Propionic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

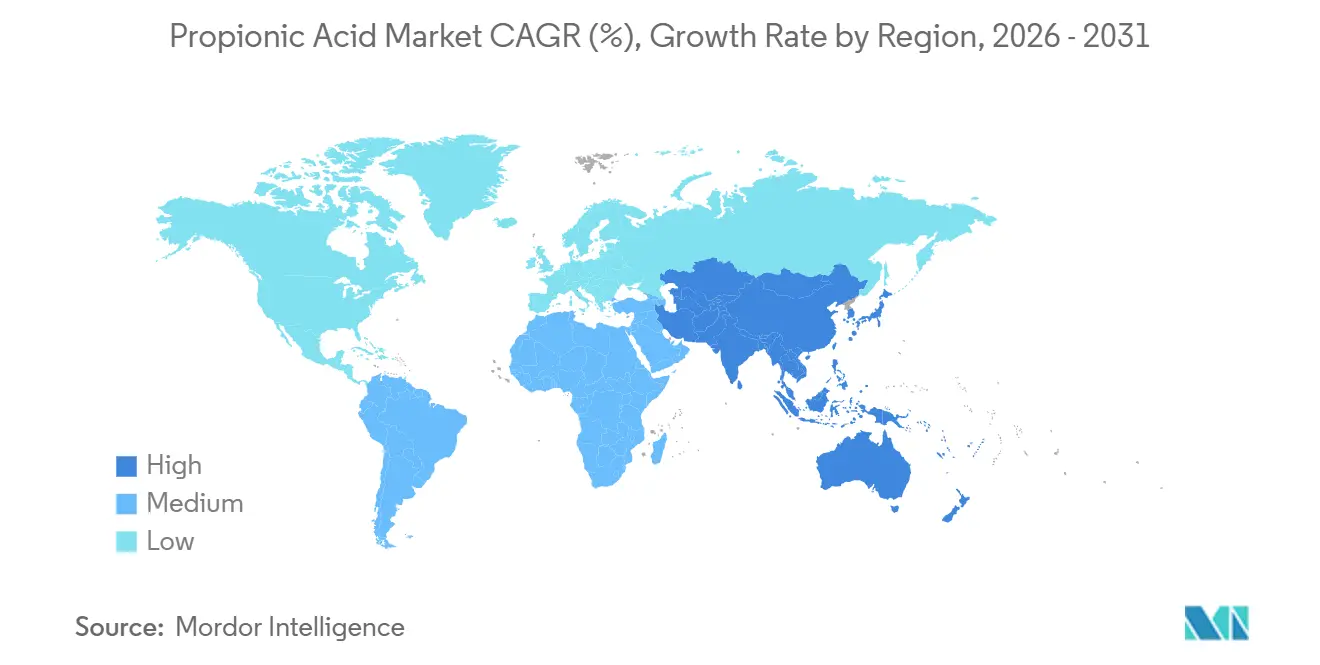

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

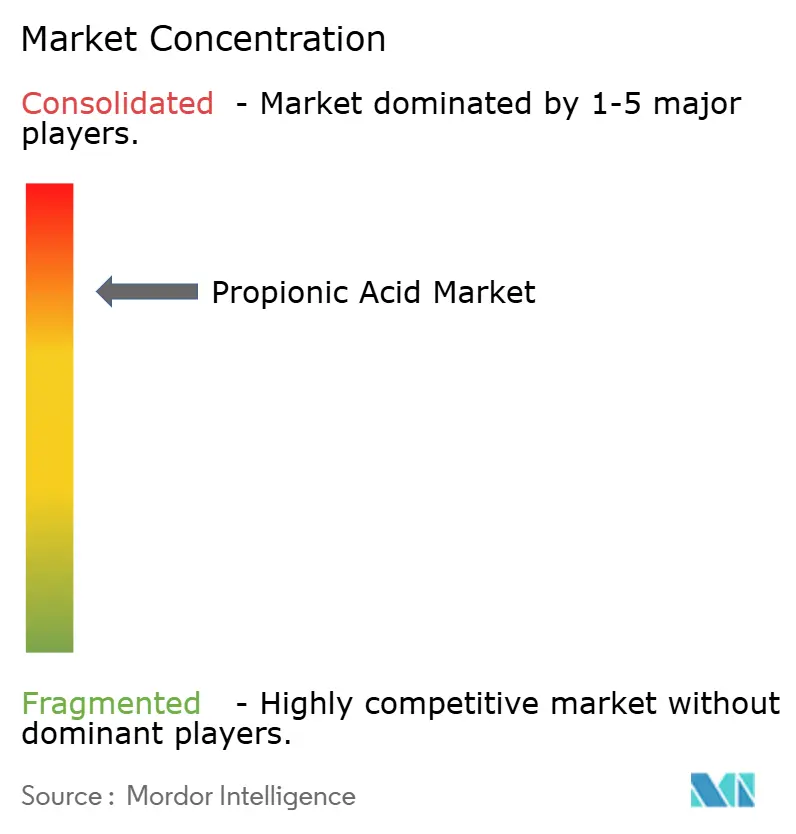

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Propionic Acid Market Analysis by Mordor Intelligence

The Propionic Acid Market size was valued at USD 1.63 billion in 2025 and is estimated to grow from USD 1.73 billion in 2026 to reach USD 2.31 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031). The propionic acid market is benefiting from the global pivot away from antibiotic growth promoters, growing demand for shelf-stable packaged foods, and steady uptake of bio-attributed production routes. Feed preservatives and bakery applications are anchoring volume, while specialty uses such as cellulose acetate propionate are capturing premium margins. Europe dominates the current value, but the propionic acid market is gaining momentum in the Asia-Pacific region as urbanization drives bread consumption and intensive livestock operations. Cost-competitive petrochemical synthesis still supplies most output, yet fermentation is advancing as food brands pursue Scope-3 emission cuts.

Key Report Takeaways

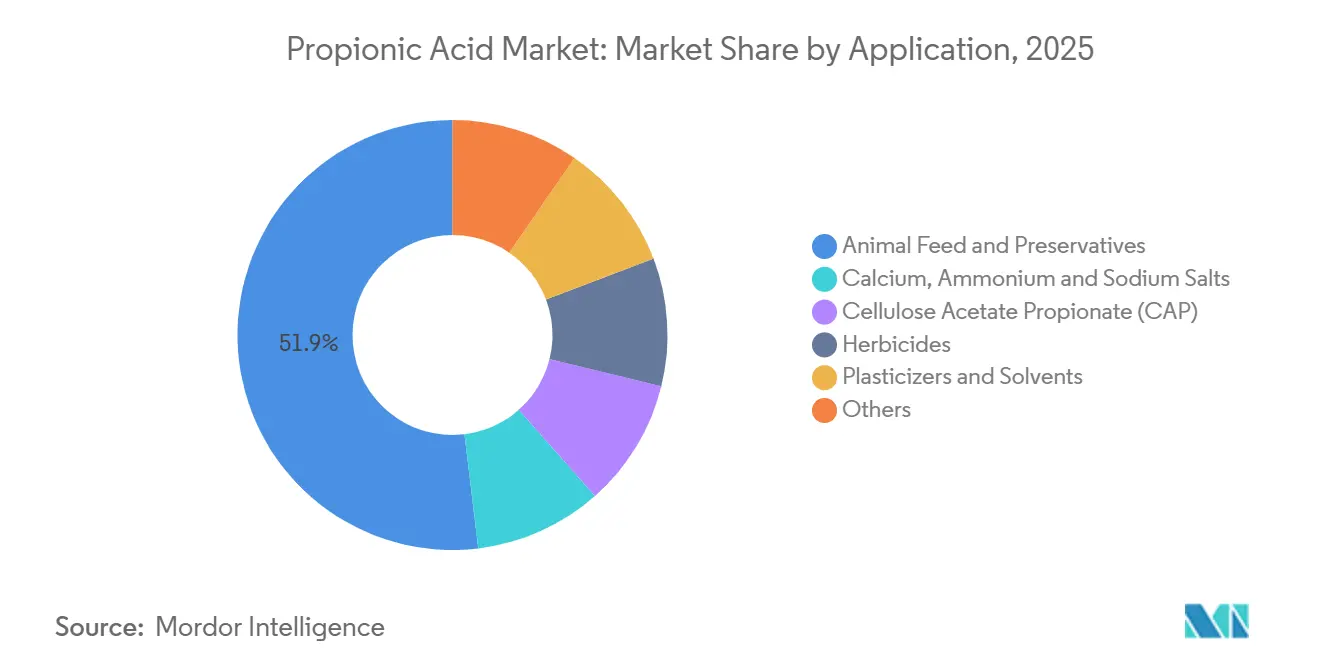

- By application, animal feed and food preservatives accounted for 51.92% of the propionic acid market share in 2025, and cellulose acetate propionate is forecast to grow at a 6.49% CAGR to 2031.

- By end-user industry, agriculture led with 56.98% revenue share in 2025, and pharmaceuticals are expected to expand at a 6.02% CAGR through 2031.

- By production route, petrochemical synthesis held a 92.34% share in 2025, and bio-based fermentation is projected to rise at a 6.19% CAGR to 2031.

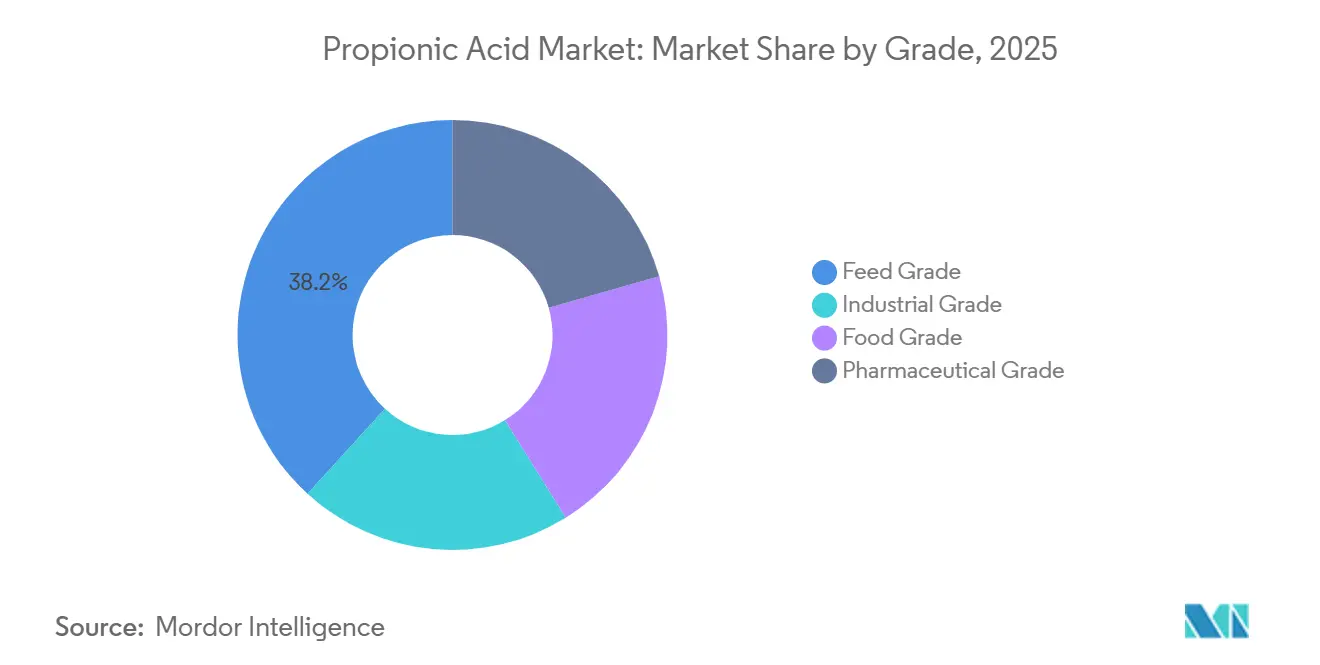

- By grade, feed variants commanded a 38.22% share in 2025, and the pharmaceutical grade is set to advance at a 6.14% CAGR up to 2031.

- By geography, Europe led with a 49.83% share in 2025, and Asia-Pacific is anticipated to register a 6.34% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Propionic Acid Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding demand for grain and silage preservatives | +1.4% | Global, with peak adoption in APAC and South America | Medium term (2-4 years) |

| Uptake of feed-grade acids in antibiotic-free meat chains | +1.6% | North America and the EU, spillover to APAC | Short term (≤ 2 years) |

| Packaged-bakery boom in emerging Asia | +1.2% | APAC core (China, India, Southeast Asia) | Medium term (2-4 years) |

| Growing requirement for shelf-life extension in processed foods | +0.9% | Global | Long term (≥ 4 years) |

| Food-brand Scope-3 decarbonization targets favouring low-carbon processes | +0.7% | North America and EU, early movers in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Demand for Grain and Silage Preservatives

Grain moisture levels exceeding a certain threshold foster the growth of Aspergillus and Penicillium, leading to aflatoxin levels surpassing Codex limits. However, many cooperatives find mechanical drying to be prohibitively expensive. Propionic acid effectively halts fungal growth, ensuring toxin levels remain within global standards. The U.S. Food and Drug Administration's GRAS status for direct feed inclusion provides livestock producers with regulatory assurance. In silage, both calcium and ammonium propionate prevent aerobic spoilage upon opening bunkers, safeguarding dry matter from potential loss. Adoption rates are highest in humid tropical regions, where mycotoxin pressures are pronounced. Consequently, the propionic acid market plays a pivotal role in enhancing feed safety and bolstering farmer profitability.

Uptake of Feed-Grade Acids in Antibiotic-Free Meat Chains

In response to European bans on sub-therapeutic antibiotics and similar policies in North America, integrators are increasingly turning to organic-acid programs. Propionic acid, known for lowering intestinal pH, effectively suppresses harmful pathogens like Salmonella and Clostridium, all while safeguarding beneficial lactobacilli. Field trials in broiler production have demonstrated its economic advantages. A 2024 assessment by the European Food Safety Authority, which found no genotoxic concerns, reaffirmed the safety of propionic acid[1]European Food Safety Authority, “Re-evaluation of Propionic Acid and Its Salts as Food Additives,” Efsa.europa.eu. In a notable industry trend, leading suppliers are now blending propionic, formic, and butyric acids. This move not only broadens their antimicrobial coverage but also indicates a shift away from single-acid strategies, bolstering the growth trajectory of the propionic acid market.

Packaged-Bakery Boom in Emerging Asia

In China, India, and Southeast Asia, urban households are now opting for sliced bread at breakfast, moving away from traditional staples. Adding calcium propionate effectively curbs the rope-forming Bacillus without compromising dough handling, thereby extending product freshness throughout lengthy distribution chains. National standards in both China and India align with Codex inclusion levels, facilitating smoother cross-border trade for bakery inputs. Operational since 2024, Corbion’s circular lactic-acid plant in Thailand not only underscores the growing confidence in fermentation-based preservatives but also positions the region for an expanded capacity in bio-derived propionic acid[2]Corbion, “Annual Report 2024,” Corbion.com . The surge in packaged-bread sales bolsters the Asia-Pacific's dominance in the propionic acid market's incremental demand.

Growing Requirement for Shelf-Life Extension in Processed Foods

Retailers favor long code dates that cut in-store waste, while consumers seek concise labels. Propionic acid is effective at low inclusion and carries E-number approval in the European Union, allowing formulators to meet both goals. U.S. Environmental Protection Agency data categorize propionic acid as a high-production-volume chemical, confirming industrial-scale availability. Food technologists now pair the acid with natural antioxidants and modified-atmosphere packaging to extract further shelf life without raising dosage, broadening the propionic acid market beyond bread toward tortillas, cheese, and ready meals.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petro-based feedstock prices | -0.8% | Global, acute in regions reliant on imports | Short term (≤ 2 years) |

| Health concerns over chronic intake in ultra-processed foods | -0.5% | North America and EU | Medium term (2-4 years) |

| Capacity concentration-driven supply-chain risk | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Petro-Based Feedstock Prices

In 2025, refinery turnarounds and fluctuating cracker operating rates caused propylene spot prices to oscillate. These price swings tightened margins for producers without integrated olefin capacity and made pricing negotiations challenging for bakeries locked into fixed-price contracts. While fermentation offers a partial hedge—thanks to crude glycerol feedstock's independent trading from oil—bio routes remain costly, often reaching twice the price of petrochemical synthesis. This financial disparity moderates the immediate transition to a wholly renewable supply in the propionic acid market.

Health Concerns over Chronic Intake in Ultra-Processed Foods

Advocacy groups link preservative-rich diets to metabolic disorders, even though regulators have not amended acceptable daily intake levels. European Farm-to-Fork objectives emphasize fewer synthetic-sounding additives, prompting premium bakeries to adopt cultured-wheat alternatives or modified-atmosphere packaging. These consumer perceptions can restrain volume growth, yet the technical necessity of preventing mold keeps the propionic acid market resilient.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Feed and Food Preservation Dominate while CAP Accelerates

Animal feed and food preservatives held 51.92% of the propionic acid market share in 2025. Cellulose acetate propionate posted a 6.49% CAGR outlook thanks to high-solids automotive refinish coatings and bio-content nail lacquers. The segment benefits from patents that increase propionyl content and support bio-content claims, boosting specialty demand. Calcium, ammonium, and sodium propionates remain indispensable in bread, dairy, and feed, where pH control is critical. Perstorp’s 2024 capacity addition supports captive production of salts and plasticizers, reinforcing supply stability. Herbicides and plasticizers occupy smaller shares, but their steady volumes diversify revenue and lessen risk.

Steady requirement for mold inhibition in global grain chains underpins the application hierarchy. The propionic acid market size for feed additives is projected to track livestock expansion in Asia-Pacific and South America at a mid-single-digit CAGR. Specialty coatings draw on cellulose acetate propionate to cut volatile organic compound levels in line with tightening regulations, adding high-margin growth. Producers balance commodity feed-grade manufacturing with smaller pharmaceutical and specialty runs to optimize capacity utilization, ensuring broad coverage of propionic acid market demand.

By End-User Industry: Agriculture Leads while Pharmaceuticals Gain Pace

Agriculture absorbed 56.98% of consumption in 2025 as integrators mandate organic-acid programs in antibiotic-free systems. The segment anchors baseline tonnage for the propionic acid market. Pharmaceuticals are forecast to grow at a 6.02% CAGR through 2031 on the rising adoption of controlled-release excipients and topical antimicrobials. Pharmacopeial monographs set the purity of propionic acid at high levels, solidifying its price premium over feed grade.

Manufacturers in the food and beverage sector rely on calcium propionate to prolong bread's shelf life, ensuring its viability through extensive distribution networks. Meanwhile, sectors like personal care, textiles, and electronics serve as niche markets, balancing out the seasonal fluctuations in demand from agriculture and bakeries. The pharmaceutical grade, bound by cGMP regulations, faces a limited supplier base, safeguarding its margins. This dynamic not only fortifies the pharmaceutical sector but also broadens the horizons of the propionic acid market, extending its reach beyond mere bulk feed preservation.

By Production Route: Petrochemical Scale Persists yet Fermentation Gains Recognition

Petrochemical Reppe carbonylation produced 92.34% of global output in 2025 by achieving high yields with mature catalysts. BASF’s plant in Nanjing exemplifies this scale, efficiently catering to regional demand. Bio-based fermentation, although smaller, carries a 6.19% CAGR forecast as food companies pursue lower-carbon sourcing. Moreover, continuous membrane fermentation has enhanced productivity on glycerol substrates, narrowing the economic gap with petrochemicals.

Petrochemical producers are adopting renewable power and heat-pump systems to reduce emissions, somewhat diminishing the sustainability edge of fermentation. Nevertheless, consumer brands are prompting suppliers for audited footprint data, spurring the growth of new bio-attributed capacities. Furthermore, hybrid approaches that integrate fermentation with catalytic upgrading may gain traction in the mid-term, broadening the supply base of the propionic acid market.

By Grade: Feed Quality Dominates while Pharmaceutical Purity Expands

Feed-grade variants held 38.22% of 2025 volume, driven by cost-centric livestock sectors. Pharmaceutical grade is set to grow at a 6.14% CAGR because drug-delivery formulators demand assured purity and traceability. Monographs from the United States Pharmacopeia and the European Pharmacopoeia set heavy-metal limits. Meanwhile, the food-grade variant, adhering to Codex standards, finds its niche in bakery and dairy applications.

Integrated producers such as BASF and Perstorp fractionate streams to address all four grades, optimizing reactor throughput and distillation cuts. Chinese producers focus on high-volume feed and food grades that serve domestic mills, leveraging freight advantages. A nascent niche combines fermentation origin with pharmaceutical purity, commanding premium pricing in nutraceutical and clean-label food products, and providing fresh headroom within the propionic acid market.

Geography Analysis

Europe controlled 49.83% of the global value in 2025. Early elimination of antibiotic growth promoters and stringent European Food Safety Authority evaluations stabilized demand for calcium propionate and feed-grade acids. Germany’s industrial bakeries and poultry farms consume large volumes, while funding for CO₂-free steam at BASF’s Ludwigshafen complex exemplifies policy support for lower-carbon chemicals. Capacity additions at Perstorp’s Stenungsund site further anchor Europe as a production base that can comply with emerging carbon-border adjustments. Mature yet stable bakery and livestock sectors keep the propionic acid market resilient across the region.

Asia-Pacific is projected to grow at a 6.34% CAGR through 2031, the fastest among regions. China leads consumption, supported by the BASF-YPC joint venture that supplies domestic feed mills and bakeries. India is ramping up organic-acid programs in poultry, and packaged-bread demand is climbing alongside urbanization. High-value markets such as Japan and South Korea require pharmaceutical-grade material, while Southeast Asia benefits from export-oriented poultry complexes. Corbion’s 2024 investment in Thailand signals confidence in fermentation-based preservatives within the region, pointing to future capacity shifts favorable to the propionic acid market.

North America, bolstered by its vast livestock operations and prominent bakery chains, accounts for about a quarter of the world's propionic acid demand. The U.S. Environmental Protection Agency reports that domestic production of propionic acid ensures a steady local supply. In a bid to enhance cross-border trade, Mexico and Canada have aligned their feed-safety protocols with those of the U.S. South America, predominantly driven by Brazil and Argentina, showcases a significant yet price-sensitive market, particularly in grain preservation. Meanwhile, the Middle East and Africa, though smaller, are on an upward trajectory. In Saudi Arabia, poultry expansion and a growing bakery sector in South Africa are fueling increased imports. Together, these varied regional dynamics play a pivotal role in sustaining the global propionic acid market.

Value Chain Analysis

Upstream supply is anchored by petrochemical feedstocks (notably propylene and/or propionaldehyde) sourced from integrated crackers and oxo-alcohol value chains, which supports a cost advantage for producers with captive olefins and intermediates. On the alternative route, bio-based production chains start with fermentation substrates such as crude glycerol or carbohydrate streams, followed by downstream separation, purification, and concentration steps where recovery efficiency and corrosion management are key operating constraints.

Midstream, propionic acid production is concentrated in mainland China, Western Europe, and the United States. Large players (for example BASF, Perstorp, Eastman, and OQ Chemicals/OXEA) leverage integrated utilities and co-product handling to stabilize unit costs. Downstream demand is served through bulk logistics for corrosive liquids, then converted by formulators into food and feed applications (direct acid and quality-controlled material for propionates), industrial and coatings chains (including cellulose acetate propionate), and pharma-grade channels that require tighter traceability and compliance. Distribution typically uses chemical distributors and regional hubs in Europe (including Germany and the Netherlands), alongside direct supply to major feed mills, industrial bakeries, and specialty chemical processors. Along the chain, storage and transport compliance, plus qualification against Codex/JECFA and pharmacopeial specifications, are recurring checkpoints.

Competitive Landscape

The propionic acid market is consolidated. Chinese suppliers expand aggressively to meet domestic bakery and feed demand, though export penetration remains constrained by quality perceptions and corrosive-acid logistics. OXEA announced additional oxo-acid capacity, signaling confidence in oxo intermediates despite force-majeure disruptions. Process innovation is intensifying: membrane fermentation, metabolic engineering, and catalytic upgrading of mixed acids are active patent areas. Suppliers able to certify cradle-to-gate carbon footprints below industry averages gain preference from multinational food brands facing Scope-3 obligations. Regulatory compliance with FDA GRAS status, EFSA approvals, and pharmacopeial standards remains a durable barrier that shields established players and supports pricing discipline in pharmaceutical and food-grade niches of the propionic acid market.

Propionic Acid Industry Leaders

BASF SE

Dow

Eastman Chemical Company

Perstorp

OXEA Gmbh

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity is decarbonization-linked differentiation in food and feed preservatives, where large buyers seek audited footprint data. Suppliers can respond with verified low-carbon products and process changes, and BASF securing Carbon Trust "Lower than Market" verification for propionic acid (November 2024) shows how third-party carbon credentials are being used in procurement. That approach creates room for producers to document cradle-to-gate reductions across both petrochemical and bio-attributed routes.

Feedstock security and vertical integration also stand out as a near-term opportunity as petro-based price volatility and supply-chain risk affect producers. OXEA confirming a final investment decision in July 2026 for a major expansion at Bay City, Texas, including higher propionaldehyde capacity and a new Air Liquide syngas unit (with site preparation scheduled for Q3 2026), highlights the value of strengthening upstream intermediates that support carboxylic acids portfolios, including propionic acid. At the same time, bio-based and circular propositions are broadening into higher-margin end uses beyond feed and bakery. AFYREN and Esse Skincare announcing a December 2025 partnership around bio-based propionic acid for skincare points to a pathway for fermentation-derived supply to enter specialty personal care formulations where origin and footprint can influence pricing.

Recent Industry Developments

- July 2026: OXEA confirmed a final investment decision for a major capacity expansion at its Bay City, Texas, site, including increasing propionaldehyde capacity that supports its carboxylic acids portfolio, including propionic acid. The plan includes an Air Liquide syngas unit, with site preparation scheduled for Q3 2026, reinforcing feedstock security and integration for oxo-acids production.

- December 2025: AFYREN and Esse Skincare announced a partnership to introduce bio-based propionic acid for skincare, produced at the AFYREN NEOXY biorefinery in France. The collaboration expands fermentation-derived propionic acid into a specialty end market where traceability and bio-based claims can shape formulation choices and supplier selection.

- December 2024: Luxi Chemical Group initiated construction of an 80,000 t/y propionic acid complex in Liaocheng, China. The project indicates continued capacity build-out in mainland China, which adds competitive pressure on regional supply and increases the importance of downstream qualification and logistics for global trade of corrosive acids.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the propionic acid market means the value of neat propionic acid sold as a chemical input to downstream users, across major producing and consuming regions, and reported in USD at current prices.

Scope exclusions: We do not count stand-alone propionate salts and most derivative products when they are sold as separate finished items rather than neat propionic acid.

Segmentation Overview

- By Application

- Animal Feed and Preservatives

- Calcium, Ammonium and Sodium Salts

- Cellulose Acetate Propionate (CAP)

- Herbicides

- Plasticizers and Solvents

- Others

- By End-user Industry

- Agriculture

- Food and Beverage

- Personal Care

- Pharmaceutical

- Other End user Industries

- By Production Route

- Petrochemical

- Bio-based Fermentation

- By Grade

- Feed Grade

- Food Grade

- Pharmaceutical Grade

- Industrial Grade

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a plain fact base on where propionic acid is made, where it is used, and what moves demand year to year. We mainly rely on public sources such as the USGS for chemical and minerals context, UN Comtrade for trade flows that help sanity-check regional balances, the US EPA for regulatory signals tied to handling and emissions, and the European Chemicals Agency for substance level registrations and safety notes. We also use sources such as the US Patent and Trademark Office and WIPO to see whether process routes and downstream uses are changing.

Next, we layer in company annual reports, investor presentations, and association websites to map capacity additions, operating footprints, and end use focus areas like food preservatives and animal nutrition. When needed, our team also uses paid subscriptions for company financials, patent lookups, and shipment-level trade views to avoid missing smaller cross-border movements that are not obvious in top line statistics. The desk sources listed here are illustrative, and many other public references were also used for data collection, cross-checking, and clarifying assumptions.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions that tend to swing the model, especially around pricing progression, regional tightness, and where consumption is actually landing by end use. We spoke with participants across the value chain such as producers, distributors, and buyers in feed, food, and industrial processing, then validated the direction of demand across APAC, EMEA, and the Americas so regional splits stayed realistic.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 53% |

| Mid tier: 51% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 20% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production and trade signals are used to reconstruct regional consumption, then totals are aligned back to end use demand pools that typically absorb propionic acid. In practice, we track indicators such as feed output and livestock growth, since propionates are used in preservation, bakery and packaged food activity, chemical intermediate demand trends, and observable changes in operating capacity and utilization at key production hubs. Pricing is handled through a simple but consistent logic where representative regional price bands are refreshed and applied to estimated volumes, and the resulting value is checked for sudden jumps that do not match market reality.

To keep the model grounded, the totals are corroborated with selective bottom-up approximations like sampled volume by region multiplied by an average selling price range, distributor channel checks, and a roll up of visible capacity additions when a supply step change is expected. Where direct volume visibility is weak, gaps are handled by using bounded ranges informed by trade balances and interviews, and then narrowed during review. Forecasts lean on scenario analysis supported by a small set of drivers (feed preservation demand, food shelf life needs, industrial activity, and price direction), and then expert feedback is used to keep the slope and timing sensible.

Data Validation & Update Cycle

Validation is done in layers so the final numbers do not depend on a single series or one assumption. We cross-check outputs against independent signals like import dependence, capacity change announcements, and whether implied per-end-use consumption looks reasonable versus known usage patterns. When variances show up, the assumptions are revisited and follow-up calls are triggered, especially if pricing or regional allocation is driving most of the gap.

Before sign-off, the model is reviewed by another analyst who re-checks arithmetic, unit consistency, and year-on-year movement so outliers are not carried forward by mistake. Reports are refreshed annually, and interim updates are made when a material event occurs such as a major capacity start-up, outage, or demand shock. Right before delivery, we run a final update pass so clients receive the latest view available at that point in time.

Mordor Intelligence's Propionic Acid Market Estimate Compared With Other Published Estimates

Published market sizes for propionic acid can look far apart because the scope boundary is not always the same, and the price and volume logic is often handled differently. Differences also show up when one source anchors on a different base year, uses a different currency timing, or assumes a faster ramp for capacity and downstream demand.

By tracking year-specific regional price bands and checking which revenue stream is tied to neat acid only, Mordor Intelligence keeps the 2026 total closer to actual buying behavior in feed, food, and industrial processing rather than mixing in separate propionate salt product sales. Some estimates also blend derivatives or application products into the number, and that can lift the value even when underlying acid volumes do not change much.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.73 B (2026) | |

| Regional Consultancy A | USD 1.15 B (2024) | Uses a nearer-term base year and a narrower demand view that is typically closer to reported application splits, which can understate forward volumes if capacity ramp and trade rebalancing are not fully reflected. |

| Industry Publisher B | USD 1.11 B (2023) | Anchors on an earlier base year and may include a wider application bucket that blends acid with related products in reporting, and the price path can stay flatter when updates are less frequent. |

The spread in the table is mainly explained by what is counted as propionic acid revenue and which year is used for anchoring prices and volumes. When scope is kept tight and the price and volume steps are documented, clients can trace each movement back to a small set of repeatable market drivers and validation checks.

Key Questions Answered in the Report

What is the projected value of the propionic acid market in 2031?

The market is expected to reach USD 2.31 billion by 2031, reflecting a 5.92% CAGR over the forecast period from USD 1.73 billion in 2026.

Which application currently dominates demand?

Animal feed and food preservatives account for 51.92% of the 2025 volume due to their role in mold and mycotoxin control.

Which region is growing the fastest?

Asia-Pacific is projected to expand at a 6.34% CAGR as urbanization boosts packaged-bread and livestock demand.

How are producers addressing sustainability pressures?

Suppliers are investing in renewable power, bio-attributed feedstocks, and verified carbon footprints to help food brands cut Scope-3 emissions.

Why is pharmaceutical-grade consumption rising?

Controlled-release excipients and topical antimicrobials require ≥99.5% purity, driving a 6.14% CAGR for pharmaceutical grade through 2031.

Page last updated on: