Epilepsy Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.41 Billion |

| Market Size (2031) | USD 12.97 Billion |

| Growth Rate (2026 - 2031) | 4.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

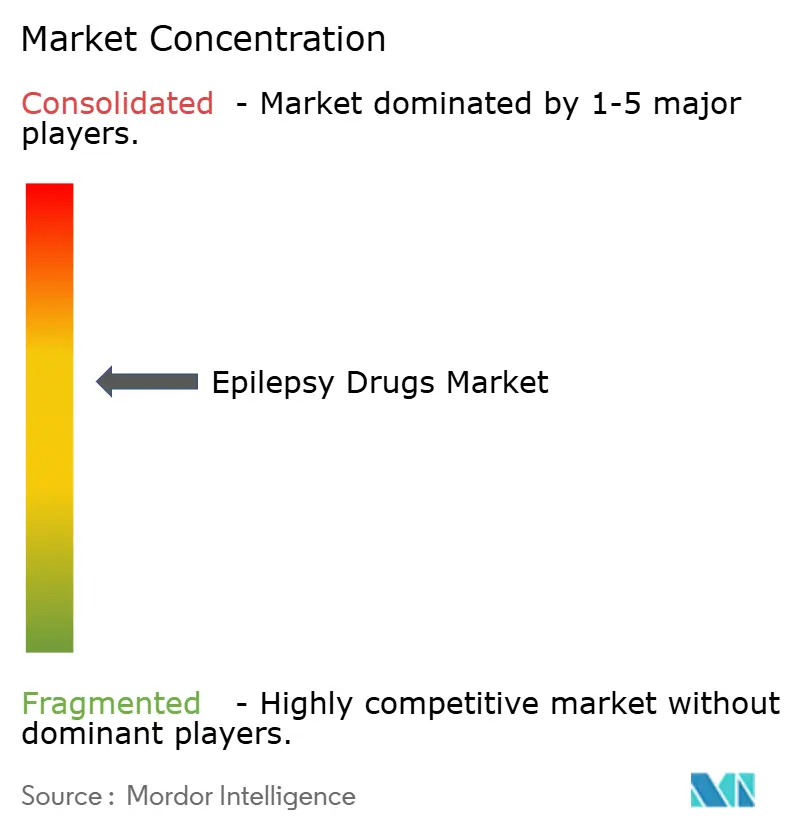

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Epilepsy Drugs Market Analysis by Mordor Intelligence

The Epilepsy Drugs market size is expected to grow from USD 9.96 billion in 2025 to USD 10.41 billion in 2026 and is forecast to reach USD 12.97 billion by 2031 at 4.5% CAGR over 2026-2031.

This advance reflects the successful launch of third-generation antiseizure medicines, fast adoption of genetic precision tools, and the growth of tele-neurology services that improve adherence. Demand keeps rising as physicians seek safer agents for focal seizures and drug-resistant epilepsy, yet pricing pressure from patent expirations and periodic API shortages temper topline momentum. North America retains leadership through deep reimbursement coverage, while Asia-Pacific shows the strongest trajectory as China and India invest in epilepsy awareness campaigns and broaden access to advanced therapies. Competitive intensity is sharpening because niche innovators are winning share in orphan indications and digital-health ecosystems.

Key Report Takeaways

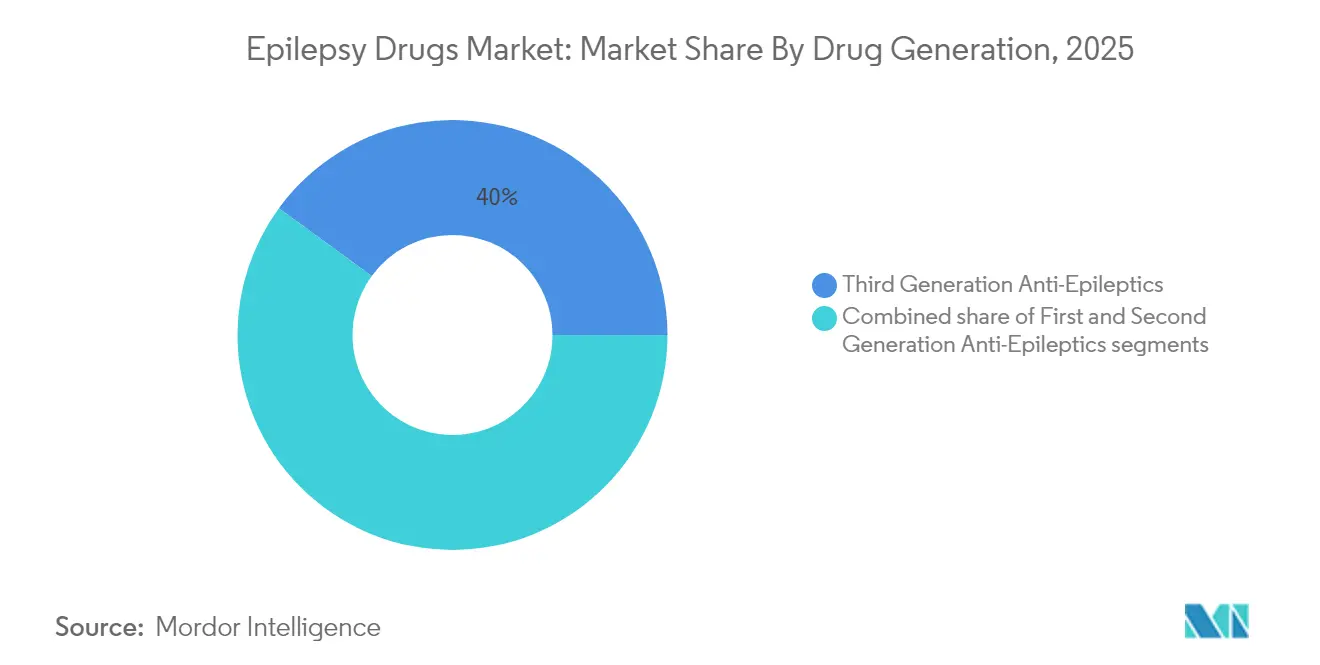

- By drug generation, third-generation agents led with 39.96% of anti-epileptic drugs market share in 2025, while second-generation products are on track for the fastest 6.08% CAGR through 2031.

- By seizure type, focal seizures commanded a 60.88% share of the anti-epileptic drugs market size in 2025. Unclassified or combined seizures are projected to post the highest growth rate of 5.76% by 2031.

- By patient type, adults held 66.72% of the anti-epileptic drugs market size in 2025; pediatrics will record the strongest 6.29% CAGR through 2031.

- By route of administration, oral formulations captured 50.74% revenue share in 2025, whereas injectables are forecast to expand at the fastest pace of 5.55% to 2031.

- By distribution channel, hospital pharmacies led with 40.21% of anti-epileptic drugs market share in 2025, but e-pharmacies and other alternative outlets will experience the quickest growth, growing at 6.68% to 2031.

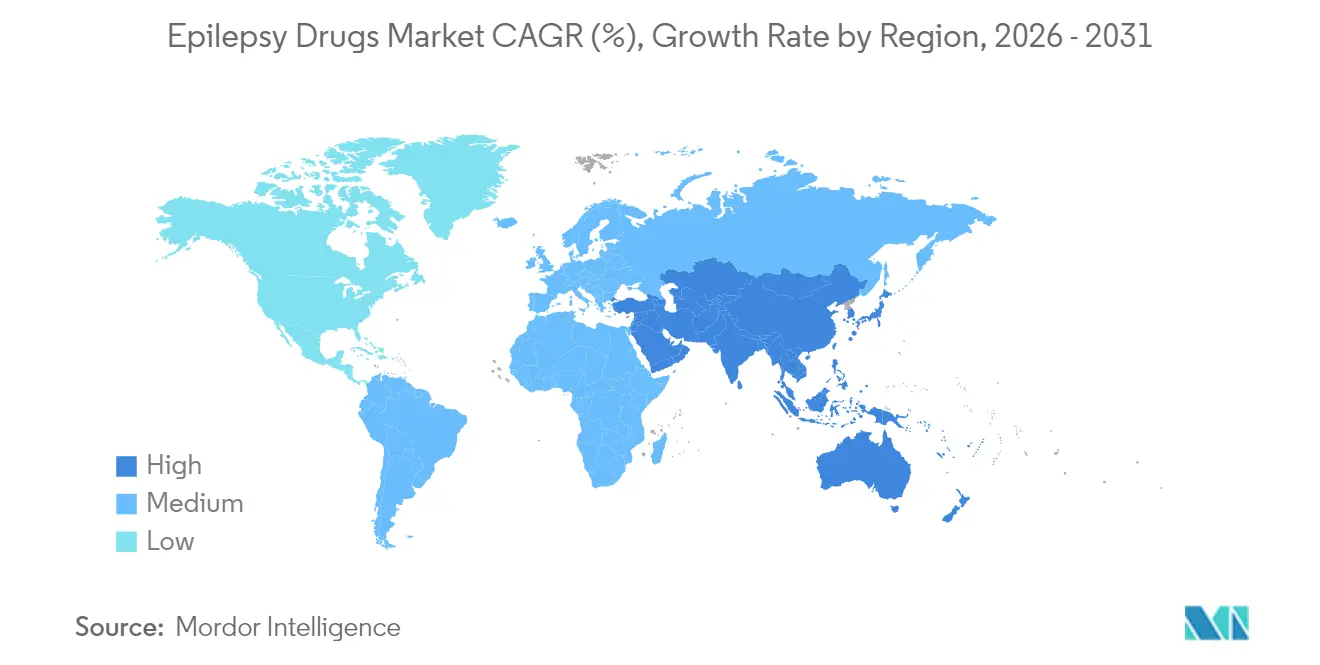

- By geography, North America led with 39.76% share of the anti-epileptic drugs market size in 2025, while Asia-Pacific is projected to expand at a 5.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Epilepsy Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Third-generation approvals with safer profiles | +1.2% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Growing pool of patients with drug-resistant epilepsy | +1.0% | Global, strongest in regions with supportive regulations | Medium term (2-4 years) |

| Precision genetics & AI-enhanced EEG diagnostics | +0.9% | North America, Europe, advanced Asia-Pacific hubs | Medium term (2-4 years) |

| Rapid tele-neurology adoption boosting adherence | +0.8% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Rising investments in cannabinoid- and neurosteroid-based pipelines | +0.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Orphan-drug incentives for rare encephalopathies | +0.6% | Global, strongest in regions with supportive regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Approvals of Third-Generation Antiseizure Medications with Improved Safety Profiles

Global regulators are clearing a steady stream of next-wave agents such as cenobamate, brivaracetam, cannabidiol and diazepam nasal formulations that demonstrate higher seizure-reduction rates and fewer adverse reactions than legacy drugs. SK Biopharmaceuticals reported a 46.6% year-on-year jump in Xcopri sales to USD 102.4 million during Q1 2025.[1]NeurologyLive Editorial Team, “FDA Action Update, April 2025,” neurologylive.com Real-world data presented at the 2025 American Academy of Neurology meeting showed an 84% median seizure cut in focal-seizure adults treated with cenobamate, while an Israeli observational study cited 27.5% seizure freedom among pharmaco-resistant patients using the same molecule.[2]A.A. Khan & M.A. Khan, “Orphan Drugs in Epilepsy Treatment – A Review,” Epilepsy & Behavior Reports, sciencedirect.com The FDA’s April 2025 decision to extend diazepam nasal spray to children aged 2–5 broadens rescue options. Collectively these advances raise expectations for better long-term outcomes and spur clinicians to transition treatment-resistant cases onto newer regimens.

Precision Genetics and AI-Enhanced EEG Diagnostics Are Improving Drug Selection and Treatment Success Rates

Artificial-intelligence algorithms now parse millions of clinical records to flag monogenic epilepsies years before typical diagnosis, enabling earlier and more appropriate therapy. Children’s Hospital of Philadelphia validated a model that detects genetic epilepsies 3.6 years sooner by screening 89 million annotations from 32,000 patients.[3]Children’s Hospital of Philadelphia, “Clinical signatures of genetic epilepsies precede diagnosis,” chop.edu Whole-exome sequencing yields a 14% diagnostic hit rate, and 59% of those findings align with precision therapies, though real-world uptake still lags at 32% for reimbursement and access reasons. As payer coverage widens and AI achieves regulatory endorsement, clinicians are expected to pair genotype insights with third-generation drugs, reinforcing personalized care pathways across the anti-epileptic drugs market.

Rapid Adoption of Tele-Neurology Platforms, Raising Prescription Refill Frequency and Long-Term Adherence

The American Epilepsy Society formally supports telehealth for epilepsy management and urges regulatory flexibility to keep remote prescribing in place.[4]American Epilepsy Society, “Telehealth Position Statement,” aesnet.org SK Biopharmaceuticals and Eurofarma are developing an AI-powered epilepsy telemedicine service aimed at U.S. users, anticipating a USD 1.8 billion remote-care segment by 2032. Controlled studies reveal that video-observed therapy reminders and digital psychoeducation tools materially lower no-show rates and improve adherence, especially among Medicaid and minority populations, reinforcing revenue durability for anti-epileptic drugs market participants.

Orphan-Drug Incentives Expediting Therapies for Rare Epileptic Encephalopathies

Seven antiseizure treatments now carry orphan designations across the United States and European Union, leveraging tax benefits, fee waivers and 7- to 10-year exclusivity windows. Success stories such as fenfluramine for Dravet and Lennox-Gastaut syndromes validate the model and encourage sponsors to advance small-population programs that enjoy premium pricing latitude. With developmental and epileptic encephalopathies often resistant to mainstream drugs, orphan pathways are central to satisfying unmet clinical needs and offer an attractive commercial hedge against generics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent expirations of legacy brands | -0.7% | Global, pronounced in mature markets | Short term (≤ 2 years) |

| Recurring API shortages for key molecules | -0.5% | Global, acute in emerging economies | Medium term (2-4 years) |

| Stringent payer controls | -0.4% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Complex titration and safety monitoring | -0.4% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patent Expirations Erode Margins of Legacy Blockbuster AED Brands

UCB’s Vimpat and several other long-standing leaders face steep price drops as exclusive protections lapse. The Federal Trade Commission is scrutinizing industry tactics to block or delay generic entry and insists that savings reach patients. While erosion can exceed 70% within the first year post-expiry, it also pushes prescribers to experiment with innovative agents still under patent, shifting volume toward companies that maintain rich late-stage pipelines.

Recurring API Shortages for Carbamazepine and Levetiracetam Disrupt Supply Continuity

Concentrated manufacturing capacity combined with transportation bottlenecks resulted in more than 1,000 medicine shortages in Sweden during 2023, a trend echoed worldwide. Breaks in therapy can trigger breakthrough seizures and elevate hospitalization risk. Regulators are mandating earlier shortage notifications, while hospital buyers diversify sources and build buffer stocks, yet medium-term uncertainty persists, nudging health systems toward newer molecules with more secure supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Generation: Third-Generation Medicines Redefine Standards of Care

Third-generation compounds dominated with 39.96% share of the anti-epileptic drugs market in 2025 thanks to superior safety and dual-mechanism action. Cenobamate’s phase 3 data showed 25.8% seizure freedom over 12 months across varied doses. This progress underpins a forecast in which the segment broadens its lead through 2031, while second-generation agents grow at 6.08% CAGR on the back of extensive real-world familiarity and favorable side-effect profiles.

Moving forward, synergy between third-generation drugs and precision diagnostics will likely speed therapy switches for refractory patients, anchoring revenue streams for innovators. Even so, first-generation staples remain cornerstones in resource-limited settings because of well-known pharmacokinetics and low cost, preserving a multi-tier landscape within the anti-epileptic drugs market.

By Seizure Type: Focal Seizure Therapies Anchor Demand

Focal seizures accounted for 60.88% of anti-epileptic drugs market size in 2025, a position that mirrors the higher prevalence of partial-onset conditions globally. First-line choices include lamotrigine and levetiracetam, while carbamazepine retains broad acceptance in cost-sensitive regions.

Unclassified/Combined Seizures segment is anticipated to record a 5.76% growth rate during the forecast period. Genomic research reveals distinct architectures for focal versus generalized epilepsies, giving pipeline developers fresh targets. As precision screening becomes routine, clinicians expect to fine-tune therapy even within the focal subgroup, yielding incremental volume growth and higher adherence across the anti-epileptic drugs market.

By Patient Type: Pediatric Care Accelerates on Tailored Formulations

Adults represented 66.72% share in 2025, yet pediatric prescriptions are expanding at 6.29% CAGR due to early genetic diagnosis and child-friendly dosage forms. The FDA’s extension of diazepam nasal spray to ages 2–5 highlights momentum in rescue therapies for younger cohorts.

The pediatric segment is anticipated to record a 6.29% growth rate, the highest amongst all the sub-segments, during the forecast period. Half of children achieve seizure control with their first medication, and precision genetic panels now accelerate the path to optimal regimens. As reimbursement widens for wearable EEG and tele-pediatrics, families gain better access, fortifying the anti-epileptic drugs market outlook in pediatric neurology.

By Route of Administration: Oral Formulations Retain Primacy but Injectable Demand Rises

Oral products held 50.74% revenue share in 2025 because of ease of use over long treatment horizons. The FDA cleared an oral suspension of cenobamate in 2024 to aid patients with swallowing difficulties.

The injectable segment is anticipated to record a 5.55% growth rate during the forecast period. Injectables and nasal/buccal routes, essential for status epilepticus rescue, are climbing fastest as hospitals refine rapid-response protocols. Emerging subcutaneous pumps promise continuous delivery for severe cases, widening therapeutic options and reinforcing the anti-epileptic drugs market’s diverse administration needs.

By Distribution Channel: Hospital Pharmacies Command Volumes while E-Pharmacies Surge

Hospital dispensaries captured 40.21% anti-epileptic drugs market share in 2025 through close clinician collaboration and emergency stock. Pharmacist-led stewardship within inpatient settings improves dosing accuracy and adverse-event monitoring.

The others segment, including online pharmacy, is anticipated to record a 6.68% growth rate, the highest amongst all the sub-segments, during the forecast period. Online pharmacies paired with tele-neurology present the quickest growth vector. Eurofarma’s collaboration with SK Biopharmaceuticals showcases direct-to-patient logistics that support refill adherence in chronic therapy. This omnichannel approach expands pharmaceutical reach and heightens competition in the anti-epileptic drugs market.

Geography Analysis

North America held a 39.76% share of the anti-epileptic drugs market in 2025 due to comprehensive insurance coverage, specialist density, and rapid uptake of third-generation products. Xcopri’s 46.6% sales surge in Q1 2025 underscores the region’s appetite for differentiated therapies. Regulatory flexibility supports tele-health prescription renewal programs that improve adherence, yet cost-containment policies create downward price pressure and keep CAGR at 3.82% through 2031.

Asia-Pacific exhibits the fastest 5.74% CAGR as governments scale public health budgets and widen diagnostic infrastructure. Despite sizable progress, China’s treatment gap persists, underscoring latent opportunity for branded and quality-assured generics. Japan’s late-stage trials for cannabidiol formulations and India’s push toward local manufacturing diversify the regional offer set and accelerate growth within the anti-epileptic drugs market.

Europe balances innovation against stringent cost controls, producing a steady 4.18% CAGR. SK Biopharmaceuticals markets cenobamate in 23 European countries via Angelini, seeking higher penetration of refractory cases. South America and the Middle East & Africa, while smaller, advance on telemedicine pilots and pragmatic diagnostic guidelines tailored to resource-limited settings. These efforts collectively raise awareness, reduce stigma, and expand the anti-epileptic drugs market footprint across emerging economies.

Competitive Landscape

The top tier comprises UCB, Pfizer and Novartis, whose broad portfolios and distribution networks secure large-volume hospital contracts. Mid-cap innovators such as SK Biopharmaceuticals, Jazz Pharmaceuticals and Marinus capture high-value niches in drug-resistant and rare genetic epilepsies. Strategic moves include SK Biopharmaceuticals’ tele-neurology joint venture with Eurofarma and Jazz’s doubling down on real-world evidence to extend Epidiolex into new geographies.

Competition increasingly hinges on digital-service wrappers that bundle medication adherence tools and remote EEG analytics. Companies racing to embed AI triage and video-observed dosing into their brand ecosystems create sticky patient relationships, securing share across the anti-epileptic drugs market. Patent cliffs remain a pivotal battleground: while generics erode legacy revenues, they liberate budget for prescribers to trial premium orphan medicines, shifting channel dynamics.

Regulatory oversight of pricing tactics adds complexity. The FTC’s active litigation record signals that exclusivity extensions will face higher scrutiny, nudging firms to prioritize unique mechanisms and orphan pathways for growth. Altogether, the anti-epileptic drugs industry is transitioning toward a hybrid arena where therapeutic innovation, precision diagnostics, and digital engagement decide long-term winners.

Epilepsy Drugs Industry Leaders

Jazz Pharmaceuticals PLC

Novartis AG

Pfizer Inc.

SK Biopharmaceuticals Co. Ltd.

UCB SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: FDA expands diazepam nasal spray (Valtoco) to children aged 2–5, broadening rescue coverage.

- January 2025: SK Biopharmaceuticals and Eurofarma launched U.S. telemedicine venture to support epilepsy management.

- January 2025: Jazz Pharmaceuticals reported Epidiolex 2024 sales of USD 972.4 million, up 15% year-on-year.

- December 2024: FDA approved diazepam (Libervant) for acute seizure clusters in children 2–5 years.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the epilepsy drugs market as all prescription antiepileptic medications, across first, second, and third generations, that are dispensed to control seizures in pediatric and adult patients. Revenue is captured at ex-factory net price, converted to constant 2024 US dollars, and aggregated globally.

Scope exclusion: Non-pharmacological interventions such as neurosurgery, neuromodulation devices, ketogenic diets, and diagnostic services are outside the present analysis.

Segmentation Overview

- By Drug Generation

- First Generation Anti-Epileptics

- Second Generation Anti-Epileptics

- Third Generation Anti-Epileptics

- By Seizure Type

- Focal (Partial) Seizures

- Generalized Seizures

- Unclassified / Combined Seizures

- By Patient Type

- Adult

- Pediatric

- By Route of Administration

- Oral

- Intravenous

- Nasal / Buccal

- Subcutaneous

- By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Others

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with neurologists, hospital pharmacists, and payers across North America, Europe, Asia-Pacific, Latin America, and the Middle East to validate dose intensity, generic-switch behavior, and upcoming price controls. They then reconfirmed findings through follow-up surveys.

Desk Research

We began by sizing the treated patient pool using prevalence and incidence datasets from the World Health Organization, the Centers for Disease Control and Prevention, Eurostat, and Japan's MHLW. Therapy guidelines and drug-utilization ratios were cross-verified through publications of the International League Against Epilepsy, country formularies, and customs shipment data. Company filings, investor presentations, and news feeds accessed via D&B Hoovers and Dow Jones Factiva helped us align molecule-level revenues with geographic splits. The sources cited here are illustrative, and many additional references informed our analysis.

Market-Sizing & Forecasting

We built a top-down demand model that multiplies country prevalence, diagnosed-to-treated ratios, and weighted annual therapy cost to arrive at the 2025 baseline. Results were checked against selective bottom-up supplier roll-ups; divergences above five percent triggered further channel calls. Key variables like refractory-case share, launch cadence of third-generation molecules, generic erosion curves, currency changes, and reimbursement ceilings drive the forecast. A multivariate regression framework, supplemented by scenario analysis for supply shocks or accelerated approvals, projects values through 2030.

Data Validation & Update Cycle

Each output passes two levels of peer review, variance checks against health-system spending dashboards, and re-contacts when anomalies persist. Reports refresh every twelve months, with interim updates when major approvals, price caps, or policy shifts occur.

Why Our Epilepsy Drugs Market Baseline Commands Reliability

Published estimates often diverge, and scope choices, price points, and refresh cadence are frequent drivers of that gap. We anchor our figures on net prices, current prevalence data, and yearly validations, which together keep our baseline transparent and actionable.

Key gap drivers include inclusion of over-the-counter therapies, aggressiveness of generic deflation, currency normalization practices, and recency of epidemiological surveys used by other publishers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.96 Bn | Mordor Intelligence | baseline reference |

| USD 11.73 Bn | Global Consultancy A | list prices, modest generic erosion |

| USD 8.70 Bn | Industry Association B | excludes post-2023 third-generation launches |

| USD 11.88 Bn | Regional Consultancy C | older prevalence inputs, no currency harmonization |

Taken together, the comparison shows that Mordor's disciplined scope, live primary checks, and annual refresh deliver a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

Which therapeutic trend is reshaping treatment protocols for drug-resistant epilepsy?

Clinicians are increasingly prescribing third-generation agents such as cenobamate and brivaracetam, whose dual mechanisms and improved tolerability raise seizure-freedom rates in refractory patients.

How is genetic testing influencing prescribing decisions in epilepsy care?

Routine whole-exome sequencing and AI-supported variant interpretation help neurologists match patients to targeted therapies sooner, reducing the trial-and-error cycle common with broad-spectrum drugs.

What role do tele-neurology platforms play in medication adherence?

Video consultations and digital refill reminders lower appointment no-show rates and support continuous dosing, leading to fewer breakthrough seizures and higher patient satisfaction.

Why are cannabinoid-based formulations gaining acceptance among practitioners?

Evidence from controlled studies shows that purified cannabidiol products can substantially reduce seizure frequency in severe genetic syndromes where conventional agents provide limited relief.

What is the primary supply-chain concern for long-standing anti-epileptic molecules?

Intermittent shortages of active pharmaceutical ingredients such as carbamazepine and levetiracetam disrupt pharmacy inventories, prompting hospitals to stock alternative therapies and diversify sourcing.

What are the main restraints facing the anti-epileptic drugs market?

Near-term challenges include patent expirations that compress margins and recurring API shortages for key molecules, both of which can disrupt supply and pricing.

Page last updated on: