Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

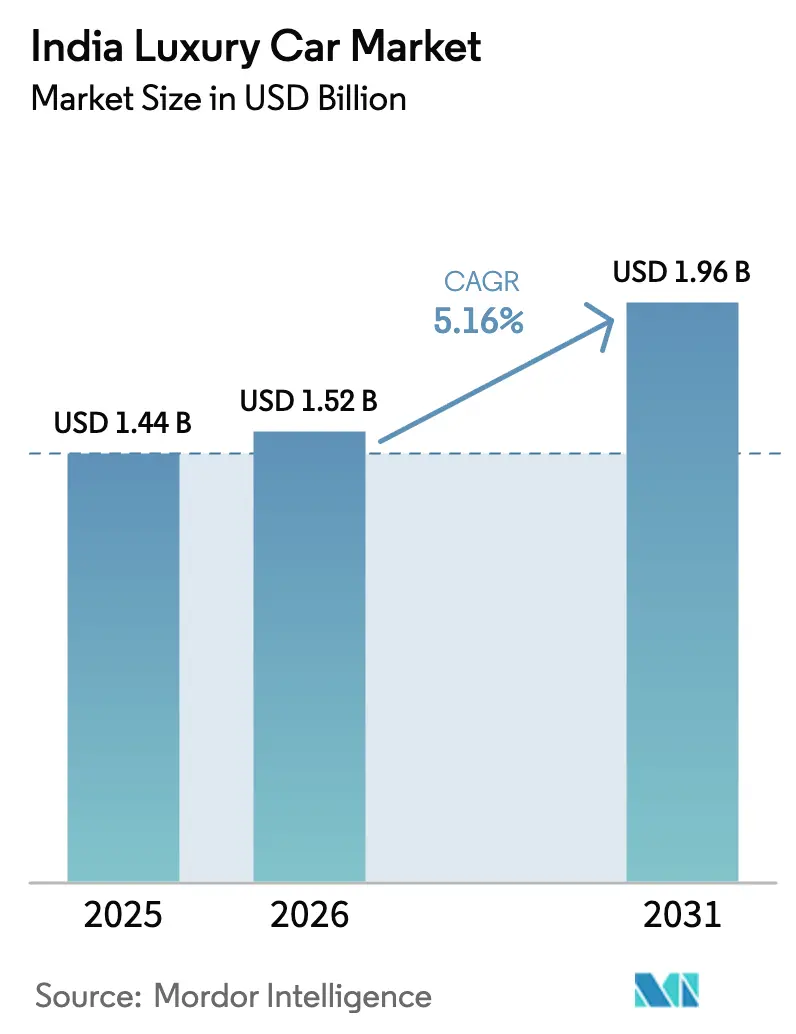

| Base Year Market Size (2025) | USD 1.44 Billion |

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 1.96 Billion |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Luxury Car Market Analysis by Mordor Intelligence

The Indian luxury car market size is expected to grow from USD 1.44 billion in 2025 to USD 1.52 billion in 2026 and is forecast to reach USD 1.96 billion by 2031, growing at a 5.16% CAGR over the forecast period (2026-2031). A widening preference gap now shapes demand: battery-electric cars are expanding at a 21.98% CAGR through 2031, more than four times the overall pace, while conventional engines still account for three-quarters of unit sales. State subsidies that reimburse up to 15% of the vehicle cost, rapid build-out of 150 kW public chargers, and GST cuts on hybrids are reinforcing the push toward electrification. In contrast, entry-level CKD sedans are sustaining price-sensitive buyers. Affluent households shifting from joint to nuclear family structures, the rise of OEM-financed subscriptions, and digital direct-to-consumer storefronts further underpin volume growth. Meanwhile, regulatory uncertainties on CBU duties and a widening technician shortfall temper long-run momentum.

Key Report Takeaways

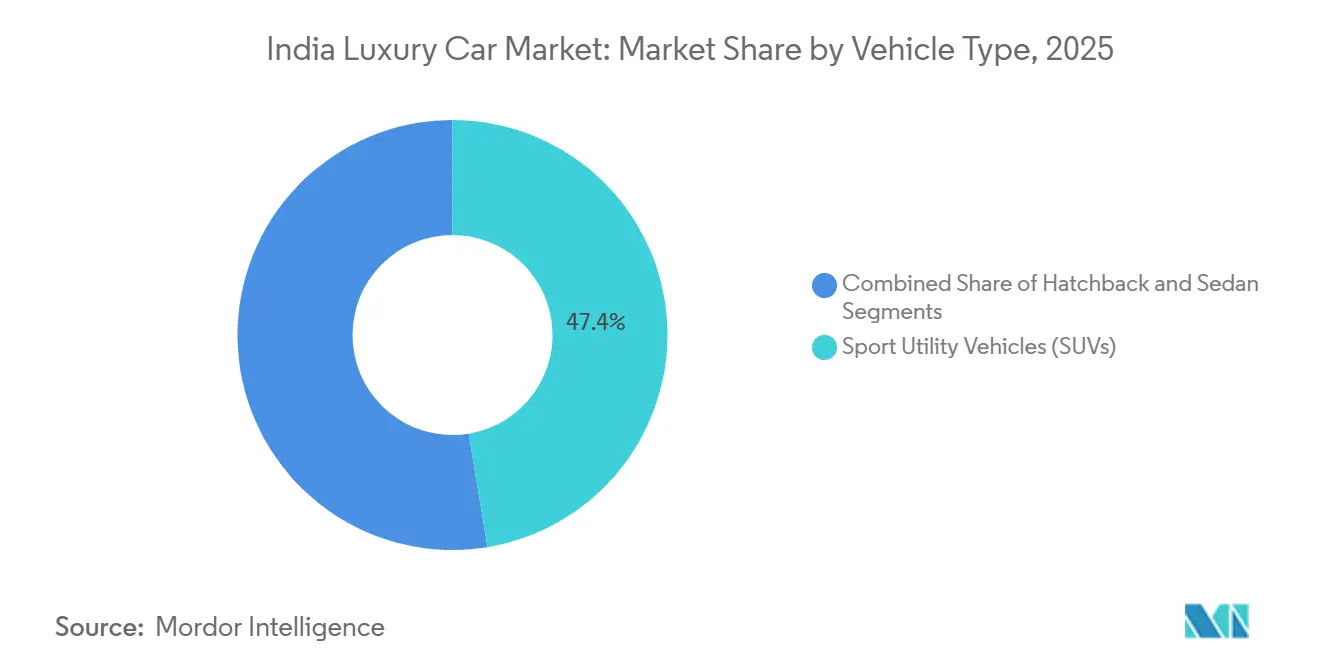

- By vehicle type, Sport Utility Vehicles (SUVs) led the Indian luxury car market with a 47.43% share in 2025; sedans are projected to post a 10.12% CAGR through 2031.

- By drive type, internal combustion engines accounted for 74.68% of the Indian luxury car market share in 2025, while battery-electric vehicles are expected to capture the fastest growth at a 21.98% CAGR through 2031.

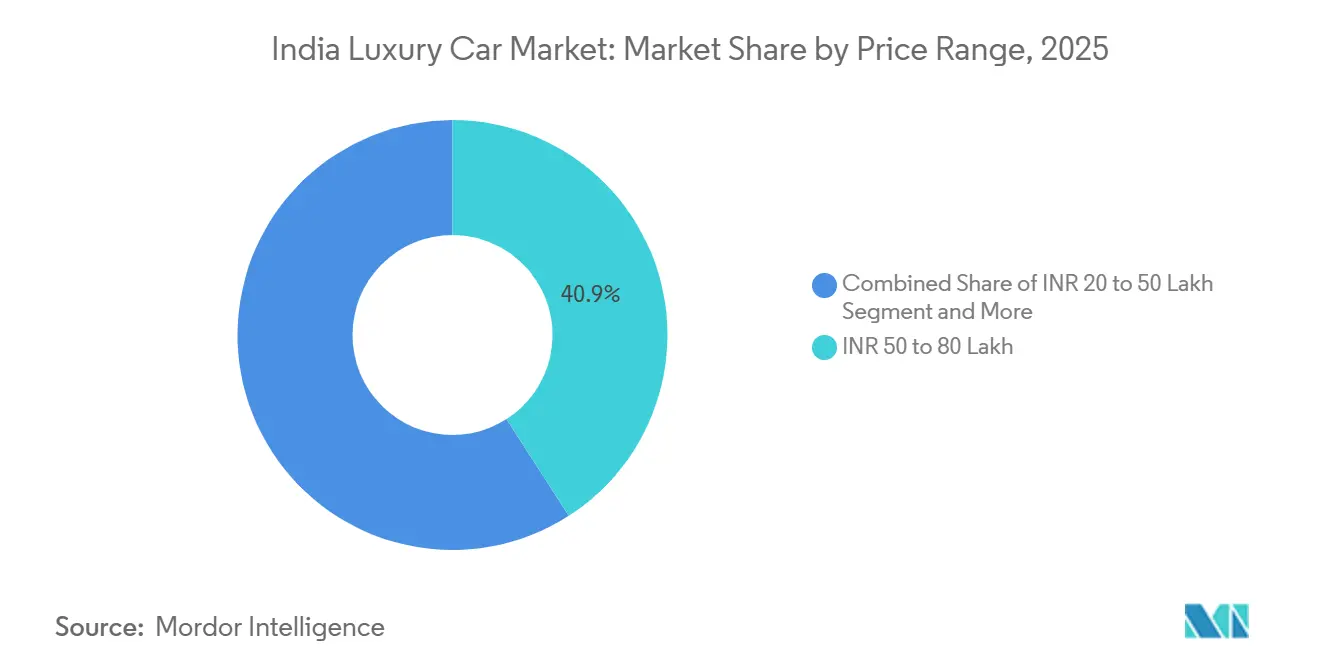

- By price band, the INR 50 to 80 lakh bracket accounted for 40.87% of the Indian luxury car market size in 2025 and is set to grow by a 10.36% CAGR through 2031.

- By sales channel, authorized dealerships held 67.82% of the Indian luxury car market share in 2025; however, online direct-to-consumer platforms are projected to rise at a 14.62% CAGR through 2031.

- By region, West India retained 32.94% of the Indian luxury car market share in 2025, whereas South India is poised to log the highest 11.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Luxury Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of Upper-Middle-Class | +1.8% | National, metros and Tier-II cities | Medium term (2–4 years) |

| Rising Availability of Entry-Level Models | +1.2% | West and North India strongest | Short term (≤ 2 years) |

| EV Incentives by State Governments | +0.9% | Maharashtra, Karnataka, Tamil Nadu | Medium term (2–4 years) |

| Rapid Rollout of Public DC Chargers | +0.7% | National highways | Long term (≥ 4 years) |

| OEM-Financed Subscription and Leasing Schemes | +0.6% | Mumbai, Delhi, Bangalore | Short term (≤ 2 years) |

| Chinese Ultra-Luxury EV Brands | +0.4% | Metros first, Tier-II later | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumization of Upper-middle-class Households

India now has an estimated 8.71 lakh millionaire households (defined as households with a net worth of INR 8.7 crore or more), marking a 90 % increase compared with 2021 (from about INR 4.58 lakh). These affluent households represent roughly 0.31 % of all Indian households and reflect strong wealth creation in the country amid economic growth[1]Rishi Kant, "India has 8.71 lakh millionaire households, up 90% from 2021: Mercedes-Benz Hurun India Wealth Report 2025," Fortune India, fortuneindia.com . Nuclear families now account for 62% of luxury purchases, up from 48% in 2020, as dual-income couples increasingly favor personal mobility. Liquidity is evident in UPI transfers above INR 1 lakh, which have surged 34% year over year. Slowing real-estate appreciation redirects status signaling toward automobile ownership.

Rising Availability of Entry-level Models (CKD)

Local assembly cut the entry point for German sedans to INR 48.9 lakh, with BMW’s X1 sDrive18i M Sport priced INR 6.5 lakh lower than the prior CBU version. CKD economics avoids 100% CBU duties, preserves 28-32% gross margins, and trims delivery lead times to six weeks. Mercedes-Benz sold 19,565 units in India in 2024[2]Ketan Thakkar, "Mercedes-Benz sells a record 19,565 units in India in 2024," AUTOCAR professional, autocarpro. in. Audi’s Aurangabad plant will accommodate BEV platforms by late 2026, extending CKD savings to electric models below INR 80 lakh.

EV Incentives by State Governments

Karnataka waives road tax and registration fees, saving INR 8-12 lakh on an INR 1 crore luxury EV, while Tamil Nadu refunds 100% of state GST for five years on locally assembled EVs[3]. These benefits stack on top of the federal PM E-DRIVE fund. Cross-state registration arbitrage has emerged, prompting Maharashtra to cap subsidies and mandate three-year in-state registration, which is expected to reduce new EV sales in the coming years.

Rapid Rollout of 150 kW+ Public DC Chargers on Inter-city Corridors

National guidelines require a 150 kW charger every 100 km; 1,200 were live by December 2025, with clusters on the Bangalore-Chennai, Mumbai-Pune, and Delhi-Jaipur routes. Fast charging now restores 10-80% of the battery in roughly 22 minutes, lowering the per-kilometer energy cost by 72% compared to petrol. Corporate chauffeur fleets exploit the shorter downtime, yet voltage sags have necessitated power throttling during peak hours on the Mumbai-Pune corridor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High GST and Cess Structure | -1.4% | National | Short term (≤ 2 years) |

| Import Duty Uncertainty on CBUs | -0.8% | National | Medium term (2–4 years) |

| Slow Build-Out of Certified Pre-Owned Luxury Networks | -0.5% | Metros, spreading to Tier-II | Medium term (2–4 years) |

| Scarcity of Trained Technicians | -0.3% | Nationwide, acute outside metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Trained Technicians for ADAS and High-Voltage Systems

The Automotive Skills Development Council estimates a 2.4 million technician shortfall by 2026, with only 50,000 of the 500,000 required EV-certified technicians currently available, resulting in a 10% fill rate. This shortfall extends warranty-claim resolution from 4 days in metros to 18 days in tier-2 cities like Coimbatore and Jaipur. The skills gap manifests in customer dissatisfaction; a 2024 J.D. Power study found that 42% of luxury EV owners in tier-2 markets rated aftersales service below expectations, citing technician unfamiliarity with battery thermal management diagnostics and over-the-air software updates, factors that depress brand Net Promoter Scores by 18 points relative to metro areas.

Slow Build-out of Certified Pre-owned Luxury Networks

The certified pre-owned segment is advancing but lacks scale, particularly outside the top ten metropolitan areas, which constrains trade-in liquidity and suppresses upgrade cycles. Audi planned to expand its pre-owned showrooms to 30 by 2025; however, coverage gaps persist in emerging wealth hubs such as Indore, Kochi, and Jaipur. Without brand-backed refurbishment, financing, and warranty frameworks, affluent buyers remain wary of secondary transactions, dampening the resale value that underpins new-car purchase decisions. The organized expansion of certified networks is therefore critical to sustaining higher absorption rates for new inventory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Dominate Despite Sedan Revival

Sport Utility Vehicles (SUVs) captured 47.43% of India's luxury car market share in 2025, while sedans are expected to resurge with a forecast 10.12% CAGR through 2031. Rear-seat entertainment uptake exceeds 2/3, indicating a shift in value toward ride quality. SUVs remain indispensable in tier-2 markets with poor road surfaces; the ultra-luxury SUV niche, priced above INR 2 crore, is advancing on the back of models like the Rolls-Royce Cullinan.

Hatchbacks remain a negligible segment, constrained by the absence of premium offerings priced below INR 40 lakh (approximately USD 48,000). The discontinuation of the Mercedes A-Class in 2023 left a void that no competitor has filled, ceding the entry-luxury space to mass-premium brands like the Skoda Octavia. Hybrid powertrains further propel the sedan revival - BMW's 530e and Mercedes E 300e - which benefit from the September 2025 GST reduction to 38%, trimming prices by INR 9-11 lakh (approximately USD 10,800-13,200) and compressing the premium over equivalent petrol variants to just INR 4 lakh (approximately USD 4,800), a gap that buyers recover within 60,000 kilometers given petrol prices averaging INR 105 per liter (approximately USD 1.26) in metros.

By Drive Type: ICE Dominance Faces EV Disruption

Internal combustion engines still held 74.68% of India's luxury car market share in 2025; however, BEVs are expected to expand at a 21.98% CAGR through 2031, thereby quadrupling the overall pace of the Indian luxury car market. Mercedes-Benz EQS SUV buyers can leverage a 40% first-year depreciation under India’s tax code, thereby narrowing the payback horizon. Plug-in hybrids gained momentum from the September 2025 GST cut to 38%, resulting in a 28% surge in month-on-month registrations. Residual-value anxiety keeps some buyers in petrol variants, where refueling convenience and lower sticker prices remain essential considerations.

The ICE segment's resilience stems from three factors: established refueling infrastructure (85,000 petrol pumps versus 12,000 public EV chargers), faster refueling (3 minutes versus 25 minutes for fast-charging), and lower upfront cost - the BMW 530i at INR 72.9 lakh (approximately USD 87,500) undercuts the i4 eDrive40 by INR 18 lakh (approximately USD 21,600), a gap that buyers with annual mileage under 15,000 kilometers cannot justify. The BMW 530e and Mercedes E 300e are leading the uptake in Bangalore and Pune, cities where buyers prioritize tax efficiency over outright performance.

By Price Range: Mid-luxury Segment Drives Growth

The INR 50 to 80 lakh (USD 55,000 to 90,000) band captured 40.87% of the Indian luxury car market size in 2025 and is expected to rise at a 10.36% CAGR through 2031, driven by CKD hybrids such as the BMW 530e and Mercedes E 300e. Banks extend up to 85% loan-to-value on this tier, easing down-payment hurdles for 4.2 million eligible households. The ultra-luxury tier, above INR 80 lakh (approximately USD 87,968.4), is smaller but posts strong growth, propelled by bespoke sports cars such as Lamborghini’s Revuelto plug-in hybrid.

This bracket benefits from the September 2025 GST reform, which reduced hybrid rates to 38%, trimming sticker prices by INR 8-11 lakh (approximately USD 8,796 -12,095) and bringing the BMW 530e INR 74.5 lakh (approximately USD 81,920.9)) and Mercedes E 300e INR 78.5 lakh (approximately USD 86,319.4)) within reach of buyers previously capped at INR 70 lakh (approximately USD 76,972.7) budgets.

By Sales Channel: Digital Transformation Accelerates

Dealerships still accounted for 67.82% of India's luxury car market share in 2025, yet OEM-operated web portals are projected to scale at a 14.62% CAGR through 2031. End-to-end online transactions compress delivery cycles by three weeks and remove 8-12% dealer markups. Trade-in friction persists; algorithmic valuations run 8-12% below physical appraisals, prompting many buyers to finalize the deal at showrooms. OEM-run service centers in metros preserve 28-32% after-sales margins and help migrate the customer base online.

The online channel's appeal extends beyond convenience; digital platforms offer transparency in pricing—eliminating the 8-12% dealer markup that franchise showrooms layer onto manufacturer-suggested retail prices—and enable side-by-side comparisons of financing options from 6-8 lenders, a feature that reduces effective interest rates by 40-60 basis points.

Geography Analysis

West India retained 32.94% of the Indian luxury car market share in 2025, whereas South India is poised to log the highest 11.27% CAGR through 2031. West India’s dominance stems from Mumbai’s 18,000 ultra-high-net-worth residents and Pune’s OEM cluster, which reduces delivery times to as low as four weeks. Yet saturation looms as luxury penetration nears five vehicles per 1,000 households.

South India benefits from Karnataka’s tax waivers and Tamil Nadu’s GST reimbursement, yielding upfront savings of INR 8-12 lakh per luxury EV and compressing seven-year ownership costs by 18%.

North India, anchored by the Delhi NCR region, faces headwinds from stricter pollution controls and odd-even restrictions. SUVs dominate here due to flood-prone roads, while East and Northeast India remain under-penetrated at 6.5%, constrained by sparse dealer networks and only 200 fast chargers across eight states.

Competitive Landscape

The Indian luxury car industry is moderately concentrated, with Mercedes-Benz, BMW, and Audi holding significant market shares. Electrification shapes brand trajectories—Mercedes-Benz sells nine EQ models, while BMW has committed to local BEV assembly by 2026.

Ultra-luxury marques set delivery records: Rolls-Royce advanced Cullinan II orders, and Bentley’s Bentayga EWB captured chauffeur-driven elites. Subscription platforms like AMP Energy’s premium EV plan yield higher lifetime margins and court younger, mobile professionals.

Technology differentiation accelerates; Mercedes’ MBUX Hyperscreen and BMW’s iDrive 8 introduce over-the-air upgrades that protect residual values. Yet a technician shortage threatens service quality, compelling OEMs to invest in academies and remote diagnostic tools to avoid erosion of brand equity.

India Luxury Car Industry Leaders

-

Jaguar Land Rover Automotive PLC

-

BMW AG

-

Mercedes-Benz Group AG

-

Audi AG

-

AB Volvo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: AMP Energy launched a premium EV subscription service in the National Capital Region, offering access to BMW iX, Mercedes EQS, Audi e-tron, and BYD models for INR 1.29 lakh (USD 1,545) per month with zero down payment, bundling insurance, maintenance, and roadside assistance to convert luxury EV ownership into a flexible operating expense.

- September 2024: Rolls-Royce Motor Cars India introduced the Cullinan Series II at INR 10.5 crore (approximately USD 12.57 million), featuring revised exterior styling, an upgraded 12.3-inch infotainment system, and bespoke interior options.

- July 2024: BMW Group introduced the 5 Series Long Wheelbase in India with a starting price of INR 72.90 lakh (ex-showroom), making India the world’s first right-hand-drive market to receive this extended wheelbase variant.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the India luxury car market covers every new passenger vehicle officially retailed in the country that is positioned by the OEM as premium or ultra-luxury and priced within the top decile of the national price ladder. Body styles span sedans, SUVs, coupes, convertibles, and performance variants, and the drivetrain mix includes internal-combustion, hybrid, and battery-electric units.

Scope exclusions include aftermarket add-ons, pre-owned or imported used cars, subscription or rental revenue, and armored fleet conversions, which are not included.

Segmentation Overview

-

By Vehicle Type

- Sport Utility Vehicles (SUVs)

- Sedan

- Hatchback

-

By Drive Type

- Internal Combustion Engine (ICE)

- Hybrid

- Battery Electric

-

By Price Range

- INR 20 to 50 Lakh

- INR 50 to 80 Lakh

- Above INR 80 Lakh

-

By Sales Channel

- Company-owned Showrooms

- Authorized Dealerships/Franchise

- Online (Direct-to-Consumer)

-

By Region

- North India

- West India

- South India

- East and North-East India

Detailed Research Methodology and Data Validation

Primary Research

We spoke with showroom heads, luxury-focused financiers, fleet buyers, and emerging EV-charging operators across Delhi NCR, Mumbai, Bengaluru, and Pune. Insights on discount spreads, booking backlogs, and price-sensitive cohorts refined assumptions drawn from desk work and grounded our demand curve.

Desk Research

Our team begins with hard counts from SIAM production releases, MoRTH's Vahan registration dashboard, and DGCI&S customs files to size yearly demand and the share taken by luxury nameplates. Macroeconomic series from the Reserve Bank of India and the Ministry of Statistics let us adjust for disposable income swings, loan rates, and urban household growth, while UN Comtrade clarifies CBU inflows that supplement local assembly. Company reports, RBI filings, tier-one business dailies, and trade association newsletters add model launch timing, typical transaction prices, and showroom network expansion. Where deeper financials are vital, we consult D&B Hoovers. These sources are illustrative only; many additional references helped cross-check numbers and close data gaps.

Market-Sizing & Forecasting

We construct the baseline top-down, starting with verified luxury registrations and multiplying by weighted average ex-showroom prices. We then sense-check those totals with sampled dealer invoices and occasional supplier roll-ups. Key variables feeding the model include high-net-worth household growth, finance penetration, average retail price movement, BEV fast-charger density, model-launch cadence, and GST plus compensation-cess levels. Forecasts employ multivariate regression with scenario analysis, and any bottom-up gaps are bridged with the nearest audited proxy.

Data Validation & Update Cycle

Outputs pass three internal reviews, variance scans against signals such as premium fuel sales and luxury loan disbursements, and senior analyst sign-off. We refresh numbers annually and trigger interim updates when material events, such as tax changes or sudden import-duty revisions, arise, ensuring clients receive the latest outlook.

Why Mordor's India Luxury Car Baseline Earns Decision-Maker Trust

Published estimates often diverge because providers draw different scope fences, price benchmarks, and refresh cadences. Some include used imports or lease revenue, others apply global average selling prices without local adjustment, and a few rely on narrow shipment samples.

Mordor grounds its view in official counts and live dealer feedback, limiting both double counting and dated pricing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.32 billion (2025) | Mordor Intelligence | |

| USD 34.02 billion (2024) | Global Consultancy A | Counts used imports and leases, applies global ASP, unclear update cycle |

| USD 1.14 billion (2024) | Regional Consultancy B | Omits BEVs, relies only on shipment estimates |

The comparison shows that Mordor's disciplined scope, timely data pulls, and multi-source validation produce a balanced, transparent baseline that decision-makers can trace to concrete inputs and repeatable steps.

Key Questions Answered in the Report

What is the current size of the India luxury car market?

The India luxury car market size reached USD 1.52 billion in 2026.

How fast is the battery-electric segment growing?

Battery electric models are forecast to expand at 21.98% CAGR through 2031.

Which price band drives the most volume?

The INR 50-80 lakh bracket accounted for 40.87% of 2025 sales and is rising at 10.36% CAGR.

Why is South India growing faster than other regions?

Generous EV incentives and a dense fast-charger network lift South India to an 11.27% CAGR.

What tax changes affect hybrid luxury cars?

In September 2025 the GST Council cut the effective rate on strong hybrids from 43% to 38%, shaving up to INR 11 lakh off prices.

How concentrated is the competitive landscape?

Mercedes-Benz, BMW, and Audi together hold major market share, reflecting moderate concentration.

Page last updated on: