Jakarta Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

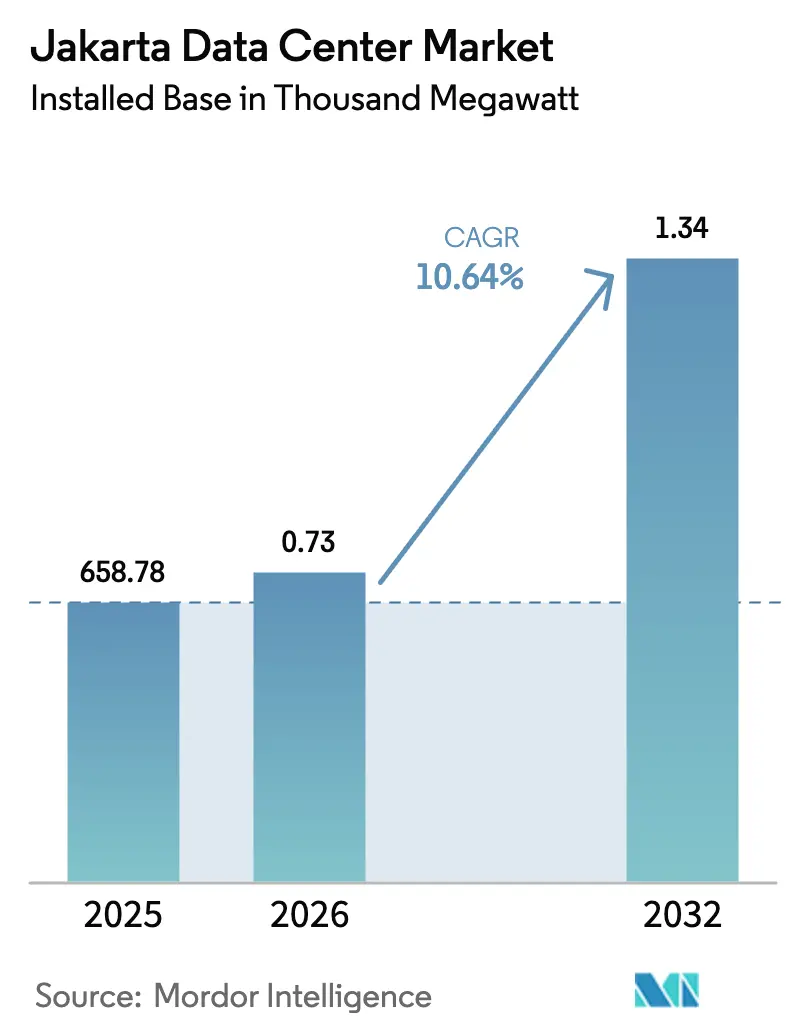

| Base Year Market Size (2025) | 658.78 Thousand megawatt |

| Market Volume (2026) | 0.73 Thousand megawatt |

| Market Volume (2032) | 1.34 Thousand megawatt |

| Growth Rate (2026 - 2032) | 10.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jakarta Data Center Market Analysis by Mordor Intelligence

Jakarta data center market size in 2026 is estimated at 728.91 MW, growing from 2025 value of 658.78 MW with 2032 projections showing 1,336.09 MW, growing at 10.64% CAGR over 2026-2032. This upward curve underscores a robust market size outlook supported by hyperscale cloud investments, a deepening 5G footprint and Indonesia’s data-sovereignty agenda. Intensifying campus builds by hyperscale tenants, the APRICOT submarine cable system’s arrival, and aggressive green-energy power-purchase agreements are further accelerating demand. Competitive pressure is already pushing colocation rents down to USD 300-320 per kVA, yet operators remain attracted by the very low per-capita installed capacity that signals ample runway. The interplay of rapid e-commerce expansion, stringent financial-services latency requirements and expanding AI workloads positions the Jakarta data center market for sustained double-digit growth.

Key Report Takeaways

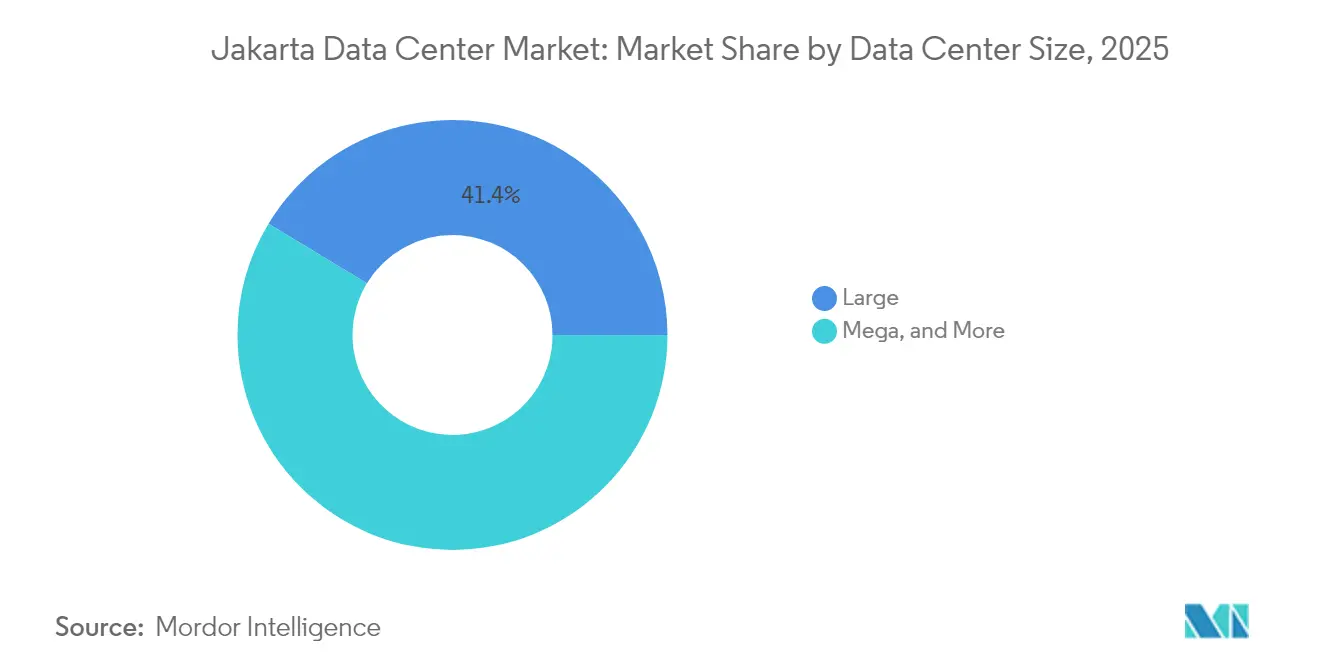

- By data center size, large facilities led with 41.35% revenue share in 2025, while mega facilities are advancing at a 20.35% CAGR through 2032.

- By tier standard, Tier III infrastructure held a 50.25% share of the Jakarta data center market size in 2025 and Tier IV deployments are growing at an 17.60% CAGR to 2032.

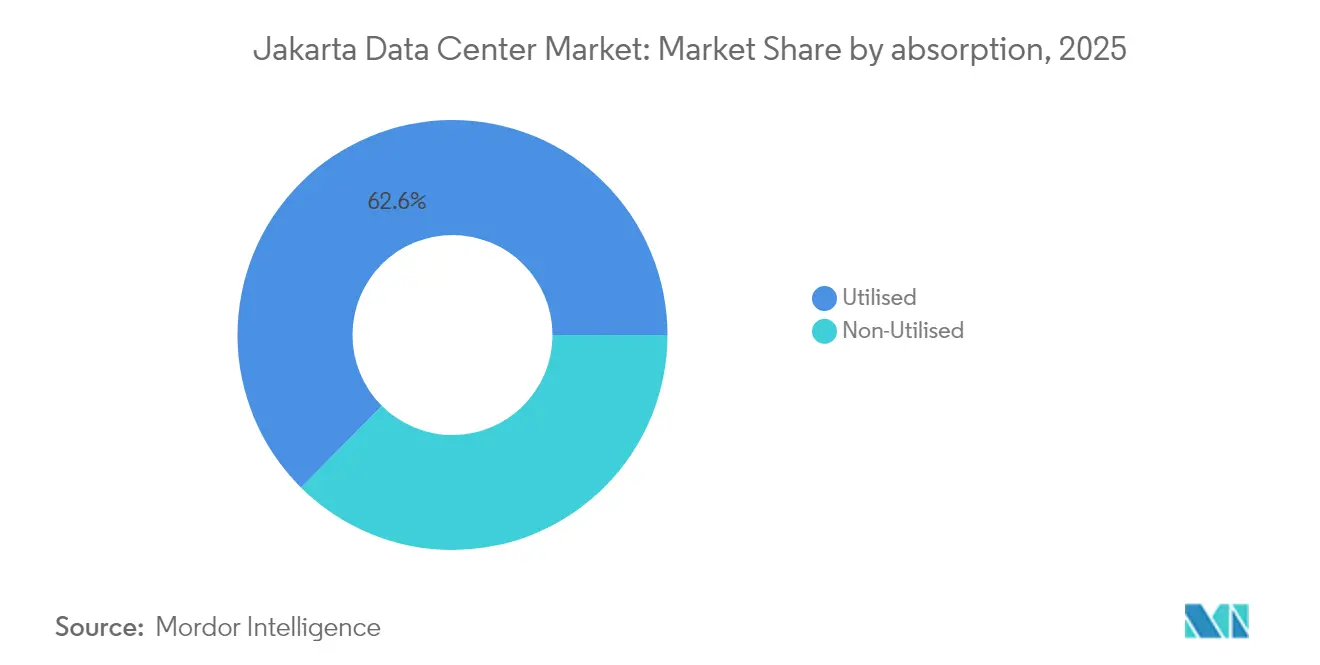

- By absorption, utilised capacity represented 62.55% of the Jakarta data center market share in 2025; hyperscale colocation is expanding at a 23.85% CAGR through 2032.

- By hotspot, Greater Jakarta accounted for 51.20% share in 2025, whereas the Bekasi-Cikarang Corridor is set to grow at a 12.94% CAGR between 2026-2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Jakarta Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding mobile-data consumption and 5G roll-out | +2.80% | Greater Jakarta, Bekasi-Cikarang Corridor | Medium term (2-4 years) |

| E-commerce and fintech boom requiring low-latency hosting | +2.10% | Greater Jakarta, Rest of Jakarta | Short term (≤ 2 years) |

| Government "Making Indonesia 4.0" and data-sovereignty push | +1.90% | National, with concentration in Greater Jakarta | Long term (≥ 4 years) |

| Influx of hyperscale cloud providers driving campus builds | +3.20% | Bekasi-Cikarang Corridor, Greater Jakarta | Medium term (2-4 years) |

| Rapid build-out of new submarine-cable landings | +1.40% | Greater Jakarta, Bekasi-Cikarang Corridor | Long term (≥ 4 years) |

| Green-energy PPAs to meet net-zero mandates unlocking permits | +0.80% | National, early adoption in Greater Jakarta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding mobile-data consumption and 5G roll-out

Indonesia’s 5G coverage accelerated in 2024, lifting total mobile data traffic by 9% to 17.9 million TB. The surge forces content and application providers to house workloads closer to end users, which in turn raises demand for low-latency edge nodes across the Jakarta data center market[1].Telecomlead, “Telkom Indonesia strategy and plans to enhance customer experience,” telecomlead.com IoT devices tied to Industry 4.0 programs are projected to contribute IDR 1,620 trillion in value by 2025, deepening the requirement for distributed processing capacity that centralized data centers cannot efficiently meet. As latency-sensitive services such as augmented-reality commerce and autonomous logistics mature, operators are prioritizing micro-modules inside dense urban footprints. These deployments improve user experience, reduce network backhaul and underpin sustained rack-fill rates. The trend also drives capital toward liquid-cooling and direct-to-chip technologies that fit high-density 5G edge environments.

E-commerce and fintech boom requiring low-latency hosting

Jakarta remains Southeast Asia’s largest e-commerce hub, and the region’s transaction-heavy platforms require resilient, latency-optimized data centers. Tokopedia reported a 10× smarter search capability after deploying vector search on AI-ready infrastructure, a result that highlights the commercial upside of high-performance hosting [2].Zilliz, “Tokopedia Achieved a 10x Smarter Search with Milvus,” zilliz.com Financial players follow suit: DOKU’s disaster-recovery configuration on Alibaba Cloud cut operating costs by 20% while safeguarding compliance with Bank Indonesia regulations. With online-payment velocity rising, colocation providers offering <2 ms round-trip latency can command premium pricing even as the broader Jakarta data center market faces rental compression. The stickiness of fintech workloads, combined with regulatory scrutiny, yields predictable occupancy and serves as a hedge against cyclical demand shifts.

Making Indonesia 4.0 and the data-sovereignty push

The government’s consolidation of 2,700 legacy facilities into a handful of national data centers is reinventing public-sector IT architecture. The flagship PDN campus in Cikarang brings 25,000 CPU cores, 40 PB of storage and 20 MW of power, underpinned by EUR 164 million in state-backed financing [3].Cloud Computing Indonesia, “Proyek Pusat Data Nasional Dipercepat,” cloudcomputing.idMandatory on-shore data residency for personal information compels multinationals to localize storage, shifting workloads out of Singapore and into the Jakarta data center market. The regulation is fostering captive demand that decouples from price competition because compliance risk outweighs hosting cost. Over the long term, the national AI strategy embeds data centers into every e-government service, anchoring sustained utilization regardless of private-sector cycles.

Influx of hyperscale cloud providers driving campus builds

Microsoft, Temasek and BlackRock have earmarked USD 30 billion for the 480 MW Project MGX hyperscale campus, signalling Jakarta’s graduation to a first-tier cloud region. Digital Realty and Bersama’s CGK11 site illustrates the new norm: starting at 5 MW, scaling rapidly to 32 MW through modular blocks. Hyperscalers demand standardized designs and end-to-end automation, forcing local incumbents to upgrade their facilities or partner for scale. The corridor east of Jakarta offers large contiguous land parcels and 150 kV grid feeds, which underpin dual-feed architectures vital to these giant deployments. As campuses expand, ecosystem participants ranging from chillers to network fabrics enjoy a multiplier effect, reinforcing the Jakarta data center market’s growth flywheel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity tariffs and grid congestion in Greater Jakarta | -1.80% | Greater Jakarta, Rest of Jakarta | Short term (≤ 2 years) |

| Land scarcity and zoning limits for large-footprint campuses | -1.20% | Greater Jakarta, moderate impact in Bekasi-Cikarang | Medium term (2-4 years) |

| Seismic and flood-risk premiums raising insurance/financing costs | -0.90% | Greater Jakarta, Rest of Jakarta | Long term (≥ 4 years) |

| Water-use restrictions for liquid-cooling in urban districts | -0.70% | Greater Jakarta, emerging in Bekasi-Cikarang | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High electricity tariffs and grid congestion in Greater Jakarta

PLN’s 2025 tariff schedule ranges from IDR 996.74 to IDR 1,699.53 per kWh for commercial accounts, inflating opex at a time when colocation prices are falling[4]Bisnis.com, “Daftar Lengkap Tarif Listrik PLN Januari–Maret 2025,” bisnis.com. The 67% share of coal in the power mix complicates renewables procurement, a key requirement for global cloud clients pursuing net-zero mandates. Grid bottlenecks delay energization dates, forcing developers to install larger diesel reserves and on-site battery systems, raising capex by 5%. Cushman & Wakefield ranks Jakarta the fourth most expensive data center construction market in Asia Pacific, evidence of combined power and labor cost pressures. These headwinds are steering future builds toward the Bekasi-Cikarang Corridor, where high-voltage feeders and industrial zoning streamline connections.

Land scarcity and zoning limits for large-footprint campuses

Urban densification has squeezed Jakarta’s supply of 10+ acre plots needed for next-gen campuses. North Jakarta Bay reclamation lifted land prices to match central-city benchmarks, eroding cost advantages. Height and power-density restrictions in many districts cap deployable IT load, challenging the economics of AI-ready halls that exceed 30 kW per rack. Environmental clearances now stretch 12-18 months, affecting project IRRs and pushing operators toward pre-zoned industrial parks east of the city. These hurdles elevate barriers to entry, favoring incumbent players with local joint-venture partners and deep permitting experience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Mega builds set the new scale benchmark

Mega facilities are rewriting the Jakarta data center market’s economics. While large sites still held the highest 2025 share at 41.35%, mega campuses are sprinting ahead at a 20.35% CAGR. That pace reflects cloud providers’ need for contiguous 20 MW blocks, standardized white space and economies of scale that shrink per-MW opex. The Jakarta data center market size attributed to mega builds is poised to more than double from 2026-2032 as AI workloads favor high-density designs.

Automation, integrated liquid-cooling and onsite sub-station builds help mega sites achieve PUE figures below 1.35. Massive facilities remain an emerging niche aligned with sovereign AI projects such as the Cikarang PDN, but the underpinning technology—immersion cooling and 100 GbE fabrics—will filter into mega campuses first. Medium and small formats retain relevance by enabling densified edge nodes for 5G and IoT deployments close to user clusters.

By Tier Standard: Tier IV certifications gain speed

Tier III still commands 50.25% of deployed power because it meets most enterprise uptime mandates without a steep cost premium. Yet the Jakarta data center market size accredited as Tier IV is projected to expand faster than any other standard, registering an 17.60% CAGR through 2032. AI inferencing clusters and real-time fintech workloads cannot tolerate scheduled downtime, pushing builders toward concurrently maintainable and fault-tolerant designs.

Dual-grid feeds, 2N+1 power architectures and ISO 14001 water-recycling systems are now baseline requirements for top-tier customers. Uptime Institute audits provide a competitive differentiator for colocation brands in bidding rounds with regulated sectors, especially banks. Tier I-II capacity remains confined to edge and content-delivery nodes where cost outweighs the benefit of extra redundancy.

By Absorption: Hyperscale colocation reshapes utilization

Utilised halls represented 62.55% of active power in 2025, reflecting healthy take-up across Jakarta’s prime campuses. Within that footprint, hyperscale cages are driving a 23.85% CAGR, eclipsing retail colocation growth as cloud providers pursue regional availability zones. The Jakarta data center market share commanded by hyperscale tenants is expected to pass the 50% mark before 2030 as multi-MW pre-commitments dominate leasing pipelines.

Non-utilised capacity remains a strategic buffer that allows operators to sign rapid-turnaround bookings without adding shell space. To maximize yield, data center landlords are deploying AI-based capacity-planning engines that rebalance power, cooling and space allocations across wholesale and retail cohorts. Edge-focused operators supplement hyperscale-centric portfolios to capture diversified revenue streams.

Geography Analysis

Greater Jakarta’s legacy connectivity and dense enterprise base gave it a 51.20% share in 2025, but land scarcity and tariff premiums are redirecting new capex toward Bekasi-Cikarang. The corridor’s 12.94% CAGR is supported by 150 kV grid links, industrial water rights and immediate proximity to landing stations for the 190 Tbps APRICOT cable.

Developers leverage lower land costs to build horizontally oriented, single-story halls that improve airflow and ease equipment logistics. Meanwhile, the rest of Jakarta hosts disaster-recovery and government-sector nodes that value geographic separation from the core business district. That mixed footprint increases resiliency across the broader Jakarta data center market.

Greater Jakarta remains the epicenter of Indonesia’s digital economy. Financial institutions and cloud-first start-ups need the sub-2 ms latency only metro-core facilities can guarantee, enabling sticky demand even as land prices climb. Equinix’s JK1 downtown site anchors peering with more than 50 carriers and validates the high-density interconnection model that underpins metro resilience.

Competitive Landscape

Intense price competition is compressing rents as new supply arrives. Conglomerates with diversified cash flows can price aggressively, prompting average colocation rates to fall to USD 300-320 per kVA in early 2025. Despite downward pressure, the Jakarta data center market continues to register new entrants because demand growth outstrips supply. Telkom Indonesia leverages a 32-site domestic network to upsell sovereign clients, while Digital Realty and Equinix rely on global ecosystems to court multinationals.

Technology leadership is pivotal. NeutraDC’s 2024 agreement with PLN secures preferential power allocation, strengthening its AI-ready positioning. EdgeConneX scales beyond 200 MW via modular block design that cuts deployment time to nine months, giving it speed-to-market advantage. Smaller incumbents often pivot toward edge and managed-service niches, or partner with foreign investors to fund capex.

M&A momentum is set to continue as capital-intensive mega projects strain balance sheets of standalone operators. Cross-border funds, regional telcos and infrastructure REITs view the Jakarta data center market as strategic, ensuring competitive tension that ultimately benefits end-users via better pricing and richer connectivity ecosystems.

Jakarta Data Center Industry Leaders

PT DCI Indonesia

Telkomsigma

NTT Communications Corporation

XL Axiata Tbk PT (Princeton Digital Group)

GTN Data Center (Edge Connex)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Equinix opened JK1, its first AI-ready International Business Exchange site in Jakarta’s CBD, offering 1,600 cabinets across 5,300 m² of colocation space.

- March 2025: Digital Realty invested USD 100 million for a 50% stake in BDIA’s campus, scaling the CGK11 data center from 5 MW to 32 MW.

- January 2025: Indonesia’s National Data Center in Cikarang moved toward March 2025 commissioning with 20 MW of power capacity to consolidate 2,700 government sites.

- December 2024: EdgeConneX expanded its Bekasi hyperscale campus to exceed 200 MW on a 45,000 m² site.

- November 2024: DCI Indonesia topped out a new data center tower in Jakarta, reinforcing its market-leading local footprint.

Jakarta Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Jakarta data center market is segmented by dc size (small, medium, large, massive, and mega), tier type (tier 1 and 2, tier 3, and tier 4), and absorption (utilized (colocation type (retail, wholescale, and hyperscale), end user (cloud and IT, telecom, media and entertainment, government, BFSI, manufacturing, and e-commerce)), and non-utilized). The market sizes and forecasts are provided in terms of volume (MW) for all the above segments.

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User Industry | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End Users | ||

| Greater Jakarta |

| Bekasi - Cikarang Corridor |

| Rest of Jakarta |

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User Industry | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End Users | |||

| By Hotspot | Greater Jakarta | ||

| Bekasi - Cikarang Corridor | |||

| Rest of Jakarta | |||

Key Questions Answered in the Report

How fast is capacity growing in Jakarta’s colocation space?

Installed IT load is projected to rise from 728.91 MW in 2026 to 1,336.09 MW by 2032, implying a 10.64% CAGR.

Which district is attracting most greenfield builds?

The Bekasi-Cikarang Corridor is the fastest-growing hotspot, set to expand at a 12.94% CAGR thanks to cheaper land, grid headroom and new submarine-cable landings.

What share of power is already committed to tenants?

Utilised halls account for 62.55% of active capacity, with hyperscale colocation driving a 23.85% CAGR in take-up.

Why are Tier IV certifications gaining traction?

AI workloads and financial-services applications require near-continuous uptime, pushing Tier IV deployments to grow at an 17.60% CAGR through 2032.

How are rental rates trending?

Intense competition has reduced average colocation pricing to USD 300-320 per kVA even as construction costs rise, suggesting continued buyer advantage.

What makes Jakarta attractive for hyperscale cloud providers?

Proximity to a 275 million-person domestic market, data-sovereignty rules, new 190 Tbps submarine cables and available industrial sites east of the city combine to form a compelling hyperscale proposition.

Page last updated on: