Chlor-alkali Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

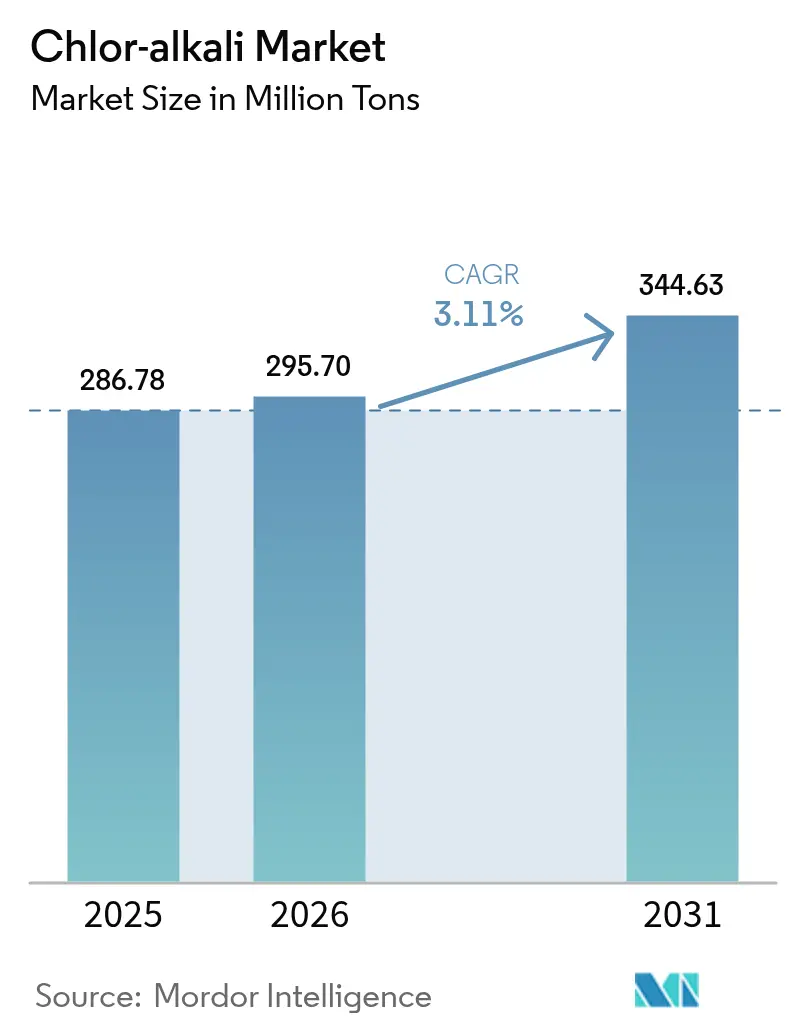

| Market Volume (2026) | 295.70 Million tons |

| Market Volume (2031) | 344.63 Million tons |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chlor-alkali Market Analysis by Mordor Intelligence

The Chlor-alkali Market size is expected to increase from 286.78 Million tons in 2025 to 295.70 Million tons in 2026 and reach 344.63 Million tons by 2031, growing at a CAGR of 3.11% over 2026-2031. End-use pull from vinyls, alumina, and water infrastructure is altering trade flows, tightening regional balances, and lifting average operating rates above 82%. Membrane-cell conversions in North America and Europe are lowering power intensity to below 2,000 kWh per ton of caustic, trimming Scope 2 emissions and unlocking hydrogen by-product revenue. Asia’s capacity additions have shifted 2 million tons of net chlorine demand eastward since 2024, while alumina refineries in Australia and China are front-loading long-term caustic offtake contracts to hedge against energy-price volatility. Zero-liquid-discharge rules and carbon pricing in the European Union are driving early retirement of small diaphragm and mercury units, accelerating capacity migration toward the Middle East where feedstock gas costs sit under USD 2 per MMBtu.

Key Report Takeaways

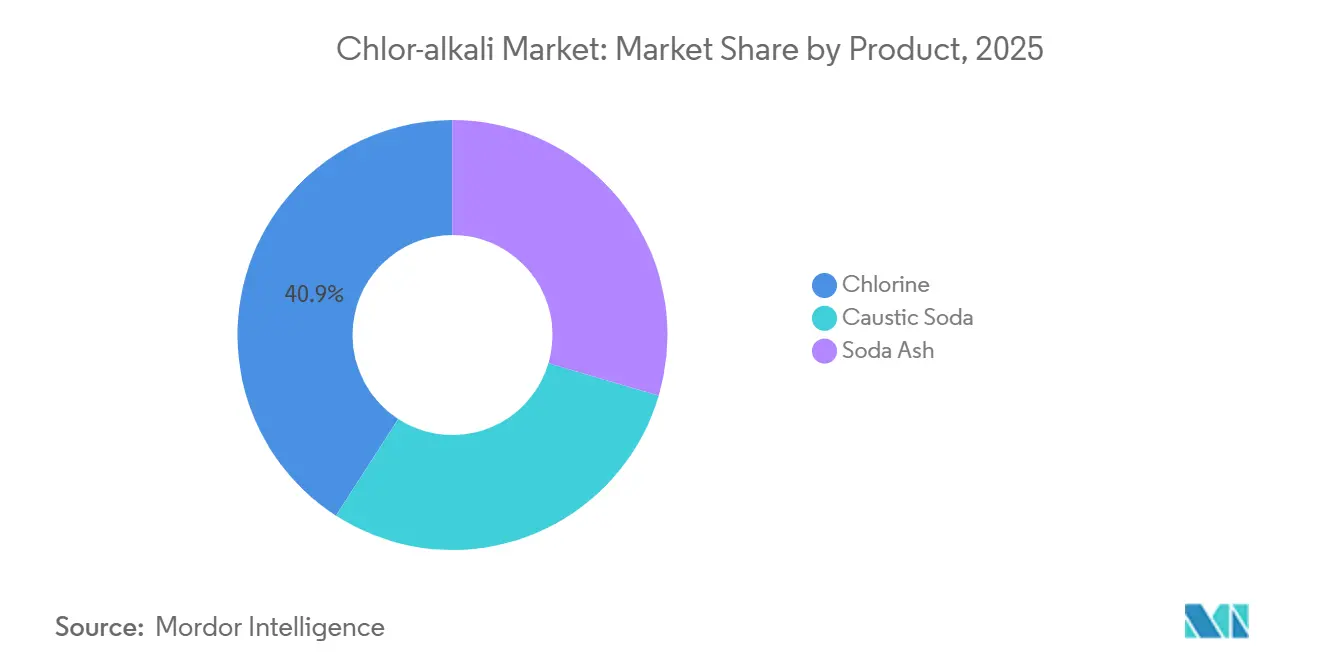

- By product, chlorine held 40.89% of the chlor-alkali market share in 2025 and is expanding at a 3.37% CAGR through 2031.

- By production process, membrane cell technology commanded 62.78% of the chlor-alkali market size in 2025 and is projected to grow at a 3.31% CAGR by 2031.

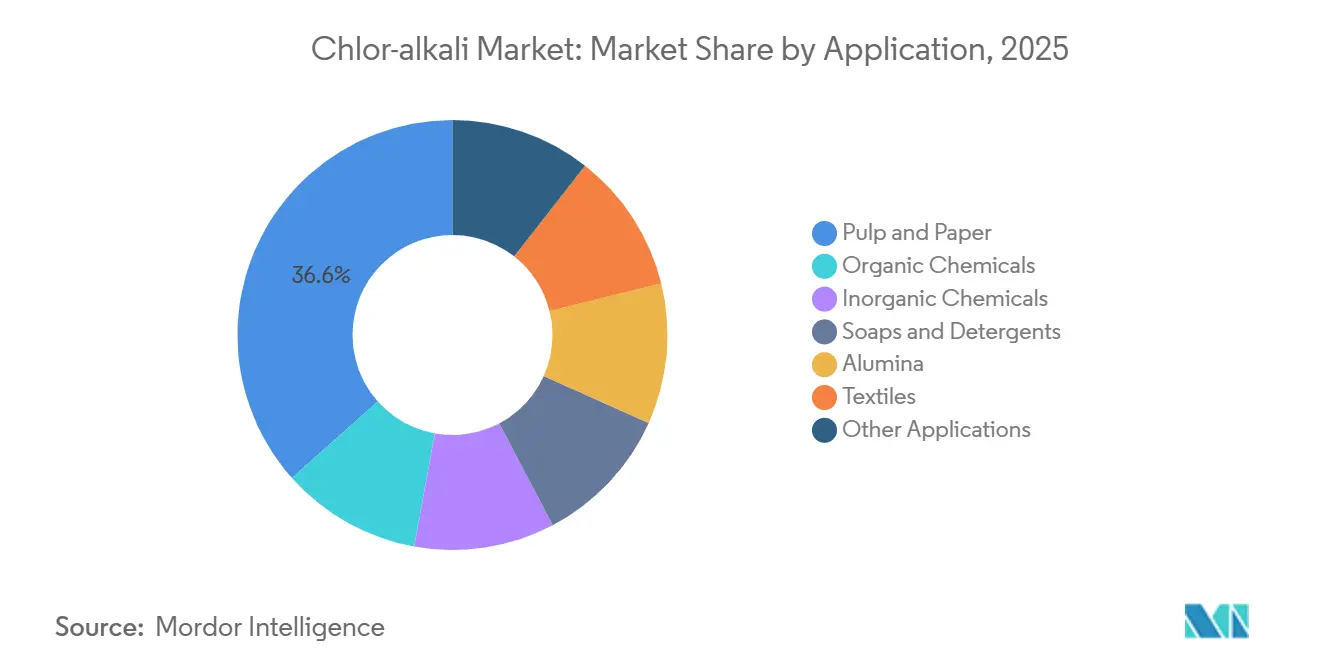

- By application, pulp and paper accounted for 36.58% of the chlor-alkali market size in 2025 and is advancing at a 3.22% CAGR to 2031.

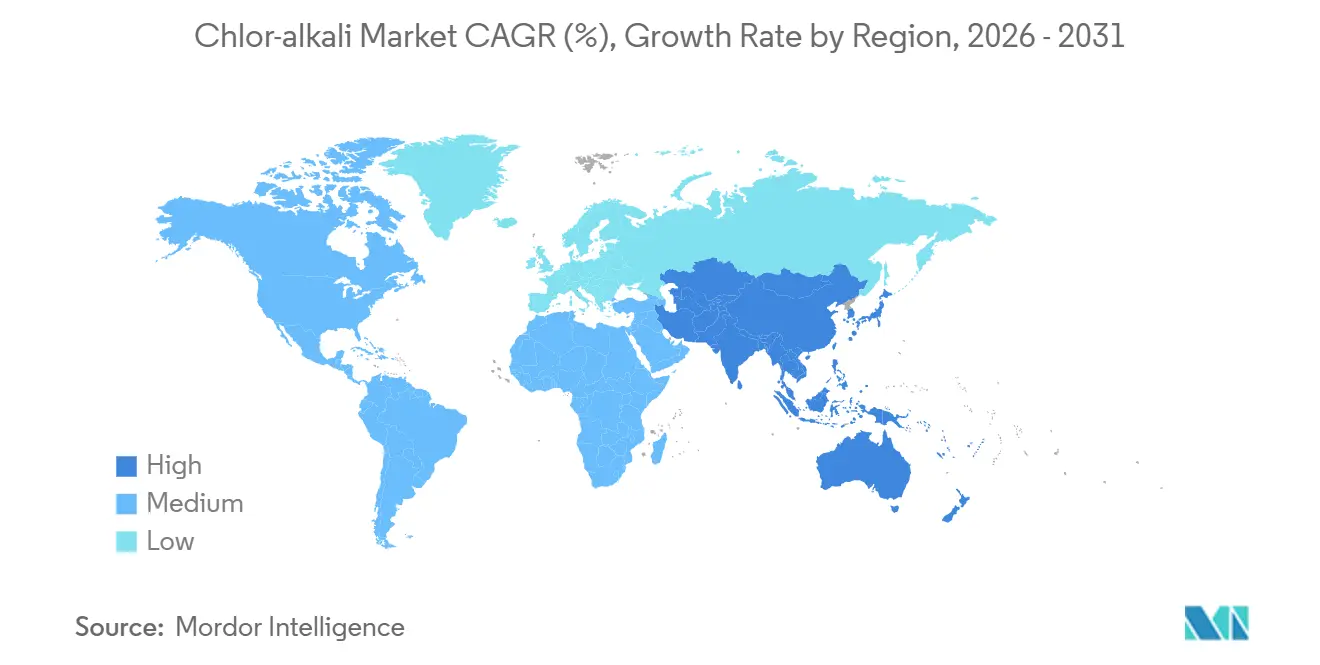

- By geography, Asia-Pacific captured 62.22% chlor-alkali market share in 2025 and is pacing ahead with a 3.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chlor-alkali Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging PVC capacity additions in Asia | +0.9% | China, India, Southeast Asia | Medium term (2-4 years) |

| Rising alumina output for EV-grade aluminium | +0.6% | China, Australia, India | Long term (≥ 4 years) |

| Booming water and wastewater projects | +0.5% | North America, Europe, India | Medium term (2-4 years) |

| Capacity-linked renewable-power incentives | +0.4% | Australia, European Union, select U.S. states | Long term (≥ 4 years) |

| Local hydrogen valorisation at membrane sites | +0.3% | Europe, Australia, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging PVC Capacity Additions in Asia

China commissioned 1.9 million tons of PVC in 2025, lifting Q4 output to 6.54 million tons and absorbing roughly 3.8 million tons of chlorine, while India’s 2.8 million-ton structural PVC deficit is prompting 1.5 million tons of new capacity at Dahej and Cuddalore. Each ton of PVC fixes 0.58 tons of chlorine, anchoring plant load factors even when caustic prices soften. Coastal clustering in China and Gujarat lowers inbound salt and outbound caustic logistics, letting producers arbitrage surplus caustic into Australia during monsoon-season outages. Southeast Asian joint ventures are adding another 1 million tons of PVC by 2027, sustaining regional chlorine tightness. The investment wave is also triggering rapid membrane retrofits to achieve the high-purity caustic grades alumina refiners require[1]Thyssenkrupp Uhde, “Chlor-Alkali Electrolysis Technology Brochure,” thyssenkrupp-uhde.com.

Rising Alumina Output for EV-Grade Aluminium

The Bayer process needs 0.08-0.12 tons of caustic per ton of alumina. IRENA projects 4-6 million tons of incremental alumina demand for EV casings by 2030, equal to 400,000-600,000 tons of extra caustic[2]International Renewable Energy Agency, “Battery Materials Supply Chain 2024,” irena.org. Rio Tinto’s 8.3 million-ton refining network is negotiating embedded-carbon clauses with membrane-cell suppliers to cut logistics miles by 30%. The European Commission’s decarbonisation pathway for aluminium privileges low-carbon caustic, enabling premium supply contracts for producers using renewable PPAs. Sodium-ion battery cathodes, an emerging storage option, also rely on caustic in precursor synthesis, cushioning demand against cyclicality.

Booming Water and Wastewater Treatment Projects

The US EPA ordered Jackson, Mississippi, to switch from bulk chlorine to on-site hypochlorite by August 2027, creating a USD 45 million equipment opportunity despite trimming 12,000 tons of merchant chlorine demand. India’s Jal Jeevan Mission has lifted rural piped-water coverage to 85%, underpinning steady chlorine consumption for residual disinfection. Desalination capacity in the Middle East reached 95 million m³ per day in 2025 and is rising 8% annually, with each plant dosing chlorine for biofouling protection. Electro-chlorination improves safety and trims insurance costs by 35%, but chlorine remains dominant where residual protection is mandated.

Capacity-Linked Renewable-Energy Incentives

Australia’s Hydrogen Production Tax Incentive pays AUD 2 per kg of qualifying hydrogen; a chlor-alkali plant co-producing 0.028 tons of hydrogen per ton of caustic captures USD 36-40 per ton of extra revenue. The U.S. chlor-alkali fleet already vents 0.7 million tons of hydrogen, 10% of national consumption, so valorisation can shave 8-12% off caustic cash costs. EU RED III lets chlor-alkali hydrogen count toward RFNBO quotas when powered by low-carbon electricity, spurring Nordic producers to sign wind PPAs at sub-EUR 40 per MWh.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent carbon-footprint regulations | -0.5% | Europe, North America, China | Medium term (2-4 years) |

| Brine-disposal compliance costs | -0.3% | United States, Europe, India (coastal) | Short term (≤ 2 years) |

| Uptake of electro-chlorination & ClO₂ | -0.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Carbon-Footprint Regulations on the Value Chain

EU ETS allowances averaged EUR 72 per ton in 2025; a membrane plant using coal-based power emits 0.9 tons CO₂ per ton of caustic, implying a EUR 65 cost penalty. The Carbon Border Adjustment Mechanism, in its reporting phase since 2026, adds compliance overhead for importers of chlor-alkali derivatives. China folded chemicals into its national ETS in 2024, benchmarking 2,200 kWh t⁻¹ for membrane cells, which is forcing high-energy Xinjiang units offline. The US facilities must now file process-emission inventories under EPA’s Greenhouse Gas Reporting Program.

Brine-Disposal Compliance Costs

Zero-liquid-discharge rules in California, Florida, and Gujarat mandate evaporators and RO units that cost USD 15-25 million per site and add USD 10/t to opex. Olin budgeted USD 42 million in 2024 for brine systems at Charleston and McIntosh. Diaphragm plants generate 1.4 m³ effluent per ton of caustic versus 0.4 m³ for membrane units, magnifying retrofit paybacks even before factoring in the EPA asbestos ban.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Chlorine Sustains Margin Leadership

Chlorine captured 40.89% of 2025 volume, anchoring 60% of integrated revenue as average realized prices stayed 15% above caustic. The chlor-alkali market size for chlorine is forecast to advance at a 3.37% CAGR as PVC, propylene oxide, and chlorinated solvents scale in Asia. Soda ash remains the smallest pool, exposed to synthetic competition in detergents but protected in flat glass where trona economics hold. Thyssenkrupp membranes deliver a 0.88:1 chlorine-to-caustic ratio, letting producers tailor output to regional pricing. HPPO technology could displace 0.3 tons of chlorine per ton of PO if installed capacity tops 3 million tons, a scenario industry planners view as post-2030. Integrated complexes at Point Comfort and Mailiao internalize full chlorine streams, insulating earnings from merchant-market swings.

Caustic soda underpins alumina refining, textiles, and pulp bleaching. Rio Tinto alone consumed 800,000 tons in 2024, and battery-grade aluminium growth signals a durable pull. However, detergent formulators continue shifting to enzyme-rich, low-alkali concentrates, trimming per-wash caustic intensity by 25%. Natural soda-ash mines in Wyoming and Turkey keep costs below synthetic routes, capping soda-ash substitution risk for glass customers.

By Production Process: Membrane Technology Dominates Post-Asbestos Ban

Membrane cells represented 62.78% of 2025 output and expand at a 3.31% CAGR as the the US EPA bans asbestos diaphragms by August 2026. Membrane upgrades cut power draw to 1,950 kWh/t and boost caustic purity to 50%, unlocking semiconductor and pharma niches priced at USD 600-800/t. The chlor-alkali market share for diaphragm technology is poised to fall below 5% by 2031. Mercury cells exit entirely under the Minamata Convention’s 2025 deadline. Retrofit economics are compelling: Westlake’s 2024 Calvert City project recycles 95% of brine, slashes freshwater intake, and meets tightened chloride limits, all while raising capacity 12%. High-current-density designs shrink cell footprints by 30%, letting greenfield plants in the Middle East break even below USD 300/t FOB.

Hydrogen valorisation is another upside. Pure-stream hydrogen at 99.9% enables sales into ammonia or mobility markets at sub-USD 2/kg when renewable power runs below USD 40/MWh, improving internal rates of return by 3-4 percentage points.

By Application: Pulp & Paper Anchors Demand Profile

Pulp and paper consumed 36.58% of chlor-alkali volume in 2025 and is tracking a 3.22% CAGR. Elemental-chlorine-free bleaching still needs chlorine dioxide precursors plus caustic for kraft pulping. Brazilian and Indonesian mills expanded hardwood capacity by 3 million tons between 2024 and 2026, underpinning caustic off-take contracts with ISO 14067 clauses. Organic chemicals, led by PVC, represent the fastest absolute growth, pulling 0.58 tons of chlorine per ton of resin. Inorganic chains such as TiO₂ and sodium hypochlorite show steadier, low-single-digit growth yet pay premiums for 32% diaphragm-grade caustic.

Alumina refining, at 0.08-0.12 t caustic/t alumina, links chlor-alkali fortunes to EV battery rollout. Textiles remain a sizable outlet in South Asia but face water-recycling mandates that curb unit consumption. Food, pharma, and niche electronic-chemicals together form a 12-15% slice distinguished by high-purity premiums that cushion cyclical dips.

Geography Analysis

Asia-Pacific led the chlor-alkali market with 62.22% of global tonnage in 2025, propelled by China’s coastal PVC expansions and India’s persisting caustic deficit. The region’s chlor-alkali market size is forecast to chart a 3.23% CAGR through 2031 as integrated complexes secure brine and renewable power. Tata Chemicals is retrofitting 200,000 tons of membrane capacity at Mithapur, slicing energy costs by USD 38/t and positioning for exports into Australia. Japanese producers are pivoting to 99.5% purity grades for semiconductors, fetching USD 750/t ex-works. South Korean additions at Yeosu will feed in-house PVC and propylene oxide, capturing co-product credits.

In North America, diaphragm conversions and electro-chlorination substitution in water treatment offset demand upside from alumina refining. Olin’s Freeport and McIntosh upgrades add 8% capacity while trimming 50 kWh/t of electricity per ton. Occidental’s OxyChem unit intends to liquefy by-product hydrogen for Gulf refineries, targeting a USD 25/t uplift in caustic economics.

Europe battles the cost drag of EUR 35-40/MWh gas and EUR 65/t carbon. Covestro sources 60% renewable power at Dormagen, dropping carbon intensity below 0.5 t CO₂/t caustic and qualifying for green-premium contracts.INEOS is piloting hydrogen co-location with methanol at Rafnes to lift returns 10-15%. Turkey leverages low-cost trona and gas to ship soda ash and caustic into MENA.

In the Middle East and Africa, natural-gas-based power under USD 0.04/kWh and downstream PVC, alumina, and desalination investments make the basin a structural exporter to Europe and Asia. SABIC’s new Jubail membrane unit will tap wind-PPA blocks, cutting life-cycle CO₂ by 40%.

South America's market share is dominated by Brazilian PVC chains that enjoy captive eucalyptus feedstock for pulp bleach demand. Braskem’s Bahia expansion synchronizes chlorine, caustic, and vinyls, allowing net-back optimisation across three revenue streams.

Competitive Landscape

The Chlor-alkali market is moderately concentrated. Integrated strategies dominate. Formosa’s Point Comfort complex internalises 100% of chlorine into captive PVC, buffering margin swings. Dow leverages in-house ethylene and electricity cogeneration to trim cash costs by 12%. Occidental is monetising hydrogen into blue ammonia under long-term Gulf Coast contracts, adding USD 20/t to caustic value. Regulation is catalyzing consolidation. The EPA asbestos ban forces USD 150-200 million of retrofit spend on eight US diaphragm sites, a cost that smaller independents struggle to finance. EU CBAM reporting raises working-capital needs for traders, nudging them toward long-term offtake with low-carbon suppliers.

Chlor-alkali Industry Leaders

INEOS

Occidental Petroleum Corporation

Olin Corporation

Tata Chemicals Ltd

Westlake Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sisecam fully acquired Ciner Group’s position in the United States soda-ash sector, taking 100% control of Pacific Soda’s 5 million ton natural soda-ash venture and raising its Sisecam Wyoming stake to 51%, with NRP Trona retaining 49%.

- November 2024: Genesis Energy’s subsidiary Genesis Alkali signed a multi-year agreement to supply SolarCycle with “Ecosoda,” a low-carbon natural soda ash produced at the Granger facility.

Global Chlor-alkali Market Report Scope

Chlor alkali refers to a group of chemicals comprising chlorine (Cl2), sodium hydroxide (NaOH), and hydrogen (H2), which are produced simultaneously through the electrolysis of brine (sodium chloride solution). This industrial process involves passing an electric current through brine to separate it into its constituent elements. Chlor alkali products have a wide range of applications across industries, including chemical manufacturing, water treatment, pulp and paper production, and construction.

The chlor-alkali market is segmented by product, production process, application, and geography. By product, the market is segmented into caustic soda, chlorine, and soda ash. By production process, the market is segmented into membrane cell, diaphragm cell, and other processes. On the basis of application, the market is segmented into pulp and paper, organic chemicals, inorganic chemicals, soap and detergents, alumina, textiles, and other applications. The report also covers the market sizes and forecasts for the chlor-alkali market in 27 countries across the major regions. For each segment, the market size and forecast are provided based on volume (tons).

| Caustic Soda |

| Chlorine |

| Soda Ash |

| Membrane Cell |

| Diaphragm Cell |

| Other Processes |

| Pulp and Paper |

| Organic Chemicals |

| Inorganic Chemicals |

| Soaps and Detergents |

| Alumina |

| Textiles |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Turkey | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Product | Caustic Soda | |

| Chlorine | ||

| Soda Ash | ||

| By Production Process | Membrane Cell | |

| Diaphragm Cell | ||

| Other Processes | ||

| By Application | Pulp and Paper | |

| Organic Chemicals | ||

| Inorganic Chemicals | ||

| Soaps and Detergents | ||

| Alumina | ||

| Textiles | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Turkey | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume of the chlor-alkali market by 2031?

It is forecast to reach 344.63 million tons, reflecting a 3.11% CAGR during 2026-2031.

Which segment holds the largest chlor-alkali market share?

Chlorine led with 40.89% of global volume in 2025.

Why are membrane cells gaining ground over diaphragm technology?

Membranes cut energy use to about 1,950 kWh per ton, eliminate asbestos, raise product purity, and enable hydrogen by-product sales.

How will carbon regulation influence regional competitiveness?

EU and Chinese carbon pricing raises cash costs by USD 60-80/t, advantaging Middle Eastern producers with low-carbon power.

What role does hydrogen valorisation play in plant economics?

Selling the 0.028 tons of hydrogen co-produced per ton of caustic can improve EBITDA by 8-12% when hydrogen prices exceed USD 3/kg.

Page last updated on: