Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

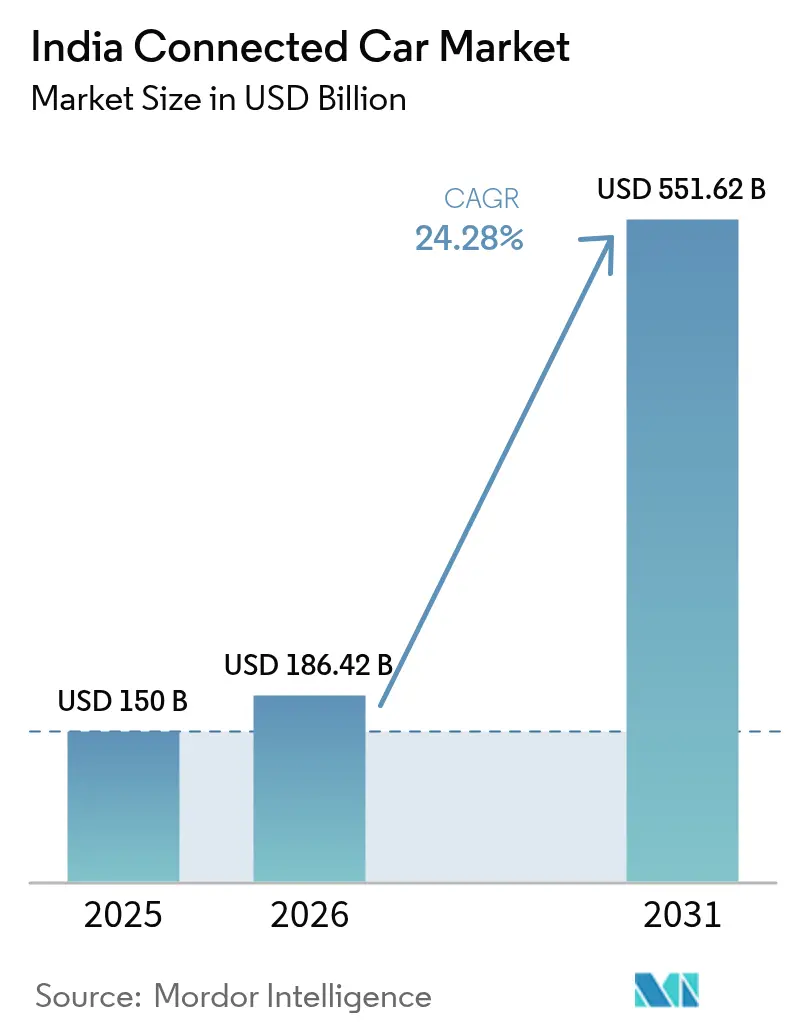

| Base Year Market Size (2025) | USD 150 Billion |

| Market Size (2026) | USD 186.42 Billion |

| Market Size (2031) | USD 551.62 Billion |

| Growth Rate (2026 - 2031) | 24.28% CAGR |

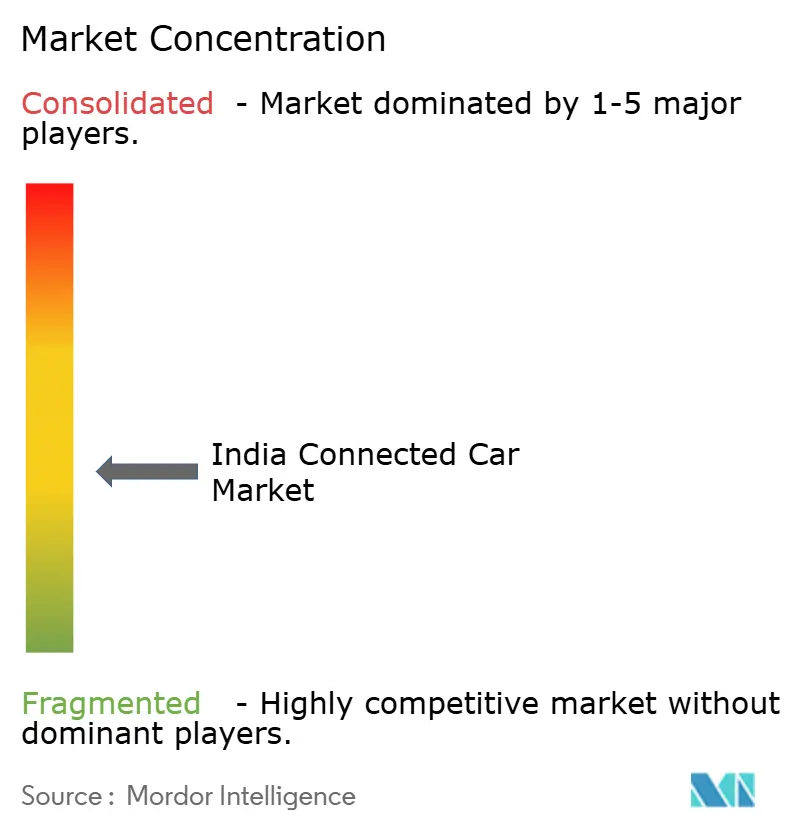

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Connected Car Market Analysis by Mordor Intelligence

The India connected car market size is expected to grow from USD 150 million in 2025 to USD 186.42 million in 2026 and is forecast to reach USD 551.62 million by 2031 at 24.28% CAGR over 2026-2031. Growth springs from mandatory telematics rules, rapid 5G coverage, and consumer appetite for smartphone-like vehicle experiences, positioning the India connected car market as a hotbed for global and domestic suppliers. Regulatory pushes such as AIS-140, NavIC positioning, and Bharat NCAP 2.0 embed connectivity into even entry vehicles, while the India connected car market benefits from the world’s third-largest automotive production base that lets OEMs amortize electronics costs quickly. Telco-OEM revenue sharing lowers subscription hurdles and lets the India connected car market deliver affordable data plans that match rising disposable income. Embedded cyber-security stacks are moving up the buying checklist as data breaches dent trust, yet vendors that prove secure OTA pipelines capture an advantage.

Key Report Takeaways

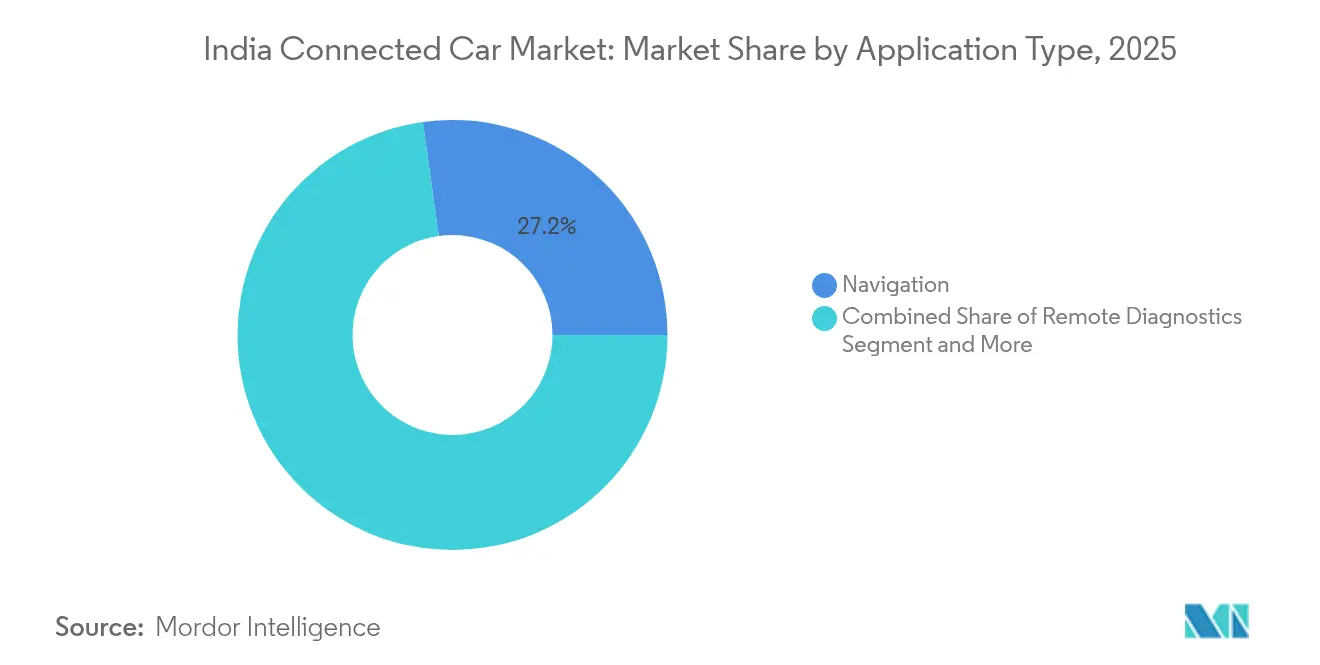

- By application, navigation held 27.20% of the India connected car market share in 2025 while over-the-air updates are projected to soar at a 26.15% CAGR through 2031.

- By connectivity type, embedded solutions accounted for 46.55% of the India connected car market size in 2025; integrated systems are forecast to expand at 25.1% CAGR between 2026 and 2031.

- By communication model, vehicle-to-infrastructure captured 52.45% revenue share in 2025, while vehicle-to-cloud communication leads CAGR growth at 26.05% until 2031.

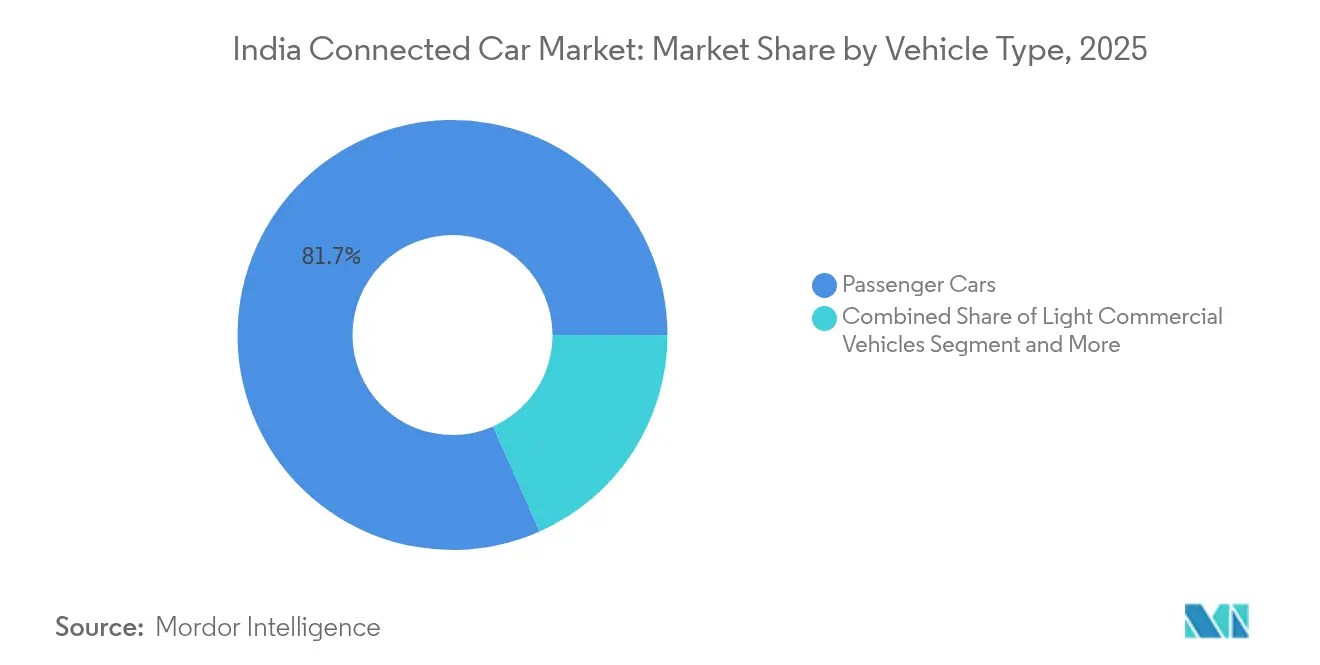

- By vehicle type, passenger cars commanded 81.65% of the India connected car market size in 2025, yet light commercial vehicles will log the fastest 24.95% CAGR to 2031.

- By sales channel, OEM factory fitment dominated with 86.65% share in 2025, although after-market retrofits are advancing at 25.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Connected Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Smartphone and 4G/5G | +6.2% | National metros and tier-1 cities | Short term (≤ 2 years) |

| Government AIS-140 and AV-NEXT | +5.8% | Nationwide, commercial and emerging passenger | Medium term (2-4 years) |

| OEM-Telco Revenue-Share Models | +4.1% | High-ARPU urban clusters | Medium term (2-4 years) |

| Rising Disposable Income and Spend | +3.7% | Tier-1 and tier-2 cities | Long term (≥ 4 years) |

| On-board NavIC Compliance | +3.2% | National corridors | Short term (≤ 2 years) |

| Pay-Per-Use Insurance Pilots | +2.8% | Dense urban traffic zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Smartphone and 4G/5G Penetration

India’s 5G user base touched 365 million as of July 2025, creating a ready canvas for vehicle-smartphone fusion that steers the India connected car market toward mass adoption [1]“BSNL 4G Expansion Note,” Department of Telecommunications, dot.gov.in. Majority of shoppers now cite connected features as pivotal when selecting a new vehicle, and OEMs respond by equipping even compact SUVs with integrated eSIMs and mobile apps. Kia’s 2024 launch of the Syros model bundled an Airtel eSIM, letting owners access live traffic, geo-fencing, and theft alerts. The India connected car market also benefits because cloud transactions ride on existing telco billing rails, keeping subscription costs near mobile-data parity. As consumer expectations migrate from phones to dashboards, infotainment and safety applications move from nice-to-have to deal-breakers, accelerating standard-fit connectivity across model lines.

Government’s AIS-140 and AV-NEXT Mandates

AIS-140 demands tracking and emergency buttons on commercial vehicles, while the AV-NEXT draft roadmap insists on NavIC integration in passenger cars, making compliance the main door-opener to the India connected car market. Bharat NCAP 2.0 scoring further elevates connected safety by awarding additional stars for telematics-enabled e-call and crash notification. The predictable demand curve allows Tier-1 suppliers to scale ECUs locally, which trims unit costs and increases domestic value addition. Over time, mandatory compliance morphs into a competitive differentiator as brands that exceed the bare minimum tout higher safety scores.

OEM–Telco Revenue-Share Models

Kia and Airtel, Honda and Jio, and Maruti Suzuki with MapMyIndia illustrate revenue-share models that distribute data costs over an entire vehicle lifecycle, reducing sticker shock. Telcos gain incremental ARPU, while OEMs turn connected features into subscription bundles ranging from entry-level roadside assist to premium concierge. Such models help the India connected car market escape the low-margin hardware trap by monetizing services like predictive maintenance and location-based coupons. Because billing, SIM management, and cyber-security already reside inside telco networks, automotive partners can plug into mature platforms instead of building from scratch.

Rising Disposable Income and Aspirational Spend

Urban households climbed significantly in 2024, and many allocate savings to in-car tech that mirrors smartphone convenience. Compact SUVs such as Hyundai’s Creta EV bundle connected features as standard, making them aspirational rather than luxury. Younger buyers gravitate to cars they can control through voice assistants, and this preference radiates into tier-2 cities as incomes rise. For fleet owners, telematics reduces fuel and maintenance, offsetting upfront costs. Consequently, the India connected car market sees higher penetration in high-growth body styles like crossovers where tech acts as a lifestyle badge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Breach and Cyber-Attack Concerns | −3.2% | Urban markets | Short term (≤ 2 years) |

| Patchy LTE Coverage on Rural Corridors | −2.8% | Northern and eastern hinterlands | Medium term (2-4 years) |

| Low ARPU on Connected-Service Subscriptions | −2.1% | Tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Legacy Fleet Unable to Retrofit | −1.9% | Logistic hubs with older trucks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-breach and Cyber-attack Concerns

Ransomware attacks on global infotainment systems raised red flags among Indian buyers who now hesitate to share driving data. While startups like SecureThings offer anomaly-detection software, uptake stays uneven because no India-specific regulation mirrors the EU WP.29 cyber-security clause. Without mandatory standards, small OEMs treat cyber spend as optional, opening gaps that erode trust. High-profile hacks would slow the India connected car market if consumers begin disabling SIM modules or refuse consent for data collection.

Patchy LTE Coverage on Rural Corridors

National highways linking mineral belts in Jharkhand or tourist routes in the Northeast suffer blind spots, forcing connected trucks to fall back on SMS beaconing. The BSNL 4G expansion, slated to finish in 2026, will plug holes, yet interim downtime dilutes fleet analytics benefits [2]“India Crosses 365 Million 5G Users,” The Economic Times, economictimes.indiatimes.com. OEMs must add dual-profile modems and store-and-forward logic, which raises BOM cost and tempers growth in value-conscious segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Type: Navigation Leads While OTA Updates Accelerate

Navigation accounted for 27.20% of the India connected car market share in 2025 as clogged city grids and mixed-quality road signs made live rerouting vital. Local mapping partners like MapMyIndia curate pothole alerts and fuel-station data that resonate with daily commuters. In contrast, over-the-air updates log a 26.15% CAGR to 2031 as OEMs realize a single remote fix avoids thousands of service-bay visits. The India connected car market size for OTA upgrades is projected to rise significantly by 2031, a gain that highlights software’s growing share of vehicle value. Remote diagnostics and multimedia streaming follow, fueled by telco bundling of in-car data plans with family mobiles. Emergency e-call adoption ticks upward under Bharat NCAP 2.0, reinforcing safety as a selling theme.

The second wave of application adoption centers on personalization. Cabin climate presets sync through cloud profiles while voice assistants learn local dialects. Such evolutions will further cement the India connected car market as a software arena in which continuous delivery outranks model-year refresh cycles.

By Connectivity Type: Embedded Solutions Dominate Despite Cost Pressures

Embedded eSIM modules shipped in 46.55% of new connected vehicles during 2025 because OEMs want lifecycle control over diagnostics, firmware, and data routing. Integrated connectivity, which piggybacks on smartphone data, grows quickest at 25.1% CAGR as supply-chain costs lift and consumers push back against rising MSRPs. The hybrid approach often lands in mid-trim variants where buyers bring their own data but the car retains a low-bandwidth fallback eSIM for critical safety traffic.

Tethered systems remain niche in penetration, used mainly by aftermarket dongles. Yet the low hardware bill keeps them alive for fleet retrofits. Over the forecast horizon, the India connected car industry will likely settle on a dual-core strategy: embedded for high-value or regulatory-heavy use cases, integrated for budget lines.

By Communication Model: V2I Infrastructure Drives Current Adoption

Vehicle-to-Infrastructure held 52.45% share in 2025, helped by municipal investments in adaptive traffic lights and toll-plaza digitization. For example, Bengaluru’s command center shares signal phase data with company fleets to minimize idle time. V2I’s share is predicted to slip modestly as Vehicle-to-Cloud usage will climb to 26.05% CAGR by 2031 on the back of cheaper storage and analytics. The India connected car market size tied to V2C services is expected to grow, thus reflecting analytics and content streaming demand.

V2V and V2P remain limited to pilot corridors such as the Delhi-Jaipur expressway. Adoption awaits spectrum allocation clarity around the 5.9 GHz band and roadside unit funding. Nevertheless, once critical mass builds, peer-to-peer alerts for blind-spot hazard and pedestrian proximity could unlock another growth inflection.

By Vehicle Type: Passenger Cars Lead While Commercial Segments Accelerate

Passenger cars contributed 81.65% revenue in 2025, fueled by high sales volumes and intense feature wars among brands. Compact SUVs dominate because tech-savvy buyers equate connected dashboards with non-negotiable value. Light commercial vehicles post the fastest 24.95% CAGR as last-mile operators chase dispatch efficiency. Heavy trucks adopt connectivity for fuel coaching, but the addressable fleet renews slower, tempering volume.

As EV sales rise, both passenger and LCV segments lean more on connectivity to manage battery health and charging route planning. Fleet owners, meanwhile, plan to exploit ADAS-driven insurance rebates, pushing adoption deeper into agrarian and mining haul routes where downtime wreaks high opportunity costs.

By Sales Channel: OEM Integration Dominates Despite After-Market Growth

OEM factory fitment commanded 86.65% of 2025 shipments since warranty assurance and AIS-140 compliance encourage buyers to pick built-in kits. This route captures almost the entire subsidy from production-linked incentive schemes that reward local module sourcing. After-market sales, however, clock a brisk 25.9% CAGR as millions of pre-2020 cars seek retrofit security and navigation. Chipset maker Quectel and integrators like Embitel target this long-tail via plug-and-play boxes. For insurers, retrofits create new data streams without waiting a decade for the fleet to turn over.

The dual-channel ecosystem means the India connected car market balances premium factory systems with affordable add-ons, expanding the total reachable customer base.

Geography Analysis

Metropolitan clusters such as Delhi NCR, Mumbai, Pune, Bengaluru, and Hyderabad account for a notable share of current connected car activations. These zones enjoy near-continuous 5G coverage, dense dealer networks, and consumers comfortable with app payments. Pune, home to multiple OEM R&D centers, doubles as a sandbox for early OTA rollouts. In West India, high per-capita income intersects with bumper-to-bumper traffic, which heightens the perceived utility of navigation and e-call.

Tier-2 cities like Indore, Coimbatore, and Lucknow form the next vanguard. As fiber backhaul extends and average incomes climb, OEMs launch mid-spec connected trims tailored to these buyers. Yet patchy LTE on peri-urban ring roads forces fallback modes and raises support costs. Government Digital India projects earmark rural BTS upgrades, but completion staggered to 2026 leaves a short-term reliability gap.

Long-haul freight corridors from Mumbai to Chennai or Delhi to Kolkata expose another dimension. Fleet managers demand minute-by-minute tracking to comply with e-way bill norms, though coverage black holes on the Odisha plateau or Jharkhand forests dilute value. Pilot satellite-cellular hybrid modems aim to plug these gaps. The India connected car industry thus adapts products to a mosaic of connectivity profiles, from ultradense metro grids to sporadic rural nodes.

Competitive Landscape

The India connected car market hosts a blend of mass OEMs, challenger brands, telcos, Tier-1 electronics suppliers, and over-the-air platform specialists. Maruti Suzuki, Hyundai, and Tata Motors leverage installed bases and dealer reach to preload telematics on fresh models. MG Motor pushes the envelope with AI-voice assistants in every variant, compelling incumbents to match. Telcos Airtel and Jio bring network, billing, and cyber-security expertise; they monetise data plans while embedding SIM life-cycle tools.

Technology startups add agility. Fleetx raised USD 34.2 million to expand AI dispatch analytics that rival OEM dash data. MapMyIndia’s NavIC-first maps became default on several 2025 launches. Cyber-security niche players like SecureThings or Cybellum pitch intrusion detection systems that meet emerging WP.29-style expectations.

M&A heats up as OEMs seek digital depth. Tata Motors revealed plans to acquire a significant stake of Freight Tiger to fold logistic SaaS into its commercial lineup [3]“Acquires Stake in Freight Tiger,” Tata Motors, tatamotors.com. Hyundai partnered with Savari to co-develop V2X stacks entrenched in Indian spectrum rules. Competitive edge now hinges less on metal stamping and more on cloud uptimes, vulnerability response time, and developer ecosystems, underscoring the software-defined car thesis within the India connected car market.

India Connected Car Industry Leaders

Maruti Suzuki India Ltd

Hyundai Motor India Ltd

Tata Motors Ltd

Mahindra & Mahindra Ltd

Kia India Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Kia India teamed up with Airtel Business on the Kia Connect 2.0 platform covering vehicle management, AI voice, remote control, and safety functions over Airtel’s secure nationwide network.

- April 2024: HARMAN stated that Tata Motors selected the HARMAN Ignite Store as its official in-vehicle app marketplace, bringing Android Automotive compliant digital services to Indian consumers.

India Connected Car Market Report Scope

A connected car is a vehicle that is equipped with internet access and wireless connectivity, allowing it to share data with other devices, systems, and networks. This connectivity enables a range of features and services, such as real-time traffic updates, remote vehicle diagnostics, and infotainment streaming.

The Indian connected car market is segmented by application, connectivity form, vehicle connectivity, and vehicle type. By application, the market is segmented into driver assistance, telematics, infotainment, and other applications. By connectivity form, the market is segmented into integrated, embedded, and tethered. By vehicle connectivity, the market is segmented into vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I), and vehicle-t-pedestrian (V2P). By vehicle type, the market is segmented into passenger cars and commercial vehicles. The report offers market size and forecasts for all the above segments in terms of value (USD).

By Application Type

| Navigation |

| Remote Diagnostics |

| Multimedia Streaming |

| Social Media and Other Apps |

| OTA Update |

| On-Road Assistance |

| E-call and SOS Assitance |

| Remote Operation |

| Auto Parking/Connected Parking |

| Autopilot |

| Home Integration |

| Stolen Vehicle Recovery/Warning |

By Connectivity Type

| Embedded |

| Integrated |

| Tethered |

By Communication Model

| Vehicle-to-Vehicle (V2V) |

| Vehicle-to-Infrastructure (V2I) |

| Vehicle-to-Pedestrian (V2P) |

| Vehicle-to-Cloud (V2C) |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

By Sales Channel

| OEM-Factory-Fit |

| After-Market Retrofit |

| By Application Type | Navigation |

| Remote Diagnostics | |

| Multimedia Streaming | |

| Social Media and Other Apps | |

| OTA Update | |

| On-Road Assistance | |

| E-call and SOS Assitance | |

| Remote Operation | |

| Auto Parking/Connected Parking | |

| Autopilot | |

| Home Integration | |

| Stolen Vehicle Recovery/Warning | |

| By Connectivity Type | Embedded |

| Integrated | |

| Tethered | |

| By Communication Model | Vehicle-to-Vehicle (V2V) |

| Vehicle-to-Infrastructure (V2I) | |

| Vehicle-to-Pedestrian (V2P) | |

| Vehicle-to-Cloud (V2C) | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| By Sales Channel | OEM-Factory-Fit |

| After-Market Retrofit |

Key Questions Answered in the Report

How big is the India connected car market in 2026?

The India connected car market size is valued at USD 186.42 million in 2026.

What is the projected CAGR for connected vehicles in India to 2031?

The market is forecast to expand at a 24.28% CAGR from 2026 to 2031.

Which application holds the largest share today?

Navigation leads with 27.20% share thanks to real-time traffic and local mapping integration.

Why are over-the-air updates growing fastest?

OTA cuts service-center visits and lets OEMs push features remotely, driving a 26.15% CAGR to 2031.

Page last updated on: