Indonesia Commercial Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 11.32 Billion |

| Market Size (2030) | USD 14.43 Billion |

| Growth Rate (2025 - 2030) | 4.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Commercial Vehicle Market Analysis by Mordor Intelligence

The Indonesian commercial vehicles market size stands at USD 11.32 billion in 2025 and is forecast to reach USD 14.43 billion by 2030, translating into a 4.97% CAGR. Robust public‐works spending, expanding e-commerce networks, and policy-backed moves toward alternative fuels collectively support steady fleet replacement and expansion. Biodiesel blending mandates (B35 today, B40 under discussion) stimulate demand for newer fuel-compatible engines even as rising oil-palm feedstock costs push operators to scrutinize the total cost of ownership. In parallel, electric light trucks and minibuses gather momentum in Jakarta, Surabaya, and Bandung, where over 3,200 public chargers already operate. Fleet owners cite uptime guarantees from Japanese incumbents and zero-down-payment loans from Chinese newcomers as the decisive factors in tender bids. A final pillar of resilience comes from Kalimantan’s mining corridor, whose double-digit coal and nickel haulage expansion shields overall volumes against cyclical softness in Java-centric consumer spending.

Key Report Takeaways

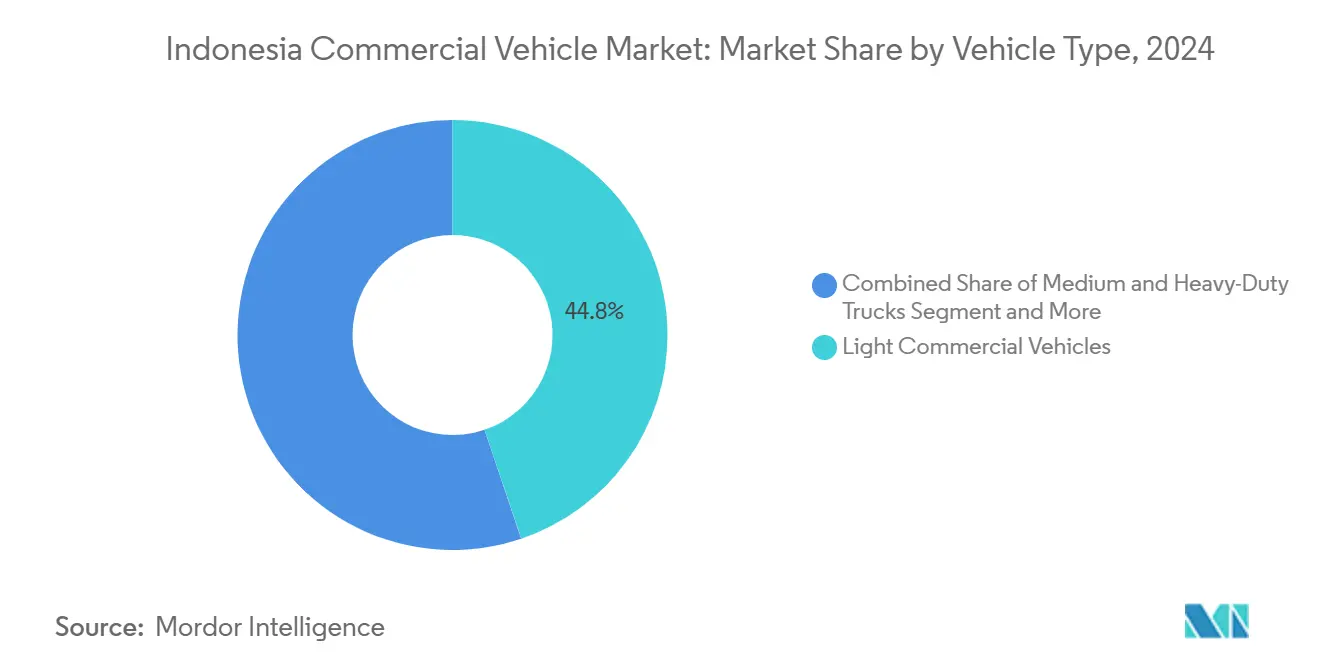

- By vehicle type, light commercial vehicles led the Indonesian commercial vehicle market with 44.81% share in 2024, and the segment is expected to advance at 6.21% CAGR through 2030.

- By propulsion, internal combustion engines commanded 86.21% share of the Indonesian commercial vehicles market size in 2024; battery-electric systems are projected to expand at 9.15% CAGR to 2030.

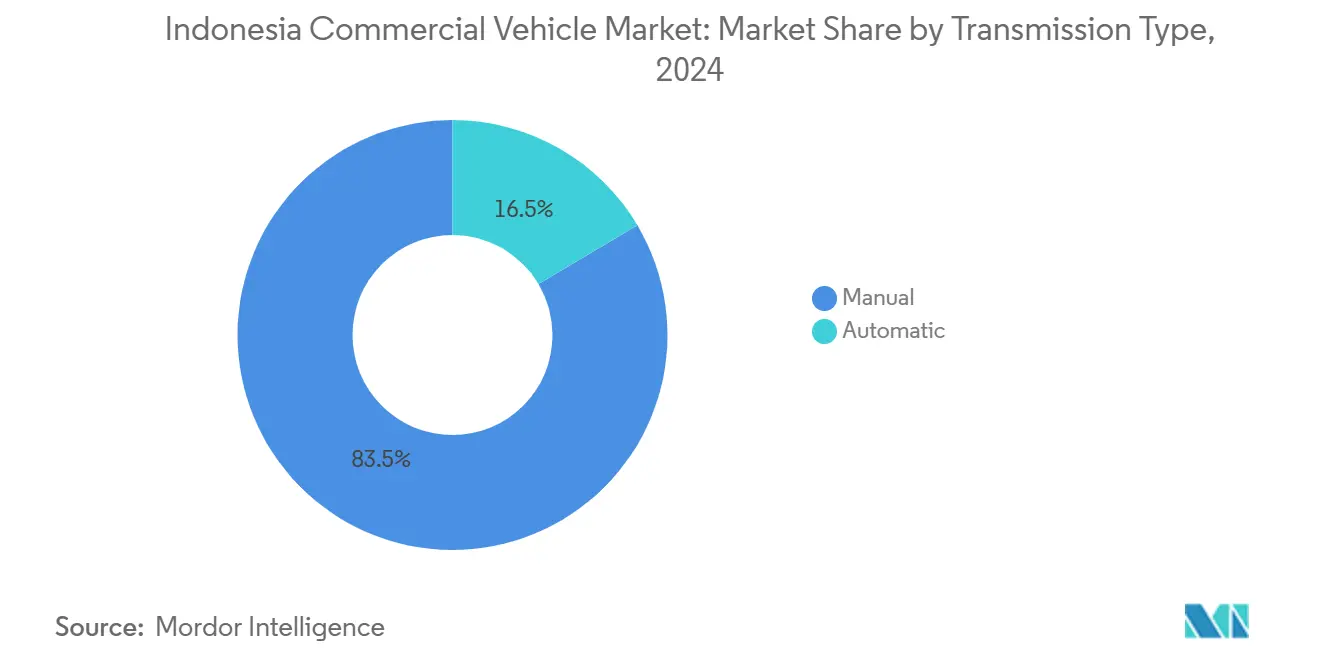

- By transmission, manual units accounted for an 83.52% share of the Indonesian commercial vehicles market in 2024, whereas automatic units are on track for an 8.19% CAGR through 2030.

- By application, logistics and freight captured 43.47% of the Indonesian commercial vehicle revenue share in 2024, and mining posted the fastest growth at 7.27% CAGR to 2030.

- By region, Java held 55.43% of the Indonesian commercial vehicles market size in 2024, while Kalimantan recorded the quickest climb at 7.35% CAGR over the outlook period.

Indonesia Commercial Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Logistics Boom from Infrastructure | +1.5% | Java, Sumatra corridors | Medium term (2-4 years) |

| Battery-Electric Fleet Incentives | +0.9% | Java and tier-one cities | Medium term (2-4 years) |

| E-Commerce Last-Mile Surge | +0.8% | Urban Java, extending to Sumatra & Kalimantan | Short term (≤ 2 years) |

| OEM Zero-Downtime Programs | +0.7% | National | Short term (≤ 2 years) |

| Government B35 Biodiesel Mandate | +0.6% | Nationwide | Long term (≥ 4 years) |

| 2-Wheel Battery-Swap Network Growth | +0.4% | Urban Java, Sumatra, Bali | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Logistics Boom

Indonesia's toll road and port upgrades are driving growth in the commercial vehicle sector. Thousands of kilometers of new toll roads have improved freight throughput and reduced truck turnaround times, prompting fleet operators to adopt heavier axle configurations for longer-haul efficiencies. The Trans-Sumatra Highway has reduced logistics costs, enabling 3PL firms to redeploy assets across key regions, such as Lampung and Medan. Upgraded inter-island ports also integrate Kalimantan and Sulawesi into Java-centric supply chains, enhancing connectivity. Vehicle configurations are shifting toward durability and performance optimization. Harmonized axle-load regulations are boosting demand for rigid trucks under 16 tons. At the same time, medium-duty platforms with reinforced suspensions and advanced cooling systems outperform older models, reflecting a shift toward durability and performance optimization.

Incentives for Battery-Electric Commercial Fleets

Indonesia's domestic-content regulations ease the financial burden on electric vehicle manufacturers, particularly in the city-class van sector. When local value exceeds a designated threshold, producers enjoy tax cuts, resulting in reduced capital expenditure per unit. This makes electric vans more appealing to fleet operators and logistics companies. The swift expansion of public charging stations, spearheaded by PLN, has broadened corridor coverage, alleviating range anxiety for logistics operators focused on green-zone deliveries. This robust infrastructure ensures reliable depot returns and facilitates off-peak charging contracts. With their reduced electricity rates, these contracts enhance the total cost of ownership (TCO) for electric fleets over five years. From Jakarta to Denpasar, city councils throughout Indonesia are showing a growing preference for zero-emission minibuses in public tenders. This trend underscores a nationwide pivot towards sustainable urban mobility, promising a long-term boost to the commercial vehicle market through 2030.

Surge in E-Commerce Last-Mile Demand

Same-day delivery services are rapidly transforming urban logistics, driving a demand for specialized vehicles designed for frequent parcel drops. To maneuver efficiently through crowded city streets, operators are turning to compact vans and mini-trucks, featuring narrow frames and sliding doors. These vehicle designs, often a collaborative effort between Japanese manufacturers and local bodybuilders, are specifically tailored to address the challenges of bustling urban environments. Digital innovations, including mobile payments and app-driven route optimization, are boosting delivery efficiency, enabling fleets to make more stops with lighter packages. Consequently, vehicle design now prioritizes durability and maneuverability over sheer payload capacity, emphasizing operational efficiency. In cities like Jakarta, a surge in logistics demand, coupled with infrastructure enhancements, is leading to more frequent vehicle rotations. Light commercial vehicles are now making multiple daily trips, amplifying their annual usage. This uptick highlights the increasing pace of urban freight operations and the growing importance of agile, tech-savvy delivery networks.

Rapid Build-Out of 2-Wheel Battery-Swap Networks

Smoot Motor is showcasing its prowess with a vast battery swapping network, catering to an expanding rider demographic. This achievement underscores the company's adeptness in battery inventory management and ensuring high station uptime—both pivotal for instilling trust in shared energy infrastructures. The approach's reliability and scalability are assuaging investor apprehensions, paving the way for wider applications, including possible adaptations for light commercial vehicles. Furthermore, leasing firms are introducing battery-as-a-service models, enabling small fleet operators to better manage cash flow by decoupling asset ownership from its usage. In urban settings, cities boasting dense swap station networks are taking the lead in electric vehicle adoption. These networks present a viable alternative to traditional charging infrastructures, especially in regions like Indonesia, where there's a surge in commercial vehicle electrification. This blend of logistical efficiency and financial ingenuity is propelling the transition to cleaner, more integrated urban transportation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High EV CV Upfront Costs | -0.9% | Nation-wide, acute outside Java | Medium term (2-4 years) |

| Sparse Fast-Charging Beyond Java | -0.6% | Sumatra, Kalimantan, Sulawesi, East | Long term (≥ 4 years) |

| Influx of Chinese Built-Up Trucks | -0.5% | Mining clusters | Short term (≤ 2 years) |

| B35 Blend Maintenance Challenges | -0.4% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse Public Fast-Charging Outside Java

Sparse public fast-charging infrastructure outside Java continues to limit the pace of commercial vehicle electrification in Indonesia. While Java hosts the majority of fast chargers, regions like Kalimantan remain underserved, with only minimal coverage along key industrial corridors. As a result, long-haul carriers continue to rely on diesel-powered rigs, dampening demand for electric trucks. Utilities cite grid fragility in remote districts and anticipate upgrades only in the longer term. Until charging coverage expands beyond urban centers, the electrification of Indonesia’s commercial vehicle market is expected to remain largely concentrated in city-based operations.

Maintenance Issues from Higher B35 Biodiesel Blend

Current biodiesel blends are causing injector clogging to occur sooner than with earlier formulations, leading to more frequent maintenance. In response, fleets are adopting additional filtration systems and shortening oil drain intervals, increasing operating costs. Some operators are trying out dual-tank retrofits: they use pure diesel for cold starts and switch to biodiesel while cruising, aiming to strike a balance between performance and emissions. Yet, the steep initial investment for these systems has curtailed their widespread adoption. Consequently, concerns about reliability are tempering enthusiasm for fleet replacements. Many operators are choosing to extend the lifespan of their current vehicles instead of investing in new models that are compatible with biodiesel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Light Commercial Vehicles Maintain Leadership

Light commercial vehicles held 44.81% of Indonesia's market share in 2024 and are expected to clock a 6.21% CAGR up to 2030. Their compact form, favorable financing, and multipurpose utility let SMEs meet urban drop densities and rural shuttle needs. Medium and heavy trucks still dominate revenue per-unit basis, serving mining and public works consignments where payload outweighs agility[1]“Commercial Vehicle Registration 2024,”, Ministry of Transportation (Dephub), dephub.go.id.

Urban gridlock incentivizes low-cab-over models that squeeze into under-3.5-m lanes; meanwhile, remote islands demand 4×4 chassis with snorkel kits and skid plates. The Indonesian commercial vehicle market size for light trucks expands further as courier networks push same-day promises. Wuling’s Formo Max, priced IDR 168–176 million, attracted hundreds of micro-enterprise buyers within the launch quarter[2]“Formo Max Specification Sheet,”, Wuling Motors Indonesia, wuling.id. Brand competition, therefore, shifts to holistic TCO rather than horsepower bragging rights.

By Propulsion Type: Electric Uptake Accelerates

Conventional engines captured 86.21% share in 2024, but electric derivatives posted the quickest 9.15% CAGR amid city emission curbs. Diesel keeps a stronghold in long-haul and quarry fleets because energy density and refueling speed remain unmatched.

In Indonesia, electric commercial vehicles are becoming increasingly popular, especially for urban deliveries. This surge is due primarily to carbon-conscious procurement policies and discounted off-peak charging tariffs from PLN, which enhance cost competitiveness. Due to these incentives, fleet operators are nearing total-cost-of-ownership parity, making electric vehicles more viable. Logistics giants are gravitating towards models like Mitsubishi’s eCanter, drawn not just by their operational efficiency but also the boost they provide to corporate social responsibility (CSR) visibility. With a blend of affordability, brand-enhancing, and sustainability credentials, these vehicles are emerging as prime choices for urban fleets.

By Transmission Type: Automatic Gains in Congested Cities

Manual boxes still dominate with an 83.52% market share, but automatic units grow 8.19% annually, driven by driver shortages and stop-and-go fatigue relief. Fleet owners calculate that smoother shifts save 2–3 minutes per delivery loop, translating to extra daily runs in Jakarta.

OEMs are now introducing torque converter and automated manual transmission (AMT) variants at slightly higher premiums than their manual counterparts. This pricing tactic is fostering wider acceptance, particularly in provincial capitals. Here, smoother driving reduces fatigue, benefiting both urban logistics and intercity transport. Yet, even with this trend, manual stick-shift transmissions continue to reign supreme in mining and rugged terrains. In these settings, where navigating steep grades and harsh conditions hinges on precise torque control, the demand leans towards mechanical simplicity and driver oversight, solidifying the manual gearbox's status as the top choice.

By Application: Logistics Commands Scale, Passenger Moves Fastest

Logistics and freight accounted for 43.47% of Indonesia's commercial vehicle market share in 2024, owing to e-commerce parcel flows and commodity haulage. Passenger use—tourist shuttles, intercity buses, ride-hailing vans—shows a 7.27% CAGR on urbanization and state subsidies for cleaner transit.

Electrification efforts begin with targeted pilots, particularly in airport shuttle operations, where predictable routes and depot-based charging make early adoption more feasible. These pilots are technology testbeds, allowing OEMs and operators to validate performance, charging logistics, and cost structures before scaling to broader applications.

Geography Analysis

Due to dense manufacturing clusters and superior tollway access, Java delivered 55.43% of Indonesia's commercial vehicle market size in 2024. Dealers hold deeper parts inventories and offer 24×7 service bays, translating into fleet uptime advantages.

Kalimantan’s 7.35% CAGR through 2030 reflects nickel and coal extraction boom feeding global battery chains. Chinese tipper trucks shipped CBU through Balikpapan now compete head-to-head with Japanese CKD units. Sumatra’s highway network further unlocks agricultural corridors, underscoring a rebalancing of the Indonesian commercial vehicles market across islands. Kalimantan’s mining tailwinds lift demand for 60-ton payload dumpers and heavy tractors hauling bauxite and coal to Samarinda loading docks[3]“Regional Mining Output 2024,”, Ministry of Energy and Mineral Resources, esdm.go.id. Remote terrain drives interest in durable 6×6 platforms with self-rescue winches. Local governments earmark IDR 25 trillion for road hardening, improving maintenance intervals, and uptime.

Sumatra completes the national triad by contributing robust agro-industrial flows. Palm-oil tankers run consistent routes between plantations and refineries, raising tank-truck churn. Emerging hotspots in Sulawesi and Eastern islands see modest but rising orders for minibuses under tourism stimulus, adding long-tail breadth to the Indonesian commercial vehicles market

Competitive Landscape

Japanese brands command a dominant share in Indonesia's commercial vehicle market, yet they face mounting pressure on their margins from swiftly rising Chinese competitors. Mitsubishi Fuso retains its leadership by offering value-added services like telematics, predictive maintenance, and round-the-clock rescue support, boosting fleet efficiency and ensuring customer loyalty. Concurrently, Hino carves out its tanker niche through strategic collaborations with Pertamina, securing fuel and lubricant contracts that bolster its standing. These developments highlight a segmented market where established players fend off intensifying pricing competition through service integration and strategic alliances.

Chinese entrants—Foton, Changan, JAC—exploit zero-down schemes and fully built imports that skip local bodywork. Dealer counts climbed from 40 to 94 between 2021 and 2024, mainly near mines. In response, Isuzu expanded mobile workshops to secondary cities and pitched five-year, unlimited-km warranties, unheard of five years ago.

Electric competition intensifies: Mitsubishi pilots 50 eCanters with PLN, BYD readies SKD assembly in Bekasi, and Foton pairs with Indomobil on sub-USD 30,000 mini-trucks. Success will hinge on local content compliance and charger coverage, both decisive levers in the Indonesian commercial vehicle market trajectory.

Indonesia Commercial Vehicle Industry Leaders

Hino Motors

Isuzu Motor

Daimler Commercial Vehicles Indonesia (Mercedes-Benz)

UD Trucks

Mitsubishi Fuso Truck & Bus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Nusatama Group proudly announces a significant step towards sustainable transportation. The company has collaborated with Norinco Vehicle, a prominent Chinese electric vehicle (EV) manufacturer. This partnership not only involves the supply of EV trucks but also designates Nusatama Group as the region's primary distributor.

- January 2024: Foton Motor, a leading truck manufacturer from China, has teamed up with Indomobil, a prominent automotive group in Indonesia, to spearhead the development of electric commercial vehicles in the archipelago. Under this strategic alliance, Indomobil will not only serve as the local distributor but also take on the role of assembler for Foton's electric trucks. Furthermore, Indomobil has ambitious plans to set up a local manufacturing hub, aiming to cater not just to Indonesia but also to the broader ASEAN market.

Indonesia Commercial Vehicle Market Report Scope

The Indonesia Commercial Vehicles Market Report is Segmented by Vehicle Type (Light Commercial Vehicles and More), Propulsion Type (Internal Combustion Engine and More), Transmission Type (Manual and Automatic), Application (Logistics and Freight, Mining and Construction, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Light Commercial Vehicles |

| Medium and Heavy-Duty Trucks |

| Buses and Coaches |

| Internal Combustion Engine (ICE) |

| Electric Vehicles |

| Manual |

| Automatic |

| Logistics and Freight |

| Mining and Construction |

| Passenger Transportation |

| Industrial Use |

| Others (FMCG, Waste Management, Utilities) |

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Nusa Tenggara |

| Maluku and Papua |

| By Vehicle Type (Value) | Light Commercial Vehicles |

| Medium and Heavy-Duty Trucks | |

| Buses and Coaches | |

| By Propulsion Type (Value) | Internal Combustion Engine (ICE) |

| Electric Vehicles | |

| By Transmission Type | Manual |

| Automatic | |

| By Application | Logistics and Freight |

| Mining and Construction | |

| Passenger Transportation | |

| Industrial Use | |

| Others (FMCG, Waste Management, Utilities) | |

| By Region | Java |

| Sumatra | |

| Kalimantan | |

| Sulawesi | |

| Nusa Tenggara | |

| Maluku and Papua |

Key Questions Answered in the Report

How large is the Indonesia commercial vehicles market in 2025?

It is valued at USD 11.32 billion and set to compound at 4.97% a year to 2030.

Which segment holds the biggest share of sales?

Light commercial vehicles account for 44.81% of 2024 registrations, capitalizing on e-commerce and SME demand.

Why do manual transmissions still dominate?

At 83.52% share, they remain cheaper to buy and simpler to maintain, traits prized by cost-sensitive fleets.

Which island is the fastest-growing sales region?

Kalimantan leads growth with a 7.35% CAGR on the back of mining and plantation logistics needs.

How intense is competition from Chinese brands?

In 2024, they boosted their market share with zero-down loans and ready-to-work imports, compelling Japanese incumbents to step up their after-sales service.

Page last updated on: