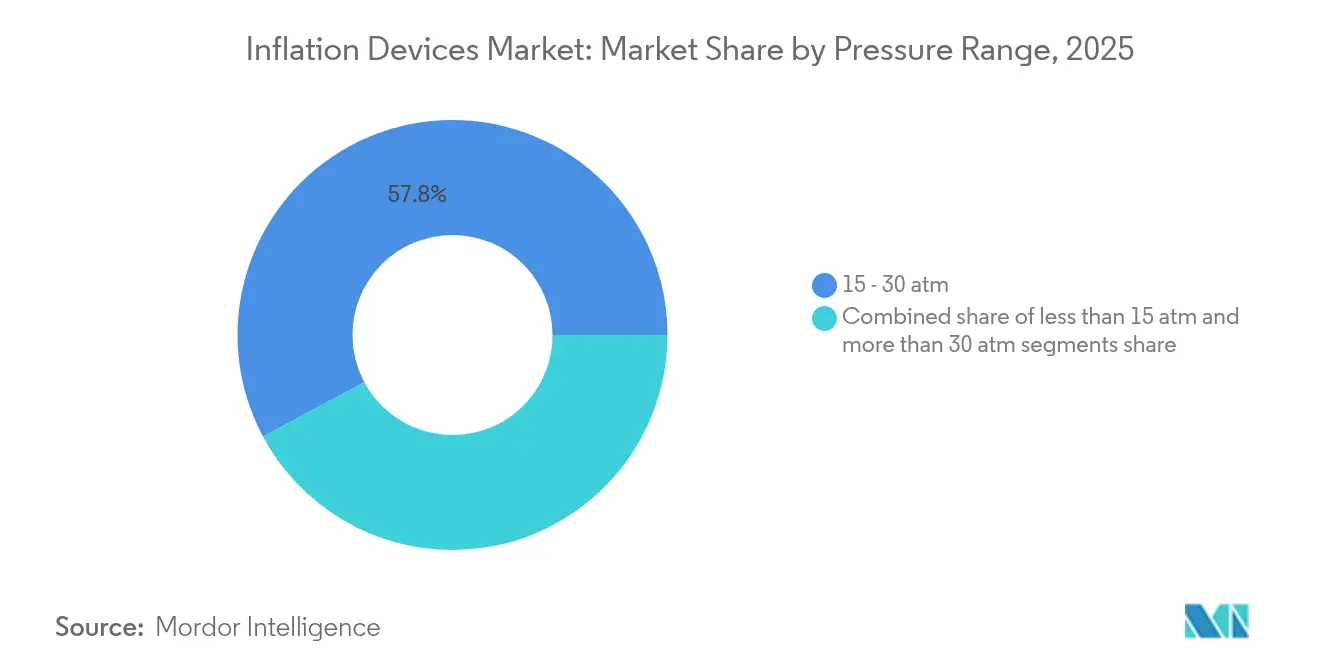

- By pressure range, the 15–30 atm segment accounted for 57.82% of Inflation devices market size in 2025 and is projected to expand at 7.54% CAGR to 2031.

- By application, coronary angioplasty generated 43.92% of Inflation devices market size in 2025, while neurovascular procedures post the quickest 6.38% CAGR through 2031.

- By end user, hospitals captured 53.15% of Inflation devices market share in 2025; ASCs deliver the fastest 6.83% CAGR through 2031.

- North America remained the largest geography at 41.95% of the Inflation devices market in 2025, whereas Asia-Pacific records a 7.06% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inflation Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular & peripheral arterial diseases | +1.2% | Global, with higher impact in North America & Europe | Long term (≥ 4 years) |

| Growth in minimally-invasive angioplasty procedures | +0.9% | Global, led by North America & Asia-Pacific | Medium term (2-4 years) |

| Favourable reimbursement reforms for catheter-based interventions | +0.7% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration of digital pressure-sensing & data logging in inflation devices | +0.6% | North America & Europe, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Adoption in neurovascular & structural-heart interventions | +0.5% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Shift toward single-use sterile inflation devices for infection control | +0.4% | Global, accelerated in post-pandemic healthcare settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of cardiovascular & peripheral arterial diseases

Ischemic-heart-disease patients in the United States are projected to top 29 million by 2060. This demographic surge underpins recurrent demand in the Inflation devices market, particularly for units rated 15–30 atm that now satisfy 58.27% of global requirement. Hospitals are scaling cath-lab capacity and choosing pumps that offer granular pressure control and temperature-stable gauges, positioning suppliers with robust, intuitive designs to win high-value contracts in aging economies.

Growth in minimally-invasive angioplasty procedures

FDA clearance of the AGENT Paclitaxel-Coated Balloon Catheter, which cut major adverse events 11.1% at 12 months, illustrates innovation’s role in expanding case volumes. ASCs, buoyed by double-digit Medicare spending growth, prioritize rapid device setup and digital monitoring. In response, manufacturers of the Inflation devices market roll out consoles with auto-inflation algorithms to streamline same-day discharge protocols.

Favourable reimbursement reforms for catheter-based interventions

CMS lifted the Physician Fee Schedule Conversion Factor 2.93% for 2024. New HCPCS codes covering dynamic balloons clarify billing, easing premium-device adoption. Parallel liberalization in India aligns local standards with EU MDR requirements. Collectively these shifts improve cash-flow visibility, encouraging providers to upgrade within the Inflation devices market to data-rich, digitally logged platforms.

Integration of digital pressure-sensing & data logging

Next-generation Wheatstone-bridge sensors achieve 460.1 kPa-1 sensitivity while bypassing temperature calibration. Wireless modules export real-time readings to electronic records, aligning with FDA change-control guidance and aiding post-market surveillance. As a result, procurement committees increasingly mandate digital readiness, driving the Inflation devices market toward sensor-centric value propositions.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High average selling price of digital inflation devices | -0.8% | Global, with higher impact in price-sensitive markets | Medium term (2-4 years) |

| Stringent Class III regulatory pathway in key markets | -0.6% | North America & Europe, expanding globally | Long term (≥ 4 years) |

| Supply-chain vulnerability for precision pressure gauges & syringes | -0.5% | Global, with concentration in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Growing catheter designs that eliminate separate inflation devices | -0.4% | North America & Europe, with spillover to developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High average selling price of digital inflation devices

Digital consoles list 30–40% higher than analog pumps, limiting uptake where hospital margins remain thin. Cost-of-ownership assessments—which include calibration, software, and training—may widen that gap. Analogue pumps therefore persist in emergency carts, tempering growth in the premium tier of the Inflation devices market.

Stringent Class III regulatory pathway in key markets

Premarket approval demands extensive data and rising user fees; FY 2025 FDA rates increased again. Smaller innovators find global launches in the Inflation devices market financially daunting, slowing disruptive entries and preserving incumbent dominance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: digital integration drives premium segment growth

Analog pumps generated 61.94% of the Inflation devices market in 2025, favored for reliability and low unit cost. High-volume hospitals continue to buy analog because technicians already master the workflow. Still, digital devices are projected to add USD 131.6 million by 2031 on a 6.15% CAGR as centers seek audit-ready data capture. Wireless consoles that log every inflation-deflation cycle satisfy accreditation mandates, raising switching incentives inside the Inflation devices market.

Digital systems integrate pressure graphs, auto-adjust algorithms, and remote diagnostics, slashing biomedical engineer call-outs. Trade-in credits and leasing plans dilute sticker shock, enabling independent ASCs to leapfrog older technology. Although analog remains entrenched, the strategic direction inside the Inflation devices market points to data-centric platforms becoming the reference standard.

By Application: neurovascular momentum accelerates adoption

Coronary angioplasty still dominates volume, but neurovascular interventions register the fastest CAGR at 6.38%. Micro-profile pumps capable of fractional-atmosphere increments are in high demand among neuro-interventionalists, highlighting the expanding technical sophistication of the Inflation devices market.

Peripheral angioplasty enjoys steady patient inflow as awareness of critical-limb ischemia spreads. Gastroenterologists report an 88.9% success rate using drug-coated balloons for benign esophageal strictures, encouraging GI units to stock dedicated inflation kits. Urologists engaged in prostate-artery embolization likewise recruit ultra-high-resolution imaging that benefits from pressure-stable devices. Combined, these applications enlarge the procedurally diverse base of the Inflation devices market.

By Pressure Range: mid-range versatility sustains demand

Units rated 15–30 atm account for 57.82% of the Inflation devices market thanks to multi-lesion versatility. These pumps handle drug-coated balloon inflation, calcified stenosis, and peripheral disease without switching tools, simplifying inventory. Growth at 7.54% CAGR underscores provider confidence that one SKU can span most anatomical challenges.

Low-pressure (<15 atm) devices survive in pediatrics and delicate visceral work, while >30 atm systems remain niche for chronic total occlusions. R&D budgets therefore center on mid-range refinements—leak-proof connectors, faster deflation—and not on pressure extremes. Fiber-optic gauge integration is the next frontier as vendors race to raise measurement accuracy within the core range of the Inflation devices market.

By End User: ASC growth transforms channel economics

Hospitals held 53.15% of value in 2025, yet ASCs will contribute the bulk of incremental gains through 2031. Outpatient centers demand compact pumps with intuitive UIs; suppliers have responded with fast-prime syringes to cut room turnover times. Specialty clinics and dedicated cath-labs reinforce mid-tier demand, procuring premium pumps for niche cases while standardizing consumables to curb costs. This user cascade diversifies revenue streams and enhances resilience for companies active in the Inflation devices market.

Geography Analysis

North America generated 41.95% of global revenue in 2025, underpinned by high procedural density and supportive reimbursement. CMS’s 2.93% fee-schedule uplift secures predictable returns for providers, fueling capital expenditure on next-generation consoles. Canadian labs, benefiting from device reciprocity with FDA approvals, follow U.S. buying patterns, while Mexico upgrades cardiac infrastructure through public–private funding.

Europe maintains second position through comprehensive insurance coverage and stringent MDR oversight, which elevates demand for pumps with exportable log files. Germany, France, and the United Kingdom together perform more than 600,000 PCI and peripheral procedures per year, guaranteeing baseline throughput for the Inflation devices market. Southern Europe, seeking cost balance, often opts for hybrid analog-digital configurations that meet compliance at lower capital cost.

Asia-Pacific is forecast to expand 7.06% annually, the sharpest pace in the Inflation devices market. China approved 12,213 medical devices in 2023, over half in Class III, reflecting regulator willingness to fast-track innovation. India’s domestic manufacturing push is narrowing import gaps, opening sub-USD 2,000 analog segments. Japan and South Korea, both aging rapidly, sustain complex neurovascular case growth, creating premium device pockets. Southeast Asian governments co-finance cath-lab rollouts, enabling first-time purchases and widening regional demand for the Inflation devices market.

Competitive Landscape

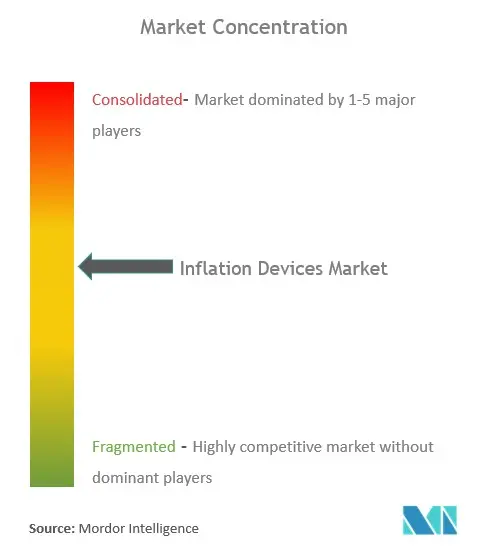

The top five players control roughly half of the Inflation devices market, constituting moderate consolidation. Medtronic logged USD 8.4 billion Q2 FY25 revenue, up 5.3%, riding TAVR and structural-heart momentum. Boston Scientific reported 26.2% cardiovascular sales growth in Q1 2025 after acquiring Bolt Medical.

Quality-control scrutiny shapes competitive fortunes; FDA warning letters to Chinese syringe makers spotlight supply risk and open doors for compliant suppliers. Established firms hedge with vertically integrated service packages—training, software analytics, and guaranteed turn-times. Niche entrants specialize in neurovascular micro-pressure devices, vying for high-margin sub-segments of the Inflation devices market. AI-enabled dashboards that benchmark inflation cycles represent the next competitive differentiator as hospitals link procurement to measurable outcome improvements.

Inflation Devices Industry Leaders

Teleflex Incorporated

Merit Medical Systems

Johnson & Johnson Services, Inc

ARGON MEDICAL

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: FDA approved the VARIPULSE Platform for paroxysmal atrial fibrillation with 74.4% 12-month success

- September 2024: FDA cleared the Minima Stent System for pediatric coarctation, showing 97.6% vessel-widening success

Global Inflation Devices Market Report Scope

As per the scope of the report, an inflation device is a sterile device designed to inflate and regulate the pressure of a balloon dilatation catheter manually by injecting and aspirating fluid or air within the balloon and deflating the balloon during medical procedures like angioplasty.

The inflation devices market is segmented by display type (analog display and digital display), application (interventional cardiology, interventional radiology, peripheral vascular procedures, gastroenterology procedures, urology procedures, and other applications), end user (hospitals and clinics, ambulatory surgical center, and other end users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally and offers the value (in USD million) for the above segments.

| Analog Inflation Devices |

| Digital Inflation Devices |

| less than 15 atm |

| 15 – 30 atm |

| more than 30 atm |

| Coronary Angioplasty |

| Peripheral Angioplasty |

| Neurovascular Procedures |

| Gastroenterology & ERCP |

| Urology & Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics & Cath Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Analog Inflation Devices | |

| Digital Inflation Devices | ||

| By Pressure Range (Value) | less than 15 atm | |

| 15 – 30 atm | ||

| more than 30 atm | ||

| By Application (Value) | Coronary Angioplasty | |

| Peripheral Angioplasty | ||

| Neurovascular Procedures | ||

| Gastroenterology & ERCP | ||

| Urology & Others | ||

| By End User (Value) | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics & Cath Labs | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Inflation Devices market?

The Inflation Devices market size is USD 677.52 million in 2026 and is projected to reach USD 876.53 million by 2031.

Which region holds the largest share in the Inflation Devices market?

North America leads with 41.95% share, supported by high procedural volumes and favorable reimbursement.

Which segment is growing fastest within the Inflation Devices market?

Digital inflation devices exhibit the highest segment CAGR at 6.15% through 2031 due to demand for data-rich workflows.

How is regulation affecting new product introductions?

Class III approval pathways require extensive clinical data and higher user fees, extending time-to-market for advanced devices.

Page last updated on: