Individual Quick Freezing (IQF) Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

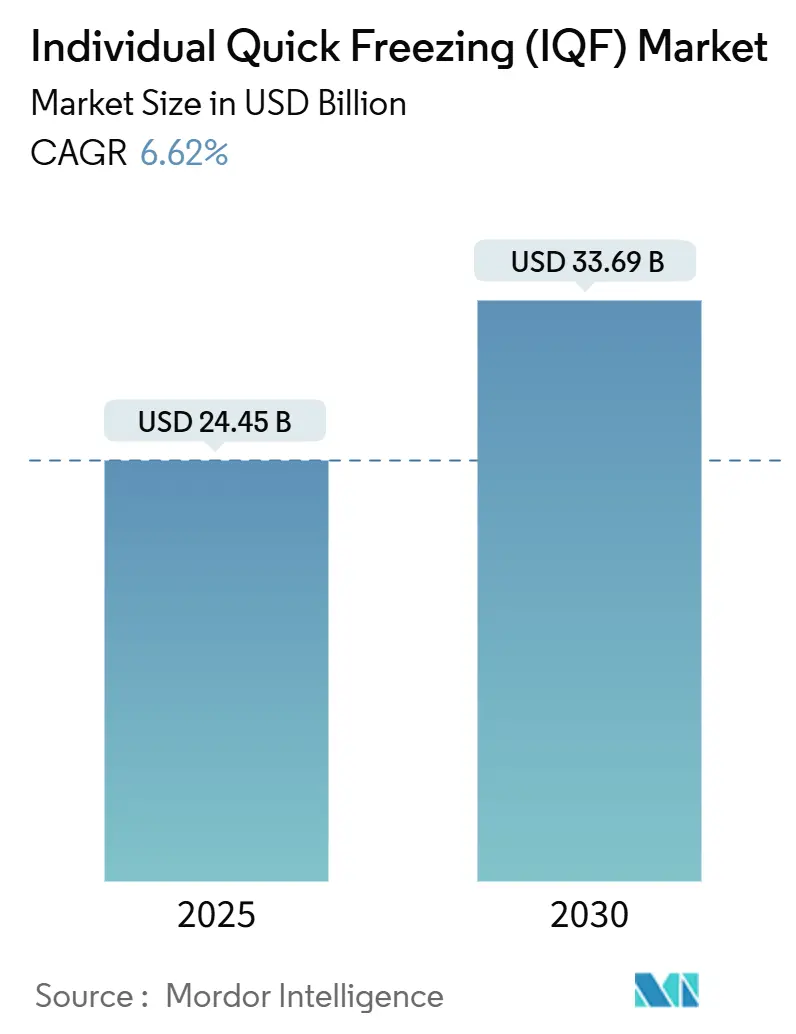

| Market Size (2025) | USD 24.45 Billion |

| Market Size (2030) | USD 33.69 Billion |

| Growth Rate (2025 - 2030) | 6.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Individual Quick Freezing (IQF) Market Analysis by Mordor Intelligence

The global Individual Quick Freezing market size achieved USD 24.45 billion in 2025 and is anticipated to reach USD 33.69 billion by 2030, demonstrating a compound annual growth rate (CAGR) of 6.62% during the forecast period. This market expansion is driven by consumers increasingly seeking convenient food options, substantial investments in retail infrastructure development, and continuous innovations in freezing equipment technology. In the current market landscape, mechanical freezing systems continue to provide cost-effective solutions for manufacturers, while cryogenic freezing technology is steadily gaining market acceptance due to its ability to deliver faster processing times and maintain higher product quality standards. The fruits and vegetables segment remains the primary revenue generator, supported by retailers' requirements for consistent year-round supply and consumer demand for natural food products. The market structure exhibits moderate consolidation, creating opportunities for regional companies to expand their operations through strategic technology partnerships and focus on specialized product categories.

Key Report Takeaways

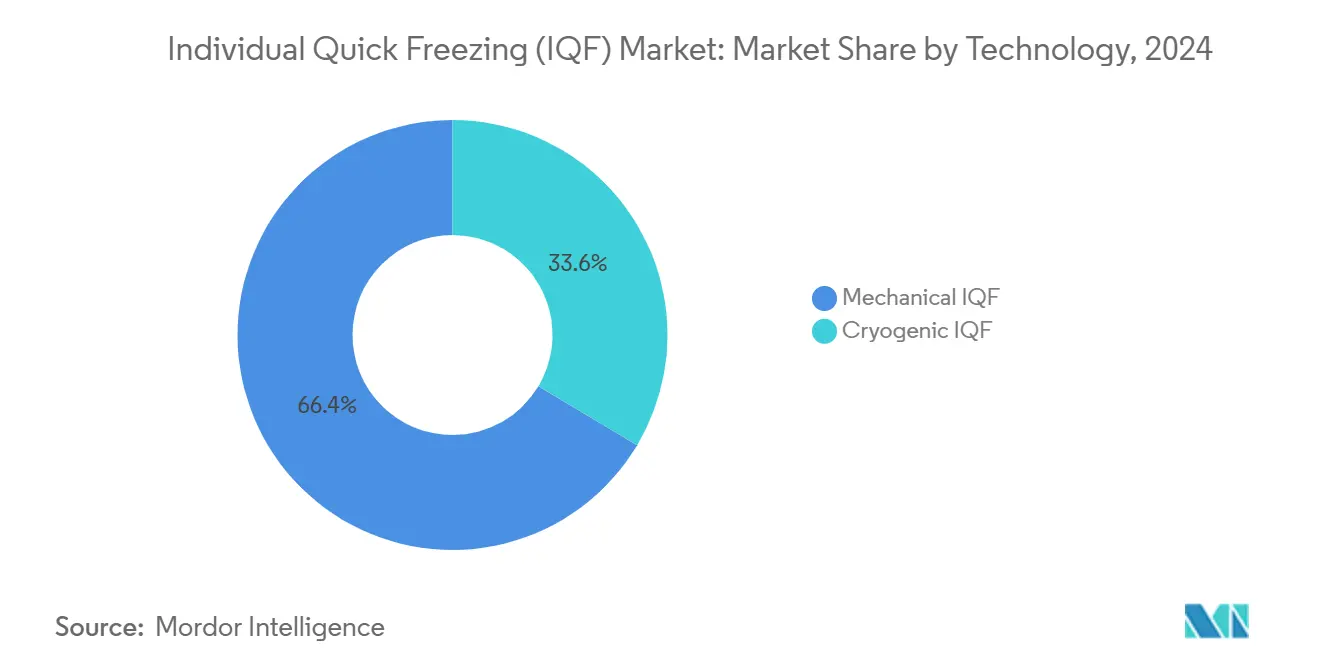

- By technology, mechanical systems captured 66.44% of Individual Quick Freezing market share in 2024 and cryogenic solutions are projected to expand at 7.37% CAGR between 2025-2030.

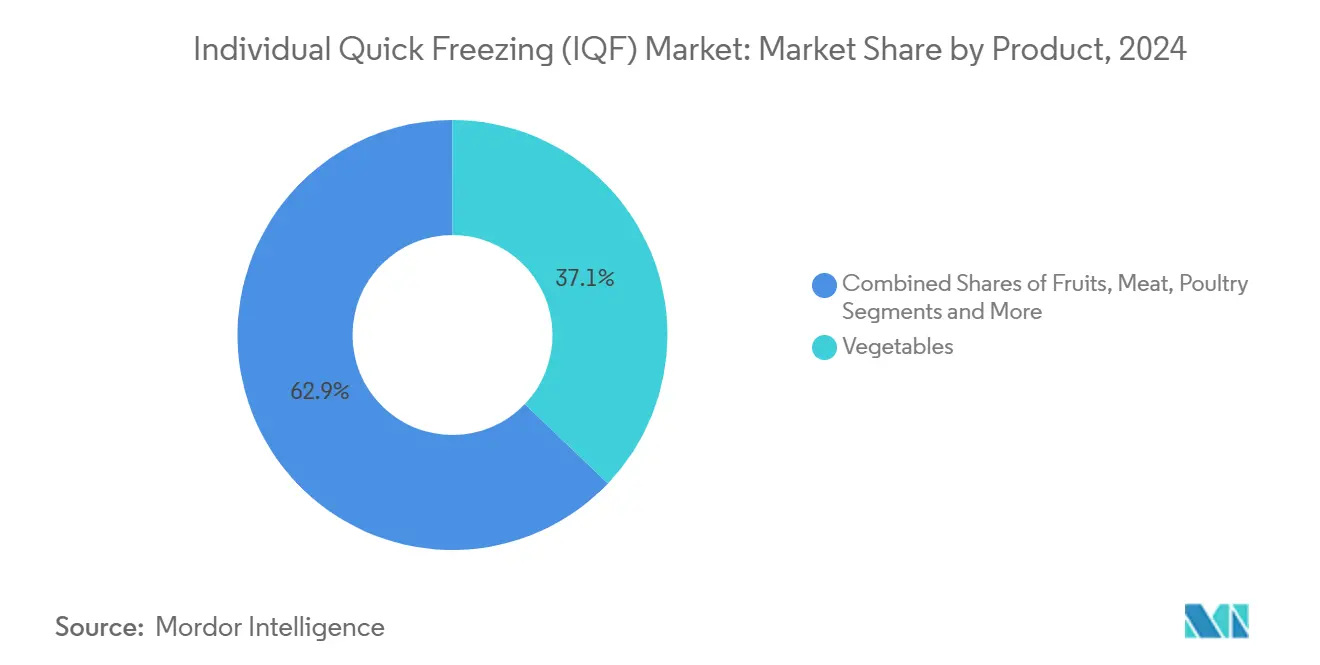

- By product, vegetables commanded 37.44% of the Individual Quick Freezing market size in 2024, while the fruits segment is forecast to post the fastest 6.99% CAGR to 2030.

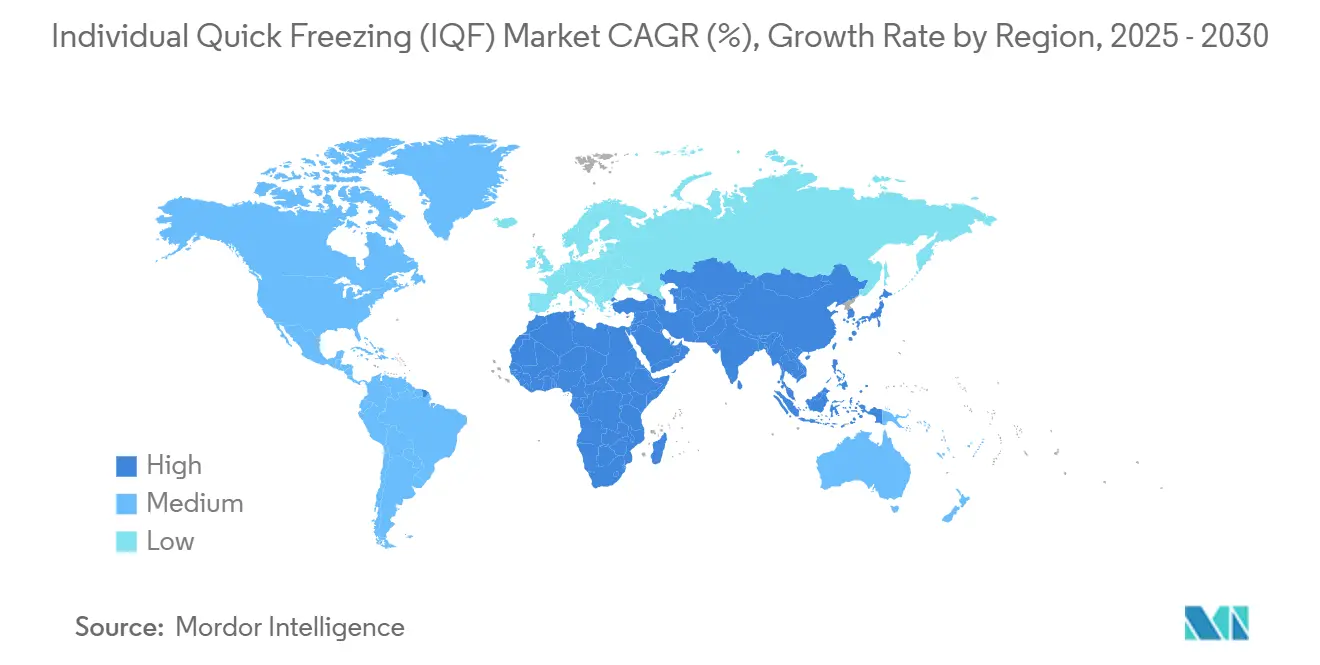

- By geography, North America held 35.22% of 2024 revenue; Asia-Pacific is pacing the outlook with a 7.24% CAGR over 2025-2030.

Global Individual Quick Freezing (IQF) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of global food retail chains | +1.2% | Asia-Pacific, Latin America, Global | Medium term (2-4 years) |

| Year-round demand for seasonal products | +1.5% | North America, EU, Asia-Pacific | Long term (≥ 4 years) |

| Shelf-life extension for perishable foods | +1.1% | Global | Short term (≤ 2 years) |

| Growth in plant-based and alt-protein foods | +0.8% | North America, EU, Emerging Asia | Medium term (2-4 years) |

| Clean-label ingredient preference | +0.9% | Developed economies, Global reach | Short term (≤ 2 years) |

| Adoption of modular IQF equipment | +0.7% | Global manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Food Retail Chains by Multinational Companies

The global expansion of multinational food retailers has intensified market demand for IQF processing capabilities, enabling these companies to deliver consistent product quality across diverse international markets. The remarkable growth in frozen food sales in the United States between 2019 and 2023, reaching USD 72.2 billion, demonstrates retailers' strategic focus on maintaining product integrity and extended shelf life throughout their supply chains. Consumer preferences for global cuisine have transformed the frozen food landscape, particularly in categories like frozen appetizers and dumplings, compelling retailers to strengthen their IQF infrastructure investments. In the Asia-Pacific region, Indian IQF processors are implementing advanced freezing technologies for products such as corn kernels, baby corn, and mangoes to meet the requirements of expanding retail networks. This retail market expansion generates ripple effects across the supply chain ecosystem, with each new retail establishment requiring robust IQF supply networks to ensure product consistency and reduce inventory management risks. The emergence of e-commerce in grocery retail has further amplified the importance of IQF technology, as digital food retail platforms require products that maintain optimal quality through extended distribution channels.

Demand for Non-Seasonal Food Products Available Year-Round

Individual Quick Freezing (IQF) technology is revolutionizing agricultural supply chains by enabling consumers to enjoy their favorite seasonal products throughout the year. The sophisticated freezing process safeguards the cellular structure of food products by preventing damaging ice crystal formation, ensuring consumers experience the same texture, taste, and nutritional benefits they expect from fresh products. The May 2024 collaboration between OctoFrost and Mekong Delta Gourmet in Vietnam illustrates this advancement, particularly in processing tropical fruits for international markets during off-season periods. Contemporary IQF systems have achieved substantial improvements in energy efficiency while maintaining optimal product quality, making continuous year-round distribution commercially viable for traditionally seasonal products. The application of IQF technology has expanded beyond conventional fruits and vegetables to encompass premium food categories, including artisanal cheeses and high-end seafood products. Furthermore, as climate change continues to affect traditional growing seasons, IQF processing has become increasingly essential for maintaining reliable and consistent supply chain operations.

Growing Consumer Demand for Perishable Foods with Longer Shelf Life

Consumer preferences continue to evolve, with a growing emphasis on nutritious products that maintain freshness for extended periods, driving substantial advancements in IQF processing technology. Research demonstrates that IQF products can maintain higher nutrient content compared to fresh produce in specific instances, showcasing the effectiveness of this preservation approach. The adoption of innovative partial freezing methods, including superchilling and micro-freezing techniques, extends product longevity compared to traditional chilling processes while preserving product quality. As of July 2025, the strategic partnership between Novella and Metaphor Foods in developing cell-based natural preservatives demonstrates the industry's commitment to extending meat product shelf life while meeting clean-label requirements. The integration of sophisticated packaging solutions, particularly vacuum sealing and modified atmosphere packaging technologies, with IQF processes enhances the overall preservation capabilities of food products.

Increasing Demand for Plant-Based and Alternative Protein Products

IQF technology has emerged as a crucial solution for addressing the intricate processing challenges faced by manufacturers in the plant-based protein industry. The technology's sophisticated approach ensures product texture remains intact while effectively controlling moisture loss throughout the freezing and thawing cycles. Food manufacturers producing plant-based meat alternatives must integrate IQF systems with precise temperature control mechanisms to protect their products against harmful pathogens, particularly Enterococcus faecium and Clostridium botulinum. While traditional heat treatment processes, such as extrusion, have proven effective in eliminating most bacterial contaminants during plant protein processing, the persistent challenge of endospore-forming bacteria like Bacillus cereus requires the implementation of IQF's advanced rapid freezing capabilities to maintain rigorous food safety standards and ensure consumer protection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Maintenance and operational costs of advanced freezing technologies | -1.8% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Strict regulations around food safety and freezer equipment standards | -1.2% | EU & North America core, expanding globally | Long term (≥ 4 years) |

| Limited awareness and adoption in certain markets | -0.9% | Emerging markets in Africa, parts of Asia | Medium term (2-4 years) |

| Waste disposal/refrigerant leakage concerns | -0.7% | Global, stricter enforcement in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Maintenance and Operational Costs of Advanced Freezing Technologies

The capital-intensive nature of advanced Individual Quick Freezing (IQF) systems presents considerable challenges for smaller processors in the market. While mechanical freezers demand substantial initial capital expenditure, they deliver significant operational cost advantages compared to cryogenic alternatives. According to OctoFrost's analysis conducted in July 2025, mechanical IQF freezing demonstrates remarkable cost efficiency in shrimp processing operations, with investment recovery periods remaining under two years despite the higher upfront costs. The intricate process of maintaining optimal airflow speed, temperature control, and defrost cycles necessitates specialized technical expertise, which many facilities currently lack, leading to operational inefficiencies and elevated energy consumption patterns. As the industry progresses toward automated systems to enhance productivity, smaller operators face difficulties in justifying the substantial investments required for training programs and maintenance infrastructure. While energy expenses continue to pose ongoing challenges, technological advancements such as OctoFrost's variable-speed axial vane fans and the elimination of floor heating requirements have yielded substantial reductions in operational costs. The maintenance requirements are particularly challenging for cryogenic systems, where disruptions in liquid nitrogen supply chains and the need for specialized handling procedures create operational vulnerabilities that can result in unexpected production stoppages.

Strict Regulations Around Food Safety and Freezer Equipment Standards

Regulatory frameworks for IQF equipment design and operation continue to evolve, with FSMA 204 requiring comprehensive traceability systems by January 2026. The regulation requires tracking of Key Data Elements and Critical Tracking Events for foods on the Food Traceability List. Companies need 6-14 months to implement these systems, depending on their existing infrastructure. The European Union's Regulation (EC) No 852/2004 establishes hygiene standards, while Regulation (EC) No 853/2004 provides specific rules for food of animal origin, requiring HACCP implementation and continuous temperature monitoring throughout the cold chain. Commission Regulation (EC) No 2073/2005 requires regular microbiological testing and compliance verification, increasing operational complexity and costs for IQF processors [1]Source: European Commission, “Food Hygiene Requirements,” europa.eu. The EPA's industrial process refrigeration compliance requirements establish strict leak repair timelines and technician certification requirements, while continuously evaluating acceptable refrigerant substitutes for environmental impact [2]Source: U.S. Environmental Protection Agency, “Industrial Refrigeration Compliance Guide,” epa.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Mechanical Systems Drive Cost Efficiency

The mechanical IQF technology continues to demonstrate its market leadership by maintaining a substantial 66.44% share in 2024. This dominance stems from its compelling operational advantages, including a notable 10% improvement in energy efficiency compared to alternative technologies and significantly lower operational costs across the equipment's lifespan. The technology's sophisticated cold air circulation mechanism effectively prevents the formation of large ice crystals while operating on conventional mechanical refrigeration cycles. This design enables facilities to maintain extended operational periods without the need for defrosting, which translates into enhanced food safety protocols and reduced cleaning-related expenses.

The cryogenic IQF systems segment is experiencing robust growth, advancing at a 7.37% CAGR. This growth trajectory is primarily attributed to the technology's superior freezing capabilities and exceptional product quality preservation features. These systems have proven particularly effective in processing delicate food items such as shrimp and strawberries, where the rapid crust formation capabilities prevent unwanted moisture loss. In the mechanical systems sector, technological advancement has centered on impingement technology, with notable innovations like OctoFrost's Multi-Level Impingement Freezer achieving remarkable improvements in production efficiency. This system has successfully doubled the production capacity per square meter while addressing traditional challenges associated with spiral freezers, including product deformation and dehydration issues.

By Product: Fruits and Vegetables Lead Market Expansion

Vegetables hold the largest market share at 37.44% in 2024, supported by consistent year-round demand and established processing infrastructure that enables large-scale IQF operations across products like peas, corn, and broccoli. This dominance stems from strong institutional and retail demand for convenient, nutritious options that maintain quality through IQF processing. Indian IQF processors are investing in specialized freezing technology for corn kernels and baby corn, indicating the segment's growth potential. The IQF process preserves the cellular structure and nutritional content of vegetables while preventing clumping, making them suitable for food service and retail applications where portion control and cooking convenience are essential.

Fruits represent the fastest-growing segment with a 6.99% CAGR from 2025-2030, driven by premium pricing for seasonal produce and increasing demand in health-conscious consumer markets. Tropical fruits show significant growth potential, as evidenced by OctoFrost's collaboration with Mekong Delta Gourmet in Vietnam to process mangoes and other tropical varieties for global distribution.

Geography Analysis

North America continues to dominate the market with a substantial 35.22% share in 2024, showcasing its market leadership through well-established cold storage infrastructure and continuous technological improvements. The region's mature market landscape has naturally progressed toward industry consolidation, while still maintaining steady growth. The market demonstrates strong financial health through significant investments, as evidenced by Lineage's successful USD 5 billion IPO completion in July 2024. Additionally, numerous strategic acquisitions valued at hundreds of millions of dollars have strengthened the region's temperature-controlled supply chain capabilities. The market's efficiency focus is exemplified by major food processors like Tyson Foods, which is implementing comprehensive cold storage optimization programs through facility consolidation and automation to achieve substantial annual cost reductions.

Asia-Pacific has emerged as the market's growth engine, achieving an impressive 7.24% CAGR. This remarkable growth trajectory is primarily attributed to the region's expanding middle-class population, accelerating urbanization trends, and increasing consumer preference for convenience foods that necessitate sophisticated cold chain infrastructure. India stands out as a particularly promising market, with food processors actively investing in advanced Individual Quick Freezing (IQF) technology for various products including corn kernels, baby corn, and mangoes, serving both domestic consumption needs and export opportunities. The Indian frozen food market demonstrates exceptional potential for growth, driven by improving living standards among middle-income groups. Similarly, Vietnam's tropical fruit processing sector has become increasingly attractive to international investors, as demonstrated by the strategic partnership between OctoFrost and Mekong Delta Gourmet, which focuses on implementing cost-efficient, high-performance IQF technology for global distribution.

The European IQF market continues to demonstrate robust performance, driven by comprehensive regulatory frameworks and proactive sustainability measures. The region's strategic focus on energy efficiency optimization offers businesses the opportunity to reduce their supply chain costs by 5-12%, while delivering tangible environmental benefits. Through the implementation of rigorous food safety standards, specifically Regulation (EC) No 852/2004 and Regulation (EC) No 853/2004 for animal products, the European Union ensures high compliance standards that encourage technological advancement in the industry. Within the Asian market landscape, China and Japan represent established markets with sophisticated cold chain requirements, yet both nations maintain significant growth potential owing to their substantial market scale and shifting consumer preferences toward premium frozen products. Europe's market dominance is reflected in its 47% share of global frozen vegetable imports, valued at EUR 791 million in 2023, with projected annual growth rates of 1-3% supported by increasing consumer demand for convenience foods and plant-based alternatives [3]Source: Government of the Netherland, “European Market Potential For Frozen Vegetables,” ebi.eu.

Competitive Landscape

The Individual Quick Freezing market demonstrates moderate fragmentation, presenting substantial opportunities for consolidation through strategic acquisitions and partnerships. This trend is exemplified by JBT Corporation's recent acquisition of Marel, resulting in the formation of JBT Marel Corporation. This strategic merger brings together complementary food processing technologies, enabling the new entity to deliver enhanced value propositions to customers while expanding its geographical footprint. The consolidation pattern is not limited to equipment manufacturers but extends to processing companies, as illustrated by Marlen's acquisition of Unitherm Food Systems, which has strengthened their thermal processing capabilities and enhanced their customer support infrastructure.

In response to increasing operational costs and environmental regulations, companies are prioritizing energy efficiency and sustainability innovations in their product development. A notable example is OctoFrost, whose equipment achieves significant energy savings of up to 30% through advanced aerodynamic design and variable-speed fan systems. These improvements eliminate the need for floor heating requirements while optimizing insulation design, demonstrating the industry's commitment to sustainable operations and cost reduction measures.

Emerging markets represent untapped potential for growth, although limited market awareness and adoption rates create entry barriers for smaller industry participants. Companies with established technical expertise and substantial financial resources are well-positioned to capitalize on these opportunities. The industry's evolution toward modular and scalable equipment solutions has enabled manufacturers to effectively serve a diverse range of customer segments, accommodating both small-scale processors and large industrial operations with varying capacity requirements.

Individual Quick Freezing (IQF) Industry Leaders

Marel

Brecon Foods

Greenyard NV

Uren Food Group Limited

Ardo NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Conagra Brands' Birds Eye, a manufacturer of individually quick-frozen (IQF) processed products, is updating its U.S. retail product line. The company intends to remove Food, Drug & Cosmetic (FD&C) colors from its products supplied to K-12 schools before the 2026-2027 academic year.

- September 2024: OctoFrost expanded its presence in India when a major Indian IQF processor purchased an OctoFrost IQF freezer for processing corn kernels, baby corn, and mangoes. This investment indicates the growing adoption of freezing technology in emerging markets.

- May 2024: OctoFrost and Mekong Delta Gourmet formed a partnership to improve IQF processing of tropical fruits in Vietnam. The collaboration aims to enhance operational efficiency and reduce costs in the regional IQF market by implementing new processing technologies.

Global Individual Quick Freezing (IQF) Market Report Scope

| Mechanical IQF |

| Cryogenic IQF |

| Fruits | Berries |

| Tropical Fruits | |

| Citrus Fruits | |

| Stone Fruits | |

| Others | |

| Vegetables | Peas |

| Corn | |

| Broccoli | |

| Others | |

| Seafood | Fish |

| Shrimp | |

| Scallops | |

| Others | |

| Meat | Beef |

| Pork | |

| Lamb | |

| Others | |

| Poultry | |

| Dairy Products |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Technology | Mechanical IQF | |

| Cryogenic IQF | ||

| By Product | Fruits | Berries |

| Tropical Fruits | ||

| Citrus Fruits | ||

| Stone Fruits | ||

| Others | ||

| Vegetables | Peas | |

| Corn | ||

| Broccoli | ||

| Others | ||

| Seafood | Fish | |

| Shrimp | ||

| Scallops | ||

| Others | ||

| Meat | Beef | |

| Pork | ||

| Lamb | ||

| Others | ||

| Poultry | ||

| Dairy Products | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Individual Quick Freezing market by 2030?

The Individual Quick Freezing market size is projected to reach USD 33.69 billion by 2030, up from USD 24.45 billion in 2025.

Which technology segment leads the Individual Quick Freezing market?

Mechanical systems dominate, holding 66.44% share in 2024 due to lower running costs and energy-efficient designs.

Which region is set to grow fastest through 2030?

Asia-Pacific is forecast to register a 7.24% CAGR, the quickest among all regions, as cold-chain infrastructure scales.

What is driving adoption of cryogenic IQF systems?

Demand for ultra-rapid freezing and premium product texture, especially in seafood and plant-based items, is fueling a 7.37% CAGR for cryogenic equipment.

How fragmented is the competitive environment?

The market shows moderate fragmentation; top players collectively control less than half of capacity, creating consolidation potential.

Page last updated on: