India Small Commercial Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

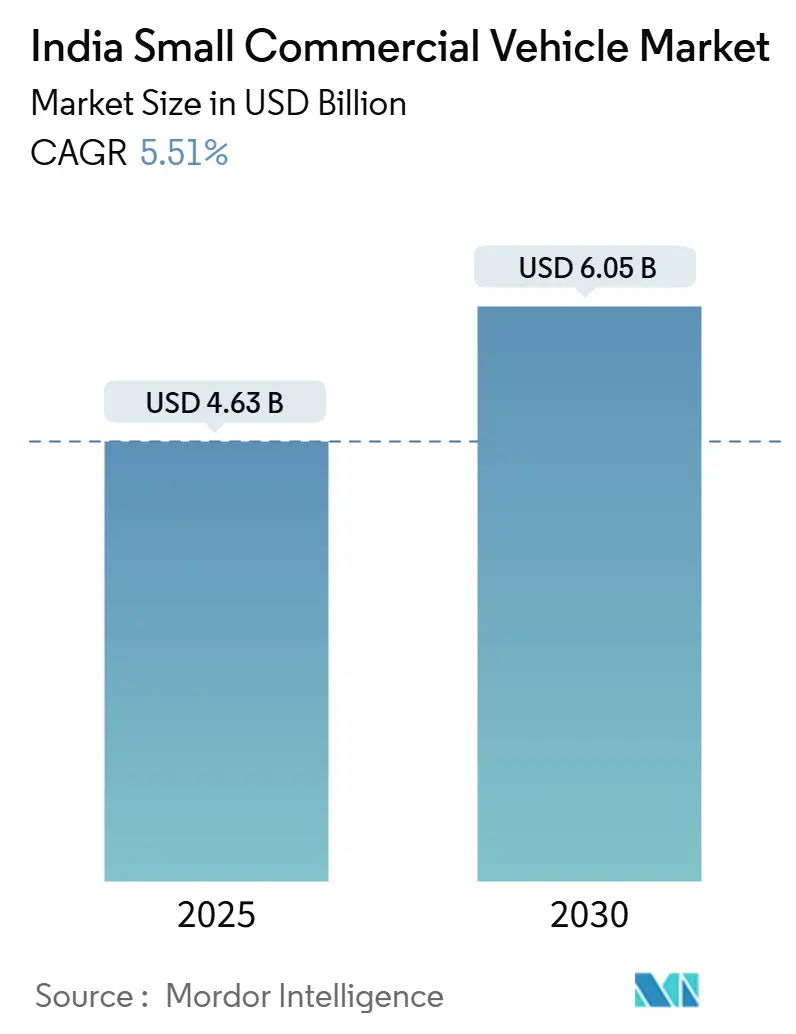

| Market Size (2025) | USD 4.63 Billion |

| Market Size (2030) | USD 6.05 Billion |

| Growth Rate (2025 - 2030) | 5.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Small Commercial Vehicle Market Analysis by Mordor Intelligence

The India Small Commercial Vehicle Market size is estimated at USD 4.63 billion in 2025, and is expected to reach USD 6.05 billion by 2030, at a CAGR of 5.51% during the forecast period (2025-2030). Sustained urbanization, a pivot toward hub-and-spoke logistics, and policy-backed electrification continue to lift volume demand even as operators focus on asset utilization and route optimization. Mini trucks dominate fleet purchases because they balance maneuverability with 1-2 tonne payload capability, while pickup trucks and electric three-wheelers address emerging niches such as cold-chain distribution and hyperlocal delivery. Government programs—most notably the PM E-DRIVE incentive running through March 2026—lower the upfront cost barrier for battery electric variants and reinforce the long-term transition away from diesel fleets. Digital freight platforms further amplify growth by cutting empty-run ratios and opening financing channels for first-time buyers. Collectively, these forces position the India small commercial vehicle market for resilient mid-single-digit expansion through the forecast window.

Key Report Takeaways

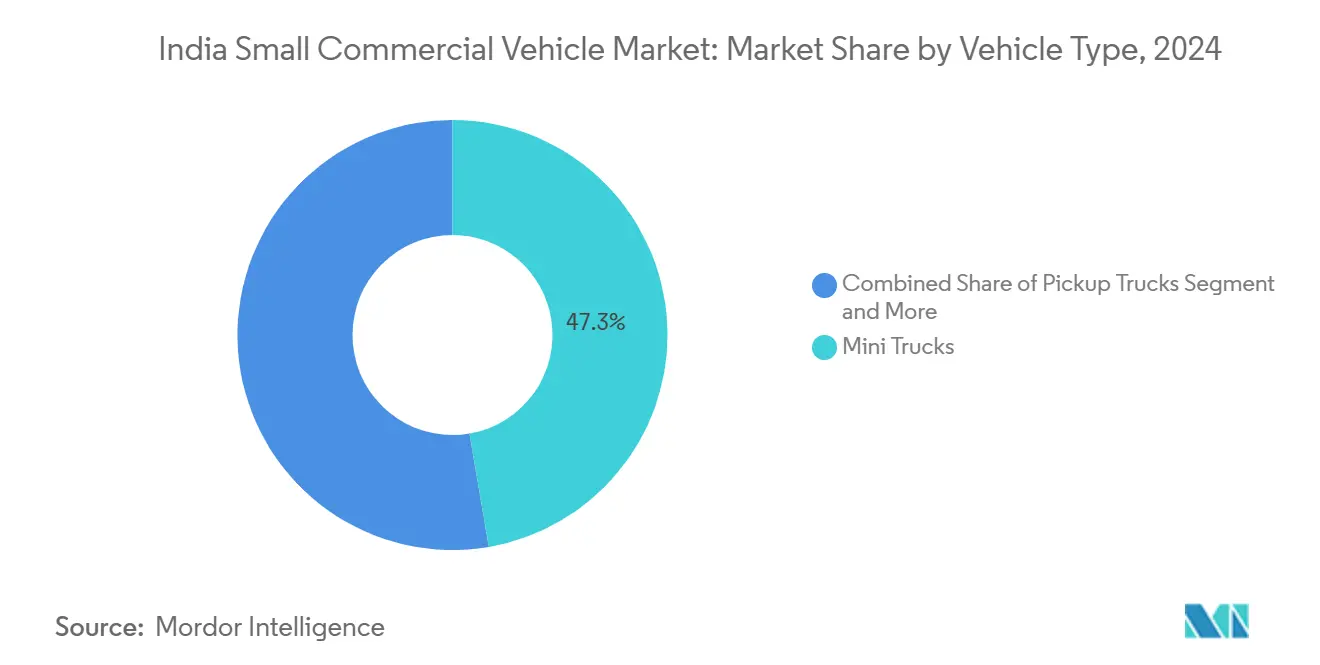

- By vehicle type, mini trucks led with 47.31% revenue share in 2024; the 2-3.5 tonne pickup sub-segment registered 31% year-over-year growth in FY2023 and is expected to sustain a 5.55% CAGR through 2030.

- By payload capacity, the sub-1-tonne category accounted for 54.37% share of the India small commercial vehicle market size in 2024 and is projected to advance at 5.61% CAGR to 2030.

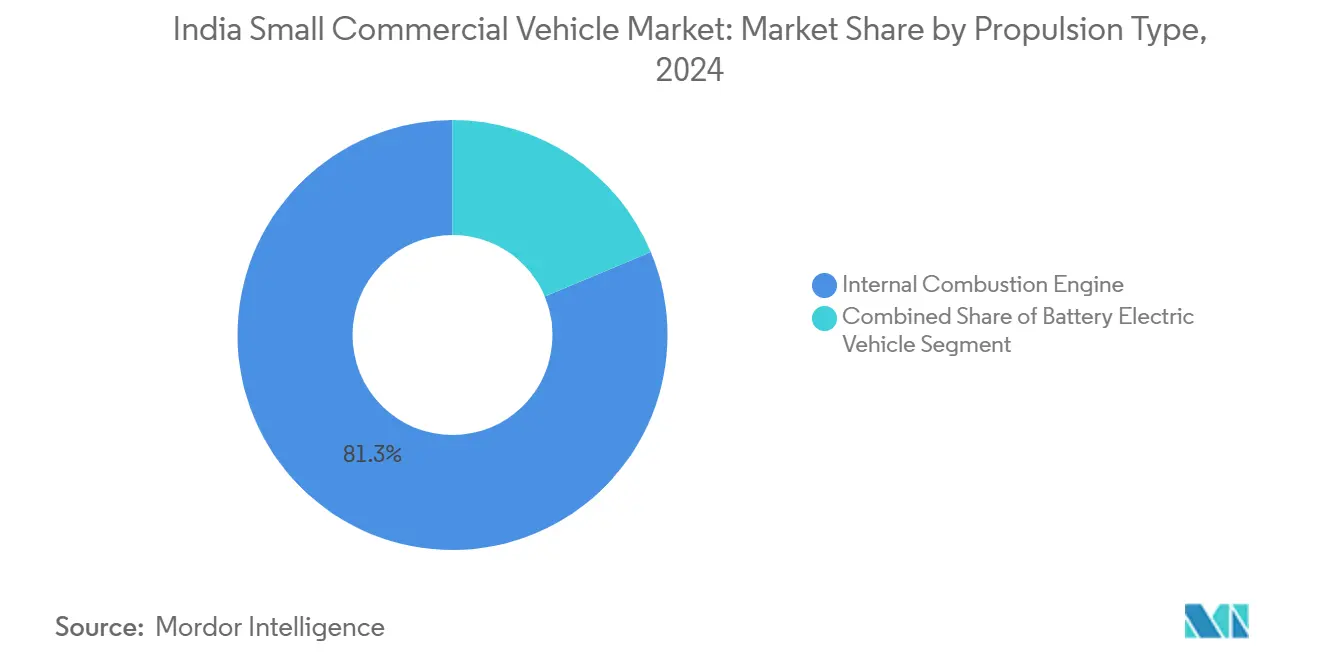

- By propulsion, internal combustion engines retained 81.25% share in 2024, while battery electric models are set to post the fastest 5.53% CAGR on the back of PM E-DRIVE incentives.

- By end-use, logistics & courier services commanded 37.63% revenue share in 2024; e-commerce last-mile delivery is forecast to expand at 5.58% CAGR through 2030.

India Small Commercial Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated E-Commerce Penetration | +1.5% | Asia Pacific core, spill-over to tier-2/3 urban centers | Medium term (2-4 years) |

| Rapid Post-GST Hub-And-Spoke Logistics | +1.2% | National, with early gains in Maharashtra, Gujarat, Karnataka | Medium term (2-4 years) |

| Growth Of Organised Retail Platforms | +0.9% | Urban centers, expanding to semi-urban markets | Medium term (2-4 years) |

| Government Fame-LI and State EV Subsidy Schemes | +0.8% | National, stronger adoption in Delhi NCR, Maharashtra, Karnataka | Short term (≤ 2 years) |

| Digital Freight Platforms | +0.7% | Metro cities expanding to tier-2 markets | Short term (≤ 2 years) |

| Food-Cold-Chain Grants Pushing | +0.4% | National, concentrated in agricultural states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated E-Commerce Penetration Into Tier-2/3 Cities

Online marketplaces extending beyond metros have intensified the need for nimble, high-stop-count vehicles capable of navigating congested streets and limited parking. The e-commerce last-mile segment is slated to post the fastest CAGR as grocery, fashion, and consumer-electronics orders proliferate in secondary cities. Bajaj Auto reported a massive jump in electric carrier three-wheelers during FY2025, attributing uptake to grocery-delivery tie-ups with BigBasket and Zepto[1]Bajaj Auto, “FY 2025 Investor Presentation,” bajajauto.com. Digital freight brokers integrate demand clustering algorithms that raise load factors and compress delivery windows, enabling micro-entrepreneurs to join organized supply chains. However, route densities differ widely across regions, prompting demand for modular body designs and telematics that can swap between parcel and refrigerated configurations within a single shift.

Rapid Post-GST Hub-and-Spoke Logistics Expansion

Implementation of the nationwide goods-and-services tax standardized interstate movement and prompted distributors to move from multi-warehouse stocking to centralized hubs feeding regional spokes. The new structure favors frequent short-haul runs with rapid turnaround, making mini trucks and light pickups indispensable for bridging hub gaps under 250 kilometers. VE Commercial Vehicles responded with the Eicher Pro X lineup manufactured on a dedicated Bhopal line, signaling OEM commitment to the 2-3.5 tonne niche. Industry registrations show the 2-3.5 tonne category growing in FY2023, far outpacing overall commercial vehicle growth. Shippers that adopted hub-and-spoke models report slightly lower inventory carrying costs, reinforcing a sustainable demand cycle for purpose-built small trucks. In turn, component suppliers benefit from higher localization as OEMs scale volumes for domestic and export markets.

Growth of Organized Retail & Kirana Aggregation Platforms

Modern trade chains and B2B aggregator apps that replenish neighborhood stores now prioritize standardized truck dimensions for back-end fulfillment. Sub-1-tonne vehicles execute two to three runs daily across 25-30 kilometers, creating steady demand with predictable loading cycles. Cold-chain mini trucks priced two-fifth above standard bodies are increasingly specified for dairy, ice-cream, and fresh-produce supply, supported by grant funding from the Mission for Integrated Cold Chain program[2]Ministry of Food Processing Industries, “Integrated Cold Chain Guidelines,” mofpi.gov.in. Organized retail’s rising share unlocks fleet-level contracts, giving OEMs visibility on multi-year replacement horizons and encouraging the release of factory-fitted reefer variants. While adoption currently skews to large metros, aggregator business models are expanding to 100+ tier-2 cities, setting the stage for broader penetration.

Government FAME-II & State EV Subsidy Schemes

The PM E-DRIVE package earmarks INR 10,900 crore until March 2026 to offset acquisition pricing for electric L5 cargo three-wheelers and light trucks. Under PM E-DRIVE, e-2W and e-3W demand incentives are set at ₹2,500 per kWh (with category-specific caps); in Delhi, the EV policy additionally provides up to ₹30,000 per vehicle for e-rickshaws/e-carts and light commercial EVs, which together can materially shorten payback for high-utilization fleets. Resultant momentum is visible in FY2025 electric three-wheeler sales, which topped and crossed more than half penetration within the segment. OEMs such as Mahindra Last Mile Mobility and Euler Motors are now timing EV launches around subsidy tranches, ensuring price parity at showroom floors. Charging consortia led by Tata Power and Fortum enhance the ecosystem by adding depot-based fast chargers, underpinning confidence among courier and grocery-delivery operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TCO Gap Between BEV and ICE | -0.6% | National, more pronounced in price-sensitive rural markets | Medium term (2-4 years) |

| Fragmented Financing Ecosystem | -0.4% | Rural and semi-urban markets predominantly | Short term (≤ 2 years) |

| Payload Derating | -0.3% | Urban markets with weight-sensitive applications | Medium term (2-4 years) |

| Slow Rollout Of Hydrogen Refuelling Corridor | -0.2% | Limited to pilot corridors in Gujarat, Haryana | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High TCO Gap Between BEV & ICE in Sub-1-Tonne Range

Electric mini trucks carry battery packs that account for nearly two-fifth of invoice price, widening the upfront premium versus diesel by INR 200,000-250,000. Operators running 60-kilometer daily routes need three to four years to recoup the premium through fuel savings, lengthening investment payback beyond typical owner-driver planning cycles. Battery mass also subtracts 90-100 kilograms of payload, cutting earning potential on per-trip fixed-rate contracts. Though lithium-ion prices fell one-fifth year-on-year in 2024, they remain well above parity thresholds for price-sensitive rural users. As a result, several states outside Delhi and Maharashtra report electric cargo three-wheeler penetration below quarter, underscoring the uneven maturity of the EV ecosystem.

Fragmented Financing Ecosystem for First-Time Buyers

Less than half of first-time owner-drivers secure loans from banks because of limited credit history and collateral, pushing them toward informal lenders that charge 4-6 percentage-points higher interest. NBFCs such as Shriram Transport and Mahindra Finance fill part of the gap, yet underwriting models still rely heavily on guarantor systems rather than cash-flow analytics. Ashok Leyland’s tie-up with Bandhan Bank and Tata Motors’ partnership with SBI exemplify attempts to streamline documentation and offer four-fifth on-road funding. Digital lending startups leverage telematics-derived duty-cycle data for risk scoring, but scale remains modest outside top cities. Without affordable capital, pent-up replacement demand among informal micro-fleets may remain unaddressed, muting otherwise strong fundamentals of the India small commercial vehicle market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Mini Trucks Anchor Urban Distribution Growth

The mini-truck sub-category captured 47.31% of the Indian small commercial vehicle market share in 2024, reflecting its sweet spot between compact footprint and 1-2 tonne payloads. Continued e-commerce expansion positions the segment for a 5.55% CAGR through 2030 as fleet operators prioritize vehicles that can navigate 3.5-meter lanes and execute 100+ daily stops. Mini-truck OEMs now integrate standard telematics that enable real-time proof-of-delivery, raising fleet uptime by a minimal amount.

Pickup trucks hold the number-two slot, serving diversified use-cases from construction aggregates to agri-produce haulage. The 2–3.5 tonne pickup cohort registered 31% year-over-year growth in FY2023, buoyed by infrastructure spending and rural road connectivity improvements under PMGSY-III. Enhanced reliability and bigger cargo decks enable pickups to back-haul building materials and seed inputs, supporting owner-driver profitability in mixed-load cycles.

By Payload Capacity: Sub-1-Tonne Category Commands Last-Mile Dominance

Vehicles carrying below 1 tonne represented 54.37% of 2024 shipments, underscoring their suitability for urban freight ecosystems where delivery density rewards agility over absolute tonnage. The category is forecast to post a 5.61% CAGR, supported by Kirana restocking rounds and quick-commerce parcels under 15 kilograms. Electric three-wheelers form the backbone of this bracket; FY2025 sales touched 699,073 units as electric rickshaw operators pivoted to cargo variants that qualify for the higher INR 50,000 PM E-DRIVE incentive slab.

The 1-2 tonne group caters to intra-district material movement, especially for FMCG wholesalers servicing rural mandis twice weekly. Operators value the segment’s ability to load five Euro pallets while staying within 6-meter overall length, avoiding urban entry restrictions levied on heavier trucks in Delhi and Bengaluru. Above-2-tonne payloaders carve out roles in brick transport and low-distance inter-city hops but face axle-load regulatory barriers and tighter turn radius issues inside tier-2 city cores. Manufacturers increasingly offer modular chassis that permit body swaps—refrigerated, high side deck, or tilting—to maximize residual value across seasonal peaks.

By Propulsion Type: Electric Variants Gather Momentum Amid ICE Predominance

Internal-combustion powertrains commanded 81.25% of demand in 2024 due to fueling convenience, broad service networks, and lower sticker prices. Diesel remains entrenched in rural and long-haul routes where daily running exceeds 300 kilometers. Nevertheless, battery electric volumes are projected to climb at 5.53% CAGR, fueled by subsidy support and fleet mandates from e-commerce majors aiming for 100% emission-free last-mile fleets by 2030.

Plug-in hybrids occupy a thin niche in hill states where regenerative braking on gradients adds range gains, while hydrogen fuel-cell pilots led by Tata Motors and IndianOil test 16-kilogram onboard tanks for 400-kilometer autonomy. Commercialization of hydrogen relies on corridor build-out along the Delhi–Mumbai Industrial Belt by 2028, but for now, ICE and BEV form the dual pillars shaping purchase decisions. OEMs hedge propulsion bets by investing in flexible platforms that accommodate both diesel drivelines and skateboard-style battery architecture, compressing development cycles and tooling amortization.

By End-Use Industry: E-Commerce Last-Mile Emerges as Fastest-Expanding Vertical

Logistics & courier operations accounted for 37.63% of sector revenue in 2024 as 3PL firms modernized fleets to meet service level agreements with FMCG, pharma, and electronics shippers. Growth remains healthy, yet e-commerce last-mile stands out with a 5.58% CAGR forecast through 2030. The surge stems from rapid grocery delivery commitments—often under 20 minutes—which necessitate dense micro-fulfillment networks and vehicles capable of multiple quick swaps per shift. Grofers and Flipkart lease dedicated electric mini trucks fitted with climate-controlled boxes to assure perishables quality over final-leg journeys.

FMCG & consumer durables channels continue to anchor base-load demand, utilizing mixed-body configurations for multipack consignments bound for rural stock-keeping units. Agriculture & dairy segments leverage refrigerated mini trucks to transport milk, curd, and fresh vegetables, a trend fortified by the National Dairy Development Board’s subsidy on reefer bodies. Construction and infrastructure freight mirrors fluctuations in cement and steel off-take, while pharmaceuticals rely on GDP-certified insulated vans fitted with real-time temperature loggers. Municipal services, though nascent, show promise as urban local bodies deploy compact tipper and sweeper variants to meet Swachh Bharat targets.

Geography Analysis

Maharashtra, Karnataka, and Tamil Nadu jointly contributed roughly two-fifths of 2024 national small commercial vehicle registrations, thanks to dense industrial clusters, port connectivity, and favorable state-level scrappage incentives that accelerate fleet renewal. Mumbai’s last-mile parcel density averages 120 packages per square kilometer, driving premium demand for 1 tonne electric mini trucks with narrow two-meter footprints[3]Municipal Corporation of Greater Mumbai, “Urban Freight Data 2024,” mcgm.gov.in. Bengaluru’s start-up ecosystem catalyzes early adoption of telematics and subscription-based vehicle leasing, shrinking average fleet age to four years, versus the national six-year benchmark.

Northern markets—Delhi NCR, Punjab, Haryana—lead the electrification curve, propelled by stringent air-quality directives that restrict new diesel LCV registrations within municipal limits. Delhi’s EV policy adds INR 30,000 beyond federal subsidies for L5 cargo three-wheelers, producing penetration rates one-fifth above the national mean[4]Delhi Transport Department, “Electric Vehicle Policy 2024,” transport.delhi.gov.in . Haryana’s IMT Manesar logistics belt, linked via the Kundli-Manesar Expressway, channels steady demand for high-deck pickups ferrying spare parts to auto OEMs.

Eastern and northeastern states lag in volume share but exhibit high growth potential. West Bengal implements an interest subvention scheme under its Banglashree industrial policy, aiding kirana aggregation fleets in Kolkata’s 300-year-old market sprawl. Odisha’s mining corridors spur demand for reinforced suspension light pickups capable of minimal grade climbs with 1.8 tonnes onboard. Northeast connectivity projects under Bharatmala Phase-I ease entry of organized freight carriers, yet challenging terrain requires four-wheel-drive micro pickups with differential locks, a niche that Mahindra’s Supro 4x4 prototype seeks to tap.

Competitive Landscape

The five market leaders—Tata Motors, Mahindra & Mahindra, Ashok Leyland, Bajaj Auto, and VE Commercial Vehicles—collectively held roughly three-fifths share in 2024, giving the India small commercial vehicle market a moderately concentrated profile. Tata Motors leverages its 1,250-outlet dealer network and Fleet Edge connected-vehicle suite to retain the lead in diesel mini trucks. Mahindra bolsters its supremacy in electric three-wheelers through the Zor Grand, which now ships with a 10-year battery warranty and fast-charge compatibility, de-risking residual value for financiers.

Challenger OEMs exploit white spaces, especially in urban EV niches. Euler Motors delivers vehicles with 12-kilowatt motors and category-leading 688 kilogram payloads, winning contracts from BigBasket and Flipkart. Altigreen Propulsion Labs focuses on high-torque three-wheelers for gradient-heavy southern metros; its low-floor deck design improves loading ergonomics, cutting driver strain. Omega Seiki Mobility pioneered a pay-per-kilometer subscription covering vehicle, charging, and maintenance, easing cash-flow pressure on gig-economy operators.

Strategic moves shape competition. In February 2025, VE Commercial Vehicles inaugurated a Bhopal assembly line staffed entirely by women, signaling progress on diversity and lean manufacturing. January 2025 witnessed Switch Mobility unveiling the IeV8 7.2-tonne electric LCV with proprietary iON telematics, positioning for medium-duty fleet electrification. The same month, Eicher Trucks & Buses rolled out the Pro X electric-first range featuring the segment’s largest cargo deck and 24x7 remote diagnostics, highlighting service uptime as a key differentiator.

India Small Commercial Vehicle Industry Leaders

Tata Motors Ltd.

Mahindra & Mahindra Ltd.

Ashok Leyland Ltd.

Piaggio Vehicles Pvt Ltd.

Maruti Suzuki India Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: VE Commercial Vehicles inaugurated a dedicated manufacturing line for the Eicher Pro X small truck range at its Bhopal plant. The line features an all-women final assembly team and Industry 4.0 compliance, targeting short-haul and last-mile logistics with an electric-first design.

- January 2025: Switch Mobility launched the IeV8 electric light commercial vehicle at Bharat Mobility Expo 2025, featuring 7.2-tonne capacity, 250 kilometer range, 4-tonne payload capability, and the proprietary Switch iON telematics system for fleet management.

- January 2025: Eicher Trucks and Buses launched the Pro X electric-first small commercial vehicle range at Bharat Mobility Global Expo, marking strategic entry into the 2-3.5 tonne segment with largest cargo loading space, advanced safety systems, and 24x7 monitoring via Eicher’s Uptime Centre.

India Small Commercial Vehicle Market Report Scope

| Mini Trucks |

| Pickup Trucks |

| Vans |

| Three-Wheelers |

| Less than 1 Ton |

| 1–2 Ton |

| Above 2 Ton |

| Internal Combustion Engine |

| Battery Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| Fuel Cell Electric Vehicle |

| Logistics & Courier |

| E-Commerce Last-Mile |

| FMCG & Consumer Durables |

| Agriculture & Dairy |

| Construction & Infrastructure |

| Retail |

| Pharmaceuticals & Healthcare Distribution |

| Hospitality & Catering |

| Municipal Services |

| By Vehicle Type | Mini Trucks |

| Pickup Trucks | |

| Vans | |

| Three-Wheelers | |

| By Payload Capacity | Less than 1 Ton |

| 1–2 Ton | |

| Above 2 Ton | |

| By Propulsion Type | Internal Combustion Engine |

| Battery Electric Vehicle | |

| Plug-in Hybrid Electric Vehicle | |

| Fuel Cell Electric Vehicle | |

| By End-Use Industry | Logistics & Courier |

| E-Commerce Last-Mile | |

| FMCG & Consumer Durables | |

| Agriculture & Dairy | |

| Construction & Infrastructure | |

| Retail | |

| Pharmaceuticals & Healthcare Distribution | |

| Hospitality & Catering | |

| Municipal Services |

Key Questions Answered in the Report

What is the forecast growth rate for the India small commercial vehicle market through 2030?

The market is projected to grow at a 5.51% CAGR, rising from USD 4.63 billion in 2025 to USD 6.05 billion by 2030.

Which vehicle type holds the largest share in India’s small commercial segment?

Mini trucks lead with 47.31% share thanks to their balance of payload and urban maneuverability.

How fast is the electric small commercial vehicle segment expanding?

Battery electric variants are poised for a 5.53% CAGR as subsidies and fleet commitments accelerate adoption.

Why is e-commerce driving demand for light commercial vehicles?

Hyperlocal delivery models require agile, high-stop-count vehicles, making e-commerce last-mile the fastest-growing end-use at 5.58% CAGR.

Which regions show the highest EV penetration for small commercial vehicles?

Delhi NCR and other northern states lead, with three-wheeler EV penetration 15-20% above the national average due to supportive policies.

Page last updated on: