Indonesia CPaaS Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

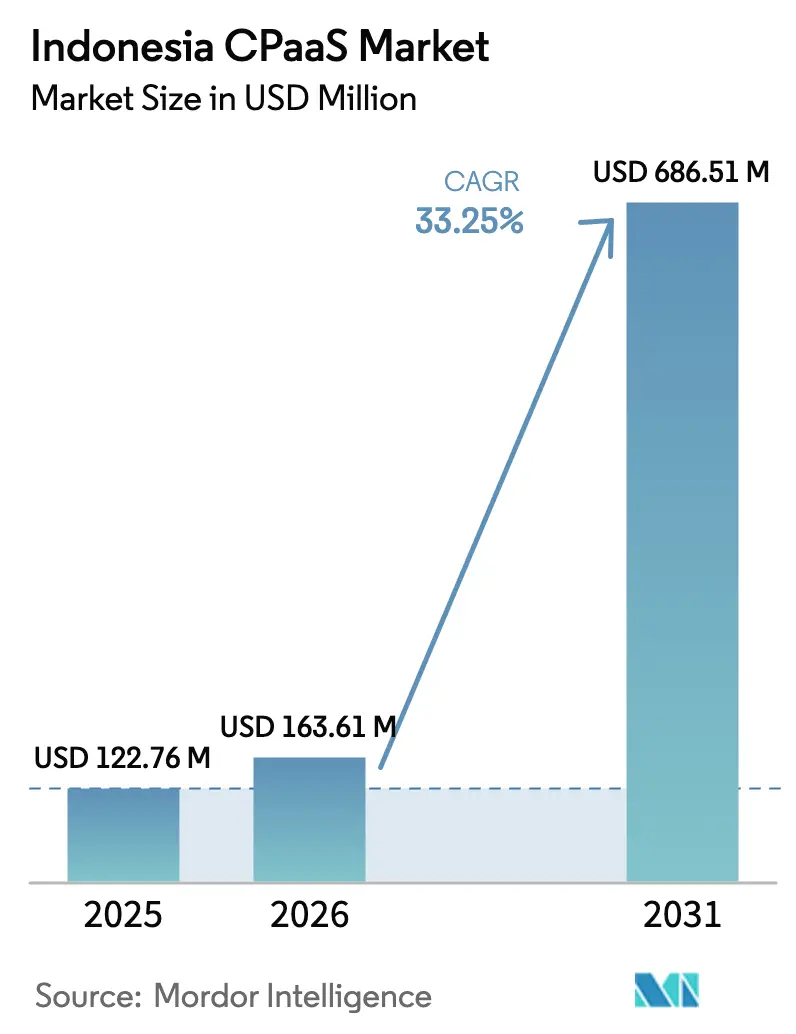

| Base Year Market Size (2025) | USD 122.76 Million |

| Market Size (2026) | USD 163.61 Million |

| Market Size (2031) | USD 686.51 Million |

| Growth Rate (2026 - 2031) | 33.25% CAGR |

| Market Concentration | Medium |

Major Players-Market-ML.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia CPaaS Market Analysis by Mordor Intelligence

The Indonesia CPaaS market size was valued at USD 122.76 million in 2025 and estimated to grow from USD 163.61 million in 2026 to reach USD 686.51 million by 2031, at a CAGR of 33.25% during the forecast period (2026-2031). This rapid expansion links to Indonesia’s USD 146 billion digital-economy target, nationwide internet penetration of 79%, and more than 180 million smartphone users, which allow enterprises to pivot toward omnichannel customer engagement.[1]U.S. Department of Commerce, “Indonesia Digital Transformation,” trade.gov Regulatory reforms such as Presidential Regulation 82/2023 mandate API integration across all ministries, accelerating demand for secure, programmable communications. Fintech growth reinforces the Indonesia CPaaS market by fueling one-time-password (OTP) and transaction-alert volumes, while carrier partnerships with global platforms create reliable nationwide delivery rails.[2]Telkomsel Enterprise, “CPaaS Product Suite,” telkomsel,com Infrastructure programs such as Palapa Ring and the SATRIA-1 satellite reduce the urban–rural digital divide, positioning CPaaS providers to serve emerging tier-2 cities.[3]Coordinating Ministry for Economic Affairs, “Digital Transformation Support,” ekon.go.id

Key Report Takeaways

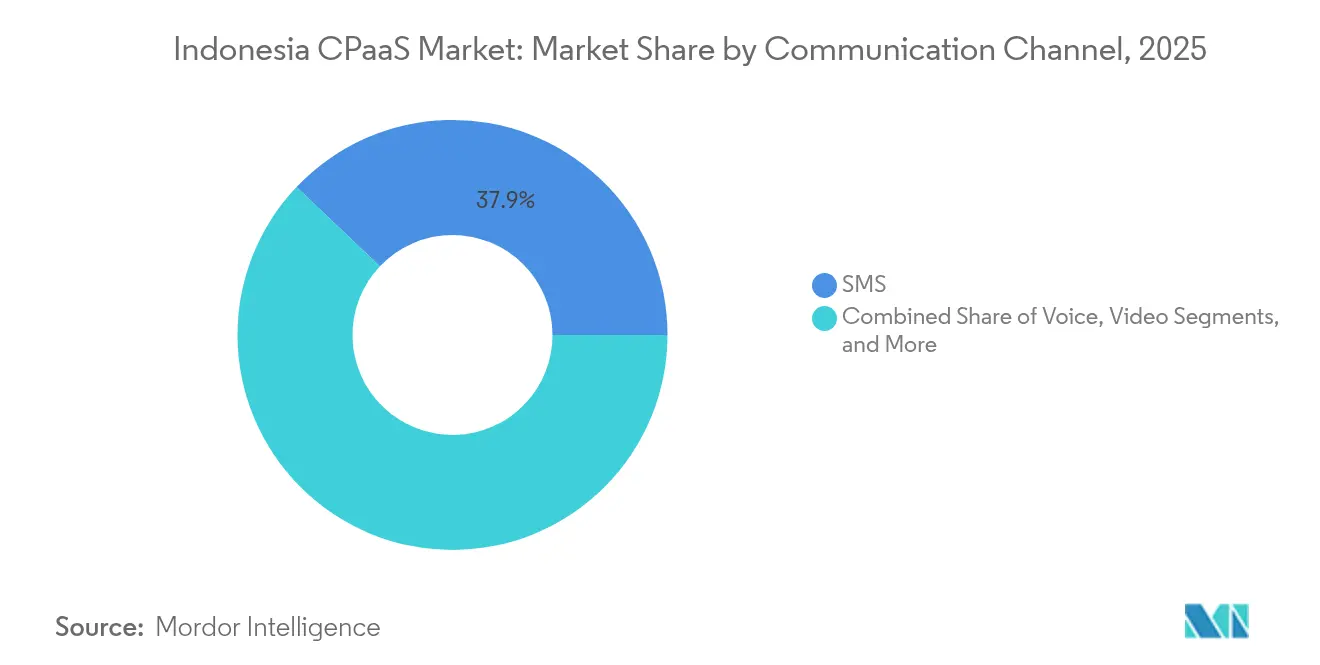

- By communication channel, SMS led with 37.92% of the Indonesia CPaaS market share in 2025 while Rich Communication Services (RCS) is forecast to post the fastest 34.88% CAGR to 2031.

- By enterprise size, large enterprises captured 61.96% of the Indonesia CPaaS market size in 2025 whereas small and medium enterprises are advancing at a 34.95% CAGR through 2031.

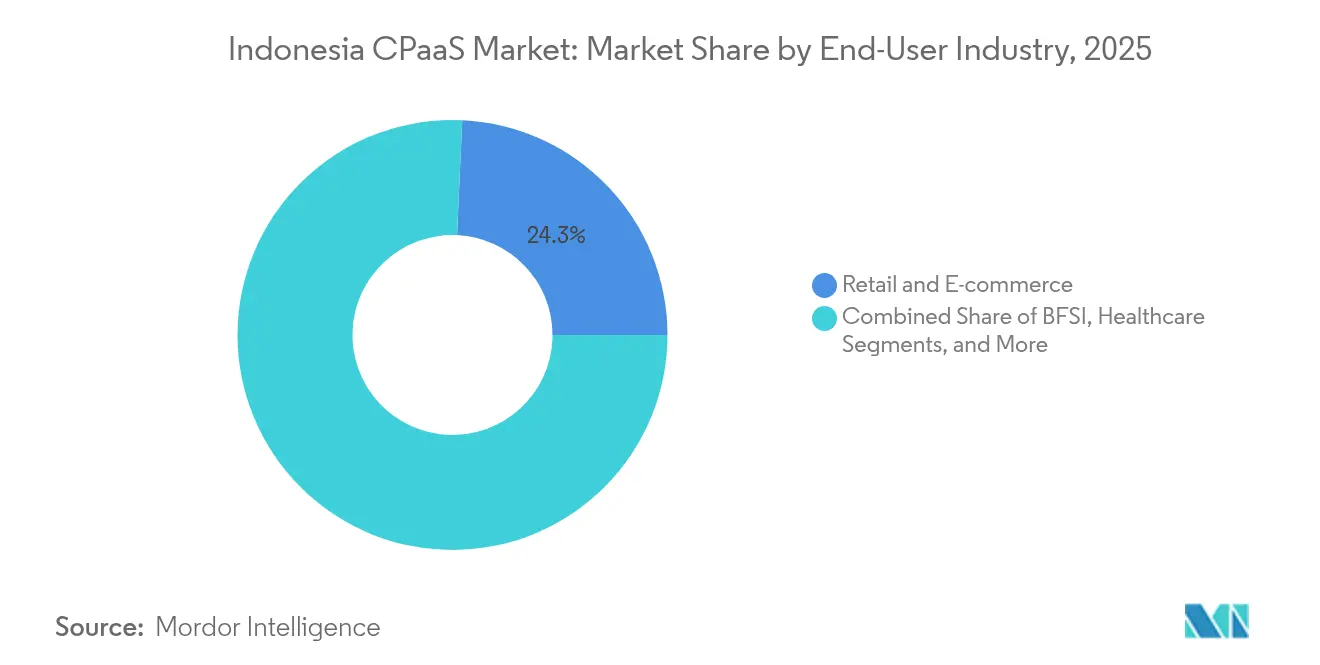

- By end-user sector, retail and e-commerce commanded 24.28% revenue in 2025 in the Indonesia CPaaS market; healthcare is growing most quickly at a 34.62% CAGR to 2031.

- By delivery model, API integration accounted for 54.83% of the Indonesia CPaaS market size in 2025, while visual flow-builder tools are rising with a 34.97% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia CPaaS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce transaction volumes driving OTP and notification traffic | +8.2% | National, concentrated in Java and major urban centers | Short term (≤ 2 years) |

| Growing smartphone penetration enabling rich omnichannel engagement | +7.1% | National, with accelerated adoption in tier-2 cities | Medium term (2-4 years) |

| Regulatory tailwinds for fintech and e-KYC boosting secure messaging demand | +6.8% | National, with early gains in Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| Post-pandemic shift to telemedicine and remote engagement across sectors | +5.4% | National, with higher penetration in urban areas | Short term (≤ 2 years) |

| Government digital social-assistance programs requiring CPaaS infrastructure | +4.7% | National, targeting rural and underserved populations | Long term (≥ 4 years) |

| Conversational commerce growth in tier-2 cities via local chat apps | +3.5% | Tier-2 and tier-3 cities, regional expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising e-commerce transaction volumes boosting OTP traffic

Digital payment value hit IDR 399.6 trillion in 2024 and continues to expand, generating large authentication volumes that flow directly into CPaaS platforms. Fintech operator BukuWarung achieved a 15% lift in OTP conversion and 97% delivery by blending SMS with WhatsApp Business API, illustrating how performance optimization strengthens the Indonesia CPaaS market.[4]Bird Case Study Team, “BukuWarung Increases OTP Conversion,” bird.com Super-apps such as GoTo and Grab bundle payments, ride-hailing, and delivery, sustaining real-time messaging across order confirmations, promotions, and fraud alerts. Urban saturation is now giving way to tier-2-city growth as smaller merchants digitize checkout flows. Consequently, providers differentiate through channel fail-over algorithms and template compliance to sustain delivery quality.

Growing smartphone penetration enabling rich engagement

More than 180 million Indonesians use smartphones, laying the groundwork for video calling, interactive chat, and in-app voice that extend well beyond traditional SMS. Telkomsel’s programmable video APIs supported 99% attendance in online education and 85% satisfaction in telemedicine, highlighting the ability of richer media to improve outcomes. WhatsApp Business API prices, USD 0.0411 for marketing, USD 0.02 for utility, and USD 0.03 for authentication, encourage brands to shift toward conversational channels. Fiber-optic projects spanning 12,100 km plus 5G rollout underpin low-latency applications such as live-stream shopping. As a result, the Indonesia CPaaS market sees growing demand for SDKs that simplify video and voice integration for non-technical teams.

Fintech and e-KYC regulations driving secure messaging need

Otoritas Jasa Keuangan’s POJK 03/2024 mandates stricter governance and consumer protection, compelling payment gateways and lenders to adopt secure multi-factor communications. Telkomsel’s alliance with Tencent Cloud extends palm-vein e-KYC from pilot to enterprise scale, embedding biometric authentication within CPaaS workflows. Digital bank Superbank integrates wallet-based notifications to tighten fraud controls while streamlining onboarding. As compliance thresholds rise, P2P lenders must raise IDR 25 billion minimum capital by 2025, platform owners require scalable, regulation-ready communications, widening the Indonesia CPaaS market footprint.

Post-pandemic pivot to telemedicine and remote services

Ministry of Health Regulation 20/2019 formalized telemedicine, pushing hospitals and clinics to deploy secure patient messaging, appointment reminders, and video consultations. Government health-check programs covering 10,000 Puskesmas rely on automated outreach to manage screenings and follow-ups. Enterprises beyond healthcare adopted remote service delivery, with omnichannel contact centers recording 85% satisfaction on daily chat volumes above 1,000. Citizen-services platform SP4N-LAPOR enforces three-day verification and five-day resolution, requiring bulletproof notification layers across ministries. These multisector use cases sustain recurring CPaaS volumes and foster long-term contract growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price pressure from declining SMS termination rates | -4.2% | National, affecting all carriers and CPaaS providers | Short term (≤ 2 years) |

| Stricter data-privacy law (PDP 2022) raising compliance costs | -3.8% | National, with higher impact on SME adoption | Medium term (2-4 years) |

| Network latency in outer islands limiting real-time API performance | -2.9% | Eastern Indonesia, remote islands, and outer provinces | Long term (≥ 4 years) |

| Carrier filtering of A2P messages impacting deliverability | -2.1% | National, with varying intensity across Telkomsel, XL, and Indosat networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price pressure from declining SMS termination rates

Domestic A2P SMS pricing has slipped to USD 0.0284, squeezing legacy-text margins and prompting providers to pivot toward higher-value channels. Carriers apply spam filters that can block up to 20% of unregistered traffic, pushing enterprises toward registered sender IDs and template fees. Infobip’s work with Indosat monetizes A2P through revenue-sharing yet still caps upside, reinforcing the urgency to upsell RCS, WhatsApp, and voice. Providers neutralize margin loss by bundling analytics, fail-over routing, and compliance tooling. As a result, the Indonesian CPaaS market gradually shifts revenue mix toward omnichannel packages rather than per-SMS volume.

Personal Data Protection Law raising compliance costs

The PDP Law’s data-localization rules and stiff breach fines create costly security obligations, especially for MSMEs that drive 57% of GDP. CPaaS platforms must add encryption at rest, audit trails, and consent-management layers, raising total-cost-of-ownership. Telkomsel’s Data Cleanroom collaboration with TikTok demonstrates how providers can share insights without raw-data exposure. Yet smaller vendors often lack capital for such tooling and may exit or merge, trimming competitive diversity. In the near term, compliance fatigue slows SME onboarding, though it eventually favors integrated platforms able to spread security investment across a larger user base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Channel: RCS poised to erode SMS leadership

SMS generated the largest slice of the Indonesia CPaaS market size at USD 46.57 million in 2025, equating to 37.92% share, yet growth slows amid saturation and pricing pressure. Telkomsel’s January 2024 tri-partite push with Singtel and Google accelerates RCS rollout, offering verified sender IDs and in-chat payments that lift click-through by 15% compared with plain text. OTT channels, especially WhatsApp Business API, record 110% usage growth, turning rich conversational commerce into table stakes. Voice APIs serving collections and customer care sustain 80% connection success, while programmable video fuels telehealth and e-learning. The evolving mix boosts average revenue per user despite SMS price deflation, keeping the Indonesia CPaaS market on its steep trajectory.

As enterprises adopt fail-over logic, an outbound OTP can trigger sequential SMS, WhatsApp, then voice calls, maximizing delivery certainty. Healthcare providers increasingly rely on video integrations for doctor-patient sessions, pushing up bandwidth-driven revenues. Push notifications tie mobile-app retention to transactional messages, and email remains indispensable for invoicing and compliance. Regulatory backing for RCS through Telekom Indonesia standardization ensures that the ecosystem matures quickly. Consequently, channel diversification mitigates risk and cements long-term revenue in the Indonesia CPaaS market.

By Enterprise Size: SMEs ignite the next growth wave

Large organizations spanning telecom, banking, and public administration generated 61.96% of the Indonesia CPaaS market share in 2025, leveraging in-house IT teams to orchestrate complex flows over API integrations. Their scale delivers predictable, multi-year contracts that underpin provider revenue. However, SMEs, defined as firms with fewer than 250 employees, are forecast to log a blazing 34.95% CAGR, shrinking the dominance gap by 2031. Government schemes such as Mitra Bukalapak expand digital-tool adoption across 8 million micro-retailers, many of whom shift cash payments to QRIS, thereby requiring instant confirmation messages.

SMEs gravitate to subscription bundles that pair WhatsApp templates with low-code flow builders, reducing onboarding to minutes. Mekari Qontak’s free-tier CRM linked to programmable messaging exemplifies this price-sensitive model, drawing thousands of merchants per month. Meanwhile, regulatory sandbox access gives young fintechs the confidence to deploy CPaaS without prohibitive compliance investment. As low-code interfaces mature, SMEs will represent a disproportionate share of incremental message volume, reinforcing their pivotal role in the Indonesia CPaaS market.

By End-User Industry: Healthcare leads in velocity

Retail and e-commerce retained 24.28% of revenue in 2025 through persistent order status alerts, delivery tracking, and flash-sale pushes. Yet healthcare registers the fastest 34.62% CAGR as clinics and hospitals embed video consultations, secured patient messaging, and prescription reminders. Telemedicine players capitalize on Ministry of Health incentives that reimburse online visits, ensuring stable traffic. Banking and fintech contribute sizeable OTP and fraud-alert loads under OJK guidelines, while logistics providers rely on geofenced notifications to cut mis-deliveries.

Government usage scales swiftly via SP4N-LAPOR! and INA Digital integration that cover education, social assistance, and payment portals. Media, education, and professional services round out demand with webinar reminders and digital-signature routing. Sector diversification insulates the Indonesia CPaaS market from cyclical shocks, ensuring broad-based momentum through 2030.

By Delivery Model: Low-code adoption accelerates

API integration secured 54.83% of 2025 revenue as developers sought granular control and microservice alignment. Telkomsel boasts 99% API success across programmable voice, facilitating number masking for ride-hailing and debt-collection workflows. Visual flow builders surge at 34.97% CAGR because marketing teams need drag-and-drop orchestration without deep coding. Vonage’s Network Registry exposes carrier APIs, quality of service, location, fraud insights, within low-code consoles, democratizing advanced capabilities.

SDKs embedded in mobile apps enable contextual in-app chat and video, while managed services resonate with firms that prefer outsourcing compliance and monitoring. Indonesia projects a 9-million-worker IT skills gap by 2030, making low-code tooling essential. This talent constraint steers CIOs toward turnkey platforms, broadening the Indonesia CPaaS market user base and fortifying ARR growth.

Geography Analysis

Java dominates early adoption because Jakarta, Surabaya, and Bandung concentrate economic activity and fiber coverage, accounting for roughly two-thirds of 2025 CPaaS revenue. Average fixed broadband in these cities exceeds 45 Mbps, allowing instant video calls and high-fidelity RCS feeds. The Indonesia CPaaS market size tied to Java stood near USD 79.12 million in 2025, but saturation pushes providers to market aggressively beyond the island.

Tier-2 and tier-3 cities, Semarang, Palembang, and Balikpapan, now contribute the fastest growth as merchant digitization expands. Government estimates show secondary regions will deliver half of national digital-economy output by 2025, supported by Palapa Ring’s 12,100-km fiber backbone and more than 1,600 new BTS sites. CPaaS volumes in these areas spike when merchants adopt QRIS, requiring real-time confirmations and settlement alerts.

Outer-island markets, including Sulawesi, Maluku, and Papua, face average mobile broadband of 24.6 Mbps, creating latency challenges for video and voice. The SATRIA-1 satellite offsets some limitations by supplying 150 Gbps across 93,000 public facilities, enabling basic messaging and audio calls. Public-sector budgets allocate IDR 400.3 trillion for digital infrastructure in 2025, incentivizing carriers to extend 5G footprints. Consequently, the Indonesia CPaaS market gains an expanding perimeter, albeit with channel-mix adjustments favoring SMS and lightweight push notifications where bandwidth remains constrained.

Competitive Landscape

Global majors such as Twilio, Infobip, Vonage, and Sinch anchor the high-end with enterprise-grade SLAs and global routing footprints. Vonage’s February 2024 partnership allows Telkomsel developers to tap network APIs, QoS, device status, fraud signals, reducing integration times from weeks to hours. These alliances ensure message deliverability above 98% and set performance benchmarks across the Indonesia CPaaS market.

Local challengers, Mekari Qontak, Citcall, and ValueFirst Indonesia, differentiate through Bahasa-first interfaces, SME-friendly pricing, and on-ground support teams. Citcall’s pay-as-you-go voice OTPs resonate with fintech apps that must verify users swiftly without long-term contracts. Carrier-owned platforms like Telkomsel Enterprise wield network proximity and data sovereignty, boasting 85% customer-satisfaction rates for omnichannel dashboards. XL Axiata’s 2024 merger with Smartfren hints at future CPaaS collaborations leveraging combined spectrum and subscriber bases.

Technology roadmaps converge on AI-assisted orchestration that predicts optimal channels, timings, and content. Telkom Indonesia’s multimodal LLM venture with Reka AI positions it to launch voice bots fluent across 700 languages, lowering regional adoption barriers. Competitive intensity remains high as providers race to embed compliance features, data localization, consent logs, encryption, as native functions, a differentiator in a PDP-Law environment. Overall, the Indonesia CPaaS market hosts a vibrant mix of global scale and localized agility.

Indonesia CPaaS Industry Leaders

Twilio Inc.

NTT Communications Corporation

Plivo Inc.

OCA Indonesia Inc. (Telkom Indonesia)

Infobip Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Telkomsel and Tencent Cloud unveiled an AI-driven cloud suite covering palm-vein e-KYC, AI-generated content, and cost-optimization services to bolster enterprise scalability.

- March 2025: Telkomsel and TikTok signed an MoU to roll out Telco Verify silent authentication and Data Cleanroom analytics that comply with PDP Law.

- October 2024: The Satu Data Indonesia program updated data-management regulations to harmonize with the PDP Law, reinforcing secure API exchange across ministries.

- August 2024: Telkom Indonesia allied with Reka AI to build multimodal language models covering 700+ local dialects to enhance CPaaS chatbots.

Indonesia CPaaS Market Report Scope

Communications platform as a service (CPaaS) is a cloud-based platform that equips businesses with application programming interfaces (APIs) to seamlessly integrate real-time communication features, ranging from voice calls and SMS to video chat, into their applications. Notable communication capabilities of CPaaS encompass SMS, MMS, and even social media messaging channels.

The Indonesia Communication Platform-as-a-Service (CPaaS) market is segmented by organization size (SME, large-scale organization), by end user (IT & telecom, BFSI, retail and E-commerce, healthcare, other end-user verticals). The report offers market forecasts and size in value (USD) for all the above segments.

| SMS |

| Voice |

| Video |

| Push Notifications |

| OTT Messaging (WhatsApp, LINE, etc.) |

| Rich Communication Services (RCS) |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Retail and E-commerce |

| Healthcare |

| IT and Telecom |

| Transportation and Logistics |

| Government |

| Other End-user Industries |

| API Integration |

| SDK / Software Toolkit |

| Visual Flow Builder / Low-Code |

| Managed Services / Bundled Solutions |

| By Communication Channel | SMS |

| Voice | |

| Video | |

| Push Notifications | |

| OTT Messaging (WhatsApp, LINE, etc.) | |

| Rich Communication Services (RCS) | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-user Industry | BFSI |

| Retail and E-commerce | |

| Healthcare | |

| IT and Telecom | |

| Transportation and Logistics | |

| Government | |

| Other End-user Industries | |

| By Delivery Model | API Integration |

| SDK / Software Toolkit | |

| Visual Flow Builder / Low-Code | |

| Managed Services / Bundled Solutions |

Key Questions Answered in the Report

How large is the Indonesia CPaaS market in 2026?

The Indonesia CPaaS market size is USD 163.61 million in 2026 and is forecast to rise to USD 686.51 million by 2031.

Which sector is growing fastest within CPaaS adoption?

Healthcare is recording the highest 34.62% CAGR as telemedicine, patient reminders, and secure consultations scale nationwide.

Why are SMEs important for future CPaaS growth?

Small and medium enterprises are projected to grow at 34.95% CAGR because low-code messaging tools and government digitization programs lower adoption barriers.

What channels are overtaking SMS?

Rich Communication Services and WhatsApp Business API traffic are expanding rapidly, fueled by verified sender IDs, in-chat payments, and interactive templates.

How does regulation influence CPaaS demand?

POJK 03/2024, PDP Law obligations, and mandatory INA Digital integrations require secure, compliant messaging frameworks, driving enterprise reliance on mature CPaaS platforms.

Page last updated on: