India Truck Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 20.18 Billion |

| Market Size (2030) | USD 26.11 Billion |

| Growth Rate (2025 - 2030) | 5.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Truck Market Analysis by Mordor Intelligence

The Indian truck market size stood at USD 20.18 billion in 2025 and is forecast to reach USD 26.11 billion by 2030, reflecting a 5.29% CAGR. Expansion stems from three converging forces: the Bharatmala and PM Gati Shakti programs that widen freight corridors, booming e-commerce that intensifies last-mile volumes, and policy-driven fleet renewal focused on greener powertrains. Light-duty platforms dominate day-to-day urban logistics while heavy-duty assets capitalize on infrastructure build-outs. Diesel retains primacy, yet a rapid surge in electric and gas options signals an unfolding energy shift. Consolidation accelerates as organized fleets out-invest individual owners in telematics, alternative fuels, and driver retention, tightening competition for profitable lanes.

Key Report Takeaways

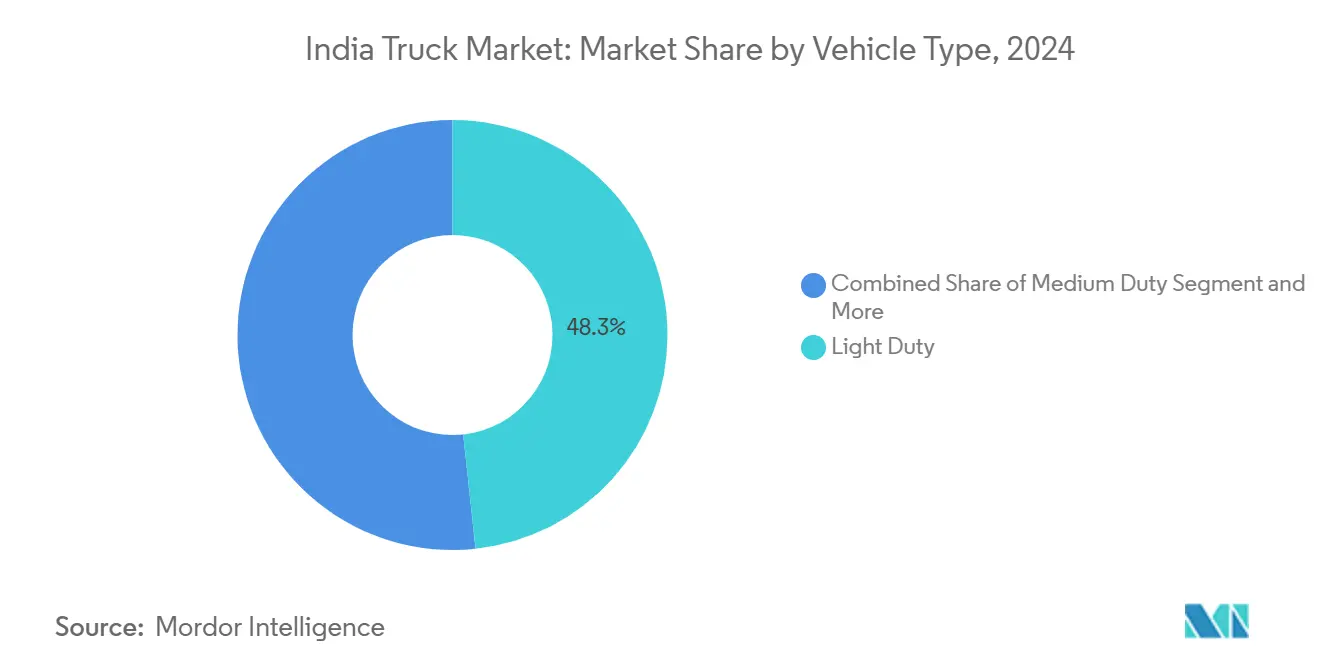

- By vehicle type, light-duty trucks held 48.33% of the India truck market share in 2024 and are advancing at a 6.94% CAGR through 2030.

- By tonnage capacity, the 3.5-7.5 tons bracket captured 39.18% share of the India truck market size in 2024 and is expanding at a 7.14% CAGR to 2030.

- By fuel type, diesel commanded 90.14% of 2024 revenue, while electric trucks are projected to grow at a 41.55% CAGR to 2030.

- By application, logistics accounted for a 55.81% share of the India truck market size in 2024 and is rising at a 7.52% CAGR through 2030.

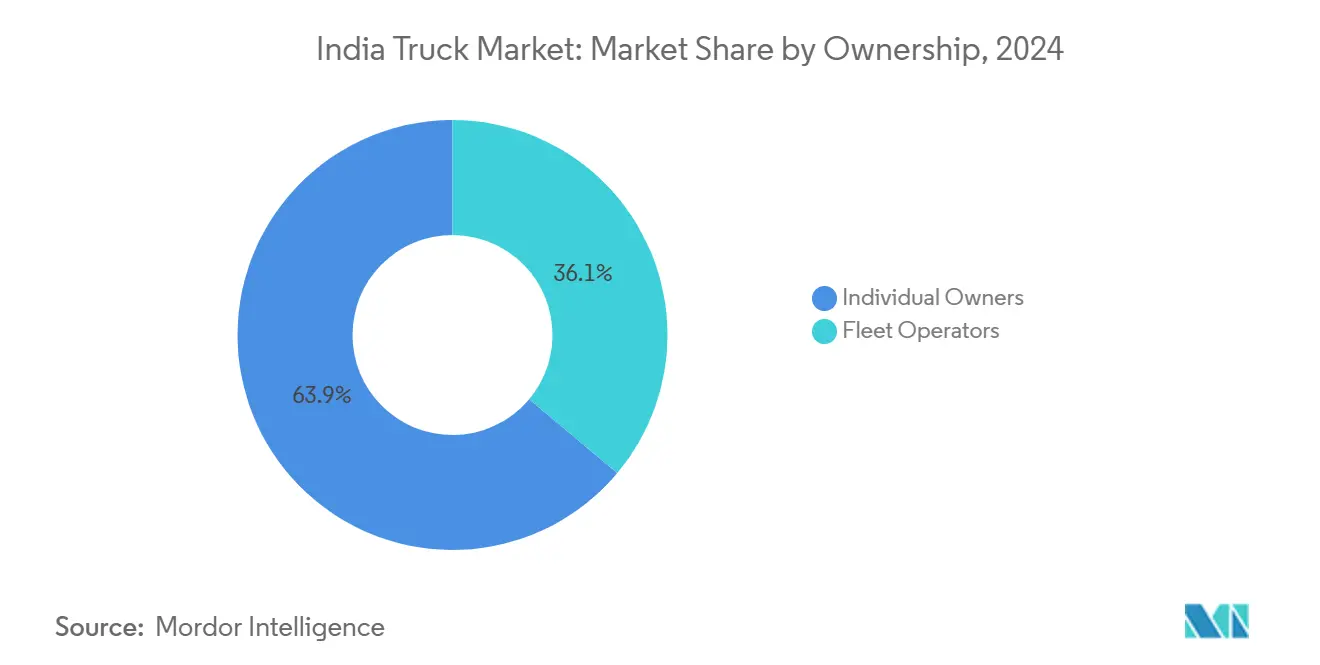

- By ownership, individual operators controlled a 63.94% share of revenue in 2024; fleet companies posted the highest 8.73% CAGR to 2030.

- By body type, flatbed controlled 41.66% share of the India truck market size in 2024, while refrigerated trucks will grow at a 8.03% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on truck market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Infrastructure Push | +1.8% | Priority corridors in North and West India | Medium term (2-4 years) |

| E-commerce Logistics Boom | +1.5% | Urban cores expanding into Tier-2/3 | Short term (≤2 years) |

| Scrappage-Policy Replacement | +1.2% | National hubs | Medium term (2-4 years) |

| CNG/LNG Shift on TCO | +0.9% | Highway and urban fueling nodes | Long term (≥4 years) |

| Cold-Chain Expansion | +0.6% | Tier-2/3 growth markets | Long term (≥4 years) |

| Connected-Truck Telematics | +0.4% | Organized Fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Push (Bharatmala, Gati Shakti)

In FY24, the National Highways Authority of India (NHAI) set a new benchmark by investing a staggering Rs. 2,07,000 crore (USD 24.79 billion) in national highway construction. This capital outlay marked a record high, surging 20% from the previous fiscal year. For the Union Budget 2025-26, the government earmarked Rs. 2,87,333.3 crore (USD 33.07 billion) for the Ministry of Road Transport and Highways, a modest 2.41% increase from FY25's allocations[1]“Road and Infrastructure Industry Analysis,” IBEF, ibef.org. Completing 19,201 km of economic corridors by 2025 already lifts tipper and tractor-trailer utilization. New axle-load norms align with higher-capacity fleets, guiding OEM chassis design. The Indian truck market responds with heavier configurations optimized for bulk cement, steel, and coal haulage. Rising freight density on the Delhi-Mumbai route alone supports continuous-duty cycles that improve truck total cost of ownership.

E-commerce-Led Logistics Boom

India’s logistics sector is experiencing a rapid transformation, driven by a sharp rise in parcel deliveries, fueling continuous demand for trucking services in the India truck market. Leading e-commerce companies are expanding their delivery networks and infrastructure to meet growing consumer expectations for faster service. As logistics operations extend deeper into smaller cities, freight routes are reoriented toward new consumption hubs, increasing the need for agile, light-duty vehicles suited for urban environments. Technological advancements in telematics enhance route efficiency and vehicle productivity, making the trucking ecosystem more responsive and optimized for evolving market dynamics.

Scrappage Policy-Driven Replacement Demand

After 15 years, fitness tests and 25% road-tax rebates for replacement vehicles stimulate structured fleet renewal. OEMs offer 1.5-3% invoice discounts for scrappage certificates, and automated test stations introduced in April 2023 enforce compliance for heavy trucks. Average fleet age at 10 presents a sizable replacement reservoir, especially in high-mileage mining corridors where asset downtime directly erodes contractor margins. The India truck market, therefore, registers a visible pull-forward of purchases ahead of mandatory testing fees and green cess assessments.

Shift to CNG/LNG on TCO Benefits

India's trucking industry is making a decisive move towards cleaner fuel alternatives. Policymakers are pushing long-haul fleets to embrace liquefied natural gas (LNG). To facilitate this shift, public infrastructure is expanding, and early adopters are already reaping significant fuel efficiency benefits over traditional diesel vehicles. Logistics and industrial players are forming strategic partnerships to pilot LNG corridors, underscoring the shift's viability. Concurrently, compressed natural gas (CNG) is gaining momentum, bolstered by an expanding fueling station network. Fleet operators are increasingly drawn to natural gas, not just for its environmental advantages, but also for its reduced price volatility, aligning with their goals of cost stability and sustainability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High BS-VI Truck Capex | -1.4% | National | Short term (≤2 years) |

| Volatile Diesel Prices | -1.1% | Nationwide, long-haul focus | Short term (≤2 years) |

| Driver Shortage and Aging Workforce | -0.8% | Nationwide, MHCV skew | Medium term (2-4 years) |

| Sparse Heavy-Duty Charging | -0.5% | Urban and highway nodes | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High BS-VI Truck Capex

Mandatory BS-VI upgrades and AC cabs add INR 20,000-30,000 (USD 250-375) per unit from October 2025, elevating industry capex to INR 60 billion (USD 750 million) in FY26 [2]“BS-VI capex burden for CV makers,” Business Standard Bureau, business-standard.com. Small operators, still 70% of ownership, struggle with higher EMIs, delaying fleet refresh, and dampening near-term demand within the India truck market.

Volatile Diesel Prices

Diesel remains a dominant cost component in trucking operations, making the industry highly sensitive to global oil price fluctuations, directly squeezing profit margins. Recent disruptions in international trade routes have significantly increased container shipping costs, increasing inland transportation expenses and prompting shippers to explore multimodal logistics solutions. Fuel hedging remains inaccessible mainly for small, independent truck owners, intensifying interest in cleaner and more cost-stable alternatives like gas and electric vehicles. This shift reflects a broader move toward sustainability and financial predictability in India’s evolving freight landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Light-Duty Platforms Anchor Expansion

Light-duty trucks held 48.33% of 2024 shipments, underpinning the India truck market while posting a 6.94% CAGR through 2030. Urban road restrictions and e-commerce time windows favor compact wheelbases that weave through dense streets. OEM financing schemes and low-maintenance EV drivetrains further tilt demand toward this class. Medium-duty units cater to regional express lines, whereas heavy tractors dominate cement, steel, and coal corridors. Light-duty electrification unlocks rapid payback on 200-km urban routes, supported by depot chargers that bypass public-grid constraints.

Second-generation models such as Magenta Mobility’s 3-ton EV now complete three turns daily, doubling asset productivity and reshaping cost curves. Meanwhile, rising ton-mile demand from Tier-3 trade clusters preserves internal-combustion variants, keeping the segment an indispensable growth engine within the India truck market.

By Tonnage Capacity: Sub-7.5 Tons at the Core of Distributed Logistics

Trucks in the 3.5-7.5 ton band captured 39.18% of 2024 volume, reflecting India’s granular retail networks that call for payload agility rather than brute capacity. Their 7.14% CAGR stands above all other tonnage classes as omnichannel retailers push fast replenishment to micro-warehouses. Tight municipal axle mandates and low-bridge clearances reinforce small-tonnage utility.

Continued highway upgrades could gradually swing freight toward 16-ton gross vehicle weights for hub-to-hub lanes, yet doorstep delivery promises keep sub-7.5-ton demand vibrant. Strategically, OEMs overlay modular body kits to stretch platform economics, augmenting the India truck market size through SKU diversity without new homologation cycles.

By Fuel Type: Diesel Rule Faces Multifold Rivalry

Diesel engines retain 90.14% share, but electric trucks record a 41.55% CAGR to 2030, narrowing TCO gaps as battery prices retreat. Roughly 6,158 electric goods carriers sold in 2024 delivered early proof points for depot-based operations. CNG fills an interim niche in short-haul distribution, while LNG books advance orders for long-corridor cement runs.

Policy-driven zero-tailpipe mandates for city freight after 2030 will gradually restrict diesel entry during peak hours, pressing fleets to diversify. Multienergy ecosystems thus emerge, making fuel choice a strategic lever for competitiveness inside the India truck market.

By Application: Logistics Dominates a Digitizing Economy

Logistics services captured 55.81% revenue in 2024 and clocked a 7.52% CAGR as parcel flows triple this decade. Express operators invest in drop-and-hook models that slash terminal dwell time. Construction trucks absorb Bharatmala-driven aggregate moves, yet regulatory axle recalibration trims overloading practices, reshaping payload economics.

Cold-chain moves stand out, with vaccine exports and dairy deficits spurring reefer adoption. Overall, application diversity shields the India truck market from cyclical shocks, distributing risk across consumer, industrial, and infrastructure verticals.

By Ownership: Fleet Scale Edges Out Atomized Players

Individual owners still manage 63.94% of trucks, but organized fleets outpace them at an 8.73% CAGR thanks to bank leverage, digital dispatch, and preventive maintenance plans. National contracts from Fast-Moving Consumer Goods leaders now specify telemetry uptime, pushing lone operators to subcontract or exit.

As fleets cross the 1,000-truck threshold, OEMs extend value-added services such as guaranteed residual buy-back that lower lifecycle cost. This professionalization cycle lifts operating standards and accelerates technology diffusion across the India truck market.

By Body Type: Flatbeds Remain the Workhorse while Reefers Sprint

Flatbeds hold a 41.66% share, moving steel, timber, and containers with unmatched versatility. Standardization on 20-ft and 40-ft container twist-locks enables intermodal transfers. In contrast, refrigerated bodies grow 8.03% annually, propelled by pharmaceuticals and processed foods requiring 2 °C-8 °C transit.

Rapid dairy throughput from cooperative hubs in Maharashtra and Gujarat triggers daytime reefer demand spikes, encouraging back-haul matchmaking apps to curb empty runs. Body-builder clusters in Jamshedpur and Pune now integrate composite panels and solar-powered gensets, broadening options for buyers in the India truck market.

Geography Analysis

India’s truck market shows clear regional contrasts shaped by logistics performance scores and infrastructure roll-outs. The LEADS 2024 index ranks Gujarat, Karnataka, Maharashtra, Odisha, and Tamil Nadu as “coastal achievers,” while Haryana, Telangana, Uttar Pradesh, and Uttarakhand top the landlocked category, highlighting where regulatory efficiency and multimodal hubs most strongly support fleet productivity. Robust industrial bases, port connectivity, and streamlined permit systems in these states raise vehicle utilization and shrink turnaround times, anchoring the nation’s densest freight corridors.

Northern and western territories—especially the Delhi-Mumbai Industrial Corridor, National Capital Region clusters, and Gujarat’s ports—absorb the heaviest ton-mile volumes via the Golden Quadrilateral highway grid. Continuous road widening along these routes sustains high-duty cycles for multi-axle tractors, while construction material haulage linked to Bharatmala projects keeps tipper demand elevated. Southern India records the fastest expansion, with the Chennai-Bangalore tech and auto belt fostering 3PL investment, telematics penetration, and early electric-truck pilots. Karnataka’s achiever status illustrates how digitized checkpoints and warehouse automation shorten dwell times and tilt freight toward organized fleets.

Eastern states contribute mining-led bulk flows yet struggle with axle-damaging road quality that slows adoption of advanced powertrains. Government outlays for the North-East Strategic Road Investment Program aim to unlock cross-border opportunities, but volumes remain modest compared with western and southern corridors. Divergent state taxes, entry permits, and toll technologies further shape route economics, prompting fleets to deploy software-driven planning that arbitrages cost gaps across the India truck market.

Mordor Intelligence provides coverage of the truck market across other key regional markets. Detailed country-level analysis extends to Egypt incorporating local coverage and market participation, as required.

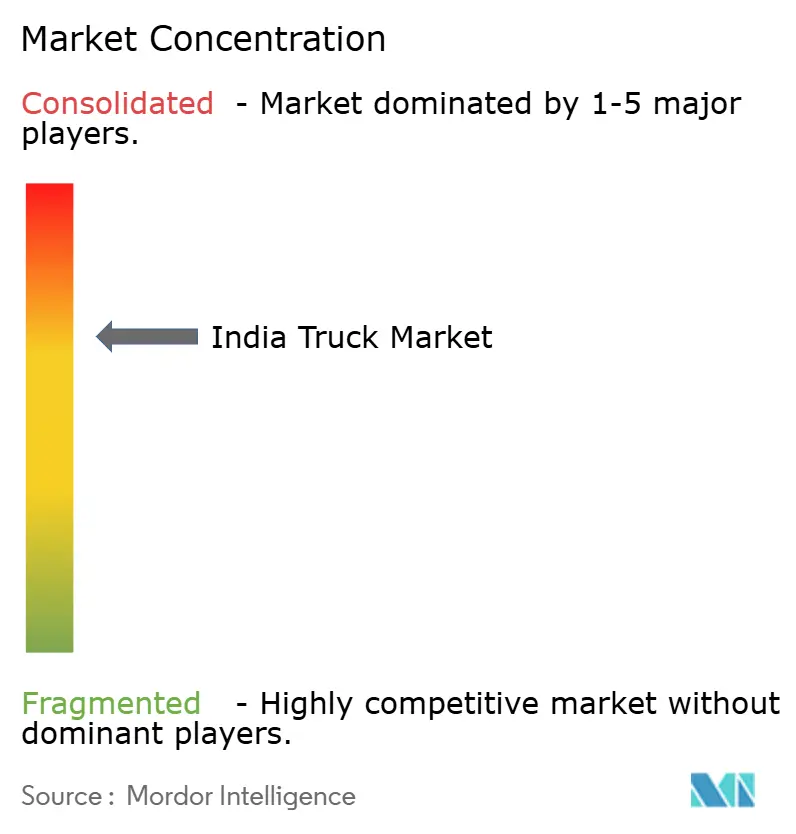

Competitive Landscape

India's truck market exhibits moderate concentration with established domestic leaders maintaining dominant positions while facing intensifying competition from alternative fuel technologies and new business models. Market leadership remains concentrated among Tata Motors, Mahindra & Mahindra, and Ashok Leyland, collectively controlling a significant share of the commercial vehicle retail market. This oligopolistic structure provides pricing stability while enabling substantial R&D investments in alternative powertrains and advanced technologies.

Strategic consolidation accelerates through targeted acquisitions, exemplified by Mahindra & Mahindra's INR 555 crore (USD 69.4 million) purchase of a 58.96% stake in SML Isuzu, designed to expand presence from 3% to 20%+ in the above-3.5-ton segment by FY36. The transaction underscores incumbents’ focus on scale efficiencies, diversified tonnage portfolios, and faster compliance with evolving emission and safety norms that shape customer procurement criteria.

Technology adoption emerges as the primary differentiator. Ashok Leyland’s alliance with Minus Zero explores autonomous Level-4 pilots, while EKA Mobility partners with KPIT on 300 kW electric axles [3]“Minus Zero autonomous collaboration,” Ashok Leyland Press Release, ashokleyland.com. Challengers such as Blue Energy Motors (LNG tractors) and Tresa Motors (battery-electric heavy rigs) target corporate sustainability budgets, forcing incumbents to accelerate telematics, financing packages, and end-to-end service contracts. White-space opportunities in integrated logistics platforms and energy-infrastructure partnerships continue to recalibrate rivalry across the India truck market.

India Truck Industry Leaders

Tata Motors Limited

Ashok Leyland

Mahindra & Mahindra Limited

VE Commercial Vehicles Ltd. (Eicher)

BharatBenz (Daimler India Commercial Vehicles)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Tata Motors, the leading commercial vehicle manufacturer in India, has unveiled the Tata LPT 812, its newest addition to the Intermediate, Light, and Medium Commercial Vehicles (ILMCV) segment. The LPT 812, featuring factory-fitted air-conditioning, proudly claims the title of India's first 4-tyre truck boasting a 5-tonne rated payload. This innovation not only ensures an unparalleled payload capacity but also facilitates seamless operations in urban settings.

- July 2025: Eicher Trucks and Buses introduced its next-generation Pro Plus Series in Pithampur, Madhya Pradesh. This new lineup features six light and medium-duty truck models tailored for diverse commercial uses, from intra-city deliveries to long-haul transport. Enhancing the existing Pro Series platform, the Pro Plus Series boasts factory-installed air conditioning, a heightened payload capacity, and advanced digital connectivity. Each truck is integrated with the MyEicher app and the Eicher Live system, facilitating real-time vehicle diagnostics and efficient fleet management.

- February 2025: Blue Energy Motors Ltd. signed an MoU with the Maharashtra government to invest Rs 3,500 crore in manufacturing 30,000 electric trucks by 2025-26. The initiative will boost Maharashtra's EV manufacturing infrastructure and create over 4,000 jobs. The facility will include R&D, battery-pack production, motor manufacturing, and charging stations.

- April 2024: Tresa Motors booked a 1,000-unit electric truck preorder from JFK Transporters.

India Truck Market Report Scope

| Light Duty |

| Medium Duty |

| Heavy Duty |

| 3.5-7.5 Tons |

| 7.5-16 Tons |

| 16-30 Tons |

| Above 30 Tons |

| Diesel |

| Petrol |

| Electric |

| Other Fuel Type |

| Logistics |

| Construction |

| Agriculture |

| Mining |

| Utility |

| Others |

| Fleet Operators |

| Individual Owners |

| Flatbed |

| Box Truck |

| Refrigerated |

| Tanker |

| Tipper |

| By Vehicle Type | Light Duty |

| Medium Duty | |

| Heavy Duty | |

| By Tonnage Capacity | 3.5-7.5 Tons |

| 7.5-16 Tons | |

| 16-30 Tons | |

| Above 30 Tons | |

| By Fuel Type | Diesel |

| Petrol | |

| Electric | |

| Other Fuel Type | |

| By Application | Logistics |

| Construction | |

| Agriculture | |

| Mining | |

| Utility | |

| Others | |

| By Ownership | Fleet Operators |

| Individual Owners | |

| By Body Type | Flatbed |

| Box Truck | |

| Refrigerated | |

| Tanker | |

| Tipper |

Key Questions Answered in the Report

How large is the India truck market in 2025?

The India truck market size was USD 20.18 billion in 2025 and is forecast to reach USD 26.11 billion by 2030 at a 5.29% CAGR.

Which segment holds the highest India truck market share?

Light-duty vehicles commanded 48.33% share in 2024, making them the leading segment by sales volume.

What fuel type is growing fastest?

Electric trucks are expanding at a 41.55% CAGR to 2030, the quickest rate among all fuel categories.

Why is fleet ownership rising?

Fleet operators access cheaper financing, deploy telematics, and negotiate bulk buys, driving an 8.73% CAGR versus slower individual growth.

Page last updated on: