Insufflation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.28 Billion |

| Market Size (2031) | USD 4.37 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

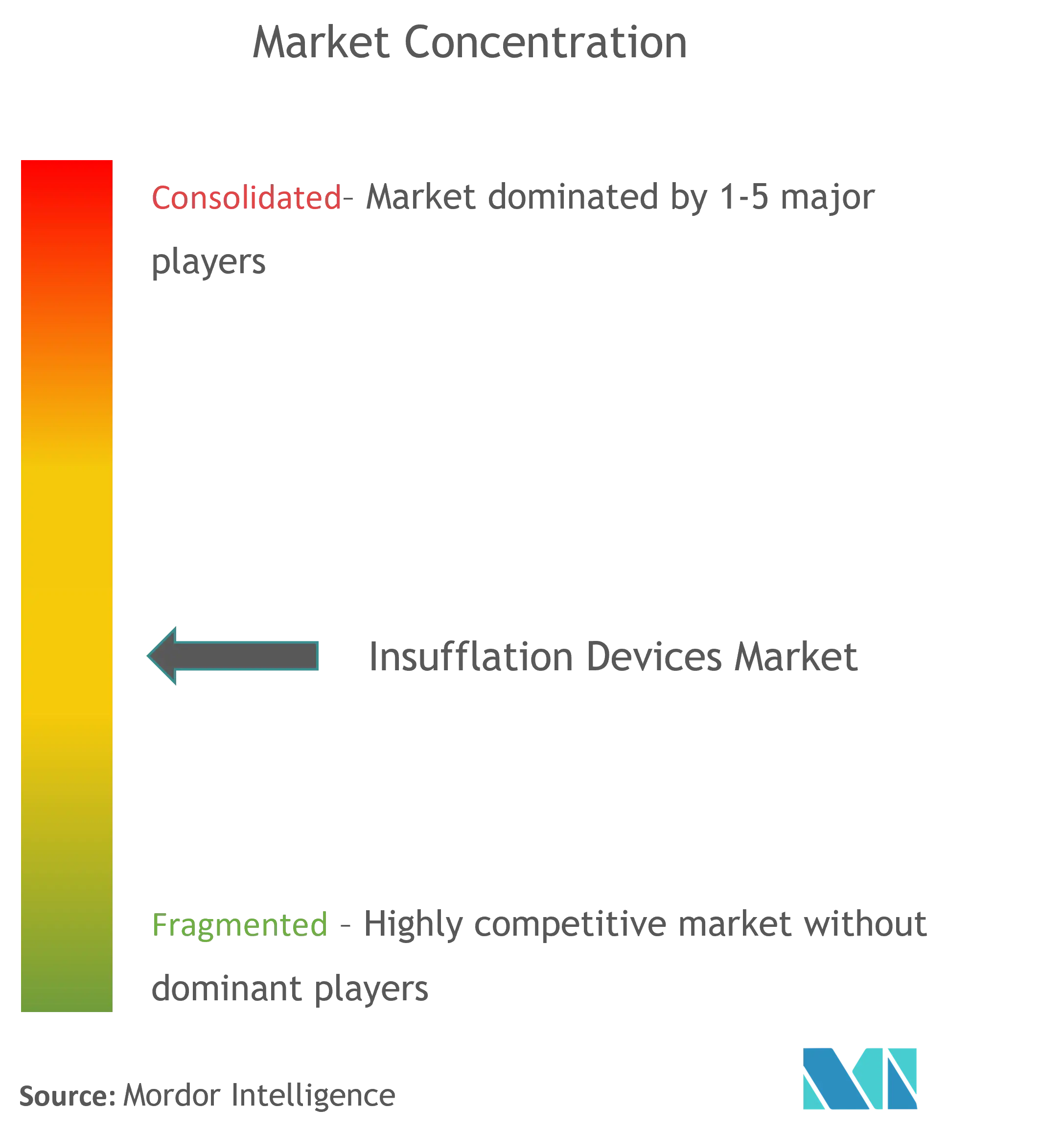

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insufflation Devices Market Analysis by Mordor Intelligence

The Insufflation Devices Market size is expected to grow from USD 3.10 billion in 2025 to USD 3.28 billion in 2026 and is forecast to reach USD 4.37 billion by 2031 at 5.88% CAGR over 2026-2031.

A measured shift from one-time capital sales to recurring revenue tied to disposable tubing, filters, and software support now shapes vendor strategies. Hospitals continue to refresh consoles every seven to ten years, yet procurement committees favor consumable-driven models that simplify infection control and spread costs across procedures. Robotic platforms embedding insufflation management, such as the da Vinci 5, expand the addressable market for proprietary tubing even as they depress standalone console volume. Meanwhile, payer pressure for shorter stays and lower complication rates increases demand for precision-flow devices capable of maintaining low-pressure pneumoperitoneum, which mitigates postoperative pulmonary complications.

Key Report Takeaways

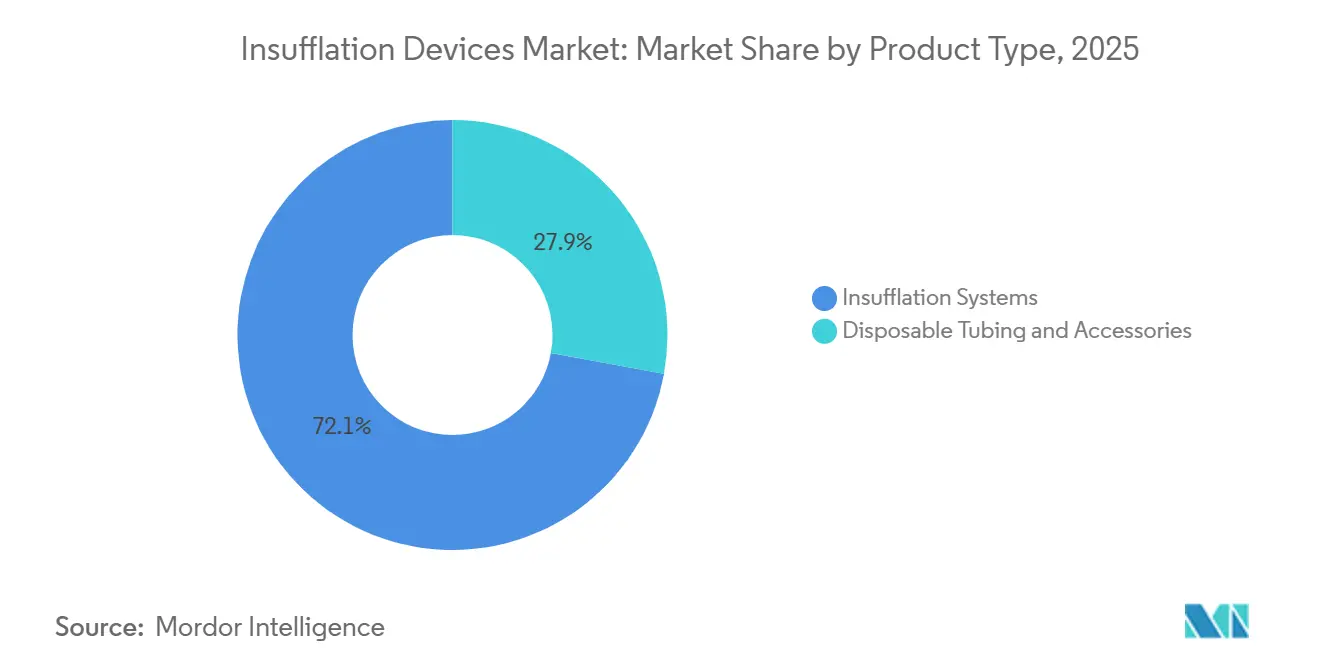

- By product type, insufflation systems held 72.12% of the insufflation devices market share in 2025, while disposable tubing and accessories are forecast to register the fastest 7.65% CAGR through 2031.

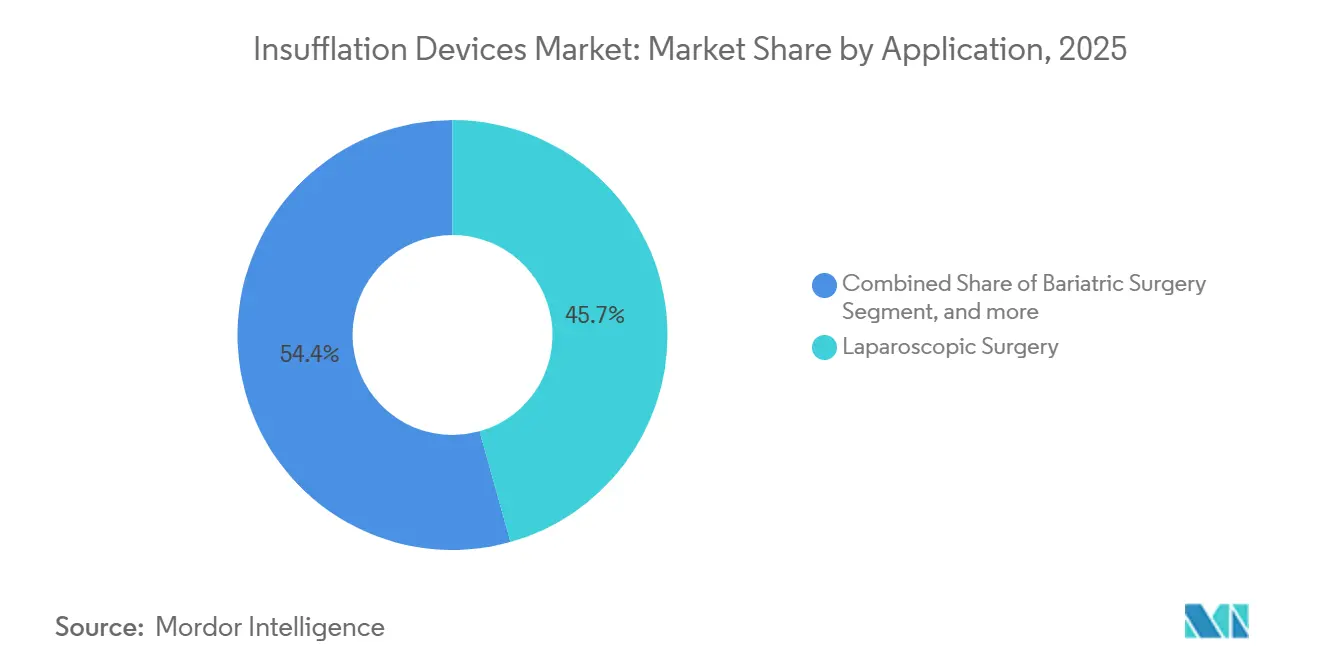

- By application, laparoscopic surgery accounted for 45.65% revenue in 2025; bariatric surgery is projected to grow at a 8.44% CAGR to 2031.

- By end user, hospitals retained 62.71% of the insufflation devices market share in 2025, whereas ambulatory surgical centers are poised for an 8.32% CAGR, underpinned by a projected 44 million U.S. ASC procedures by 2034.

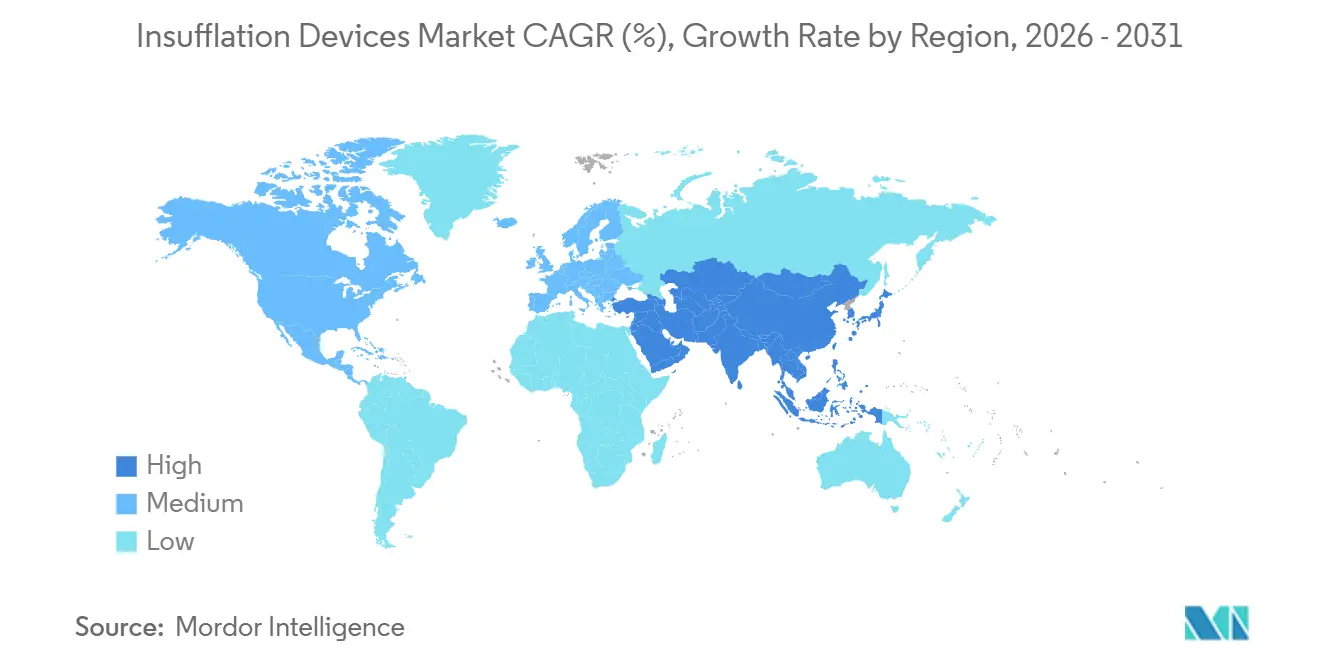

- By geography, North America dominated with 42.54% share in 2025; Asia-Pacific is on track for the fastest 6.54% CAGR through 2031 as infrastructure investments accelerate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insufflation Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Minimally Invasive Surgery | +1.8% | Global, with APAC acceleration | Medium term (2-4 years) |

| Continuous Technological Advancements in Insufflation Platforms | +1.2% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Surge in Bariatric and Gynecologic Procedure Volumes | +1.5% | North America, Western Europe, GCC | Medium term (2-4 years) |

| Integration with Digital Operating Room Ecosystems | +0.9% | North America, select EU markets | Long term (≥ 4 years) |

| Expansion of Ambulatory Surgery Infrastructure | +1.1% | North America, Australia | Short term (≤ 2 years) |

| Shift Toward Disposable Insufflation Consumables | +1.0% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Minimally Invasive Surgery

Minimally invasive surgery accounted for 65% of eligible abdominal cases in the United States by 2024 and shows uneven uptake elsewhere, producing sizable white spaces for vendors to target surgeon training and bundled leasing solutions. Sleeve gastrectomy led bariatric procedures, with robotic assistance rising to 30% by 2024. Near-complete laparoscopic conversion rates for cholecystectomy in OECD markets demonstrate how standardization cements console utilization, whereas penetration below 40% in parts of Southeast Asia and Sub-Saharan Africa reflects capital and training gaps. Regulatory burden remains light because 510(k) reviews emphasize safety over clinical efficacy, leaving reimbursement as the primary driver of adoption. Bundled payment policies that reward shorter stays favor low-pressure pneumoperitoneum management and therefore stimulate purchases of advanced consoles that sustain pressures below 10 mmHg.

Continuous Technological Advancements in Insufflation Platforms

Innovation is migrating from stand-alone hardware toward software-defined modules that interoperate with anesthesia workstations and navigation systems. CONMED’s AirSeal iFS, now installed in 5,857 facilities and used in more than 8 million procedures, exemplifies continuous smoke evacuation and valve-free pressure control that reduces postoperative shoulder pain by 34%. AI-enabled algorithms predict phase transitions and preempt pressure spikes, though Software-as-a-Medical-Device clearances add 18 months to development cycles. ISO 13485 compliance remains entry-level, but competitive advantage now hinges on HL7 FHIR-ready data output that feeds OR dashboards. Vendors that master connectivity gain a service revenue stream from predictive maintenance and analytics subscriptions.

Surge in Bariatric and Gynecologic Procedure Volumes

United States bariatric cases reached 280,000 in 2024, up 6.5% year over year, following broader insurance coverage for patients with BMI ≥ 35 and comorbidities. Robotic hysterectomies exceeded 40% penetration by 2025, requiring precision insufflation to mitigate hemodynamic and pulmonary risks from steep Trendelenburg positioning. Evidence published in 2024 showed sub-10 mmHg pressure during robotic hysterectomy cuts postoperative nausea and vomiting by 28%, an outcome metric affecting hospital star ratings. Medicare’s 2024 parity for laparoscopic and robotic bariatric facility fees removed financial barriers, enabling hospitals to justify investment in integrated insufflation-robotic platforms. Vendors that tailor pressure algorithms for longer bariatric case times stand to win replacement cycles in high-volume centers.

Integration with Digital Operating Room Ecosystems

Private 5G networks installed in over 200 U.S. hospitals by mid-2025 enable sub-50 millisecond feedback loops linking insufflation sensors to OR dashboards. Intuitive Surgical’s da Vinci 5 console lets surgeons adjust flow via touchscreen, reducing verbal commands and cognitive load while locking facilities into a single-vendor stack. FDA cybersecurity guidance issued in September 2024 mandates secure update mechanisms and a Software Bill of Materials, favoring multinationals that already operate DevSecOps teams. Stand-alone console makers must release open APIs or confront rapid commoditization as robotic OEMs vertically integrate insufflation functionality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical Concerns Over Carbon Dioxide-Related Complications | −0.7% | Global | Medium term (2–4 years) |

| High Upfront Investment for Next-Generation Console Systems | −0.9% | Emerging markets in APAC, Latin America, MEA | Short term (≤2 years) |

| Tightening Regulations on Medical-Grade Carbon Dioxide Supply | −0.4% | North America, EU | Short term (≤2 years) |

| Emerging Cybersecurity Compliance Burden for Connected Devices | −0.6% | North America, EU, advanced APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Clinical Concerns Over Carbon Dioxide-Related Complications

Prolonged CO₂ insufflation can elevate arterial PCO₂ by up to 25%, producing respiratory acidosis that complicates anesthesia and extends recovery. Meta-analysis published in 2024 linked pressures above 12 mmHg for more than 90 minutes to pulmonary complications in up to 20% of cases. Although alternatives such as helium remain unapproved, clinician caution slows uptake of high-flow devices unless they include closed-loop pressure caps. Subcutaneous emphysema incidence of 0.5-2% further heightens scrutiny in bundled-payment environments where hospitals absorb readmission costs. Absent mandatory clinical trial data in 510(k) submissions, surgeons rely on peer-reviewed studies and society guidelines, forcing manufacturers to generate post-market evidence to counter safety concerns.

High Upfront Investment for Next-Generation Console Systems

Premium consoles with integrated smoke evacuation list for USD 35,000-50,000, a 40-60% premium over legacy units. Capital scarcity in India, Brazil, and Indonesia prompts many hospitals to operate refurbushed equipment that lacks closed-loop control. Leasing lowers entry cost but ties facilities to multiyear consumable minimums that limit bargaining leverage. A 2024 cost-utility analysis by the American College of Surgeons concluded that high-volume centers performing more than 500 laparoscopic procedures per year achieve lower per-procedure cost with premium consoles, yet smaller hospitals struggle to justify the outlay. As a result, market penetration of next-generation systems risks stalling in lower-income regions unless financing programs broaden.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Capture Momentum

Disposable tubing & accessories accounted for 27.88% revenue in 2025 and are projected to expand at a 7.65% CAGR through 2031. The insufflation devices market for disposables is poised to grow steadily as infection-prevention regulations tilt preference toward single-use components. Proprietary filter and tubing sets priced between USD 15 and USD 45 per procedure deliver gross margins above 60%, encouraging vendors to discount consoles in exchange for consumable contracts. A 2024 U.S. hospital survey revealed that 78% of infection-control committees now require single-use tubing, a 16-percentage-point increase in two years. Vendors exploit this trend by bundling disposables with software licenses that monitor tubing expiration dates, enhancing supply-chain compliance and reducing waste.

Conversely, console revenue grows modestly at 3-4% as the installed base ages across seven-to-ten-year replacement cycles. The insufflation devices market share held by Insufflation Systems remains dominant at 72.12% in 2025, yet pricing headwinds and embedded integration within robotic platforms erode standalone demand. Manufacturers, therefore, position consoles as gateways to higher-margin consumable streams, emulating razor-and-blade economics. Facilities with high laparoscopic case volumes justify console upgrades when predictive maintenance and closed-loop pressure modulation cut unplanned downtime and postoperative complications, supporting procurement under value-based payment models.

By Application: Bariatric Lines Fuel Fastest Growth

Bariatric surgery is anticipated to post an 8.44% CAGR to 2031, outpacing all other indications as global obesity rates push sleeve gastrectomy and gastric bypass demand. The insufflation devices market size for bariatric procedures is set to escalate because each operation consumes up to double the CO₂ volume of a routine cholecystectomy and requires pressure stability for 90-120 minutes. Hospitals investing in robotic bariatric programs favor integrated insufflation modules that streamline setup and support low-pressure protocols to reduce postoperative pain and pulmonary complications.

Laparoscopic surgery nevertheless retains 45.65% of 2025 revenue, reflecting high volumes of cholecystectomy, appendectomy, and hernia repair in mature markets. Growth moderates as penetration nears saturation, prompting console makers to differentiate through analytics that document pneumoperitoneum quality for credentialing and quality metrics. Gynecologic, urologic, thoracic, and pediatric niches together form a meaningful tail, where specialization demands miniaturized tubing and delicate flow algorithms that command premium pricing from vendors able to tailor kits to subspecialty needs.

By End User: ASC Expansion Reshapes Sales Channels

Ambulatory surgical centers captured an incremental share in 2025 and are expected to grow at an 8.32% CAGR through 2031. These facilities seek compact consoles with mobile carts that fit smaller footprints and support rapid turnover. Vendor leasing programs aligning monthly fees with case volume, mitigate capital constraints, and embed proprietary consumable usage in long-term contracts. The insufflation devices market share controlled by hospitals remains high at 62.71%, but procurement decisions increasingly weigh total cost of ownership under bundled-payment models that penalize postoperative complications.

Tier I academic centers and high-acuity urban hospitals represent early adopters of AI-enabled consoles with predictive maintenance, while Tier II rural facilities often extend legacy hardware life by purchasing refurbished units. Specialty clinics in bariatric and gynecologic care create pockets of demand where surgeon preference overrules centralized purchasing, enabling smaller vendors to gain footholds through direct engagement and differentiated consumable offerings.

Geography Analysis

North America led the insufflation devices market with 42.54% revenue share in 2025, translating to an insufflation devices market size of about USD 1.38 billion that year. Robust robotic‐surgery penetration exceeding 50% in prostatectomy and hysterectomy, Medicare payment parity for bariatric procedures, and early deployment of digital OR ecosystems sustain mid-single-digit growth in console replacements. The United States drives the region, performing 280,000 bariatric surgeries in 2024, a volume that demands extended insufflation times and repeat filter changes. Canada’s CAD 120 million (USD 88 million) surgical modernization outlay in 2024–2025 funded insufflator upgrades in 45 hospitals, while Mexico’s 1.2 million inbound medical tourists in 2024 spurred private‐hospital investment in premium equipment. Vendor strategies center on bundled equipment-consumable deals that lock high-volume U.S. centers into proprietary tubing, while offering Mexico’s price-sensitive clinics flexible leasing options. FDA cybersecurity rules, effective in 2025, add compliance costs yet also raise switching barriers, cementing incumbent share.

Asia-Pacific is forecast to grow at a 6.54% CAGR through 2031, the fastest regional pace in the insufflation devices market. China logged 18.5 million laparoscopic procedures in 2024, up 9.2% year on year, after the National Health Commission financed 400 new minimally invasive surgery suites. India’s Ayushman Bharat insurance expansion unlocked district-hospital procurements, though domestic brands undercut multinationals by 40-50% on console price, fracturing share. Japan counted 450 da Vinci installations by 2025, but tight reimbursement caps limit procedure growth, curbing console refresh cycles. Australia’s private hospitals, which are responsible for 60% of elective surgeries, adopt compact, battery-powered consoles that align with ambulatory workflows. Regional distributors play an outsized role, especially in Indonesia and the Philippines, where fragmented hospital networks favor vendors able to offer local service and financing packages. The insufflation devices industry faces localization mandates in China that require joint manufacturing, pushing global OEMs toward technology-transfer partnerships to secure tenders.

Europe accounts for roughly 30% of global revenue, yet EU Medical Device Regulation stringency lengthens certification timelines, consolidating share with Medtronic, Karl Storz, and Olympus. Germany’s 1.8 million laparoscopic cases in 2024 generate steady filter demand, while hospital DRG reimbursement tables reward low complication rates that precision-flow consoles can document. The United Kingdom invested GBP 200 million (USD 255 million) in surgical equipment upgrades during 2024–2025, though 30% of planned installs face delivery delays from supply-chain bottlenecks[1]UK Department of Health and Social Care, “Elective Recovery Funding 2024-25,” gov.uk. France’s target of 70% ambulatory surgery by 2025 lifts sales of space-saving consoles with mobile carts. Gulf Cooperation Council countries, led by the UAE and Saudi Arabia, import premium systems for medical-tourism hubs that promise surgeons integrated smoke evacuation and cybersecurity compliance. South America and Africa trail in absolute volume; Brazil’s pilot laparoscopic programs under the SUS scheme and Nigeria’s private-hospital corridor in Lagos represent beachheads for vendors prepared to bundle training with equipment financing.

Competitive Landscape

The top five players held an estimated 55–60% of global revenue in 2025, giving the insufflation devices market a moderate concentration profile. Medtronic leverages its global service network and bundled contracts with the Hugo robotic platform to secure multi-year consumable commitments that temper hardware price erosion. Stryker’s trade-in program, launched in October 2024, offers up to USD 15,000 credit toward consoles with integrated smoke evacuation, accelerating replacement cycles in facilities constrained by capital budgets. Karl Storz’s ENDOFLATOR+ won FDA clearance in January 2025 and anchors a razor-and-blade strategy built on USD 28 proprietary filters that generate 60% gross margin[2]Karl Storz SE, “ENDOFLATOR+ 510(k) Summary,” accessdata.fda.gov . Olympus defends its share through ISO 13485-certified manufacturing and cross-selling to its vast endoscopy installed base, while Johnson & Johnson’s Ethicon division packages insufflation with energy devices for integrated tender bids.

Second-tier challengers pursue the disposables niche. CONMED’s AirSeal iFS, used in more than 8 million procedures, monetizes valve-free filters that hospitals reorder automatically through inventory software APIs. Applied Medical undercuts incumbents by 20% on disposable tubing, and courts surgeons to champion inside GPOs to bypass central purchasing. Lexion Medical and B. Braun focus on pediatric and ASC-optimized systems, respectively, exploiting gaps where large OEMs lack specialized SKUs. Intuitive Surgical rewired industry dynamics by embedding insufflation into its da Vinci 5 console in 2024, reducing standalone console demand yet enlarging the proprietary consumables pie. Smaller software-first entrants tout AI-based predictive maintenance that cuts downtime, though FDA cybersecurity rules raise their regulatory burden, nudging many toward OEM licensing or acquisition.

Price competition intensifies in emerging markets where refurbished consoles from Chinese brands enter at 30–40% discounts. To preserve margin, multinationals expand service offerings that bundle annual safety audits, uptime guarantees, and cybersecurity patches. Sustainability mandates push R&D toward CO₂ capture or recyclable tubing, a feature early-adopter hospitals desire for ESG reporting but one that increases bill-of-material cost. Overall, the insufflation devices market shows a market concentration score of 6, as the top five players command just over 55% share yet face agile niche rivals that fragment the disposables segment.

Insufflation Devices Industry Leaders

Medtronic plc

STERIS plc

Stryker Corporation

Smith & Nephew plc

Karl Storz SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: KARL STORZ received FDA 510(k) clearance for ENDOFLATOR+ with 50 L/min smoke evacuation and automated pressure compensation

- July 2025: Innovia Medical acquired Grace Medical and Hurricane Medical to expand its specialty surgical product offerings in ENT and Ophthalmic solutions. These acquisitions enhance its global presence and ability to support healthcare providers worldwide.

Global Insufflation Devices Market Report Scope

As per the scope of this report, insufflation is the act of blowing gas, powder, or vapor into a body cavity. Gases are often insufflated into a body cavity to inflate the cavity for more workroom during various surgery.

The Insufflation Devices Market is Segmented by Application (Laparoscopic, Endoscopic, and Others), End-users (Hospitals, Clinics, Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| Insufflation Systems |

| Disposable Tubing & Accessories |

| Laparoscopic Surgery |

| Bariatric Surgery |

| Gynecological Surgery |

| Cardiac & Thoracic Surgery |

| Urological & Renal Surgery |

| Pediatric Surgery |

| Other Applications |

| Hospitals (Tier I/II/III) |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Insufflation Systems | |

| Disposable Tubing & Accessories | ||

| By Application | Laparoscopic Surgery | |

| Bariatric Surgery | ||

| Gynecological Surgery | ||

| Cardiac & Thoracic Surgery | ||

| Urological & Renal Surgery | ||

| Pediatric Surgery | ||

| Other Applications | ||

| By End User | Hospitals (Tier I/II/III) | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the global insufflation devices market in 2031?

The market is forecast to reach USD 4.37 billion by 2031, growing at a 5.88% CAGR from 2026.

Which segment is expanding fastest within the insufflation devices market?

Disposable tubing & accessories are projected to increase at a 7.65% CAGR through 2031 as hospitals tighten infection-control rules.

How quickly is the Asia-Pacific region expanding?

Asia-Pacific is expected to grow at a 6.54% CAGR, the fastest rate among all regions, driven by hospital construction in China and India.

Why are ambulatory surgical centers important for vendors?

ASCs are opening at scale in North America and favor compact, lease-financed consoles, pushing vendors to bundle equipment and consumables.

Which technological features are now decisive for new console purchases?

Closed-loop low-pressure control, integrated smoke evacuation, and cybersecurity-compliant connectivity top hospital procurement checklists.

Page last updated on: