Industrial Salts Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

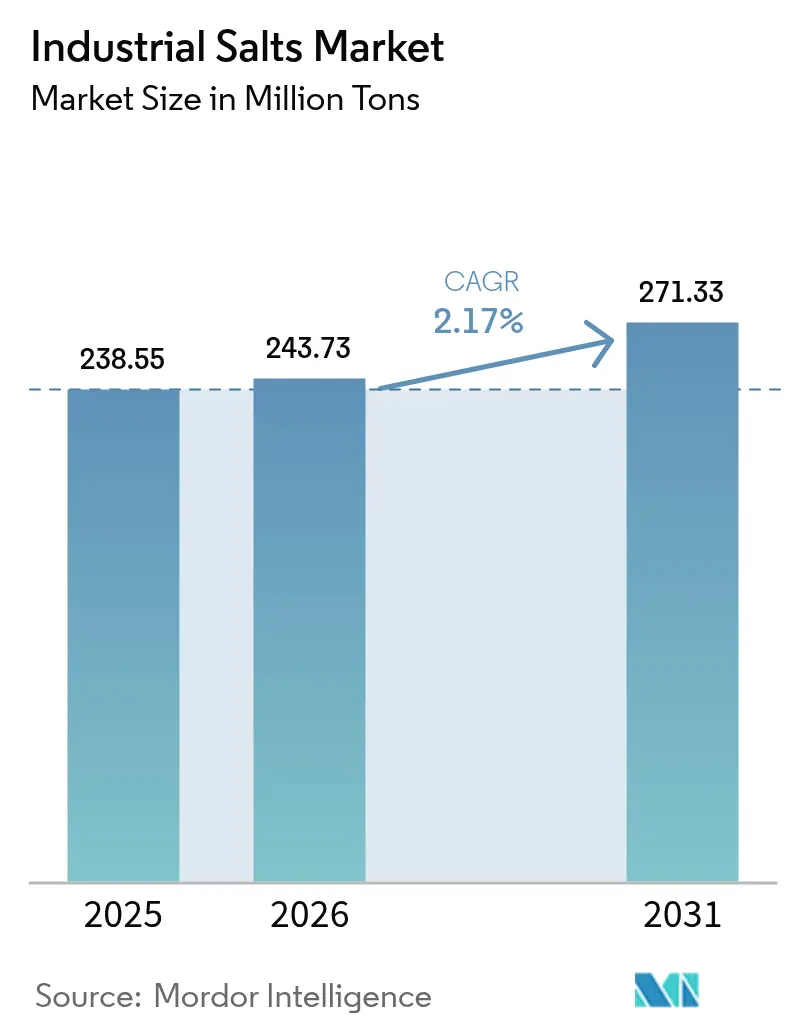

| Market Volume (2026) | 243.73 Million tons |

| Market Volume (2031) | 271.33 Million tons |

| Growth Rate (2026 - 2031) | 2.17% CAGR |

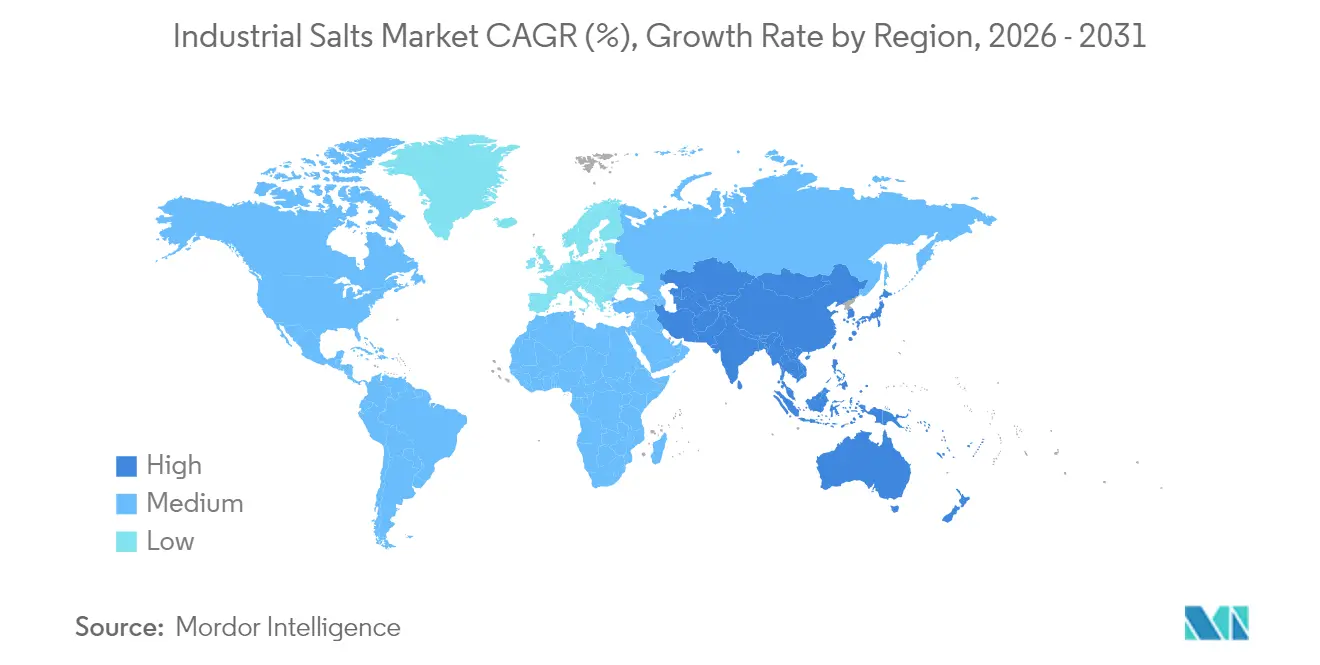

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Salts Market Analysis by Mordor Intelligence

Industrial salts market size in 2026 is estimated at 243.73 Million tons, growing from 2025 value of 238.55 Million tons with 2031 projections showing 271.33 Million tons, growing at 2.17% CAGR over 2026-2031. This measured trajectory reflects a maturing demand base, yet structural growth persists as membrane-grade chlor-alkali capacity accelerates in Asia and the Middle East, municipal water utilities upgrade to ion-exchange and reverse-osmosis systems, and ultra-high-purity specifications gain momentum in next-generation batteries and semiconductors. Rock salt, solar evaporation ponds, and chemical processing remain the volume leaders, but tightening discharge rules in the U.S. and EU, plus substitution threats from calcium chloride and organic de-icers, are pushing producers toward energy-efficient vacuum evaporation and specialty grades that command premium pricing.

Key Report Takeaways

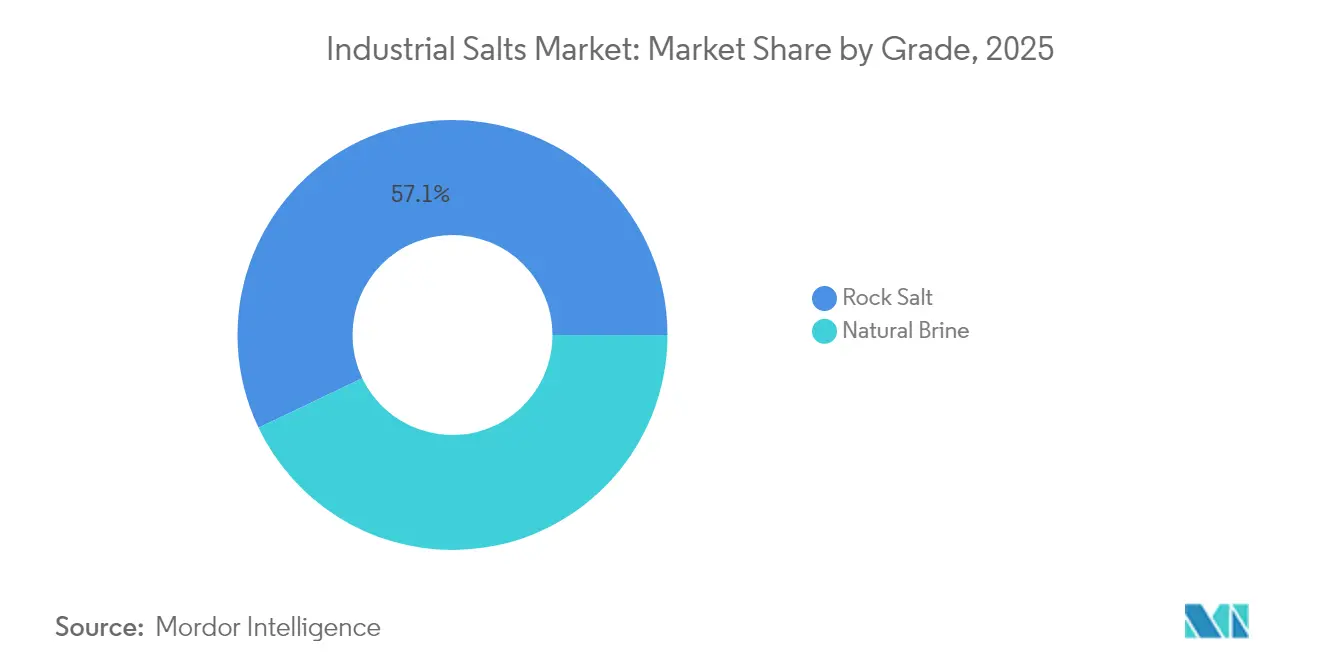

- By source, rock salt led with 57.10% industrial salts market share in 2025; and is projected to grow at a 2.73% CAGR through 2031.

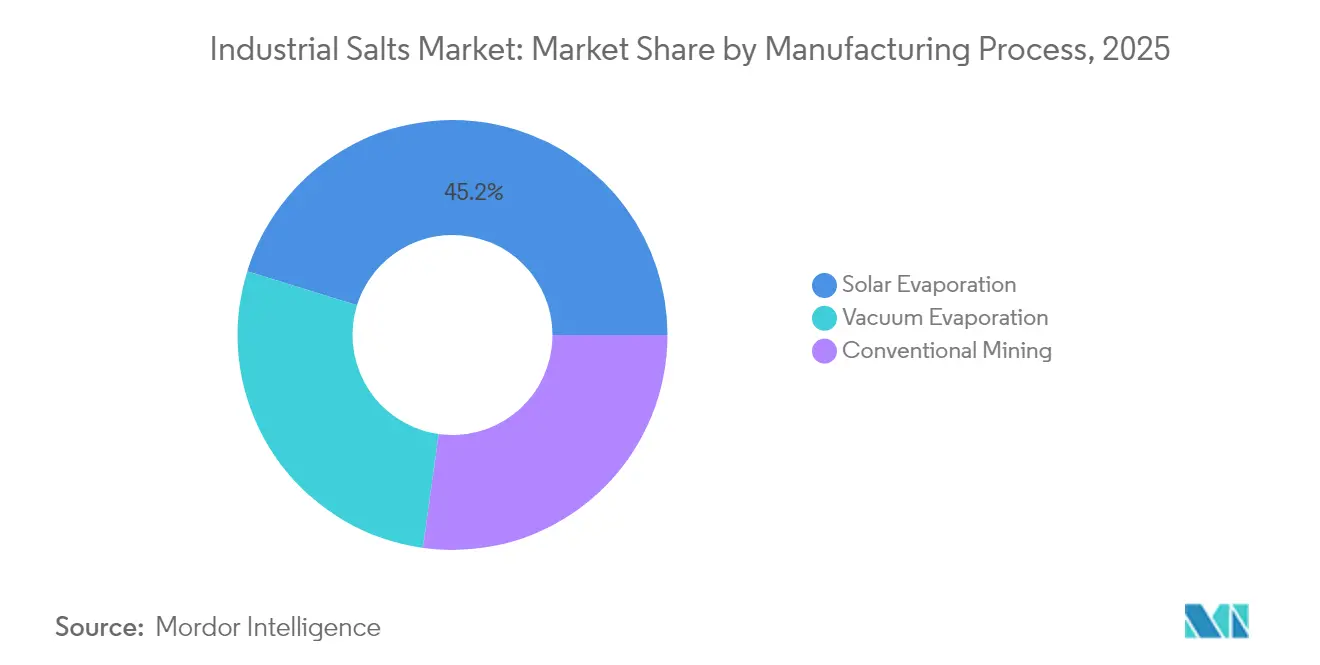

- By manufacturing process, solar evaporation controlled 45.20% revenue in 2025, while vacuum evaporation is forecast to expand at a 2.79% CAGR to 2031.

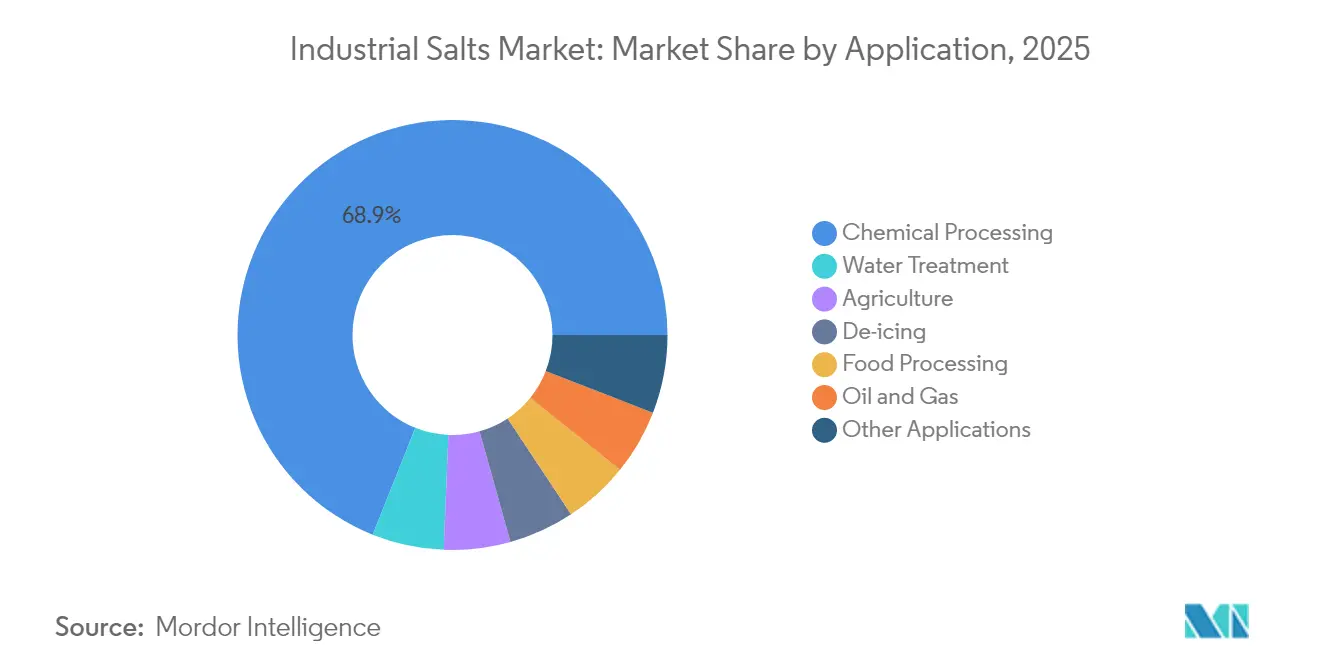

- By application, chemical processing captured 68.95% of the industrial salts market size in 2025; water treatment is advancing at a 2.87% CAGR to 2031.

- By geography, Asia-Pacific accounted for 45.50% of global demand in 2025; the region is set to post a 2.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Salts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Chlor-Alkali Capacity in Asia and Middle East | +0.8% | Asia-Pacific core, spill-over to Middle East | Medium term (2-4 years) |

| Rising Adoption in Municipal Water Treatment | +0.6% | Global, with early gains in APAC and MEA | Long term (≥ 4 years) |

| Growing De-Icing Demand Amid Harsher Winters | +0.4% | North America and EU primarily | Short term (≤ 2 years) |

| Ultra-High-Purity Salt for Next-Gen Membranes | +0.3% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Drone-Enabled Yield Gains in Solar-Pond Operations | +0.1% | APAC and MEA solar salt regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Chlor-Alkali Capacity in Asia and Middle East

China’s 2024 membrane-cell additions of 2.1 million tons caustic soda lift salt demand by almost 1.8 million tons a year, and similar projects in India and the Gulf are reinforcing long-run pull for low-calcium, low-magnesium grades. Membrane technology doubles down on purity, cutting impurity thresholds to below 50 ppm and prompting upstream investments in advanced washing, hydrocyclone, and ion-exchange polishing. Saudi-based producers are leveraging low-cost energy to export chlorine derivatives, locking in multi-year salt offtake contracts that stabilize regional pricing.

Rising Adoption in Municipal Water Treatment

Ion-exchange softening and reverse-osmosis upgrades by cities above 100,000 residents now require pharmaceutical-grade regenerant salt with tight particle-size controls to limit membrane fouling[1]3M, “Water Treatment Solutions Technical Bulletin,” 3m.com . Desalination hubs in the Gulf and Southern Europe are piloting zero-liquid-discharge crystallizers that capture salt by-products for resale. Regulatory targets such as the EU Urban Waste-Water Treatment Directive move utilities toward chloride caps below 250 mg/L, further amplifying demand for high-purity inputs.

Growing De-Icing Demand Amid Harsher Winters

North America and Northern Europe recorded 23% more severe winter events in 2024-2025 than the prior decade, pushing road-salt call-off volumes 15-20% higher and straining municipal reserves. Precision spreaders and real-time weather telemetry trim usage 10-15%, yet calcium chloride and organic acetate blends are winning share in environmentally sensitive corridors despite cost premiums exceeding 200%.

Ultra-High-Purity Salt for Next-Gen Membranes

Membrane suppliers to semiconductor fabs stipulate 99.8% sodium chloride with sub-10 ppm trace metals, achievable only through multi-effect vacuum evaporation coupled with hydro-extraction. Sodium-ion battery developers demand battery-grade feedstock free of sulfate contaminants, opening adjacent revenue streams for integrated salt-chemical producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter EU/US Brine-Discharge Regulations | -0.5% | North America and EU primarily | Short term (≤ 2 years) |

| Substitution by CaCl₂ and Organic De-Icers | -0.3% | North America and EU cold regions | Medium term (2-4 years) |

| Opposition to Inland Solution Mining Near Aquifers | -0.2% | Regional, concentrated in water-stressed areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tighter EU/US Brine-Discharge Regulations

U.S. EPA Rule 82 (2024) lifts monitoring and bonding costs by up to USD 5 million per well, while EU directives cap chloride discharges at 250 mg/L in sensitive basins. Mid-size facilities must budget USD 10-20 million for crystallizers or face closure, shifting supply to integrated majors with existing wastewater assets.

Substitution by CaCl₂ and Organic De-Icers

Calcium chloride now holds 15-20% of premium de-icing spend because it operates below -15 °C and reduces road-salt volumes by roughly one-third. Airports increasingly favor potassium acetate for runway clearance, despite unit prices five times higher, due to mandated corrosion metrics. Municipal tenders weigh life-cycle corrosion costs, nudging adoption of brine pretreatment systems that cut overall sodium chloride use by 20-30%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Rock Salt Prevails, Brine Gains Specialty Share

Rock salt controlled 57.10% of the industrial salts market in 2025, supported by mature underground mines and established rail and barge logistics. The segment should post a 2.73% CAGR through 2031 as de-icing and general chemical uses sustain baseline demand. Natural brine remains smaller but captures higher-value slots in pharmaceutical and membrane-grade supply chains, especially where solution-mining mitigates land disturbance.

Natural brine’s growth hinges on rising purity needs and environmental pressure against deep-shaft mining. Solution wells paired with pressure-retarded osmosis increase brine concentration efficiencies, while selective extraction curbs aquifer mixing. Producers in China’s Qinghai basin and the U.S. Great Lakes are piloting dual-purpose brine schemes that co-produce lithium concentrates, introducing optionality and raising realized prices per ton.

By Manufacturing Process: Solar Evaporation Dominant, Vacuum Evaporation Fastest

Solar evaporation delivered 45.20% of 2025 volume, exploiting high-insolation coastal flats in Australia, China, and Mexico. Ample pond acreage and minimal energy inputs keep operating costs low, but land intensity and weather variability pose constraints. Vacuum evaporation will expand at 2.79% CAGR to 2031 as heat-pump integration and mechanical vapor recompression drive energy use below 25 kWh per ton, enabling premium multi-grade outputs.

Conventional mining retains a foothold where thick halite beds align with rail corridors, yet tailings management, subsidence, and brine disposal rules inflate sustaining capital. Several European mines are trialing backfill cemented paste techniques to cut surface impacts, while North American operators test automated continuous miners to raise productivity.

By Application: Chemical Processing Strength Meets Water Treatment Upswing

Chemical processing owned 68.95% of the industrial salts market share in 2025, anchored by chlorine, caustic soda, soda ash, and chloro-vinyl chains. Membrane-cell conversions intensify purity filters, spurring investments in triple-wash centrifuges and inline spectrographic controls.

Water treatment, though smaller, is on track for a 2.87% CAGR to 2031 as utilities in India, Southeast Asia, and the Gulf install reverse-osmosis and nanofiltration trains. Ion-exchange regenerant salt for softening and de-alkalization helmets industrial boiler make-up water, lifting demand for low-sulfate grades. De-icing remains cyclical; however, precision application and anti-icing brines temper growth, while the oil-and-gas segment follows U.S. drilling cycles and Middle Eastern produced-water requirements.

Geography Analysis

Asia-Pacific accounted for 45.50% of global volume in 2025 and is expected to log a 2.82% CAGR to 2031. China produces over 95 million tons annually, allocating nearly 60% to industrial routes. India’s consumption rises 4-5% each year on pharmaceuticals and municipal water upgrades. Indonesia and Thailand open new solar ponds and brine wells to feed chlor-alkali and aquaculture operations.

North America ranks second, consuming roughly 40 million tons a year in 2025. Road safety agencies absorb 35-40% of U.S. tonnage during winter peaks, while Midwest chemical clusters draw high-purity feedstock from Great Lakes mines. Canadian operators face stricter brine-discharge permits near the Prairie Potash region, and Mexican solar projects expand to capture U.S. Gulf Coast chemical import demand.

Europe is mature but regulation-intensive. Germany leads with 12 million tons purchased in 2024, driven by chlor-alkali and pharma grade demand. The U.K. and France keep large de-icing programs, yet organic acetates grow fastest under environmental mandates. Middle East and Africa exhibit the highest relative upside; Saudi Arabia leverages desert solar evaporation for export-oriented chlorine derivatives, while South Africa integrates salt into diversified mining portfolios.

Competitive Landscape

The industrial salts market remains moderately fragmented, though scale and integration offer decisive advantages. Compass Minerals cut 10% of corporate headcount in March 2025, projecting USD 11-13 million annual cash savings and narrowing its focus on salt and plant nutrition[2]Compass Minerals, “Form 10-K 2025,” compassminerals.com . K+S, Rio Tinto’s divested Lake MacLeod asset, and emerging Middle Eastern ventures round out a top tier that collectively holds near-40% of global capacity.

Technology differentiation centers on vacuum evaporation retrofits, real-time impurity scanning, and zero-liquid-discharge crystallizers. Producers able to certify 99.8% purity capture semiconductor and battery channels at margins 2-3 times commodity rock-salt. Drone-guided solar-pond monitoring is boosting yields by 3-5% in Australia and Oman, while U.S. operators deploy automated continuous miners to trim labor intensity.

Regulation acts as both barrier and moat. EPA Rule 82 and EU chloride caps elevate compliance costs but favor firms with sunk wastewater and tailings infrastructure. Constrained junior miners pivot to service brine-to-lithium tolling, whereas majors hedge by partnering with battery-grade sodium manufacturers. The market’s shift from volume to value underscores innovation, sustainability, and contiguous chemical integration.

Industrial Salts Industry Leaders

Cargill, Incorporated

K+S Aktiengesellschaft

Compass Minerals

Rio Tinto

China National Salt Industry Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Minerals Development Oman (MDO) signed a partnership agreement with Dev Salt Pvt Ltd to establish the Naqa Salt Project in Wilayat Mahout, Al Wusta Governorate. The solar-powered evaporation technology project will produce high-purity bromine-rich industrial salt.

- September 2024: QatarEnergy, through its TAWTEEN localization program, formed a joint venture with Mesaieed Petrochemical Holding Company (MPHC), Qatar Industrial Manufacturing Co. (QIMC), and Turkey's Atlas Yatirim to create Qatar Salt Products Company (QSalt) in Um Al Houl, Qatar. The facility aims to produce 1 million tons of industrial and food-grade salt annually using reject water from reverse osmosis desalination units, reducing Qatar's dependence on salt imports.

Global Industrial Salts Market Report Scope

Industrial salts are mainly consumed by the chemical industry to produce caustic soda and other chloralkali products and are also used in the manufacturing of polyester, glass, paper, tires, brass bleach, as well as used to set dye in the fabric. Industrial salts are available in various levels of purity, depending on the applications. The industrial salts market is segmented by Source, Manufacturing Process, Application, and Geography. By Source, the market is segmented into Rock Salt and Natural Brine. By Manufacturing Process, the market is segmented into Solar Evaporation, Vacuum Evaporation, and Conventional Mining. By Application, the market is segmented into Chemical Processing, Water Treatment, De-icing, Agriculture, Oil and Gas, and Other Applications. The report also covers the market size and forecasts for the industrial salts market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilotons).

| Rock Salt |

| Natural Brine |

| Solar Evaporation |

| Vacuum Evaporation |

| Conventional Mining |

| Chemical Processing |

| Water Treatment |

| De-icing |

| Oil and Gas |

| Agriculture |

| Food Processing |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Rock Salt | |

| Natural Brine | ||

| By Manufacturing Process | Solar Evaporation | |

| Vacuum Evaporation | ||

| Conventional Mining | ||

| By Application | Chemical Processing | |

| Water Treatment | ||

| De-icing | ||

| Oil and Gas | ||

| Agriculture | ||

| Food Processing | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global volume for industrial salts?

The industrial salts market size stood at 243.73 million tons in 2026.

How fast is demand expected to grow?

Global volume is projected to reach 271.33 million tons by 2031, showing a 2.17% CAGR.

Which region leads in consumption?

Asia-Pacific commands about 45.50% of worldwide demand, fueled by chlor-alkali expansions.

Which application is expanding fastest?

Water treatment is advancing at a 2.87% CAGR thanks to membrane-based upgrades in municipalities.

Page last updated on: