Indonesia Mining Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

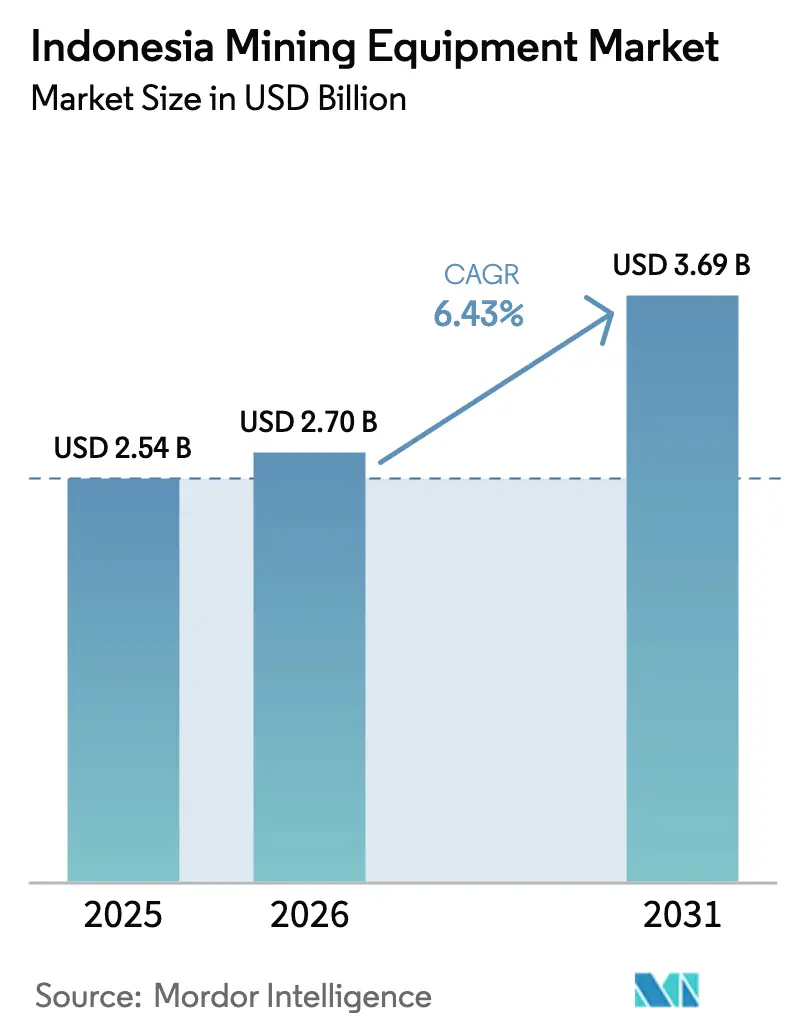

| Base Year Market Size (2025) | USD 2.54 Billion |

| Market Size (2026) | USD 2.7 Billion |

| Market Size (2031) | USD 3.69 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Mining Equipment Market Analysis by Mordor Intelligence

The Indonesia mining equipment market size was valued at USD 2.54 billion in 2025 and estimated to grow from USD 2.7 billion in 2026 to reach USD 3.69 billion by 2031, at a CAGR of 6.43% during the forecast period (2026-2031). This trajectory reflects Indonesia’s pivot from raw-ore exports to integrated mineral processing and battery-metal manufacturing. Deeper ore bodies and productivity pressures fuel uptake of underground, semi-autonomous, and fully autonomous systems, while compact battery-electric vehicles (BEVs) appeal to small contract miners seeking fuel savings and faster deployment. The Indonesia mining equipment market also benefits from government incentives for domestic value addition, insurance-led safety requirements, and a multi-faceted push to digitize operations for higher uptime and lower labor exposure. Meanwhile, coal-price cyclicality, stricter diesel rules, and limited grid power in remote Papua and eastern Kalimantan temper procurement cycles, but these headwinds are outweighed by long-term electrification and EV supply-chain momentum.

Key Report Takeaways

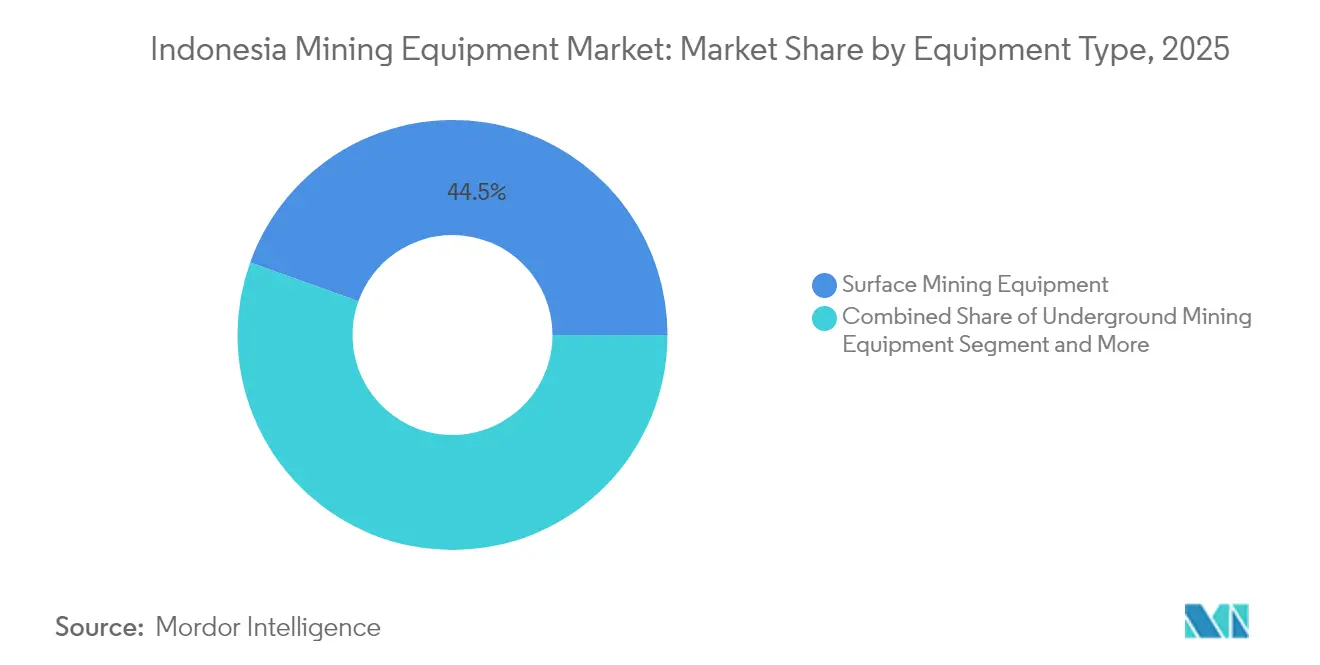

- By equipment type, surface mining equipment led with 44.52% share of the Indonesia mining equipment market in 2025; underground mining is projected to expand at an 8.17% CAGR through 2031.

- By automation level, manual equipment accounted for a 64.38% share of the Indonesia mining equipment market in 2025, while fully autonomous systems are poised for the fastest growth at a 10.02% CAGR over the forecast period.

- By powertrain, internal-combustion platforms dominated with 78.62% share of the Indonesia mining equipment market in 2025; electric vehicles are set to rise at a 12.05% CAGR between 2026 and 2031.

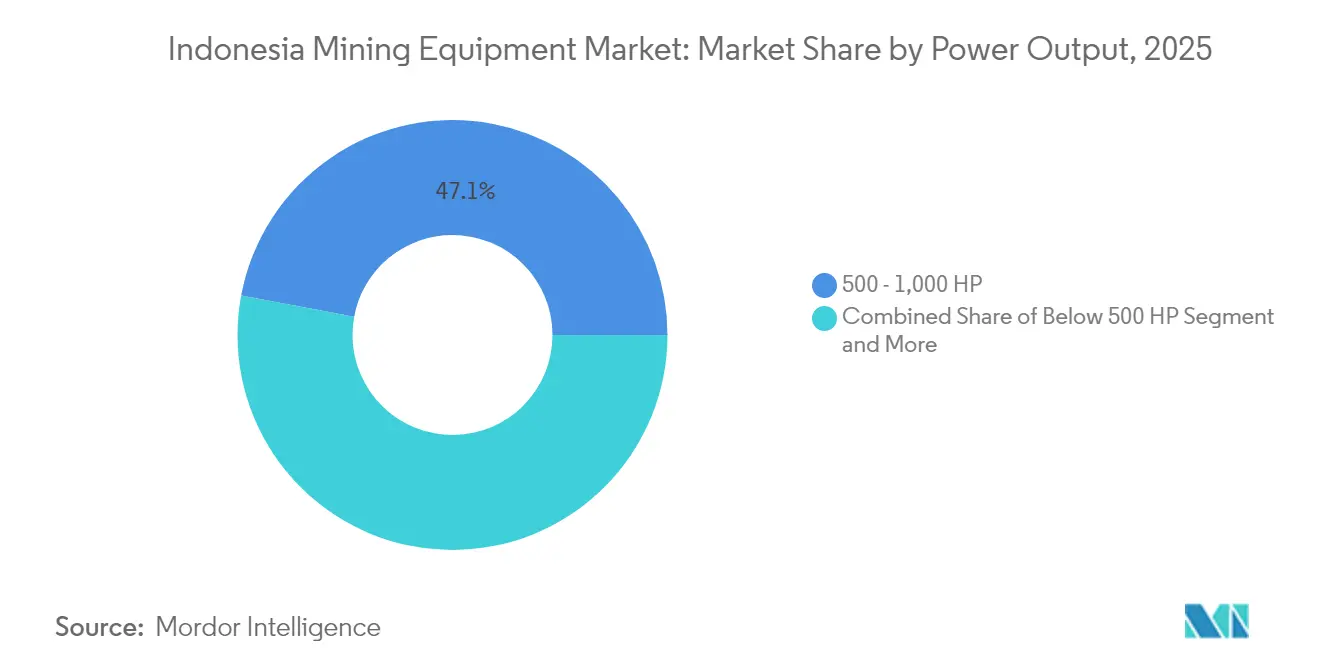

- By power output, the 500-1,000 HP band captured 47.06% share of the Indonesia mining equipment market in 2025, whereas equipment under 500 HP is advancing at a 9.48% CAGR through 2031.

- By application, coal mining held a 49.15% share of the Indonesia mining equipment market in 2025; metal mining represents the fastest-growing use case, with a 10.55% CAGR during the outlook period.

- By region, Kalimantan generated a 41.98% share of the Indonesia mining equipment market in 2025, while Sulawesi is forecast to record the highest regional CAGR at 9.72% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Downstream-Processing Mandate | +1.8% | Sulawesi, Kalimantan | Medium term (2-4 years) |

| Nickel And Copper Build-Out for EV Supply Chain | +1.5% | Sulawesi, Papua | Long term (≥ 4 years) |

| Digitization And Autonomy Adoption | +1.2% | Java, Kalimantan | Medium term (2-4 years) |

| Small-Contractor Shift to Compact BEVs | +0.9% | Sumatra, Kalimantan | Short term (≤ 2 years) |

| Local-Content (TKDN) Rules Driving Retrofit Opportunities. | +0.7% | National with manufacturing focus in Java | Medium term (2-4 years) |

| Insurance-Led Uptake of Collision-Avoidance Technologies | +0.4% | National, prioritized in high-risk underground operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Downstream-Processing Mandate Accelerates Mineral-Processing Equipment Demand

The downstream mandate banning unprocessed nickel exports and restricting copper concentrate shipments from 2025 has already been unlocked for three Vale Indonesia HPAL smelters in Sulawesi. Each facility requires high-pressure acid-leach autoclaves, sulfuric-acid plants, and mixed-hydroxide precipitate circuits far beyond the scope of conventional open-pit fleets. OEMs that integrate mechanical, process-control, and local-content packages benefit most as IUPK license holders face strict timelines. The policy realigns the Indonesia mining equipment market toward plant-level capital goods while stimulating aftermarket opportunities in lining replacement, valve refurbishment, and process-reagent handling.

Expansion of Nickel & Copper Projects for EV Supply Chain

Indonesia contributes most of the global nickel output, and EV battery makers are racing to secure supply. Vale Indonesia’s 20-year license extension and Tesla-linked partnerships underline multidecade horizons for mine-to-cathode lines. On the copper side, Petromindo sees mined output topping 1,019 kt in 2024 as Amman Mineral’s 900 kt/a plant and Freeport’s 700 kt/a Fakfak smelter progress. These complexes consume integrated equipment footprints—pit-to-port conveyors, 200 MW power plants, and anode furnaces—shifting procurement toward high-throughput, digitally controlled assets. Demand additionally skews to precision crystallizers able to deliver battery-grade nickel sulfate, opening white-space for chemical-process specialists within the Indonesia mining equipment market.

Digitization and Autonomy Initiatives to Raise Productivity and Safety

Skill shortages and deeper pits push operators to automation. Epiroc expanded Jakarta facilities in 2025 to assemble autonomous surface drill rigs locally, while Sandvik increased Indonesia field-service engineers for AutoMine deployments [1]“AutoMine Roadmap for ASEAN,”, SANDVIK Automation Division, sandvik.com. Caterpillar’s collision-awareness retrofit packages rolled out at multiple Kalimantan coal pits reduced recordable incidents by 25% in 2024, making insurers more willing to lower premiums [2]“Collision Awareness Systems Debut in Asia-Pacific,”, Caterpillar Press Office, caterpillar.com. Hexagon’s HxGN MineProtect bundles and Wabtec’s FLXdrive battery-electric locomotives combine safety and energy savings, aligning with regulators’ push for comprehensive mine monitoring. As cloud-based platforms from KHA deliver real-time equipment health dashboards, procurement conversations increasingly revolve around lifetime data analytics rather than upfront horsepower, reshaping vendor evaluation criteria in the Indonesia mining equipment market.

Surge of Small Contract Miners Needing Compact BEV Fleets

Indonesia’s mining equipment market is evolving rapidly, with smaller contract miners driving demand for compact, battery-powered machines. Companies like PT Riung Mitra Lestari are shifting to electric loaders to cut operating costs and meet emission rules in remote areas. OEMs offering modular charging and battery-swap systems are gaining early traction, while financing models now include carbon credit sharing. This agile buyer segment is accelerating localization and innovation in smaller equipment formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Coal-Price Cyclicality | -1.1% | Kalimantan, Sumatra | Short term (≤ 2 years) |

| Stricter Diesel-Emissions Rules and Carbon Tax | -0.8% | Java focus | Medium term (2-4 years) |

| Grid-Power Deficits at Remote Sites Delaying Electrification | -0.6% | Eastern Indonesia, Papua and remote Kalimantan | Long term (≥ 4 years) |

| Shortage Of Skilled Technicians for Advanced Systems | -0.4% | National, acute in specialized automation roles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Coal-Price Cyclicality Deferring New Equipment CAPEX

Thermal coal price declines have led major producers to cut capital spending, delaying fleet renewals and reducing orders for hydraulic excavators and 200-tonne trucks. While demand dips in the short term, historical trends in Indonesia show quick recovery cycles once prices rebound. To manage revenue volatility, companies are leaning more on aftermarket services, component re-life programs, and rentals—shifting margins toward maintenance rather than new equipment sales.

Stricter Diesel-Emissions Rules and Carbon-Tax Exposure

Euro IV diesel engine mandates for off-highway machines take effect in major Java ports by 2026, compelling costly retrofits or early retirements. Operators face a choice between cleaner engines, hybrid kits, or BEVs, complicating procurement and budgeting. For suppliers, certification, homologation, and local-content proof add administrative load, stretching go-to-market timelines and slightly dampening the overall CAGR of the Indonesia mining equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Mining Dominates Despite Underground Growth

Surface mining equipment generated a 44.52% share of the Indonesia mining equipment market in 2025, underpinned by Kalimantan coal and Sulawesi laterite operations that favor 120-tonne excavators, 200-tonne haul trucks, and mobile conveyors. Though only a mid-teen share, underground machinery delivers the quickest 8.17% CAGR as copper and high-grade gold seams in Papua go deeper. Mineral-processing assets linked to nickel HPAL plants now equate to more than one-quarter of new capex pipelines. This confirms a downstream pivot within the Indonesia mining equipment market size for process technology. Demand for crushers, screens, and autogenous mills rises at smelter sites and pithead beneficiation hubs required under domestic-processing quotas.

A supportive regulatory backdrop and integrated mine-to-metal strategies ensure healthy tender volumes for OEMs spanning mobile and fixed plant. Global brands with strong local after-sales infrastructure, alongside rising Chinese entrants, compete fiercely on total cost-of-ownership guarantees. Meanwhile, niche specialists supplying slurry pumps, valve-automation skids, and high-temperature materials see double-digit growth on the back of smelter rollouts. Such diversity of opportunity maintains a balanced revenue mix within the Indonesia mining equipment market.

By Automation Level: Manual Operations Transition to Autonomous Systems

Manual fleets still hold a majority 64.38% share of the Indonesia mining equipment market in 2025, reflecting Indonesia’s abundant low-wage labor and established operating protocols. Yet safety mandates and falling connectivity costs drive year-on-year upgrades to semi-autonomous dozers, operator-assist shovels, and radar-based collision nets. Once confined to Pilbara-style mega-pits, fully autonomous haulage is now piloted at two East Kalimantan coal mines using 100-tonne Komatsu trucks. The segment is forecast to surge 10.02% CAGR as insurers tie premium discounts to technology adoption, thereby nudging reluctant mid-tier miners.

Lifecycle analytics, predictive maintenance, and centralized control rooms become crucial value propositions. Vendors differentiate via open-architecture software that can overlay mixed OEM fleets, encouraging mine operators to migrate progressively without stranded assets. Consequently, the Indonesia mining equipment market witnesses a gradual but accelerating pivot from horsepower-centric conversations to data-driven performance contracts.

By Powertrain Type: ICE Dominance Challenged by Electric Transition

Internal combustion equipment retained a 78.62% share of the Indonesia mining equipment market in 2025. High-sulfur diesel is readily available near Balikpapan supply hubs, and decades of servicing expertise support these fleets. However, battery pack density improvements and falling lithium-iron-phosphate costs narrow total-cost-of-ownership gaps. The BEV slice is on a 12.05% CAGR path, especially within underground and short-haul quarry settings where ventilation savings amplify returns. Hybrids play an interim role, giving miners flexibility while grid-power build-outs lag, especially in Papua.

The Indonesia mining equipment market size for electric drivetrains gains momentum from favorable tax incentives on locally assembled packs and nickel-rich domestic cathode output that cuts battery import bills. Charging standards, interoperability, and safe-disposal regulations remain in progress but are improving through multi-stakeholder task forces led by the Ministry of Energy.

By Power Output: Mid-Range Equipment Optimized for Indonesian Conditions

Equipments in the 500-1,000 HP band commanded a 47.06% share of the Indonesia mining equipment market in 2025, matching overburden volumes, haul-road gradients, and pit widths common to Indonesian coal and laterite sites. Sub-500 HP units rose 9.48% CAGR during the forecast period, propelled by contract miners opening satellite pits with lower stripping ratios and favoring nimble equipment. Above-1,000 HP giants stay niche, used mainly at Grasberg-scale copper or KPC overburden removal, where economies of scale justify sheer capacity.

OEMs adapt by offering modular frame designs spanning 400-900 HP, letting customers upgrade drivetrains or add BEV modules without changing chassis. Dealers like United Tractors stock tiered spare-parts catalogs to support cross-model interchangeability, reducing downtime and carrying costs across the Indonesia mining equipment market.

By Application: Coal Mining Leadership Challenged by Metal Mining Growth

Coal extraction still accounts for 49.15%share of the Indonesia mining equipment market in 2025, owing to Indonesia’s top-three exporter status and domestic market obligation tonnages. Yet the 10.55% CAGR in metal-mining equipment, particularly for nickel and copper, shifts strategic weight. Integrated EV battery supply chains require HPAL plants, pressure oxidation autoclaves, and solvent-extraction electrowinning cells, broadening the technology envelope.

As copper projects in Sumbawa and Fakfak demand block-cave loaders and large-diameter shafts, new procurement pools are open for specialized OEMs less exposed to coal cycles. Mineral-gangue segregation, fines-dry stacking, and tailings paste backfill technologies also gather pace as environmental scrutiny intensifies. Together, these trends diversify revenue streams and strengthen resilience within the Indonesia mining equipment market.

Geography Analysis

Kalimantan generated the 41.98% of equipment demand in 2025, underpinned by mature coal concessions and emergent laterite-nickel undertakings near North Kalimantan industrial estates. Robust road-and-port infrastructure enables reliable supply of large excavators, haul trucks, and drill consumables. Leading producers implement fleet-management software to reduce idle time, pushing local dealers toward higher-tech maintenance packages and remote-monitoring centers.

Java, despite minimal mining activity, functions as the logistical and manufacturing nucleus. United Tractors’ Jakarta headquarters orchestrates parts distribution, lease financing, and operator training for nationwide fleets. Multiple OEMs run knock-down assembly lines in West Java to meet local-content quotas, creating an ancillary ecosystem for hydraulic cylinders, control harnesses, and undercarriage rebuilds, further anchoring the Indonesian mining equipment market on the island.

Sulawesi posts the fastest growth through 2031 with 9.72% CAGR. Massive HPAL, MHP, and matte lines at Morowali and Pomalaa compel shipments of autoclaves exceeding 600 t each, plus sulfuric-acid towers, oxygen plants, and ABB drive systems. Chinese consortia streamline EPC schedules, accelerating equipment pull-through even before mines hit steady-state. Sumatra maintains steady coal-linked orders, serving state utility PLN’s demand and seaborne exports via Lampung. Papua remains an emerging frontier where Freeport’s block-cave expansion and Wabu Gold reserve delineation spark early groundwork contracts. The region’s remoteness and limited grid power tilt procurement toward diesel-hybrid and energy-storage solutions, underscoring localized nuances in the Indonesia mining equipment market.

Competitive Landscape

The marketplace shows moderate fragmentation, with key players competing through strong dealer networks, local partnerships, and product strategies. Caterpillar benefits from Trakindo and United Tractors’ logistics strength, while Komatsu leverages PAMA’s captive demand. Hitachi boosts its excavator footprint via local assembly incentives. Chinese brands like Sany and XCMG multiply through bundled financing, though after-sales support remains challenging. Meanwhile, FLSmidth and Metso focus on process-plant equipment, and Epiroc and Sandvik compete in high-margin automation technologies.

Winning strategies emphasize technology stack integration, TKDN compliance, and lifecycle performance contracts. Hexagon ties software subscriptions to collision-avoidance hardware, creating annuity revenue. Meanwhile, Indonesian fabricators collaborate with global licensors to produce pressure vessels locally, supporting cost efficiency and regulatory quotas. Consequently, the Indonesia mining equipment market rewards participants able to combine capital goods, digital layers, and financing within a single proposition.

Indonesia Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hitachi Construction Machinery Co. Ltd.

Epiroc AB

Sandvik AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Vale Indonesia sought up to USD 1.2 billion financing for 2026-2027 mine-and-smelter expansion, signaling heavy upcoming equipment tenders.

- September 2024: Volvo Construction Equipment introduced the L120 Electric wheel loader, its latest electric machine, to customers in Indonesia. This launch made the L120 Electric the largest electric machine Volvo CE offers in the Indonesian market.

Indonesia Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills & Breakers |

| Crushing, Pulverizing & Screening |

| Loaders & Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 - 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| Sumatra |

| Java |

| Kalimantan |

| Sulawesi |

| Papua |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills & Breakers | |

| Crushing, Pulverizing & Screening | |

| Loaders & Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 - 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining | |

| By Region | Sumatra |

| Java | |

| Kalimantan | |

| Sulawesi | |

| Papua |

Key Questions Answered in the Report

How large is the Indonesia mining equipment market in 2026?

It is valued at USD 2.7 billion in 2026.

What is the expected CAGR for mining equipment demand in Indonesia?

Demand is projected to grow at a 6.43% CAGR between 2026 and 2031.

Which segment shows the fastest growth in Indonesia’s mining equipment landscape?

Fully autonomous equipment leads with a 10.02% CAGR due to safety mandates and productivity gains.

How are carbon tax and emissions rules influencing fleet choices?

Rising carbon-tax costs and Euro IV engine mandates push operators toward battery-electric or hybrid powertrains despite higher upfront prices.

Why is Sulawesi important for equipment suppliers?

Massive nickel HPAL and MHP projects driving integrated mining-to-smelter investments make Sulawesi the fastest-growing regional market.

Page last updated on: