Poland Fencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

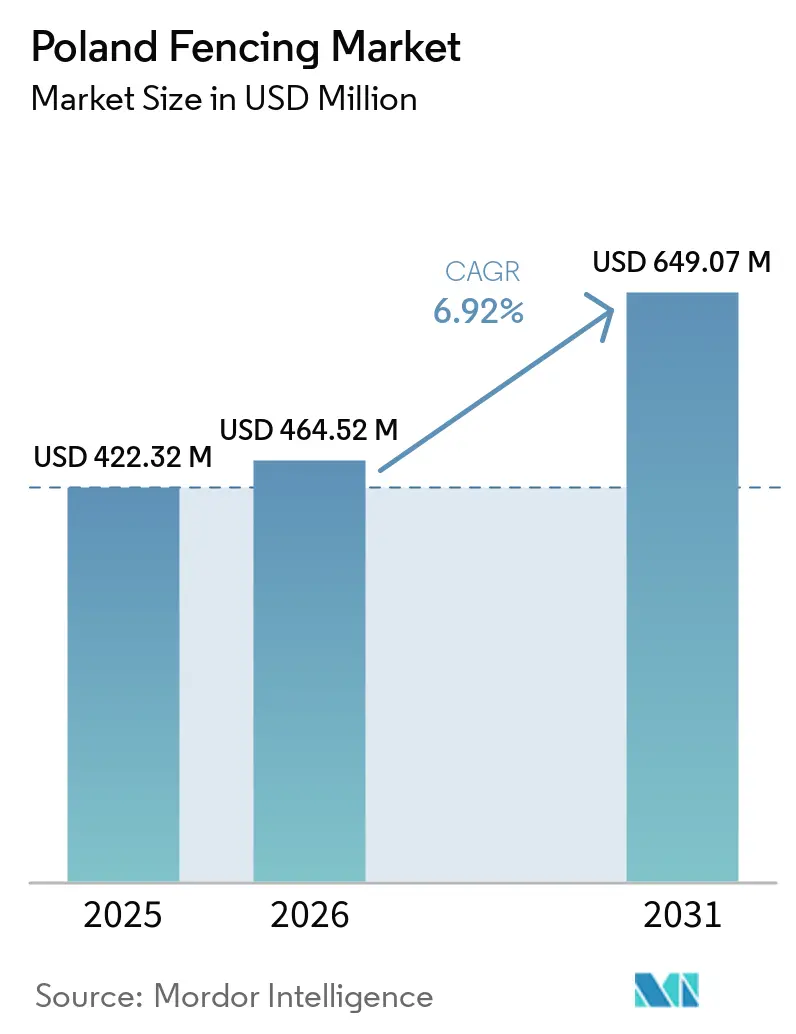

| Base Year Market Size (2025) | USD 422.32 Million |

| Market Size (2026) | USD 464.52 Million |

| Market Size (2031) | USD 649.07 Million |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Fencing Market Analysis by Mordor Intelligence

The Poland Fencing Market size is expected to increase from USD 422.32 million in 2025 to USD 464.52 million in 2026 and reach USD 649.07 million by 2031, growing at a CAGR of 6.92% over 2026-2031. Demand is being reinforced by a defense spending cycle that has kept Poland's 2025 military allocation close to 5% of GDP, translating into sustained procurement for border infrastructure and critical perimeter systems. The logistics base is also widening, with Poland's industrial and warehouse stock reaching 37.4 million sqm by Q1 2026 and leasing activity rising sharply in the same period, which keeps perimeter fencing tied to each new logistics park, warehouse buildout, and build-to-suit site.

Residential construction adds another steady layer, with 208,800 dwellings completed in 2025, up 4.3% year on year, which continues to support routine demand for boundary systems, gates, and privacy installations. Poland's position on NATO's eastern frontier means that part of the Polish fencing market now follows multi-year public security programs rather than only civilian property cycles, which gives suppliers a more resilient order base during slower phases in residential or commercial construction. This mix of defense, logistics, residential renovation, and utility protection is pushing the Poland fencing market toward higher-specification products, longer-life coatings, and integrated access control systems where pricing power is stronger than in standard volume panels.

Key Report Takeaways

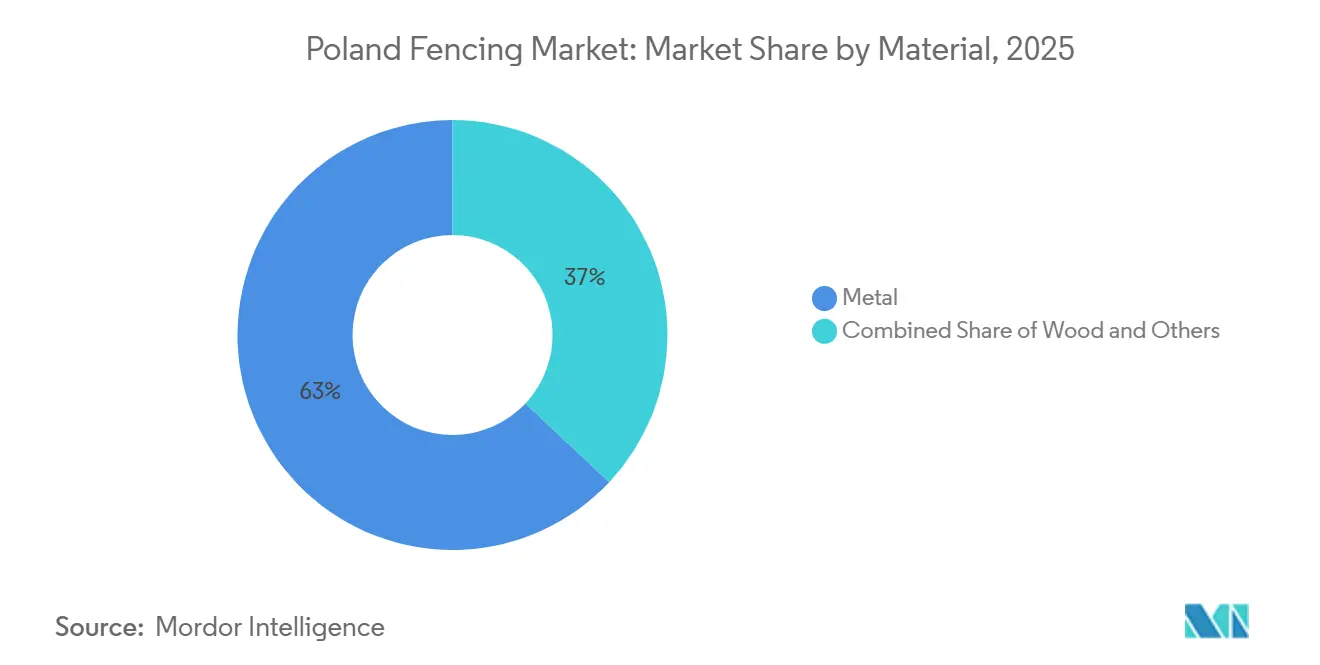

- By material, metal held 63% of the Poland fencing market share in 2025, while plastic and composite is projected to grow at an 8.9% CAGR through 2031.

- By end-user, residential accounted for 31% of the Poland fencing market size in 2025, while military and border security is forecast to expand at an 8.1% CAGR through 2031.

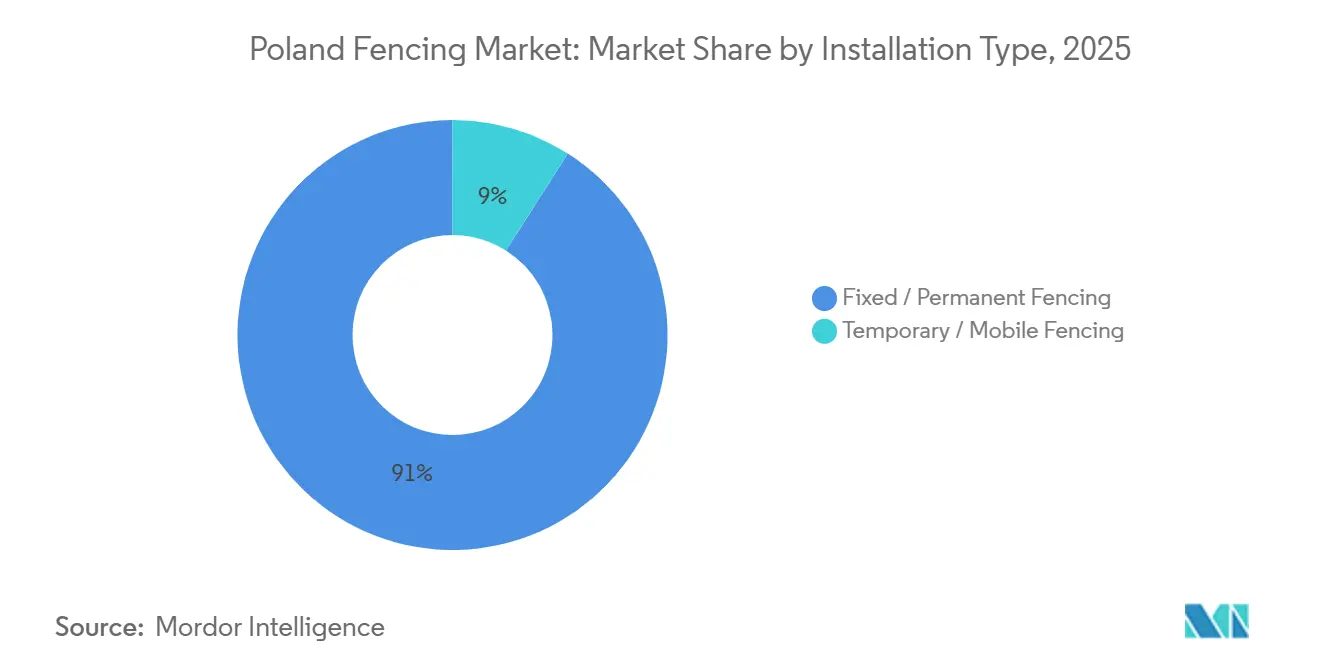

- By installation type, fixed and permanent systems held 91% share in 2025, while temporary and mobile fencing is projected to grow at a 9.3% CAGR through 2031.

- By installation channel, professional contractors held 66.21% share in 2025, while the others category is projected to grow at an 8.2% CAGR through 2031.

- By geography, Mazowieckie held 18% of the Poland fencing market share in 2025, while Pomorskie is forecast to expand at an 8.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Fencing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eastern Border Barrier Reinforcement and East Shield Procurement | +1.8% | Podlaskie, Warmian-Masurian, Lubelskie, with spillover to national defense supply chains | Medium term (2-4 years) |

| Logistics Parks and Warehouse Expansion | +1.2% | Mazowieckie, Śląskie, Dolnośląskie, Łódzkie | Short term (≤ 2 years) |

| Residential Renovation and Privacy-Led Premium Fencing Demand | +0.8% | National, strongest in Mazowieckie, Małopolskie, Dolnośląskie urban catchments | Short term (≤ 2 years) |

| Solar Farm and Utility-Site Perimeter Build-Out | +0.7% | Lubuskie, Pomeranian Voivodeship, Opole | Medium term (2-4 years) |

| Smart Perimeter Integration for Critical Sites | +0.5% | National, concentrated in border zones, energy facilities, and water utilities | Medium term (2-4 years) |

| Agricultural and Wildlife-Protection Fencing Demand | +0.4% | Lubelskie, Podkarpackie, Podlaskie | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Eastern Border Barrier Reinforcement and East Shield Procurement

The East Shield program is the largest border fortification project undertaken by Poland since 1945, with PLN 10 billion (USD 2.55 billion) committed to securing nearly 700 km of the Polish border with Russia and Belarus by 2028. Its first phase combines physical counter-mobility works, reinforced concrete obstacles, and a sensor-backed linear barrier, tying procurement demand not only to steelwork but also to specialized perimeter systems and access control hardware[1]Maciej Szopa and Jędrzej Graf, “How Is the East Shield Being Built? Chief of Military Engineering Reveals Details,” Defence24, defence24.com. By the end of 2025, 100 km of terrain had already been secured, and the obstacle belt was targeting half of its planned 500 km length by the end of 2026, providing suppliers with a visible pipeline rather than one-off project demand. The program also gained greater funding visibility after the European Commission identified it as a priority defense project, reducing the risk that fencing and barrier orders will be cut back by short-term domestic budget changes. This matters for the Poland fencing market because military-grade specifications tend to favor manufacturers with stronger compliance, coating, fabrication, and installation capabilities rather than low-cost panel suppliers. It also widens the addressable space for domestic specialists who had previously focused on civilian or industrial fencing and are now moving into defense-linked supply chains.

Logistics Parks and Warehouse Expansion

Poland's industrial and logistics stock reached 37.4 million sqm by Q1 2026, and gross leasing take-up rose to 1.58 million sqm in Q1 2026, up 42% from Q1 2025, which keeps perimeter fencing tied directly to new warehouse completions and leased industrial sites. Each new logistics park requires fencing as a standard site security item, so demand follows not only headline construction volumes but also the spread of large-format warehouses across national transport corridors. The construction pipeline remained structurally supported rather than speculative, with 60% of projects under development in 2025 already pre-let, which improved visibility for associated perimeter spending. Mazowieckie led the active logistics pipeline with 37% of projects, followed by Śląskie at 15% and Łódzkie at 11%, which concentrated much of the Poland fencing market in a few core logistics belts. Build-to-suit contracts represented 42% of Q1 2026 take-up, and that matters because tenant-led facilities in food processing, pharmaceuticals, and defense logistics often specify stronger perimeter systems than standard warehouse stock. That lifts project value per linear meter and shifts part of the Poland fencing market toward higher-specification industrial formats rather than basic site enclosures.

Residential Renovation and Privacy-Led Premium Fencing Demand

Residential renovation activity and rising preference for privacy are key drivers of growth in the Poland fencing market, particularly across urban and suburban catchments. Increasing investment in home improvement, supported by stable housing demand and refurbishment of older residential stock, is driving replacement and upgrade cycles for fencing solutions. Homeowners are prioritizing modern, durable, and visually appealing fencing systems that enhance property value while providing improved security and privacy.

Demand is especially strong in regions such as Mazowieckie, Małopolskie, and Dolnośląskie, where urban expansion and higher disposable incomes support spending on premium fencing materials, including composite panels, metal systems, and automated gates. Privacy concerns, noise reduction needs, and aesthetic preferences are further accelerating the shift toward higher-margin, design-oriented fencing solutions. In the short term (≤2 years), this trend is expected to sustain robust demand for premium residential fencing, benefiting manufacturers offering customized, low-maintenance, and weather-resistant products.

Solar Farm and Utility-Site Perimeter Build-Out

Utility-scale solar development is creating a steady stream of perimeter work because each photovoltaic site requires secure boundary protection, controlled access, and long-life corrosion performance. Polenergia launched the 67 MW Szprotawa photovoltaic farm in May 2025 across more than 300,000 sqm, which showed the scale at which even a single utility asset can translate into fencing demand. Electrum then began building the 100 MWp Grabno solar farm in April 2026 across 130 hectares in Lubusz Voivodeship, while Polenergia continued work on the 35 MWp Rajkowy project in Pomeranian Voivodeship with a 2026 grid connection target. A 100 MW-scale solar installation usually spans well over 100 hectares and can require 3 km to 5 km of perimeter fencing, which gives the Poland fencing market a repeatable project category outside housing and logistics. Utility sites are also becoming more security-sensitive, so operators are moving from simple mesh solutions toward systems that can support stronger monitoring and access control requirements. This makes renewable energy one of the clearer mid-market channels where specification values are rising faster than simple installation volume in the Poland fencing market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel, Zinc, Aluminum, and Coating Cost Volatility | -0.9% | National, strongest for mid-market panel manufacturers in Śląskie, Łódzkie, Mazowieckie | Short term (≤ 2 years) |

| Fragmented Installer Base and Price-Led Competition | -0.6% | National, more acute in secondary cities and rural voivodeships | Medium term (2-4 years) |

| Permitting and Procurement Delays in Infrastructure and Energy Projects | -0.5% | National, concentrated in border zones and large energy project corridors | Medium term (2-4 years) |

| Skilled Installation Labor Shortages | -0.4% | National, most acute in Opole, Warmian-Masurian, and Łódź voivodeships | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steel, Zinc, Aluminum, and Coating Cost Volatility

Raw material volatility remains the clearest system-wide pressure on the Poland fencing market because steel panels, welded mesh, posts, gates, galvanizing, and powder coating all depend on metal input pricing. CBAM became fully effective from January 2026 and added EUR 20 to EUR 22 per tonne (approximately USD 22 to USD 24 per tonne) to rebar imports, which tightened pricing for buyers that had depended on lower-cost external material[2]Louis Haas, “Polish long steel prices keep climbing amid higher costs, less pressure from import,” Eurometal, eurometal.net. The pressure does not stop at steel alone because galvanizing economics remain sensitive to zinc, and premium residential systems also carry aluminum exposure in higher-value formats. That matters most in the mid-market, where producers compete aggressively on installed price and have less room to pass on cost increases to distributors or end users. Cost inflation also narrows the pricing gap between standard and premium systems, potentially delaying replacement decisions in price-sensitive residential, agricultural, and basic commercial projects. Even where demand remains structurally firm, margin pressure can still reduce bidding appetite, shorten quote validity periods, and increase channel volatility across the Poland fencing market.

Fragmented Installer Base and Price-Led Competition

A fragmented installer base and price-led competition act as a key restraint in the Poland fencing market by limiting pricing power and slowing the adoption of higher-value fencing solutions. A large number of small, local installers and fabricators operate across the country, particularly in secondary cities and rural voivodeships, where competition is primarily driven by cost rather than product quality or technological differentiation. These players often offer low-cost fencing options made from basic materials and standardized designs, putting downward pressure on margins for organized manufacturers and premium solution providers.

This environment also leads to variability in installation quality, durability, and compliance with performance standards, which can affect long-term customer satisfaction and lifecycle value. In price-sensitive segments, end users tend to prioritize upfront affordability over advanced features such as automation, corrosion resistance, or customized designs, limiting the penetration of premium fencing systems. Over the medium term, continued fragmentation and aggressive pricing strategies are expected to constrain market value growth despite steady underlying demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Steel Dominates, but Composites Redefine the Growth Ceiling

Metal fencing commanded 63% of the market in 2025, and that large base reflects how widely galvanized steel panels, welded mesh, and standard post systems are used across residential, logistics, public, and industrial sites. In practical terms, steel still forms the bulk of volume in the Poland fencing market because it balances cost, durability, finish options, and installation familiarity better than other materials across mass-market applications. Concrete retains a role in privacy-led residential boundaries and in some rural installations where weight and visual screening matter more than design flexibility. Wood remains a smaller aesthetic niche because upkeep, weathering, and lifecycle maintenance make it harder to scale at broad volume. Polargos's January 2026 launch of 14 new steel residential models shows that mainstream suppliers still see enough depth in the steel segment to keep refreshing portfolio breadth rather than treating it as a mature category.

The Poland fencing market size for plastic and composite fencing is projected to expand at 8.9% CAGR between 2026 and 2031, making it the fastest-growing material group in the forecast period. This growth does not mean composite will replace steel at scale, but it does show that buyers are giving more weight to low maintenance, uniform finish, and regulatory alignment in selected projects. Public contracts and specification-led jobs are helping this shift because recycled-content positioning and compliance-friendly product formats are becoming more relevant than they were a few years ago. At the premium end, aluminum is also gaining visibility, and WIŚNIOWSKI's 2026 AW.AL.203 and INFINITY launches show how leading suppliers are using cleaner form factors and advanced fabrication to lift the value ceiling within the Poland fencing industry. Even so, steel remains hard to displace because duplex coating systems have extended service expectations and preserved metal's long-term cost position in the Poland fencing market.

By End-User: Defense Procurement Disrupts the Residential-Led Equilibrium

Residential demand held a 31% share in 2025, making it the largest end-user base in the Poland fencing market. That position was supported by 208,800 housing completions in 2025 and a residential pipeline that remained active through 2026 and 2027, sustaining routine demand for front fences, garden boundaries, gates, and privacy upgrades. Residential spend is also rising in quality terms because homeowners are putting more value on gate automation, coordinated facade design, and higher privacy standards, rather than buying only basic perimeter closure. Industrial and logistics demand sits close behind in strategic importance because Poland's warehouse corridor expansion keeps generating new perimeter requirements in regions with the heaviest buildout activity. Commercial and institutional projects add a stable layer where durability, standardized dimensions, and contractor execution remain central.

Military and border security is forecast to grow at a 8.0% CAGR from 2026 to 2031, making it the fastest-growing end-user group in the Poland fencing market. East Shield alone gives this segment a multi-year order base with a procurement logic that differs sharply from housing or ordinary commercial cycles. Mining and energy demand is also moving higher as large solar assets require protected boundaries, controlled site access, and more robust security features than older passive enclosures. Transportation infrastructure remains a steadier volume outlet, while agriculture and plantation fencing stays more price-sensitive and more exposed to farm economics than the rest of the Poland fencing industry. The net effect is a broader demand base, where residential still anchors volume but public security and infrastructure categories increasingly shape the direction of product mix.

By Installation Type: Permanent Systems Anchor Revenue, Temporary Leads the Growth Rate

Fixed and permanent fencing held 91% share in 2025, which reflects the basic structure of the Poland fencing market. Most end-users, especially households, logistics parks, public institutions, and industrial plants, need durable installations with long service lives, stable foundations, and reliable gate systems rather than short-term enclosures. This also explains why producers continue to invest in coatings, finish quality, and integrated gate systems, since the initial installation decision often determines replacement cycles for many years. Permanent systems gain further support from regulatory compliance because new residential builds are more likely to specify compliant dimensions and access features at the time of first installation rather than retrofit later. That keeps the permanent category central to revenue even when faster-growing niches attract more attention.

The Poland fencing market size for temporary and mobile systems is projected to expand at 9.3% CAGR between 2026 and 2031. Growth is being supported by active construction pipelines in logistics, infrastructure, and defense-linked works, where site security is needed before permanent barriers are finalized. Sonto's nationwide 18-location warehouse network with 24-hour delivery illustrates that the supporting commercial infrastructure for temporary fencing is already well developed in Poland. This segment is also becoming more sophisticated because modular formats are being used for medium-duration projects where installation speed and relocation matter almost as much as basic enclosure. As a result, temporary systems are not taking over the Poland fencing market, but they are gaining a larger role in how contractors and project sponsors manage phased development and worksite security.

By Installation Channel: Contractors Hold Volume, Modular Kits Capture the Growth Rate

Professional contractors accounted for 66.21% of channel share in 2025, which keeps them at the center of the Poland fencing market. That dominance is rooted in the complexity of permanent installations that require post setting, concrete work, gate alignment, automation, electrical connections, and, in some cases, integrated detection systems. Government, military, industrial, and logistics clients usually rely on certified installers because compliance, liability, and warranty requirements are harder to meet through informal execution. Betafence's UNILOX system also points in the same direction by reducing contractor labor time without turning professional jobs into DIY projects. This means the contractor channel continues to shape volume, specifications, and after-sales accountability across the Poland fencing market.

The others category is projected to grow at an 8.2% CAGR from 2026 to 2031, making it the fastest-growing channel. This group includes fabricators, online sellers, and modular self-assembly kits, and its rise is tied to labor constraints and the widening appeal of faster-installation formats within the Poland fencing industry. Polargos's Element System, distributed through large retail chains, shows that domestic manufacturers are building this route intentionally rather than treating it as a peripheral sales outlet. The channel is benefiting from cost-conscious residential buyers who still want branded systems but are more willing to handle part of the installation process themselves. That said, modular growth complements rather than displaces the contractor-led structure, because the most valuable parts of the Poland fencing market still depend on professional execution, site customization, and certified installation support.

Geography Analysis

Mazowieckie held an 18% share of the Poland fencing market in 2025, making it the largest regional contributor. Warsaw gives the region a dense mix of warehouse stock, government facilities, institutional assets, and premium residential development, all of which require perimeter systems with higher average specification levels[3]“MARKETBEAT Poland Residential Sector Q4 2025,” Cushman & Wakefield, cushmanwakefield.com. The region also accounted for 37% of active logistics construction in Q1 2026, which concentrated a large share of warehouse-linked fencing demand in one geography. Śląskie ranked second on the strength of its large warehouse base and high concentration of mining, energy, and heavy industrial sites that require stronger perimeter solutions. Wielkopolskie also remained important because a healthier labor backdrop and active private investment supported housing and commercial property spending around Poznań.

Pomorskie is forecast to grow at an 8.4% CAGR from 2026 to 2031, giving it the fastest regional growth profile in the Poland fencing market. New industrial and logistics supply in the region reached 139,100 sqm in Q1 2026, ranking it among the strongest markets nationally and underscoring the importance of Tricity's port-linked economy. NRF Group's expansion to 52,000 sqm at Panattoni Park Gdańsk West II illustrates the scale of tenant moves now underway in the region and the perimeter work that follows. Rajkowy adds another layer because utility-scale solar investment is raising security and boundary requirements in Pomerania beyond traditional logistics uses.

The Rest of Poland still captures important demand across several distinct sub-regions. Lubelskie and Podkarpackie support agricultural fencing volumes, while Podlaskie remains tied to border infrastructure spending and security-focused perimeter works. Lubuskie is also gaining relevance because large photovoltaic projects such as Grabno expand energy-site perimeter demand outside the core warehouse corridors. The national regulatory backdrop matters everywhere, since the updated Construction Law taking effect in September 2026 will shape material choices, gate formats, and compliant residential designs across all voivodeships.

Competitive Landscape

The Poland fencing market remains moderately to highly fragmented, with more than 20 active domestic producers alongside international brands competing across residential, industrial, temporary, and high-security categories. WIŚNIOWSKI and Betafence Polska hold visible positions at different ends of the market, with the former stronger in premium residential systems and the latter more focused on high-security and critical infrastructure applications. WIŚNIOWSKI's PLN 160 million (USD 40.8 million) plant expansion approved in September 2025 points to a capacity-first strategy built around residential upgrades, higher-value product design, and sustained demand from new project activity. Its 2026 launches, including the INFINITY collection and AW.AL.203, show that this strategy is not based on volume alone but also on premium differentiation through design, finish quality, and system integration. Betafence's critical infrastructure positioning creates an effective moat because specification complexity, gate certification, and institutional procurement rules are harder for smaller firms to match.

Betafence's TriMax anti-personnel proposition and its faster-installation UNILOX system show a product roadmap aligned to government, infrastructure, and controlled-access projects rather than only standard panel demand. At the same time, there is still open space in smart-enabled perimeter systems for mid-market industrial and energy buyers that do not yet purchase full military-grade packages. Integrated AI detection and sensor-based perimeter platforms remain concentrated at border, defense, and top-tier industrial sites, which leaves room for scaled-down offerings aimed at logistics parks, utilities, and renewable energy facilities. That gap is important because security expectations are rising faster than many mid-market buyers' legacy purchasing habits, which creates room for product tiering rather than simple price competition.

Smaller specialists are also shaping competitive behavior in specific niches of the Poland fencing market. Sonto has built a national rapid-delivery position in temporary fencing, while Panel System Group has a clear B2B orientation in temporary and permanent solutions for construction and infrastructure users. Large permanent-fence manufacturers have not fully replicated that asset-light rental and deployment model, which keeps the temporary segment more open than the permanent category. Compliance requirements also protect established producers because ISO 1461 galvanizing standards and CE marking for automated gate products set practical thresholds that low-end imports struggle to meet in institutional or warranty-sensitive projects. As a result, rivalry remains active, but competition is centered less on pure commodity pricing and more on delivery speed, channel reach, finish quality, and the ability to meet tighter specification demands.

Poland Fencing Industry Leaders

WIŚNIOWSKI

Betafence Polska

Polargos Sp. z o.o.

Plast-Met Systemy Ogrodzeniowe

Konsport Majewscy sp.j.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: WIŚNIOWSKI launched the INFINITY palisade fence collection, a minimalist 60×40 mm closed steel box-section system compatible with HOME INCLUSIVE, CLASSIC, and MODERN gate ranges, expanding the company's premium residential portfolio and targeting design-led architectural cohesion demand.

- May 2026: Poland's East Shield obstacle belt reached approximately 50% of its 500 km target length for end-2026, with storage site construction expanding onto KOWR-acquired non-military land in parallel with linear barrier works across the Russian Kaliningrad and Belarusian border sectors.

- April 2026: Electrum commenced construction of the 100 MWp Grabno photovoltaic farm across approximately 130 hectares in Lubusz Voivodeship, generating large-scale utility perimeter and security fencing demand for a site targeting autumn 2026 completion.

- January 2026: Polargos launched 14 new steel residential fencing models including Agat, Nicea, Londyn 2, Milton, Topaz, Opal, and Lavender, distributed through Leroy Merlin, OBI, PSB, and Castorama, reinforcing the company's mid-market steel portfolio ahead of the 2026 spring installation season.

Poland Fencing Market Report Scope

The Poland Fencing Market is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete), End-User (Residential, Agriculture & Plantation, and more), Installation Type (Fixed / Permanent Fencing, Temporary / Mobile Fencing), Installation Channel (Professional Contractor, Others – Fabricators, DIY / Modular Kits), and Region (Mazowieckie, Śląskie, and more). Market Forecasts are in Value (USD).

| Metal | Steel |

| Aluminum | |

| Wood | |

| Plastic & Composite | |

| Concrete |

| Residential |

| Agriculture & Plantation |

| Government & Public Infrastructure |

| Military & Border Security |

| Industrial & Logistics |

| Mining & Energy |

| Transportation Infrastructure |

| Commercial & Institutional |

| Fixed / Permanent Fencing |

| Temporary / Mobile Fencing |

| Professional Contractor |

| Others – Fabricators, DIY / Modular Kits |

| Mazowieckie |

| Śląskie |

| Wielkopolskie |

| Pomorskie |

| Rest of Poland |

| By Material | Metal | Steel |

| Aluminum | ||

| Wood | ||

| Plastic & Composite | ||

| Concrete | ||

| By End-User | Residential | |

| Agriculture & Plantation | ||

| Government & Public Infrastructure | ||

| Military & Border Security | ||

| Industrial & Logistics | ||

| Mining & Energy | ||

| Transportation Infrastructure | ||

| Commercial & Institutional | ||

| By Installation Type | Fixed / Permanent Fencing | |

| Temporary / Mobile Fencing | ||

| By Installation Channel | Professional Contractor | |

| Others – Fabricators, DIY / Modular Kits | ||

| By Region | Mazowieckie | |

| Śląskie | ||

| Wielkopolskie | ||

| Pomorskie | ||

| Rest of Poland |

Key Questions Answered in the Report

What is the 2031 outlook for fencing demand in Poland?

The Poland fencing market is projected to reach USD 649.07 Million by 2031 from USD 464.52 Million in 2026, rising at a 6.9% CAGR over 2026 to 2031.

Which material category leads demand and which one grows fastest?

Metal remained the largest category with a 63% share in 2025, while plastic and composite is expected to post the fastest growth at an 8.9% CAGR through 2031.

Why is border and defense spending becoming more important for suppliers?

East Shield and related security programs are creating multi-year procurement for heavy-duty barriers, perimeter systems, and specialist installations that do not depend on normal civilian construction cycles.

Which Polish regions are driving the strongest fencing activity?

Mazowieckie led with an 18% share in 2025 because of Warsaw's logistics, institutional, and residential base, while Pomorskie is expected to grow fastest at an 8.4% CAGR due to ports, logistics, and renewable energy projects.

What are the main operating pressures facing manufacturers and installers?

Raw material cost volatility and labor shortages remain the main pressures, since margins are sensitive to steel and coating costs while fragmented installer capacity can slow project conversion and raise execution costs.

Page last updated on: