Indonesia Managed Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

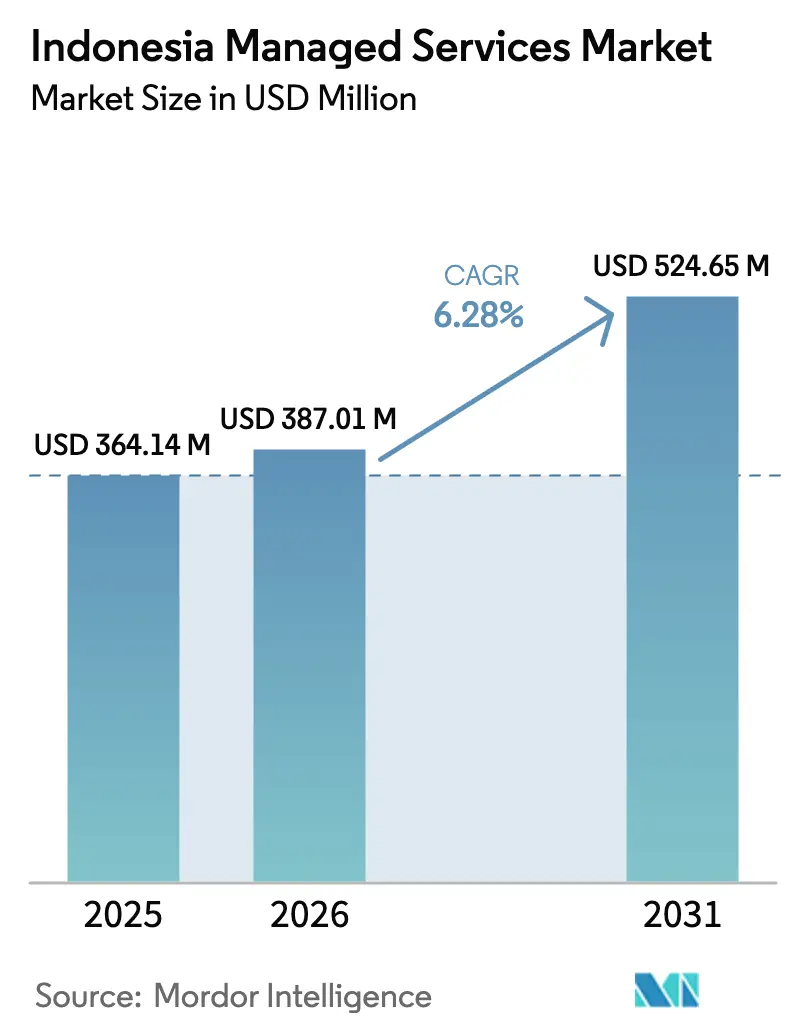

| Base Year Market Size (2025) | USD 364.14 Million |

| Market Size (2026) | USD 387.01 Million |

| Market Size (2031) | USD 524.65 Million |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Managed Services Market Analysis by Mordor Intelligence

The Indonesia managed services market size is expected to grow from USD 364.14 million in 2025 to USD 387.01 million in 2026 and is forecast to reach USD 524.65 million by 2031 at 6.28% CAGR over 2026-2031. This uptick mirrors a nationwide pivot toward cloud-first IT architectures, stricter cyber-security mandates, and steady inflows of hyperscale data-center capital that collectively expand the addressable base for outsourced IT expertise. Government SPBE requirements, the Personal Data Protection Law, and fast-growing e-commerce volumes are accelerating adoption of full-scope managed security, cloud, and application services across industries. Enterprises value the predictable costs and guaranteed service-level agreements that managed providers deliver in a market where senior engineering talent remains scarce. Hyperscale investments such as Digital Realty’s USD 499 million Jakarta campus and Microsoft’s multi-year cloud pledge signal long-term confidence that the Indonesia managed services market will keep expanding despite near-term connectivity gaps outside Java.

Key Report Takeaways

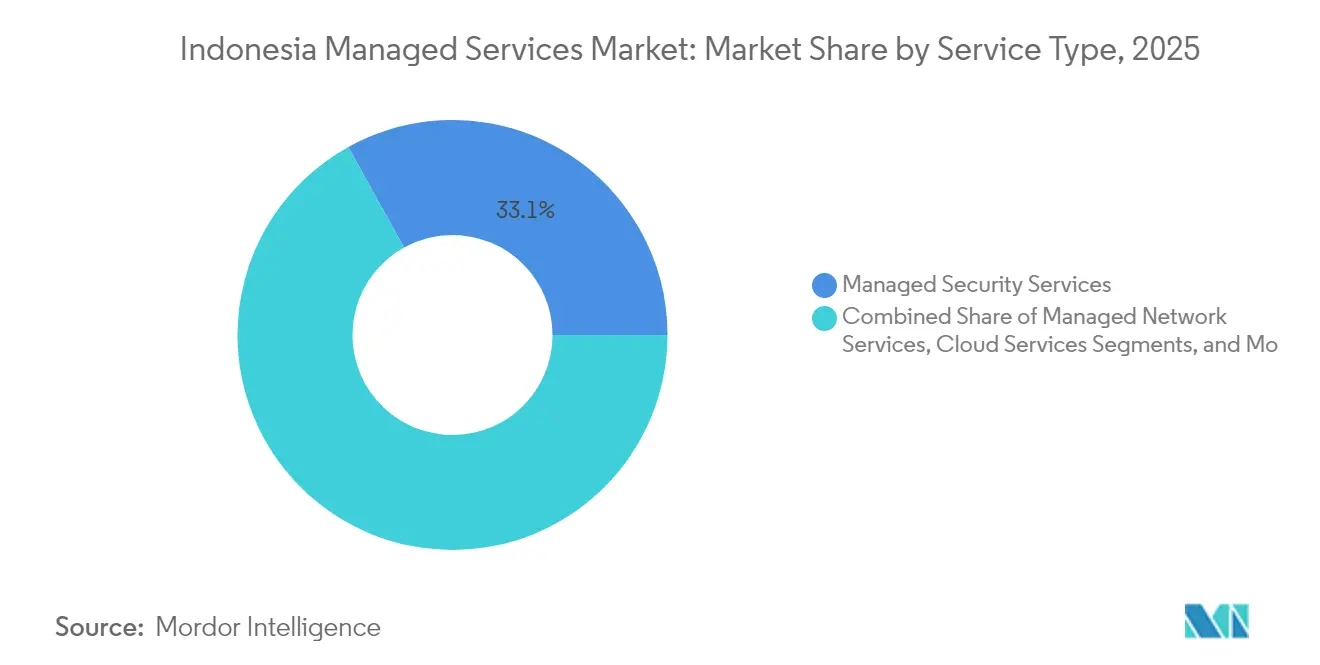

- By service type, managed security services captured 33.05% of the Indonesia managed services market share in 2025, while managed cloud services are projected to advance at a 16.52% CAGR through 2031.

- By deployment type, cloud-based models commanded 63.80% share of the Indonesia managed services market size in 2025 and are on track for a 15.9% CAGR to 2031.

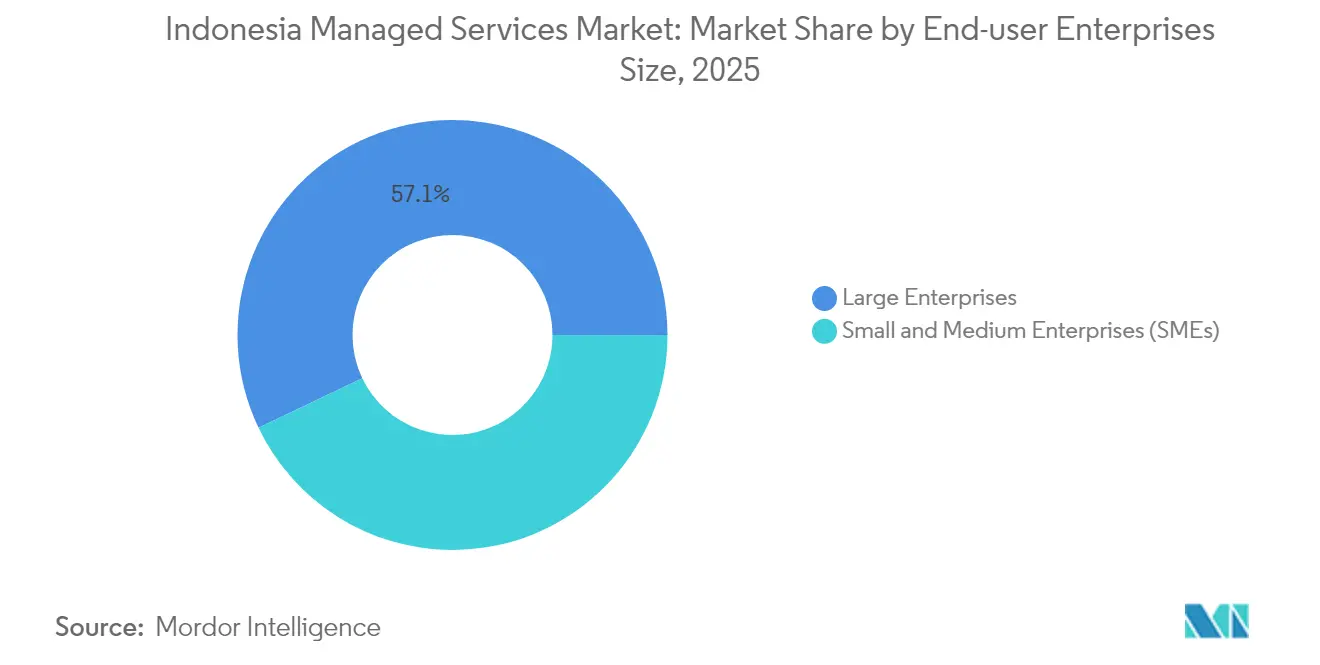

- By end-user enterprise size, large enterprises accounted for 57.10% of the Indonesia managed services market size in 2025, whereas SMEs will expand at an 17.69% CAGR during the outlook period.

- By end-user industry, BFSI led with 23.20% Indonesia managed services market share in 2025; retail and e-commerce are poised for the fastest 18.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cloud-first enterprise strategies | +1.2% | Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| Government SPBE digital-transformation mandate | +1.8% | Nationwide, binding on agencies and SOEs | Short term (≤ 2 years) |

| Escalating cyber-threat environment | +1.4% | Financial hubs, national scope | Short term (≤ 2 years) |

| Submarine-cable landings and data-center corridors | +0.9% | Java–Sumatra with reach to eastern provinces | Long term (≥ 4 years) |

| Local hyperscale facilities | +0.7% | Greater Jakarta, Surabaya, Batam, Bali | Medium term (2-4 years) |

| Digital-economy special zones for SMEs | +0.6% | Mandalika, Batam, Kendal, Nongsa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government SPBE Digital-Transformation Mandate

The SPBE regulation obliges every public agency to digitize core processes by 2025, instantly enlarging demand for cloud migration, security operations, and application-management contracts. The National Data Center in Cikarang online since August 2024 with 25,000 CPU cores and 40 PB storage illustrates the state’s preference for centralized, professionally managed platforms[1]Cloud Computing Indonesia. "Proyek Pusat Data Nasional Dipercepat, Diresmikan 17 August 2024. State-owned enterprises must meet parallel targets, and their suppliers are adapting in tandem to keep public-sector business, spreading a ripple effect across the Indonesia managed services market. Because neighboring ASEAN states lack a comparable mandatory framework, service providers view SPBE as a structural advantage that will support multi-year revenue visibility.

Escalating Cyber-Threat Environment and Compliance Fines

Indonesia’s Personal Data Protection Law entered enforcement in October 2024, levying sizable penalties on breached organizations and spurring a rush toward managed security operations. Financial institutions face additional OJK anti-fraud rules that require 24-hour threat monitoring, incident response, and audit-ready reporting. With qualified cybersecurity engineers in short supply nationally, outsourcing emerges as the only feasible path for mid-sized and smaller banks. Providers with Indonesian data-center footprints gain further edge because cross-border transfer clauses favor local processing[2]Info Komputer. "Teknologi AI Privat Bakal Jadi Tren Infrastruktur IT 2025 di Indonesia." December 20, 2024.

Rapid Cloud-First Strategies Among Enterprises

Hyperscalers are scaling local zones and training programs in anticipation of broader cloud workloads. Microsoft’s multiyear commitment, coupled with workforce-skilling targets, illustrates how capital and capability are converging to sustain cloud adoption momentum[3]Bloomberg. "Microsoft (MSFT) to Invest $1.7 Billion in Cloud Computing, AI Tech in Indonesia." April 30, 2024. Enterprises are migrating beyond basic IaaS into managed database, AI model hosting, and DevSecOps pipelines, expanding contract value per customer. Local AI models such as Sahabat-AI underscore the growing need for managed orchestration and governance services to comply with data-sovereignty norms while enabling innovation

Submarine-Cable Landings and Data-Center Corridors

The Palapa Ring backbone finished in 2024, while new subsea systems and hyperscale campuses reduce latency and make high-availability SLAs realistic outside Java. Digital Realty’s CGK11 site starts with 5 MW but is pre-designed for 32 MW, offering wholesale space for service providers that need proximity to cloud on-ramps. Parallel projects in Batam and Bali extend the footprint, creating geographic diversification for disaster recovery and edge workloads. These physical upgrades underpin long-term demand by making nationwide service delivery technically viable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of senior cloud and security engineers | -1.6% | Jakarta, Surabaya tech clusters | Short term (≤ 2 years) |

| High price-sensitivity among SMEs | -1.1% | Outer islands and rural districts | Medium term (2-4 years) |

| Inter-island network latency outside Java | -0.8% | Kalimantan, Papua, eastern provinces | Long term (≥ 4 years) |

| Uncertain data-sovereignty rule-making | -0.7% | Nationwide, cross-border cloud connections | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Senior Cloud and Security Engineers

Annual demand for qualified cloud architects and SOC analysts far exceeds the domestic talent pipeline, forcing providers into costly salary bidding that narrows operating margins. Remote-work arrangements partly alleviate the gap, yet visa limits curb large-scale inflows of expatriate specialists. Hyperscaler academies are scaling boot-camp programs, but meaningful capacity increases will take multiple years. Until then, service quality variations remain a market-wide concern.

High Price-Sensitivity Among SMEs

SMEs form the bulk of Indonesian enterprises, yet many perceive managed services as non-essential overhead. Government programs now subsidize 100 Mbps broadband at monthly fees below USD 100 to jump-start digital adoption. Even so, comprehensive managed security or multi-cloud governance contracts often remain outside SME budgets. Providers that bundle essential support into subscription tiers or leverage digital-economy zones for scale can improve affordability, but price elasticity will still temper market penetration in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Security Dominance with Cloud Momentum

Managed Security Services contributed 33.05% to the Indonesia managed services market share in 2025, a lead rooted in new data-protection fines and headline breaches that keep security at board-level priority. The Indonesia managed services market size for this segment is projected to expand steadily as regulatory scope widens. In parallel, managed cloud services post a 16.52% CAGR through 2031, buoyed by hyperscale infrastructure growth and enterprise migration into AI workloads that exceed in-house administration capabilities. Network and IT Infrastructure services remain indispensable, particularly as organizations modernize WAN topologies to support SaaS consumption. Application, communication-collaboration, and mobility services round out portfolios, and sovereign AI offerings such as GPU Merdeka indicate how traditional service lines are blending with emerging compute demands.

Cost certainty, guaranteed availability, and compliance peace-of-mind explain why even regulated sectors migrate critical workloads to managed platforms. Providers increasingly differentiate on vertical expertise such as PCI-DSS for payments or IEC 62443 for industrial control making single-vendor, multi-service deals commonplace. As more enterprises adopt zero-trust architectures, cross-selling opportunities between security operations, endpoint management, and identity services enlarge contract values inside the Indonesia managed services market.

By Deployment Type: Cloud-Based Models Prevail

Cloud environments secured 63.80% of the Indonesia managed services market size in 2025 and will appreciate at a 15.9% CAGR. Enterprises view cloud as the quickest path to SPBE compliance and scalable innovation. Local availability zones remove latency barriers, while data-residency features satisfy regulators, allowing even financial firms to commit critical workloads to managed cloud. Hybrid estates survive mainly to serve legacy OT systems, but the long-run trajectory favors full cloud transformation.

On-premises contracts persist in defense, healthcare, and energy utilities where latency or sovereignty rules demand local hosting. Still, these customers increasingly offload backup, patching, and SIEM functions to external specialists. The Indonesia managed services market therefore sees converging demand: cloud-native organizations source end-to-end operations, and traditional enterprises carve out specific workloads for managed oversight as compliance pressures intensify.

By End-user Enterprise Size: Large-Company Scale, SME Growth Spark

Large enterprises accounted for 57.10% of 2025 revenue as they align multi-year IT roadmaps with data-center upgrades and advanced threat-intelligence feeds. Their contract scopes often cover 24/7 SOC, multi-cloud optimization, and DevSecOps automation, driving consistent subscription income. Nevertheless, SMEs represent the fastest 17.69% CAGR, lifted by government digital-literacy campaigns and platform pricing that now bundles baseline support with entry-level cloud plans.

Service providers refine tiered offerings that package essential monitoring, backup, and vulnerability scanning in affordable bundles. Digital-economy zones Mandalika, Batam, Kendal cluster small firms and improve provider economics, encouraging wider SME onboarding. Such democratization is crucial because SMEs collectively power domestic employment, and their digital resilience underpins confidence in the broader Indonesia managed services market.

By End-User Industry: BFSI Stays Leader; Retail Takes Off

BFSI segment preserved 23.20% Indonesia managed services market share in 2025 amid unrelenting anti-fraud directives and real-time payment rollouts that demand resilient, compliant infrastructure. Cloud-based core banking experiments accelerate outsourcing needs for application refactoring and regulatory reporting tools. Elsewhere, retail and e-commerce accelerate at 18.8% CAGR on the back of a USD 62 billion transaction base that pressures merchants to guarantee site performance during seasonal peaks.

Manufacturing extends adoption as factories introduce IoT gateways and predictive-maintenance analytics that benefit from centrally managed platforms. Government agencies rely on managed partners to satisfy SPBE milestones, while healthcare institutions cautiously progress toward tele-health models that require HIPAA-style protections. Energy, utilities, transportation, and hospitality round out an industry mix where each vertical is discovering workload pockets ideally suited for specialist managed support.

Geography Analysis

Greater Jakarta retains the lion’s share of Indonesia managed services market demand thanks to dense enterprise headquarters, sovereign data centers, and international cable landings. Digital Realty’s CGK11 opens with 5 MW and pre-allocates for a 32 MW campus, signaling sustained co-location appetite from service providers needing metropolitan proximity for low-latency SLAs. The SPBE-backed National Data Center in Cikarang further cements Java’s role as the primary hub for centralized workloads.

Surabaya and Bandung act as secondary nodes where manufacturing clusters and academic communities create both demand and talent supply. Completion of the Palapa Ring extends high-capacity fiber into Sumatra and Sulawesi, enabling providers to market uniform SLA tiers across previously underserved provinces. Batam’s Nongsa Digital Park and special-zone incentives cultivate a cross-border fintech corridor that draws Singapore-adjacent firms into managed hybrid-cloud contracts.

Eastern regions Kalimantan, Maluku, Papua still wrestle with long-haul latency and limited local data-center presence. Government plans to develop facilities in the upcoming Nusantara capital could rebalance service distribution over the long term. Tourism-centric Bali shows growing appetite for managed customer-engagement platforms as hotels and airlines prioritize digital guest experiences. Providers leveraging edge caching and regional PoPs can gain early mover advantage as economic activity disperses beyond Java.

Competitive Landscape

Indonesia managed services market competition remains moderate, with domestic telcos, hyperscalers, and niche specialists each holding meaningful footholds. PT Telkom Indonesia exploits nationwide fiber and close public-sector ties to secure multi-year IT infrastructure contracts. Global players Microsoft, AWS, Google Cloud offer advanced analytics and AI platforms, positioning themselves for multi-cloud orchestration deals that domestic rivals cannot match in depth.

Differentiation increasingly hinges on data-sovereignty guarantees and vertical compliance expertise. Lintasarta’s GPU Merdeka demonstrates how local providers counter foreign competition through sovereign AI services that keep sensitive training data onshore. Aggressive merger activity 19 tech-startup MandA deals in 2024 worth USD 1.64 billion shows firms seeking scale, skill, and geographic reach to meet enterprise SLAs.

Talent scarcity amplifies competitive pressure; providers equipped with in-house academies can secure engineers faster and maintain service quality reliability. Strategic alliances also blossom: Indosat Ooredoo Hutchison partners with AIonOS to develop industry-specific AI frameworks that necessitate managed deployment and monitoring. Over the forecast horizon, market share is likely to consolidate around operators that combine sovereign infrastructure, certified expertise, and industry-tuned service catalogs.

Indonesia Managed Services Industry Leaders

-

Zettagrid Indonesia

-

Telkomsigma

-

PT VADS Indonesia

-

PT Cyberindo Mega Persada (CBNCloud)

-

Eranyacloud

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Indosat Ooredoo Hutchison and AIonOS signed a Government-to-Government MoU to grow Indonesia’s AI ecosystem under the AI³ initiative.

- February 2025: GoTo Group and Indosat Ooredoo Hutchison introduced Sahabat-AI, an open-source LLM optimized for Bahasa and regional languages.

- January 2025: Digital Realty formed a USD 499 million data-center joint venture with Bersama Digital Infrastructure Asia, launching 5 MW capacity expandable to 32 MW.

- November 2024: GoTo Group debuted Sahabat-AI with 8-billion and 9-billion parameter models for localized applications.

- August 2024: Lintasarta unveiled GPU Merdeka, a sovereign NVIDIA-powered AI cloud service.

Indonesia Managed Services Market Report Scope

The Indonesian managed services market study tracks the demand for end-to-end services related to infrastructure management, networking, data centers, etc., outsourced to third-party vendors in Indonesia based on the service-based revenues accrued by vendors operating in Indonesia.

The market studied is segmented by service type (managed security service, managed network service, and managed IT infrastructure and data center service), deployment type (on-premise and cloud), and region (Java, Sumatra, Kalimantan, and Other Regions). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Managed Security Services |

| Managed Network Services |

| Managed IT Infrastructure and Data-center Services |

| Managed Cloud Services |

| Managed Application Services |

| Managed Communication and Collaboration Services |

| Managed Mobility Services |

| On-premises |

| Cloud-based |

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| Banking, Financial Services and Insurance (BFSI) |

| IT and Telecom |

| Government and Public Sector |

| Manufacturing |

| Retail and E-commerce |

| Healthcare |

| Energy and Utilities |

| Others End-user Industry (Transportation and Hospitality) |

| By Service Type | Managed Security Services |

| Managed Network Services | |

| Managed IT Infrastructure and Data-center Services | |

| Managed Cloud Services | |

| Managed Application Services | |

| Managed Communication and Collaboration Services | |

| Managed Mobility Services | |

| By Deployment Type | On-premises |

| Cloud-based | |

| By End-User Enterprise Size | Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) | |

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) |

| IT and Telecom | |

| Government and Public Sector | |

| Manufacturing | |

| Retail and E-commerce | |

| Healthcare | |

| Energy and Utilities | |

| Others End-user Industry (Transportation and Hospitality) |

Key Questions Answered in the Report

How fast is the Indonesia managed services market expected to grow through 2031?

It is projected to expand from USD 387.01 million in 2026 to USD 524.65 million by 2031 at a 6.28% CAGR.

Which service line currently leads adoption in Indonesia?

Managed Security Services hold the largest 33.05% revenue share because companies prioritize threat mitigation to meet new data-protection rules.

Why are cloud-based deployments dominant among Indonesian enterprises?

Cloud models command 63.80% share due to SPBE mandates, local data-center expansion, and the operational agility they offer over on-premises setups.

What is driving rapid managed-services uptake among Indonesia’s SMEs?

Government broadband subsidies, falling entry-level cloud prices, and e-commerce growth are encouraging SMEs to outsource routine IT operations.

Which industry vertical is growing fastest in managed-services spending?

Retail and e-commerce show the highest 18.8% CAGR as merchants scale platforms to support USD 62 billion in online transactions.

How will talent shortages affect providers over the next two years?

Limited availability of senior engineers is likely to squeeze margins and may prompt further industry consolidation as firms pool scarce expertise.

Page last updated on: