Solvents Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 35.16 Billion |

| Market Size (2031) | USD 44.30 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solvents Market Analysis by Mordor Intelligence

The Solvents Market size was valued at USD 33.57 billion in 2025 and is estimated to grow from USD 35.16 billion in 2026 to reach USD 44.30 billion by 2031, at a CAGR of 4.73% during the forecast period (2026-2031). Petrochemical-based grades still dominate volume, yet the combination of bio-feedstock innovation, closed-loop recovery investments, and tightening volatile organic compound (VOC) limits is reshaping growth patterns within the solvents market. Rising pharmaceutical outsourcing in Asia-Pacific, infrastructure spending that lifts architectural coatings demand, and brand-owner sustainability commitments are broadening opportunities for high-purity oxygenated grades while eroding prospects for high-aromatic blends. Suppliers with integrated feedstock positions, AI-enabled recovery systems, and credible bio-routes are capturing early margin upside, whereas mid-tier producers dependent on spot crude or imported naphtha face widening cost swings. Competitive positioning, therefore, hinges on the agility to serve both legacy commodity volumes and emerging specialty niches, especially as solvent-based polymer recycling moves from pilot scale toward commercial deployment.

Key Report Takeaways

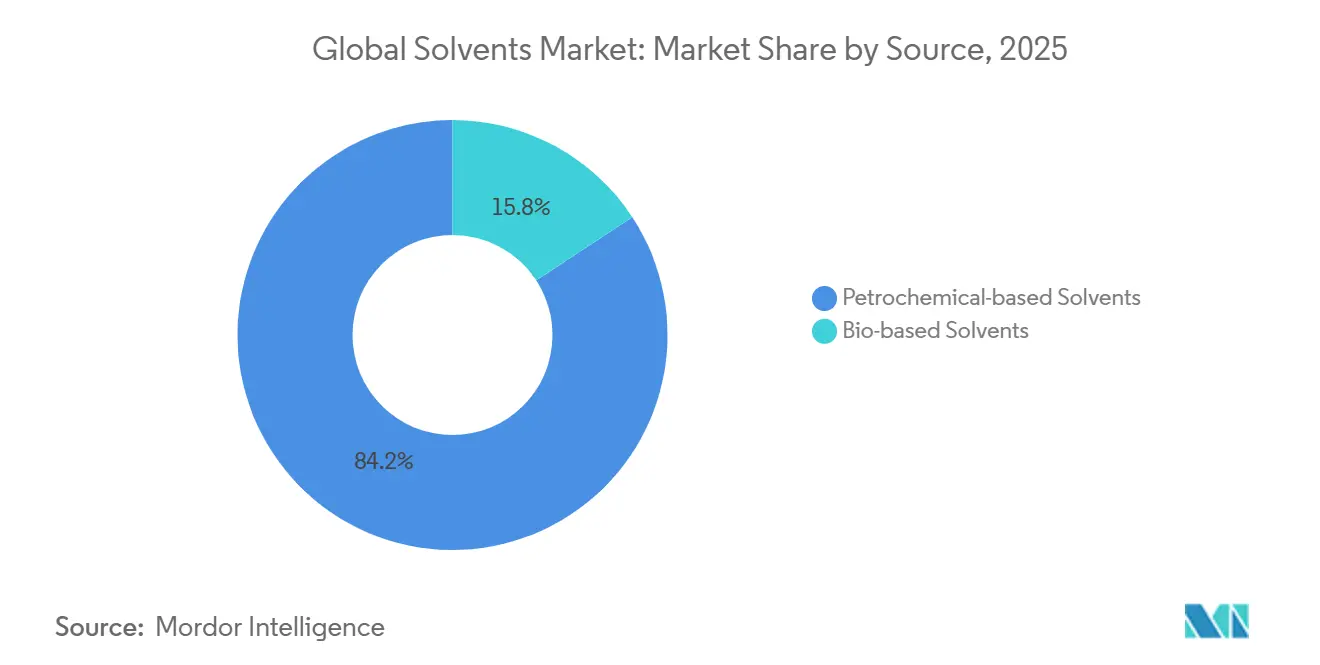

- In 2025, petrochemical-based solvents accounted for 84.23% of the market share, reflecting their dominance in the solvents market. Meanwhile, bio-based grades are projected to exhibit the highest growth, with an anticipated CAGR of 8.13% during the forecast period (2026-2031).

- Oxygenated solvents emerged as the leading type in 2025, representing 65.78% of the market size. This segment is expected to maintain steady growth, with a forecasted CAGR of 4.97% through 2031.

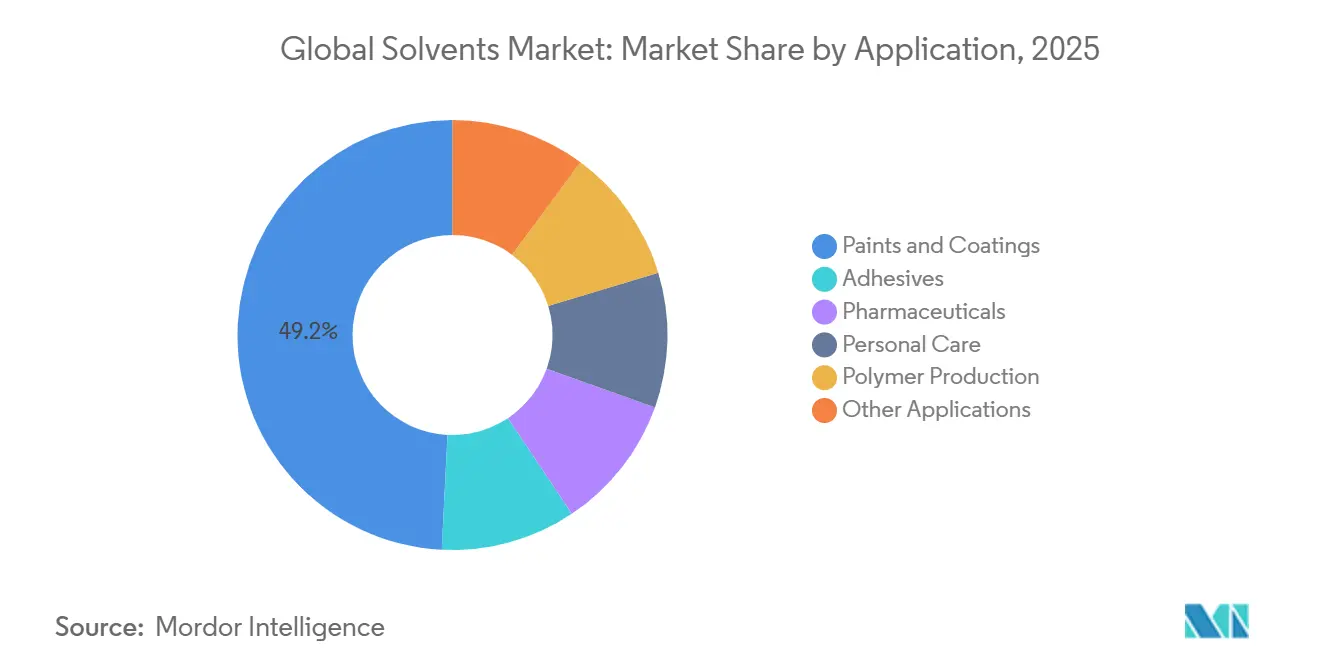

- The paints and coatings application segment generated the highest revenue in 2025, contributing 49.22% to the market. However, the pharmaceuticals segment is poised for the fastest growth, with a projected CAGR of 5.04% during the forecast period.

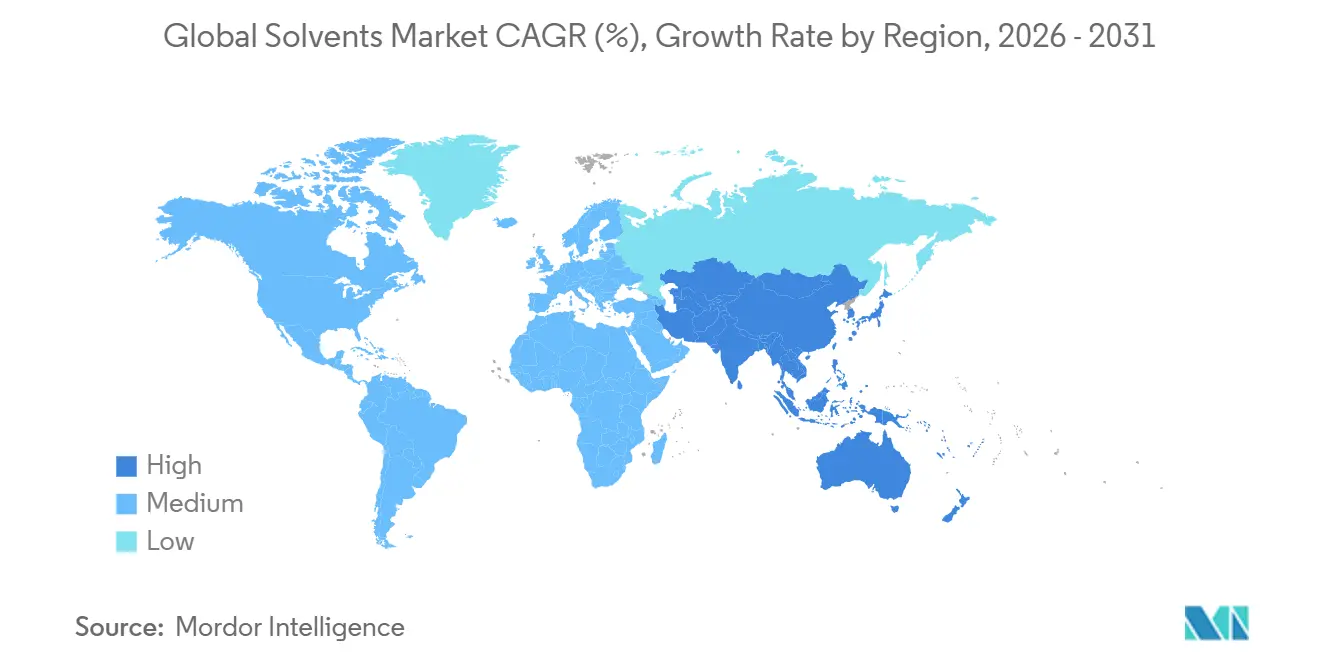

- Asia-Pacific led the geographical landscape in 2025, capturing 42.35% of the market share. The region is anticipated to sustain robust growth, with a forecasted CAGR of 5.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solvents Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from paints and coatings | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Accelerating pharmaceutical manufacturing in emerging Asia-Pacific clusters | +0.9% | Asia-Pacific core (India, China, Vietnam), spill-over to Middle East and North Africa | Long term (≥ 4 years) |

| Tightening VOC caps in North America and EU encouraging solvent substitution | +0.8% | North America and EU, early adoption in California and Nordic countries | Short term (≤ 2 years) |

| Rapid scale-up of solvent-based polymer recycling technologies | +0.6% | EU and North America, pilot deployments in Japan and South Korea | Medium term (2-4 years) |

| AI-driven, closed-loop solvent-recovery systems cutting opex for end-users | +0.4% | Global, with early gains in pharmaceutical and specialty-chemical facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand From Paints And Coatings

Architectural and industrial coatings absorbed nearly half of global solvent output in 2025, and regulatory ceilings on VOC content are accelerating reformulation toward acetone, methyl ethyl ketone, and acetate esters. The U.S. National Emission Standards for aerosol coatings that became effective in 2024 limit VOC to 45% by weight, prompting formulators to displace hydrocarbon blends with low-VOC oxygenates. China extended its low-VOC coatings mandate in 2025 to refinishing and furniture lines, triggering a double-digit jump in demand for compliant glycol ethers. Simultaneously, Middle Eastern pipeline refurbishment budgets exceeding USD 120 billion through 2030 are sustaining epoxy and polyurethane coatings that rely on high-solvency oxygenated carriers. Commodity hydrocarbon suppliers, therefore, face margin pressure, while specialty oxygenated producers command 10%–15% price premiums in compliant formulations.

Accelerating Pharmaceutical Manufacturing In Emerging Asia-Pacific Clusters

India and China produced 38% of global active pharmaceutical ingredients in 2025, lifted by Production-Linked Incentives worth USD 2 billion and a surge of export-oriented manufacturing parks[1]Government of India, “Production-Linked Incentive Scheme for Bulk Drugs,” india.gov.in. Hainan’s Free Trade Port alone attracted USD 8 billion of pharma capital expenditure in 2024-2025, adding solvent demand surpassing 120,000 metric tons per year. Vietnam’s ten-year tax holidays for greenfield API plants are set to pull in USD 1.5 billion of exports by 2030, further lifting regional uptake of high-purity ethanol, isopropanol, and tetrahydrofuran. Although these markets apply lighter environmental oversight, planned International Council for Harmonisation (ICH) residual-solvent updates will tighten purity targets, favoring suppliers with robust quality systems and validated recovery loops.

Tightening VOC Caps In North America And EU Encouraging Solvent Substitution

The EU Industrial Emissions Directive lowered solvent emission thresholds for coating and printing by up to 30% in 2024, forcing manufacturers to pivot toward exempt acetone or to install costly abatement equipment. California’s amended Rule 1113 caps interior flat paints at 10 g/L VOC as of 2025, effectively shifting the local coatings chain to waterborne or zero-VOC formulas. Large multinationals can absorb reformulation costs within 24 months, yet smaller firms confront USD 0.5-2 million capital outlays, spurring consolidation. Oxygenated and bio-based suppliers are consequently signing multi-year technical-service agreements to guide mid-tier formulators through compliance, embedding themselves more deeply into customer workflows.

Rapid Scale-Up Of Solvent-Based Polymer Recycling Technologies

Solvent-mediated dissolution of mixed plastics is moving from pilot to commercial status. ExxonMobil’s Exxtend processed 40,000 metric tons of waste in 2025 and targets 500,000 metric tons annually by 2027[2]ExxonMobil, “Exxtend Advanced Recycling Technology Overview,” exxonmobil.com . Fraunhofer’s 95% solvent-reuse loop for polystyrene achieved virgin-grade properties, easing concerns over quality drift. The EU Packaging and Packaging Waste Regulation now mandates 65% recycled content in PET bottles by 2030, creating a regulatory pull for advanced recycling volumes that could absorb 200,000 metric tons of solvents by 2031. Supply chains are therefore examining toluene- and xylene-based dissolution recipes as strategic hedges against virgin-resin price volatility.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock volatility and margin pressure for petro-solvents | -0.7% | Global, acute in regions dependent on imported crude (Europe, Asia-Pacific net importers) | Short term (≤ 2 years) |

| High cost-of-ownership for bio-solvent formulations in high-spec inks | -0.5% | North America and EU, limited impact in Asia-Pacific | Medium term (2-4 years) |

| Growing OEM bans on aromatic solvents in automotive interiors post-2027 | -0.3% | Global, with early enforcement in EU and California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Feedstock Volatility And Margin Pressure For Petro-Solvents

Brent crude oscillated between USD 70 and USD 85 per barrel during 2024-2025, translating each USD 10 move into a 100- to 150-basis-point swing in integrated solvent margins. European operators endured an additional spike in natural-gas feedstock to EUR 45 per megawatt-hour after Norwegian outages in January 2025, triggering unplanned cracker shutdowns and curtailing naphtha-sourced solvent output. Smaller standalone units, lacking hedging programs or refinery integration, recorded revenue declines of 5%–8% and accelerated asset divestitures. Although bio-routes offer partial insulation, volatility in corn and sugar prices introduces parallel risk profiles, and scale disadvantages keep cash costs higher than large cracker complexes.

High Cost-Of-Ownership For Bio-Solvent Formulations In High-Spec Inks

Bio-alcohols and esters sourced from corn or sugarcane still carry 20%–40% price premiums versus petrochemical equivalents, a gap that narrows materially only when Brent exceeds USD 90 per barrel. Food-contact ink applications require residual-impurity levels below 10 ppm, often mandating double distillation and activated-carbon polishing steps that add USD 100–200 per metric ton. Despite EPA Safer Choice and carbon-credit incentives, uptake in North American converters remains below 5% because brand owners resist passing on incremental costs without visible sustainability labeling. Until bio-refineries approach 200,000-plus metric-ton scale, economics will restrict adoption to niches where performance or regulatory mandates justify price differentials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Bio-Based Gains Outpace Petrochemical Incumbents

Petrochemical grades retained 84.23% solvents market share in 2025, yet bio-based alternatives are advancing at an 8.13% CAGR that nearly doubles overall solvents market growth. The solvents market size attributable to bio routes is projected to surpass USD 8 billion by 2031 as EU carbon-intensity scoring and California’s low-carbon mandates translate into tradable credits. Cargill expanded bio-ethanol output by 50,000 metric tons in 2025 to supply pharmaceutical syntheses with carbon-label claims. Groupe Berkem’s lignin-derived stripper landed ISO 14001 certification and is displacing N-methyl-2-pyrrolidone in European cleaning lines.

In price-sensitive adhesives and metal cleaning, petrochemical solvents still dominate on cost grounds. Shell and ExxonMobil now co-process certified bio-naphtha within crackers, producing mass-balance solvents that carry renewable labels without dedicated units—a tactic that shields share while facing scrutiny from NGOs over chain-of-custody credibility. As regulatory intensity rises, the solvents market is likely to bifurcate further: bio-based or mass-balance streams serve regulated regions, while Asia-Pacific growth keeps petrochemical demand buoyant.

By Type: Oxygenated Solvents Dominate Across Pharmaceutical And Coatings Applications

Oxygenated grades captured 65.78% of the solvents market size in 2025 and are predicted to expand at a 4.97% CAGR, underpinned by polarity, low odor, and multiple exemptions from VOC caps. Alcohols such as ethanol and isopropanol lead sub-segments, fueled by a surge in sanitizers and API crystallization. Glycol ethers are rising quickly as formulators chase sub-50 g/L VOC targets in architectural paints, supported by 80,000 metric tons of fresh capacity commissioned by Dow and Eastman in 2024-2025.

Hydrocarbon solvents held a considerable share in 2025 but are plateauing as OEM cabin-air standards retire aromatics. Halogenated niches are sliding by roughly 1% per year as REACH restrictions tighten. Eastman 168, launched in 2025, offers a non-halogenated drop-in with 90% lower global-warming potential, signaling momentum toward safer substitutes.

By Application: Pharmaceuticals Outpace Paints As API Production Shifts East

Paints and coatings consumed 49.22% of solvent volume in 2025, yet pharmaceutical demand is growing faster at 5.04% annually through 2031 as contract manufacturing organizations scale up in India, China, and Vietnam. A single 1,000-kilogram API batch can employ up to 10,000 liters of high-purity oxygenated solvent, and India alone added 3.2 million metric tons of API output in 2025, translating to an extra 50,000 metric tons of solvent demand.

Adhesives hold a considerable market share but migrate steadily toward hot-melt and waterborne chemistries, capping growth. Personal-care products are witnessing rising demand driven by rising disposable income in emerging regions. Polymer production demand is driven by toluene and xylene in synthetic rubber, while printing inks and ag-chemicals face distinct regulatory and digital-conversion headwinds.

Geography Analysis

Asia-Pacific generated 42.35% of the solvents market share in 2025 and is forecast to expand at a 5.21% CAGR through 2031. India secured USD 4.5 billion of foreign direct investment into pharma hubs between 2024-2025, boosting solvent uptake by 90,000 metric tons annually. China’s coatings output rose 6% in 2025 as residential construction in tier-2 cities resumed, prompting domestic giants to add 120,000 metric tons of solvent capacity. Vietnam’s tax incentives could lift regional demand by another 20,000 metric tons by 2031.

In North America, VOC regulations redirect consumption from hydrocarbon blends toward oxygenated and bio-based streams. The U.S. EPA tightened vapor-recovery rules for chemical storage tanks in 2024, compelling a USD 300-500 million spend on compliance that favors exempt acetone and methyl acetate as reformulation solvents. Mexico’s 3.8 million vehicle output in 2025 sustains 5% growth in OEM coatings consumption, even as aromatic bans loom post-2027.

Europe's solvent demand is led by Germany’s EUR 1.2 billion solvent-recovery upgrades that cut virgin demand by up to 40%. France commissioned a 30,000-metric-ton bio-propanol plant in 2025 to serve low-VOC coatings lines. South America and the Middle East and Africa are witnessing rising demand, with Brazil’s herbicide formulations and Gulf ethane-advantaged solvent exports filling regional niches.

Competitive Landscape

The global solvents market is moderately fragmented, where the top five players account for a considerable market share. BASF’s 2024 patent couples membrane separation with distillation to achieve 98% solvent reuse, offering a 40% energy cut and positioning the firm as a turnkey recovery partner. Dow and Eastman are co-developing bio-glycol ethers with farm-cooperative feedstock streams, seeking 10%–15% price premiums where renewable labeling carries weight. White-space innovation thrives in three pockets: ultra-high-purity pharmaceutical solvents below 50 ppm residuals, low-odor carriers for indoor architectural paints, and proprietary blends optimized for polymer dissolution recycling. AI-enabled recovery systems, led by Honeywell’s Forge installations that trim solvent losses to 2%–3% of throughput, can lop USD 50–100 per metric ton off operating costs, creating an efficiency wedge that favors technology-forward producers. Meanwhile, mass-balance certification debates may shake customer confidence; NGOs are pressing for segregated bio-streams rather than bookkeeping approaches, potentially reshaping investment flows toward dedicated renewable assets.

Solvents Industry Leaders

BASF SE

Dow

Exxon Mobil Corporation

LyondellBasell Industries Holdings BV

INEOS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BASF committed EUR 200 million to expand oxygenated-solvent capacity in Ludwigshafen by 80,000 metric tons per year, integrating a closed-loop recovery train that targets a 35% cut in virgin-solvent usage.

- October 2025: Shell and TotalEnergies formed a USD 300 million joint venture to build a 60,000-metric-ton bio-refinery in Rotterdam, producing bio-ethanol and bio-esters for pharma and personal-care segments.

- September 2025: Eastman Chemical introduced Eastman 168, a non-halogenated paint-stripper solvent with 90% lower global-warming potential and EPA Safer Choice certification, aiming for USD 50 million in revenue by 2027.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the global solvents market as all virgin, commercially traded liquids (with minor gaseous or solid grades) whose primary function is to dissolve or disperse other substances across manufacturing, processing, or formulation lines. Coverage spans petro-based and bio-based oxygenated, hydrocarbon, and halogenated chemistries that flow into paints and coatings, adhesives, pharmaceuticals, personal care, polymer production, and allied uses.

Scope Exclusion: This study omits on-site recycled streams and niche super-critical extraction fluids that are sold largely as equipment packages rather than discrete solvent volumes.

Segmentation Overview

- By Source

- Bio-based Solvents

- Petrochemical-based Solvents

- By Type

- Oxygenated Solvents

- Hydrocarbon Solvents

- Halogenated Solvents

- By Application

- Paints and Coatings

- Adhesives

- Pharmaceuticals

- Personal Care

- Polymer Production

- Other Applications (Printing Inks, Agricultural Chemicals, and Metal Cleaning)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordic

- Turkey

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- Qatar

- United Arab Emirates

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Seasonal interviews with bulk solvent manufacturers, regional distributors, coating formulators, and pharmaceutical process engineers across Asia-Pacific, North America, Europe, and Latin America help verify demand pulses, typical contract pricing, and substitution trends. Follow-up surveys allow Mordor analysts to test preliminary growth assumptions and calibrate regulatory impact assessments, especially on VOC limits and bio-content incentives.

Desk Research

Our desk review pulls production and trade statistics from United Nations Comtrade, the U.S. Energy Information Administration's refinery yield tables, Eurostat PRODCOM chemical codes, and Japan METI shipment surveys, which together map baseline volume and price corridors. Complementary insights stem from industry group bulletins such as the American Coatings Association and Cefic, academic journals indexed on ScienceDirect, and patent counts retrieved through Questel that flag emerging bio-based routes.

A second pass screens company 10-Ks, investor decks, and Factiva news to capture capacity additions, turnarounds, and spot price swings that affect average selling prices. These open-source anchors are supplemented by paid datasets, D&B Hoovers for financial splits and WSTS for downstream electronics solvent pulls, before being collated into our working library. The sources cited here are illustrative; numerous additional publications support data validation and clarification.

Market-Sizing & Forecasting

Sizing begins with a top-down reconstruction that aligns global petrochemical feedstock output with solvent yield factors, reconciled against import-export balances and apparent domestic consumption. Results are cross-checked through selective bottom-up roll-ups of supplier capacities and channel checks on average solvent prices. Key variables in the model include: 1) construction-weighted paint and coatings output index, 2) Brent crude-linked naphtha cost curve, 3) bio-acetone penetration rates, 4) Asia-Pacific vehicle build numbers influencing cleaning-grade demand, and 5) regulatory VOC threshold timelines. A multivariate regression marries these drivers with historical volume-price elasticity, while an ARIMA overlay captures seasonality. Where bottom-up samples show gaps, proportional allocation techniques bridge missing country splits before final triangulation.

Data Validation & Update Cycle

Once the model stabilizes, analysts benchmark outputs against independent trade flows and spot price dashboards, flagging anomalies that exceed a two-standard-deviation band. Senior reviewers sign off after variance checks, and we refresh each dataset annually, with mid-cycle updates triggered by material plant outages, policy shifts, or double-digit price moves. A last-mile review occurs immediately before client delivery, ensuring the freshest perspective.

Why Mordor's Solvents Baseline Commands Reliability

Published estimates often differ because firms choose unique product scopes, pricing bases, and refresh calendars. Buyers need clarity on those moving parts before trusting a number.

Key gap drivers include whether recycled streams are counted, how aggressively bio-based price premiums are projected, and the cadence at which new capacity announcements are folded into models. Mordor's analysts disclose scope choices up front, refresh every twelve months, and balance top-down volume math with selective bottom-up reality checks; alternative publishers may emphasize only one approach or roll several derivative fluids into the headline figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 35.09 B (2025) | Mordor Intelligence | - |

| USD 35.07 B (2024) | Global Consultancy A | Counts industrial cleaning blends and recycled stocks, inflating base. |

| USD 38.60 B (2024) | Industry Research Firm B | Uses revenue-only roll-up with higher ASPs and biennial updates. |

| USD 32.32 B (2024) | Market Publication C | Excludes bio-based volumes and several oxygenated grades. |

Differences above highlight why a transparent scope, yearly refresh, and dual-path modeling make Mordor's baseline the dependable starting point for strategic decisions.

Key Questions Answered in the Report

How fast is global demand for solvents projected to grow through 2031?

The solvents market is forecast to expand at a 4.73% CAGR, reaching USD 44.30 billion by 2031.

Which end-use segment will add the most incremental volume?

Pharmaceutical manufacturing, particularly in India and China, is set to show the quickest 5.04% annual increase in solvent consumption.

What was Asia-Pacific’s share in 2025, and how fast is it expected to grow through 2031?

Asia-Pacific already held 42.35% in 2025 and is on course for a 5.21% CAGR, keeping it the largest regional demand center.

Which solvent types face the steepest regulatory headwinds?

Hydrocarbon, especially aromatic, solvents confront phase-outs in automotive interiors and tougher VOC caps in coatings markets.

Are bio-based solvents cost-competitive with petroleum grades?

They currently carry 20%–40% premiums, becoming economically attractive mainly when crude prices sustain above USD 90 per barrel or when carbon-credit mechanisms offset the gap.

How fragmented is supplier competition?

The top 10 companies control 45%–50% of installed capacity, so the global field remains moderately fragmented, offering opportunities for niche specialists.

Page last updated on: