Market Overview

| Study Period | 2021 - 2031 |

|---|---|

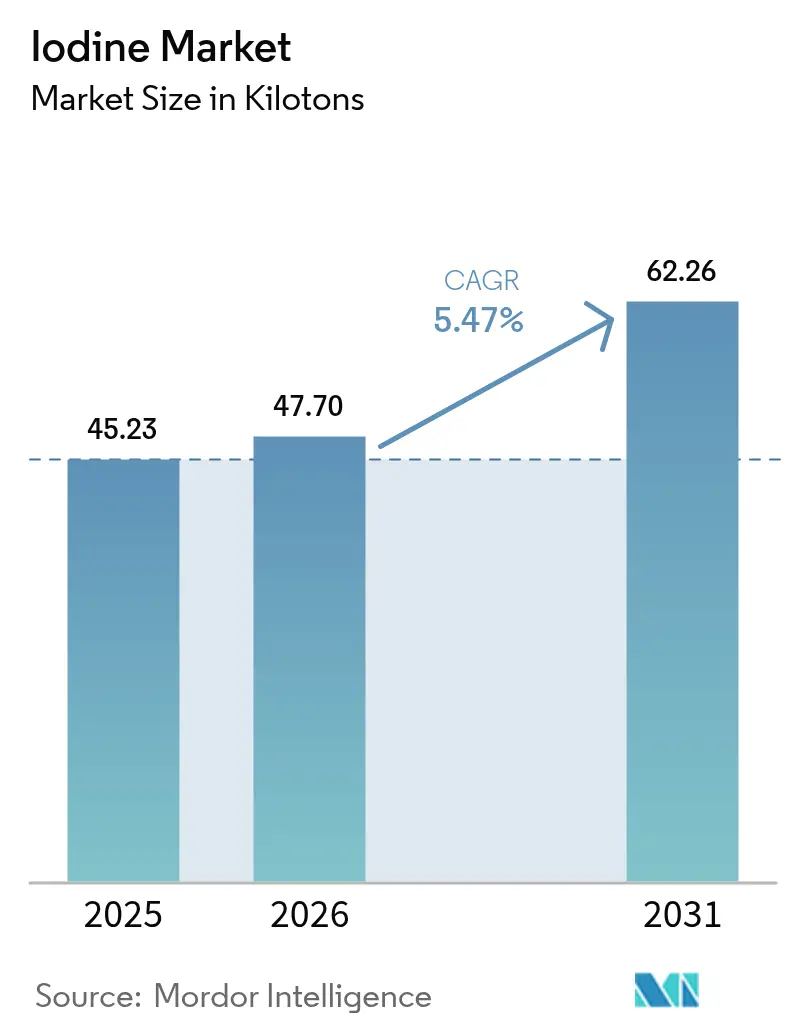

| Market Volume (2026) | 47.70 kilotons |

| Market Volume (2031) | 62.26 kilotons |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iodine Market Analysis by Mordor Intelligence

The Iodine Market size is projected to expand from 45.23 kilotons in 2025 and 47.70 kilotons in 2026 to 62.26 kilotons by 2031, registering a CAGR of 5.47% between 2026 to 2031. Structural shifts are broadening demand beyond traditional pharmaceuticals and nutrition, most notably toward low-carbon fluorochemical catalysts and next-generation aqueous battery electrolytes that position iodine as a critical enabler of decarbonization strategies. Spot prices climbed 40% in 2024 to USD 38,000 per ton as Chilean caliche output tightened, signaling sustained supply risk for buyers that lack long-term contracts. Underground brine operators are scaling proprietary extraction technologies to mitigate weather-driven volatility, while closed-loop recycling programs in Europe and Japan are beginning to recapture medical-grade molecules, albeit at modest volumes. Grid-scale zinc-iodine batteries that deliver more than 10,000 charge–discharge cycles are moving from laboratory proof-of-concept toward industrial pilots, underpinning a potential step-change in industrial offtake during the latter half of the forecast period.

Key Report Takeaways

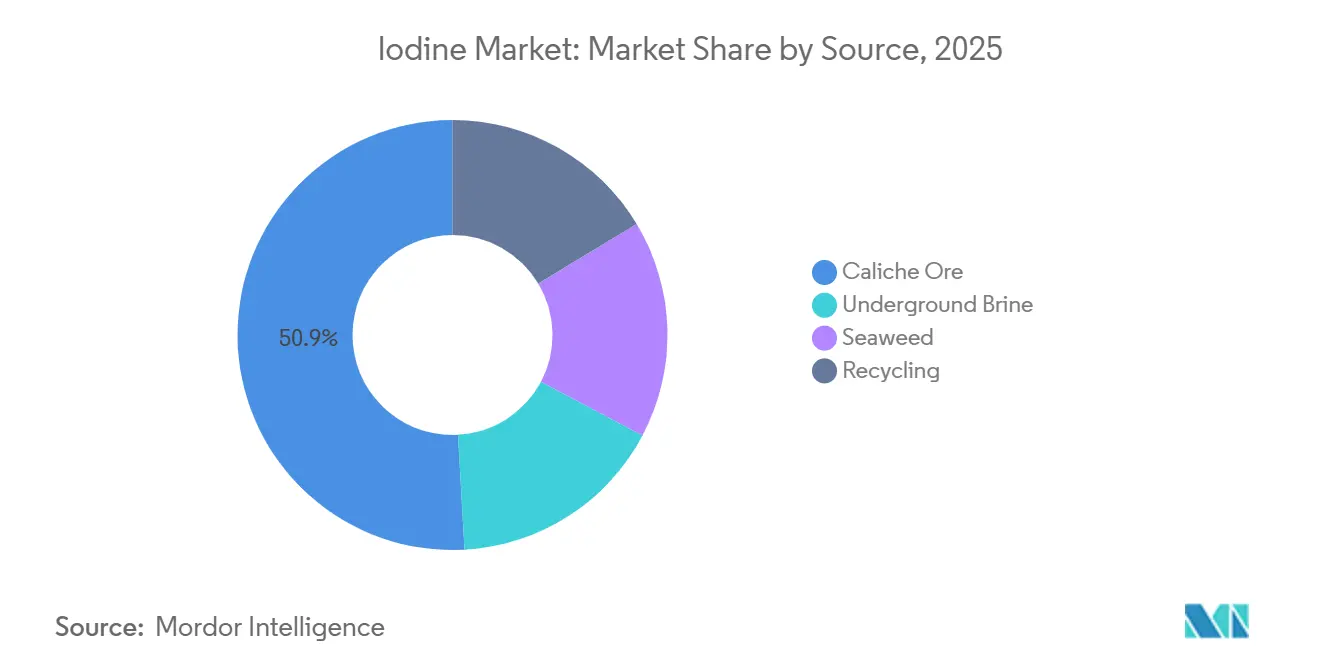

- By source, caliche ore held 50.88% of the iodine market share in 2025, while underground brine extraction is projected to expand at a 5.56% CAGR through 2031.

- By form, organic compounds accounted for 48.23% of the iodine market size in 2025; inorganic salts and complexes represent the fastest-growing form segment at a 5.68% CAGR through 2031.

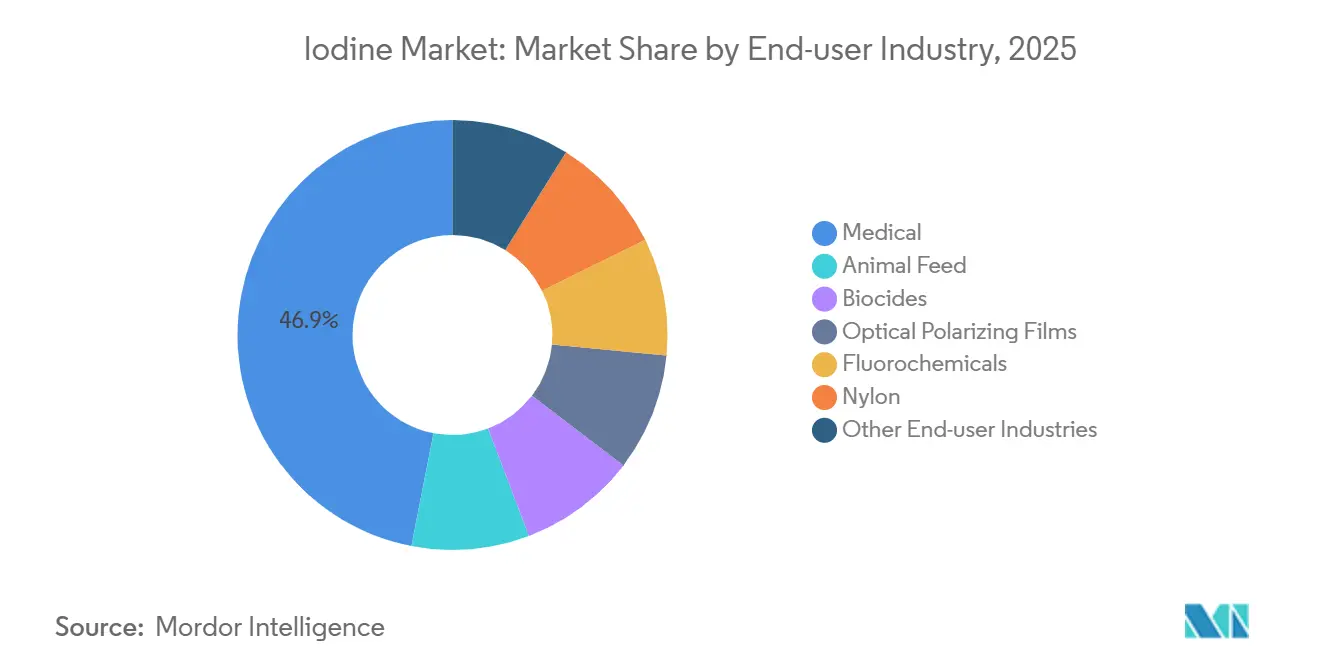

- By end-user industry, the medical segment captured 46.93% of 2025 volume and is advancing at a 5.66% CAGR through 2031.

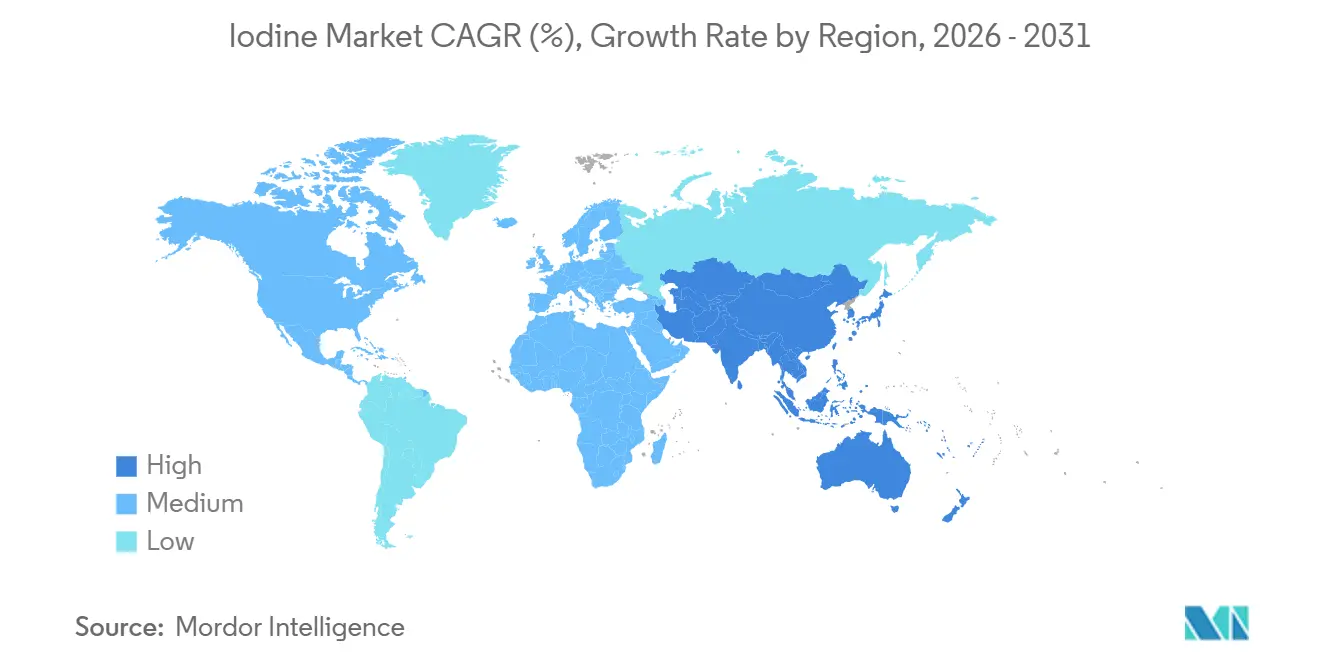

- By geography, Asia-Pacific commanded 34.31% of 2025 demand and is outpacing all regions with a 6.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Iodine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for X-Ray/CT Contrast Media | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Government-Mandated Salt Iodization Programs | +0.8% | Global, particularly India, Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Expansion of LCD/OLED Polarizer Film Manufacturing | +0.9% | Asia-Pacific core (China, South Korea, Japan), spill-over to North America | Short term (≤ 2 years) |

| Rapid Adoption of Iodine-Based Electrolytes in Next-Gen Aqueous Batteries | +1.4% | Global, early adoption in China, US, EU for grid-scale storage | Medium term (2-4 years) |

| Regulatory Push for Low-Carbon Fluorochemical Routes That Require Iodine Catalysts | +0.6% | North America and EU, with emerging interest in Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for X-Ray/CT Contrast Media

Roughly 75 million diagnostic exams per year use iodinated contrast agents, and about 48% of U.S. CT scans require contrast enhancement. GE Healthcare invested USD 30 million in its Cork, Ireland plant during 2024 to secure additional supply as global contrast demand is expected to double within a decade. Photon-counting CT technology lowers per-patient iodine usage by around 10% per 5 keV energy bin, yet absolute volumes keep rising as screening programs expand. SQM signed multi-year feedstock contracts with pharmaceutical intermediaries to lock in medical-grade output at premium pricing, insulating revenue from commodity swings. The WHO lists iodinated contrast agents on its essential medicines inventory, guaranteeing baseline procurement even in low-income health systems.

Government-Mandated Salt Iodization Programs

Roughly 88% of households used iodized salt in 2024, up from 86% in 2020, yet more than 2 billion people remain at risk of deficiency. India’s 2024 mandate for double fortification with iodine and iron has lifted per-kilogram iodine loading, expanding the iodine market across rural retail channels. Southeast Asian and Sub-Saharan regulators are tightening compliance audits, raising the technical threshold for suppliers that must now document ISO 9001 traceability. Low-purity grades funneled into fortification create a price floor that stabilizes producer cash flows during cyclical downturns in higher-spec segments. UNICEF’s bulk procurement favors vendors with proven logistics, elevating barriers for small regional entrants.

Expansion of LCD/OLED Polarizer Film Manufacturing

Iodine-doped polyvinyl alcohol enables the dichroic polarizing layer in LCD and OLED displays at concentrations up to 5 mol %. Kuraray is adding 38 million m² of optical-grade PVA film capacity, supporting growth in large-screen TVs and automotive cockpit displays. ISE Chemicals estimates polarizer films already absorb roughly 8% of global iodine, and share is expected to grow as foldable phones and augmented-reality headsets scale. China controls over half of global LCD capacity, concentrating demand in Guangdong and Jiangsu where proximity to Japanese and Chilean supply chains trims freight costs. South Korean panel makers protect margins through proprietary iodine purification, preserving long-term contracts over volatile spot purchases.

Regulatory Push for Low-Carbon Fluorochemical Routes

Iodine catalyzes isomerization steps in low-GWP fluorochemical manufacturing, a pathway favored by the EU F-Gas phase-down and Kigali Amendment compliance schedules. Organoiodine mediators in electrocatalytic chlorination reduce greenhouse emissions compared with chlorine-intensive sequences. Producers that retrofit plants to iodine-enabled flows boost ISO 14001 scores, gaining procurement preference from automotive and refrigeration OEMs. NREL estimates about 16% of iodine now serves industrial catalysis, a share likely to rise as petrochemical decarbonization accelerates[1]National Renewable Energy Laboratory, “Organoiodine Catalysts in Low-Carbon Fluorochemicals,” nrel.gov . Because capex cycles exceed 4 years, the demand inflection is back-loaded but already visible in multiyear supply agreements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Pricing Linked to Chilean Caliche Output Swings | -0.9% | Global, with acute exposure in Asia-Pacific and North America import-dependent markets | Short term (≤ 2 years) |

| Toxicity and Specialised Handling Costs for Bulk Iodine | -0.5% | Global, particularly affecting smaller distributors and emerging-market buyers | Medium term (2-4 years) |

| Tightening EU Limits on Residual Iodine in Dairy Products | -0.3% | Europe, with indirect effects on global animal feed formulation practices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Pricing Linked to Chilean Caliche Output Swings

Chile supplies roughly 60% of world iodine, and 2024 precipitation events in the Atacama Desert curtailed ore processing, pushing spot prices to USD 38,000 t⁻¹ from USD 27,000 t⁻¹ the prior year. Asia-Pacific buyers face 8–12-week transit windows, and strategic stockpiles seldom exceed 60 days, magnifying volatility. Underground brine output is scaling at a 5.56% CAGR but remains an order of magnitude smaller than caliche, limiting near-term diversification. Producers with long-term offtake contracts are better cushioned, yet converters in contrast media and catalysts report margin compression when spot jumps exceed USD 5,000 t⁻¹. Weather risk and nitrate-mining cycles therefore remain the leading supply-side drag on the iodine market.

Toxicity and Specialized Handling Costs for Bulk Iodine

Elemental iodine sublimes and is corrosive, necessitating UN 3077 hazardous-goods routing and OSHA ceiling exposure of 0.1 ppm[2]U.S. OSHA, “Occupational Exposure Limits for Iodine,” osha.gov . Logistics premiums average 15-20% above non-hazardous chemicals, an outsized burden for small distributors that lack dedicated ventilation or storage. ISE Chemicals’ ISEFLO prills cut dust yet command a 5-10% surcharge, forcing price-sensitive buyers into a quality-cost dilemma. Carriers with hazmat certifications are in short supply across South Asia and Sub-Saharan Africa, extending lead times. These frictions consolidate share among large incumbents and cap penetration in emerging use cases unless safer derivatives gain traction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Brine Extraction Outpaces Legacy Caliche

Caliche ore still held 50.88% of the iodine market share in 2025, anchored by SQM’s 16,200 t output, yet underground brine is growing faster at a 5.56% CAGR, reflecting end-users’ pursuit of supply diversity. The iodine market size attributable to brine is projected to rise as operators such as Iofina commission new wells in the U.S. Permian Basin.

Brine production bypasses nitrate-mining cycles and exploits flowback water that would otherwise be reinjected, lowering marginal extraction costs despite iodine grades below 0.1 g L⁻¹. Japanese firms extracting brine at roughly 1,000-fold seawater concentration supply 30% of global volume, proving commercial viability. Recycling—led by GE Healthcare’s take-back network—recovered 18% of iodine used in contrast agents during 2025, signaling white-space for closed-loop growth. Seaweed now accounts for low supply because of labor intensity and low yields.

By Form: Organic Compounds Lead, Inorganic Salts Accelerate

Organic compounds captured 48.23% of the iodine market size in 2025 as tri-iodinated contrast media and povidone-iodine antiseptics dominated value-added consumption. In contrast, inorganic salts and complexes are advancing at a 5.68% CAGR, buoyed by mandatory fortification schemes.

The iodine market share of elementals and isotopes remains low but commands high price points in nuclear medicine. Feed-grade ethylenediamine dihydroiodide supports dairy fertility. Rising environmental scrutiny is steering some formulators toward organic complexes with improved uptake, adding complexity to procurement strategies.

By End-user Industry: Medical Segment Sustains Leadership

The medical segment captured 46.93% of the iodine market share in 2025 on the back of roughly 75 million annual diagnostic exams that rely on contrast agents, and it is set to advance at a 5.66% CAGR through 2031. Within this segment, GE Healthcare’s USD 30 million expansion in Cork underpins rising demand as photon-counting CT scanners enter service across North America and Europe, reducing per-exam dosage but widening overall procedure counts.

Animal feed is absorbing ethylenediamine dihydroiodide and potassium iodide at roughly 0.35–0.8 mg kg⁻¹ inclusion rates for poultry and dairy cattle, yet tightening EU residue caps on milk are curbing growth prospects in Europe. Display manufacturing is growing as iodine-doped polyvinyl alcohol films scale with larger televisions, automotive clusters and foldable phones, helped by Kuraray’s 38 million m² annual capacity addition. Catalysts used in low-carbon fluorochemical routes consume about 16% of global iodine, a proportion that is expected to edge higher as industrial emitters retrofit plants in response to the Kigali Amendment. Biocides such as povidone-iodine maintain demand in hospital and consumer antiseptics, having shown 99.99% virucidal efficacy against SARS-CoV-2 at 0.5% strength.

Geography Analysis

Asia-Pacific led the iodine market with 34.31% of world demand in 2025 and is expanding at a 6.89% CAGR through 2031. China’s LCD polarizer film production and India’s double-fortified salt program underpin the region’s volume gains. Japan, sourcing brine at 0.1 g L⁻¹, remains a pivotal supplier to downstream processors across the bloc.

North America benefits from rising brine output, notably Iofina’s additional 170-220 t yr⁻¹ Permian plant slated for H2 2026. Europe remains contrast-media-centric; GE Healthcare’s Cork expansion reinforces supply security yet faces headwinds from stricter dairy residue caps.

South America supplies majority of global iodine via Chilean caliche, but weather disruptions and water scarcity inject volatility. UNICEF-led iodization drives incremental demand across Sub-Saharan Africa, though logistics barriers persist.

Competitive Landscape

Chile and Japan jointly deliver majority of supply, yet SQM’s 30% individual share leaves room for mid-tier players, producing a moderately concentrated iodine market. Iofina’s WET IOsorb technology exemplifies how brine innovation can erode caliche dominance and unlock regional offtake integration. GE Healthcare’s material-take-back scheme points to circular-economy models that may become differentiators in pharmaceutical procurement.

Technology is a key moat: ISE Chemicals markets prilled formats that lower dust exposure, while GODO SHIGEN specializes in high-purity reclamation from waste streams. The absence of cross-border mega-mergers suggests partnerships and licensing will shape the competitive map more than consolidation. Emergent battery players could realign the demand profile if grid storage achieves mass deployment.

Iodine Industry Leaders

Cosayach

Iofina plc

SQM

Algorta Norte S.A.

GODO SHIGEN Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Iofina plc collaborated with Western Midstream to build a new IOsorb plant in the Permian Basin, located between western Texas and southeastern New Mexico. The plant added 170-220 tons per year (t/yr) of iodine production capacity and expected to have a total processing capability of approximately 50,000 barrels of brine water per day.

- September 2024: Iofina plc commissioned its IO#10 WET IOsorb extraction plant in Oklahoma in September 2024 to enhance iodine production by utilizing brine from oil and gas operations. This facility, the seventh in the region, contributed an additional 100-150 metric tons (MT) of crystalline iodine capacity annually.

Global Iodine Market Report Scope

Iodine is known as a chemical material that turns purple by reacting with starch and being contained in various seaweed types. Iodine and its derivatives are indispensable in a wide range of nutritional, pharmaceutical, and industrial applications.

The iodine market is segmented by source, form, end-user industry, and geography. By source, the market is segmented into caliche ore, underground brine, seaweed, and recycling. By form, the market is segmented into organic compounds, elementals and isotopes, and inorganic salts and complexes. By end-user industry, the market is segmented into medical (X-ray contrast media, pharmaceuticals, iodophors, and povidone-iodine), animal feed, biocides, optical polarizing films, fluorochemicals, nylon, and other end-user industries. The report also covers the market size and forecasts for the iodine in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

By Source

| Caliche Ore |

| Underground Brine |

| Seaweed |

| Recycling |

By Form

| Organic Compounds |

| Elementals and Isotopes |

| Inorganic Salts and Complexes |

By End-user Industry

| Medical (X-ray contrast media, pharmaceuticals, iodophors and povidone-iodine) |

| Animal Feed |

| Biocides |

| Optical Polarizing Films |

| Fluorochemicals |

| Nylon |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Source | Caliche Ore | |

| Underground Brine | ||

| Seaweed | ||

| Recycling | ||

| By Form | Organic Compounds | |

| Elementals and Isotopes | ||

| Inorganic Salts and Complexes | ||

| By End-user Industry | Medical (X-ray contrast media, pharmaceuticals, iodophors and povidone-iodine) | |

| Animal Feed | ||

| Biocides | ||

| Optical Polarizing Films | ||

| Fluorochemicals | ||

| Nylon | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is iodine demand growing in medical imaging?

The medical segment is advancing at a 5.66% CAGR through 2031 and already represents 46.93% of global volume.

What is the main supply risk for buyers today?

Weather-related disruptions to Chilean caliche mines can swing spot prices by more than 40%, making geographic concentration the top risk factor.

Will underground brine replace caliche as the leading source?

Brine extraction is growing faster, yet caliche still holds over half of global volume; meaningful parity is unlikely before 2031.

How might zinc-iodine batteries influence future demand?

If the chemistry secures even 5% of projected grid-storage deployments by 2030, iodine demand could rise by roughly 3,000 t yr⁻¹.

What is current market size of Iodine Market?

The Iodine Market size is projected to expand from 45.23 kilotons in 2025 and 47.70 kilotons in 2026 to 62.26 kilotons by 2031, registering a CAGR of 5.47% between 2026 to 2031.

Page last updated on: