India Roadside Safety Barriers Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

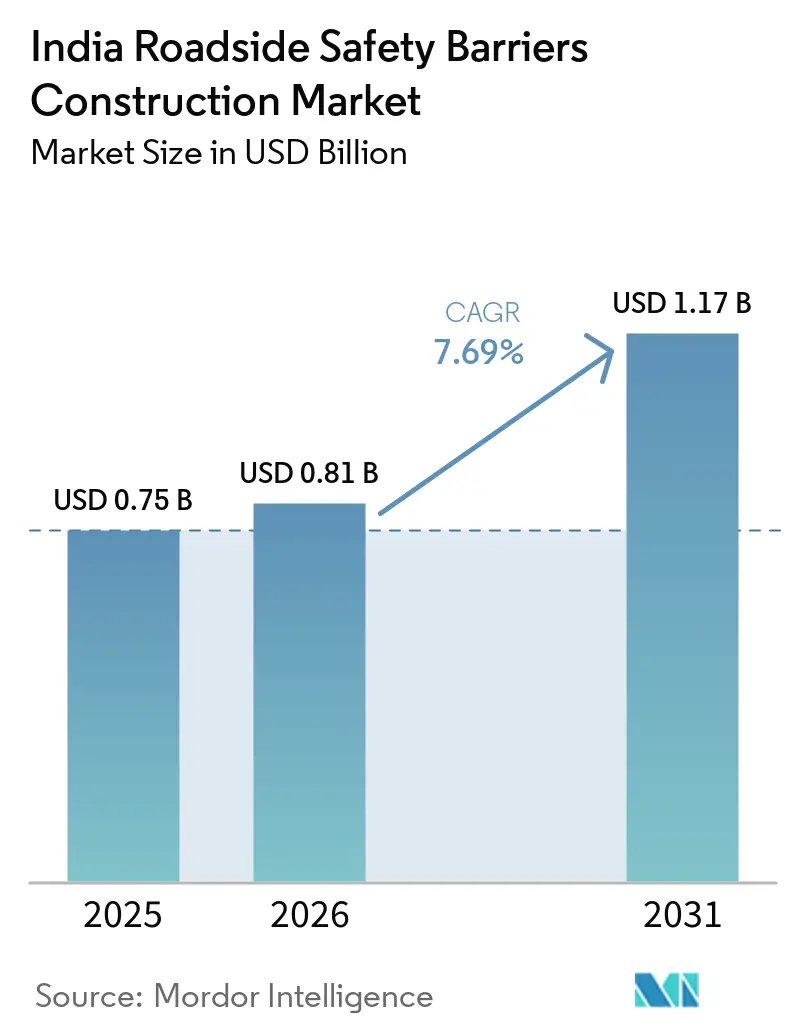

| Base Year Market Size (2025) | USD 0.75 Billion |

| Market Size (2026) | USD 0.81 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

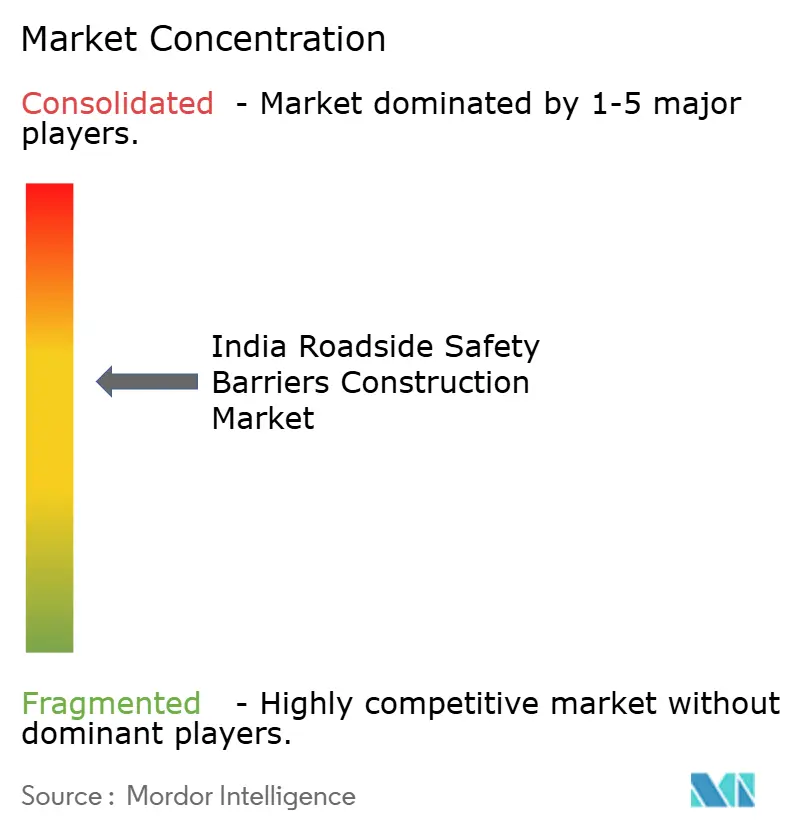

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Roadside Safety Barriers Construction Market Analysis by Mordor Intelligence

The India Roadside Safety Barriers Construction Market size was valued at USD 0.75 billion in 2025 and is estimated to grow from USD 0.81 billion in 2026 to reach USD 1.17 billion by 2031, at a CAGR of 7.69% during the forecast period (2026-2031). The development of expressways under the Bharatmala Pariyojana, stricter black-spot rectification regulations by the Ministry of Road Transport and Highways (MoRTH), and the adoption of Hybrid Annuity Model (HAM) and Engineering, Procurement, and Construction (EPC) contracts are collectively driving the annual demand for barriers. Developers are incorporating guardrails, crash cushions, and parapets into milestone-linked payments, ensuring timely installation and minimizing last-minute budget reductions. Additionally, mandatory crash-test certification from the National Automotive Testing and R&D Infrastructure Project (NATRAX) is enhancing product quality, shifting market share toward well-capitalized fabricators with ready stock and digital traceability systems. Domestic steel manufacturers have increased capacity, enabling major suppliers such as Utkarsh India and Shyam Metalics to offer competitive lead times. Meanwhile, the Directorate General of Trade Remedies (DGTR) safeguard investigation into flat steel imports may accelerate a gradual shift toward composites and bamboo-steel hybrid materials.

Key Report Takeaways

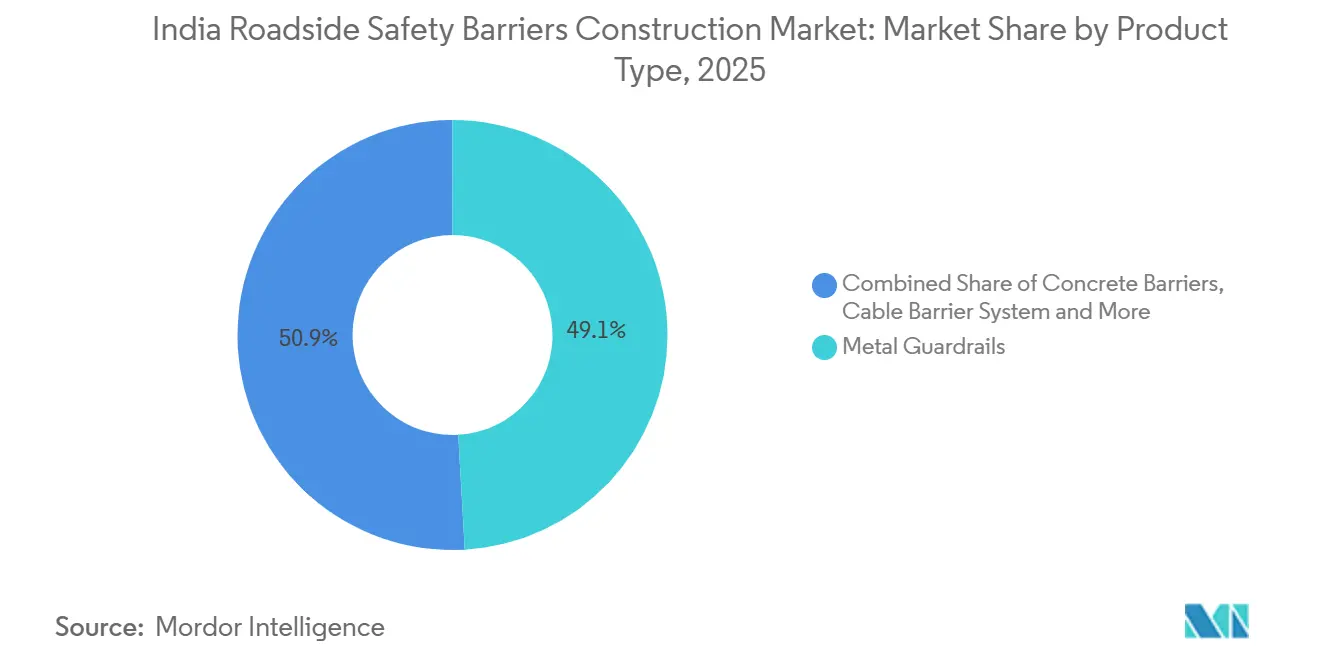

- By product type, Metal Guardrails captured 49.1% of the India roadside safety barriers construction market share in 2025, and Crash Cushions & Impact Attenuators are projected to grow at 8.19% CAGR between 2026 and 2031.

- By Material, Steel captured 60.9% of the India roadside safety barriers construction market share in 2025. Plastic & Composite materials are projected to grow at 8.08% CAGR between 2026 and 2031.

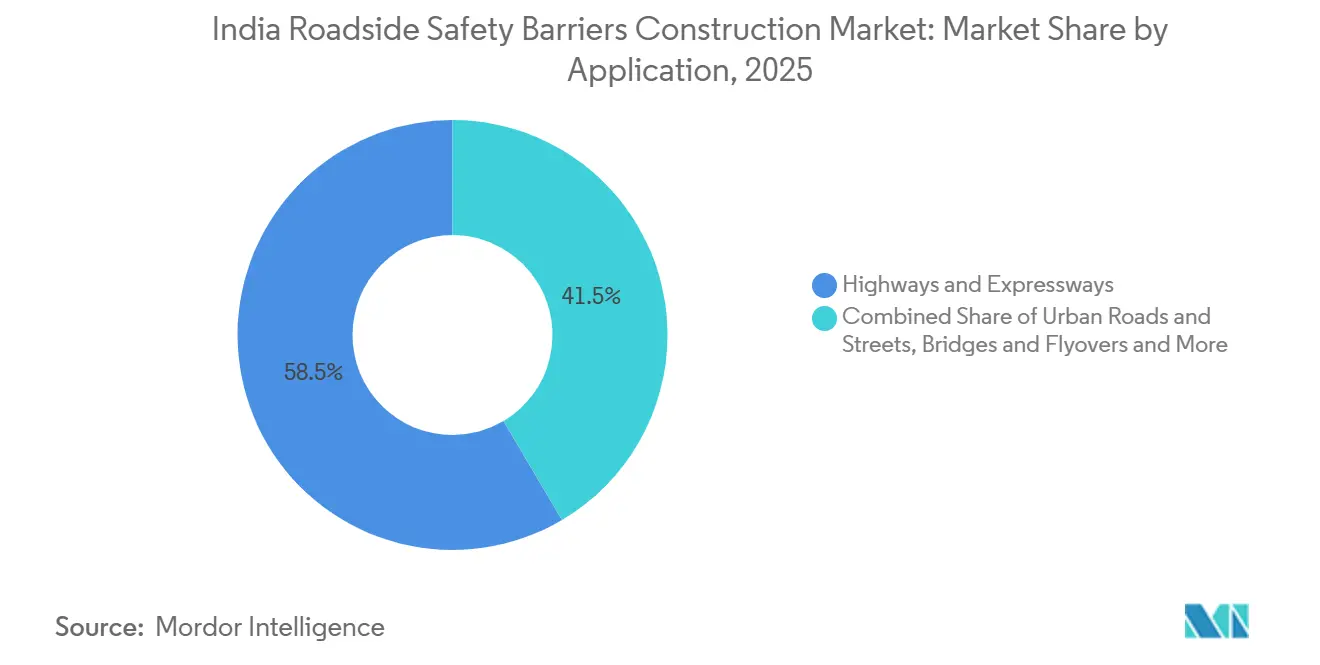

- By Application, Highways & Expressways captured 58.5% of the India roadside safety barriers construction market size in 2025, and Bridges & Flyovers are projected to grow at 8.31% CAGR between 2026 and 2031.

- By Installation, New Installation captured 72.3% of the India roadside safety barriers construction market size in 2025. Renovation/Retrofit/Repair is projected to grow at 7.98% CAGR between 2026 and 2031.

- By City, the Mumbai Metropolitan Region captured 19.1% of the India roadside safety barriers construction market share in 2025, and Hyderabad is projected to grow at 8.71% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Roadside Safety Barriers Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bharatmala, expressway, and access-controlled highway expansion | +2.3% | National, the highest in the Golden Quadrilateral states | Long term (≥ 4 years) |

| MoRTH and IRC compliance requirements for standardized barriers | +1.9% | Nationwide, first on National Highways | Medium term (2–4 years) |

| Black-spot rectification programs on hazardous stretches | +1.5% | High-fatality corridors such as NH-44 and NH-48 | Short term (≤ 2 years) |

| Rise in bridge, ghat-road, and elevated corridor construction | +1.2% | Hilly zones and the top six metro cities | Medium term (2–4 years) |

| HAM and EPC models linking payments to safety milestones | +0.9% | Bharatmala Phase-I and state highway upgrades | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Bharatmala, Expressway, and Access-Controlled Highway Expansion

The 34,800 km Phase-I scope under Bharatmala has significantly increased the demand for barriers, as each kilometer of a four-lane expressway requires approximately 2 km of median and roadside guardrails[1]Press Information Bureau, “Year End Review 2025 of Ministry of Road Transport & Highways,” pib.gov.in . The National Highways Authority of India (NHAI) plans to commission 23 expressways, spanning a total of about 7,800 km, by 2025. These expressways will feature full access control, necessitating continuous H2-rated thrie-beam systems at ramps, bridge approaches, and animal overpasses. Notable projects, such as the 1,380 km Delhi-Mumbai Expressway and the 343 km Bengaluru-Kadapa-Vijayawada corridor, highlight this shift, with barrier tonnage per route kilometer nearly doubling compared to older two-lane roads. With the national highway network expected to expand to 200,000 km by 2030, this growth is projected to sustain long-term demand for all types of roadside safety systems.

MoRTH and IRC Compliance Requirements for Standardized Barriers

Since 2024, the IRC:119-2015 crash-test certification has been a mandatory requirement for all highway projects exceeding USD 12 million. Contractors are required to provide NATRAX or EN 1317-2 test evidence before achieving payment milestones[2]Indian Road Congress, “IRC:119-2015 Guidelines for Traffic Safety Barriers,” indianroads.org . A directive issued by the NHAI in December 2024 further strengthened these requirements by mandating embossed batch identifiers and QR codes on every metal-beam element, enabling a digital audit trail. This development has excluded smaller mills lacking the budget for testing. Premium accredited suppliers, such as Utkarsh India, Prakash Asphalting & Toll Highways (PATH), and Valmont India, now dominate expressway orders due to their H2 crash reports, which facilitate faster concessionaire approvals. As more state public works departments implement similar requirements between 2026 and 2028, standardized and traceable safety hardware is expected to become the default specification in the market.

Black-Spot Rectification Programs on Hazardous Stretches

The Ministry of Road Transport and Highways (MoRTH) has identified 13,795 accident black spots across the country and approved improvements at approximately 10,000 locations by March 2025. These improvements primarily involve the installation of guardrails, crash cushions, and rumble strips. Guardrails, costing only USD 27 per running meter based on current schedule-of-rates values, are the most cost-effective safety measure for single-carriageway highways. For FY 2025-26, the ministry aims to address an additional 1,000 black spots and conduct 40,000 km of road safety audits, ensuring a consistent demand for retrofitting work by fabricators over the next two years. However, limited federal safety budgets mean that many projects rely on state co-funding and World Bank loans, which can delay contract awards.

Rise in Bridge, Ghat-Road, and Elevated Corridor Construction

Demand for edge-protection systems is increasing due to the construction of new viaducts, bored tunnels, and ghat realignments. The Bengaluru–Mysuru highway, for instance, features nine major bridges and 44 minor spans, all equipped with concrete or steel H2/H3 parapets. Mountain roads in regions such as the Western Ghats and Himalayas require specialized three-beam guardrails with enhanced lateral stiffness. This demand is addressed by PATH’s proprietary design, which has been installed along more than 130 km of hill roads in Himachal Pradesh and Mizoram. Additionally, urban flyovers, such as the 8.9 km Indora-Dighori project in Nagpur, are adopting ultra-high-performance fiber-reinforced concrete parapets. These parapets offer slimmer profiles and reduced life-cycle costs, contributing to a more diverse product mix in China.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-sensitive state road projects are limiting higher-spec systems | –0.8% | Bihar, Jharkhand, Uttar Pradesh, Odisha, Madhya Pradesh | Medium term (2–4 years) |

| Inconsistent installation quality and maintenance | –0.6% | Nationwide, severe conditions on state and rural roads | Long term (≥ 4 years) |

| Approval delays and fragmented execution across agencies | –0.5% | National Highways intersecting forest and urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost-Sensitive State Road Projects Limiting Higher-Spec Systems

Several financially constrained states continue to award contracts based solely on the lowest price, accepting underweight W-beam rails as thin as 2.5 mm and omitting galvanization to reduce costs by 15-20%[3]West Bengal Public Works Department, “Schedule of Rates 2022-23,” westbengalpwd.gov.in . Limited central safety funding—amounting to just 0.2% of MoRTH’s 2025 allocation—prevents the adoption of premium three-beam or cable solutions on many state highways, despite high fatality rates. Unless states allocate dedicated budgets for crash barriers or implement QR-code traceability similar to NHAI, a dual-quality market is likely to persist until at least 2028.

Inconsistent Installation Quality and Maintenance

Field audits indicate that up to 30% of installed barriers deviate from their design specifications due to issues such as shallow post embedment, missing reflectors, or untorqued fasteners. Although the National Highways Authority of India (NHAI) conducts reinspections of flagship corridors, such as Bengaluru-Mysuru, within months of their opening, most state highways lack dedicated maintenance contracts. While 45,000 km of national corridors are covered under performance-based maintenance agreements, the significantly larger state highway network depends on ad-hoc repairs. This approach allows corrosion to reduce containment capacity by half, undermining public trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Metal Guardrails Keep the Lead While Crash Cushions Accelerate

In 2025, metal guardrails accounted for 49.1% of the India roadside safety barriers construction market, driven by their low installation cost of approximately USD 27 per meter and crash-tested performance suitable for four-lane highways. Major fabricators, such as Utkarsh India, supply up to 500 km of W- or thrie-beam guardrails monthly, enabling EPC contractors to complete entire projects without relying on overseas procurement. Frequent expressway contracts sustain the demand for bulk steel rails, black-spot retrofitting projects, and Indian Railways parallel-track developments. Additionally, the introduction of digital QR coding facilitates on-site compliance verification by inspectors.

The crash cushion and impact attenuator segment is the fastest-growing category, projected to achieve a CAGR of 8.19% by 2031. This growth is supported by the National Highways Authority of India's (NHAI) mandate for energy-absorbing devices at toll plazas, median openings, and ramp gores. International suppliers, such as Valtir’s QuadGuard, compete with domestic manufacturers like Dhawal Safety India, prompting increased local investment in crash testing. Since attenuators contribute only 1-2% to overall civil costs while significantly reducing the severity of collisions, concessionaires are increasingly incorporating them early in Hybrid Annuity Model (HAM) bids. Over time, stricter enforcement of IRC: SP:84-2019 guidelines may shift the market share from purely steel rails to integrated systems that combine cushions and terminal treatments into certified solutions.

By Material: Steel Dominates but Composites Gain Traction

Steel accounted for 60.9% of the India roadside safety barriers construction market in 2025, supported by 16 million tons of new capacity from JSW Steel, which ensured steady coil availability despite global price increases. Additionally, ResponsibleSteel-certified meltshops enable builders to secure sustainability credits under the new federal tender scoring system. Tier-one fabricators maintain stocks of Fe360/Fe410 rails in 2.8-3.0 mm gauges and have integrated embossing, bending, and galvanizing processes under one facility, reducing lead times to less than one week for highway packages.

However, plastic and composite materials are projected to grow at the fastest rate, with a CAGR of 8.08% through 2031. PATH has already implemented an automated pultrusion line for producing glass-fiber-reinforced polymer (GFRP) rebars, capable of manufacturing 40,000 running meters daily. Furthermore, the installation of the world’s first bamboo-steel hybrid barrier on Maharashtra’s Vani–Warora highway in 2023 demonstrated that natural fibers can meet NATRAX impact test standards while reducing embodied carbon by 50%. If the Directorate General of Trade Remedies (DGTR) imposes anti-dumping duties on flat steel imports, concessionaires may expedite the adoption of bio-composites, particularly for greenfield projects with environmental performance requirements.

By Application: Highways Dominate, Bridges Prove the Growth Story

Highways and expressways accounted for 58.5% of the projected 2025 expenditure, driven by the Bharatmala initiative, which added over 5,600 km of new national highways in a single fiscal year. The implementation of continuous three-beam lines along the 1,380 km Delhi-Mumbai Expressway and the 343 km Bengaluru-Kadapa-Vijayawada corridor highlights how greenfield expressways require approximately two kilometers of guardrail steel for every kilometer of pavement, significantly increasing baseline demand.

Bridges and flyovers are expected to experience the fastest growth, with a projected CAGR of 8.31% through 2031, supported by large-scale projects in Karnataka and Maharashtra, as well as 8-9 km urban viaducts in cities like Nagpur and Pune. Unlike flat highways, elevated structures necessitate H2/H3 containment levels or ultra-high-performance concrete parapets. This added complexity benefits specialist suppliers capable of designing seamless transitions between flexible steel and rigid concrete, minimizing snag points. Such expertise enhances margins despite the lower tonnage requirements compared to extended highway projects.

By Installation Type: New Projects Still Rule, but Retrofit Budgets Are Climbing

New installations accounted for 72.3% of the 2025 deployment, as each new kilometer constructed under the Bharatmala program or the 10-project bundle approved in February 2026 requires guardrails before the commercial operation date (COD). The 15-year maintenance clause under the Hybrid Annuity Model (HAM) incentivizes concessionaires to prioritize higher specifications during initial construction to minimize mid-cycle repair needs.

Retrofitting and repair activities are increasing, driven by 13,795 recorded black spots, with a forecasted compound annual growth rate (CAGR) of 7.98% through 2031. Projects such as NH-22 Zirakpur–Parwanoo explicitly allocate funds for “repairing/providing” missing barriers, indicating a sustained aftermarket demand. State highways, which account for 60% of road fatalities but have limited existing protective infrastructure, present significant opportunities. Even a modest increase in budget allocations could lead to numerous retrofit contracts for mid-sized local fabricators over the forecast period.

Geography Analysis

Barrier spending is most concentrated in the Mumbai Metropolitan Region, accounting for 19.1% of the projected 2025 expenditures. This is driven by infrastructure projects such as coastal expressways, metro lines, and four-level interchanges, which limit space for bulky steel rails and promote the adoption of concrete parapets and tensioned-cable systems. Delhi NCR follows closely, supported by the 1,380 km Delhi-Mumbai Expressway. Maintenance teams for this expressway are already planning phased retrofits for damaged three-beam segments and animal-overpass transitions. Pune and Nagpur collectively contribute a significant double-digit share, as the state highway authority prioritizes elevated corridors that utilize ultra-high-performance fiber-reinforced concrete side walls to reduce construction time and minimize repainting requirements.

Southern India is experiencing the fastest growth in barrier demand. Hyderabad is leading with a CAGR of 8.71%, driven by the Hybrid Annuity upgrade of the Hyderabad–Panaji corridor and the second-ring expansion, which effectively doubles the city’s fenced transport network. Bengaluru benefits from four Guinness World Record paving stretches, all of which incorporate QR-coded rails across 17 interchanges. Meanwhile, Chennai, nearing completion of its Bengaluru expressway connection, sources significant quantities of W-beam barriers from regional mills in Tamil Nadu. The eastern region is also witnessing notable activity. Jindal (India) Limited’s twin crash-barrier facilities in Howrah secured USD 36 million in orders across West Bengal and Assam in FY 2025. This reflects growing demand along the NH-12 and Siliguri corridors, which are being expanded to four lanes.

Hill states represent a niche but technically challenging market. Himachal Pradesh’s ghat roads feature modified three-beam rails, while Mizoram’s bridge-heavy alignments are testing composite parapet solutions due to the high cost of steel transport. While absolute spending remains concentrated in four major urban hubs, growth momentum is increasingly decentralized. Capacity expansions in locations such as Sambalpur, Giridih, and Ranihati are expected to meet nearby demand, ensuring a broader distribution of infrastructure investments.

Competitive Landscape

The competitive landscape in the steel industry is structured across three tiers. Integrated steel producers, such as Tata Steel Long Products and JSW Steel, leverage captive coil production to secure ResponsibleSteel certifications. This serves as a key differentiator, particularly as federal bids will begin incorporating sustainability criteria starting in 2026. Mid-tier specialists, including Utkarsh India, Shyam Metalics, and Pinax Steel, dominate National Highways Authority of India (NHAI) approvals by financing full-scale crash tests at NATRAX and maintaining 5,000-10,000 MT of finished inventory. This inventory allows EPC contractors to access materials on short notice. At the installer level, companies like Larsen & Toubro and G R Infraprojects are bundling supply, erection, and 15-year operations and maintenance (O&M) clauses, ensuring stable margins over the asset lifecycle.

Recent strategic initiatives highlight the growing scale of operations. Shyam Metalics has commissioned a 24,000 MT plant in Giridih and plans to invest an additional USD 6 million in a 60,000 MT facility in Sambalpur, aiming for a 10% domestic market share and exports to the Gulf region. Jindal (India) has increased its production capacity by 75% and doubled its crash-barrier revenue to account for 8-10% of total group sales, indicating that demand in the eastern region justifies dedicated production lines. Vibhor Steel Tubes has launched a greenfield mill in Odisha and secured USD 2.26 million in new barrier contracts as of December 2025, demonstrating opportunities for new entrants in the market.

Technological advancements are creating a clear divide among market players. Tier-one producers are embossing QR codes on each rail, linking them to site-specific standard operating procedures (SOPs) to comply with the NHAI traceability mandate effective December 2024. These players are also experimenting with bamboo-steel and glass fiber-reinforced polymer (GFRP)-steel hybrids to mitigate raw steel price volatility. In contrast, cost-sensitive state tenders continue to accept uncertified 2.5 mm rails, sustaining a shadow market where over 20 micro-fabricators operate. As regulatory enforcement extends from national highways to state roads, this informal segment is expected to contract, potentially increasing the combined market share of the top ten producers to significantly above the current 60%.

India Roadside Safety Barriers Construction Industry Leaders

Tata Steel Long Products

Utkarsh India Ltd.

Pinax Steel Industries

Hill & Smith India

Valtir (Trinity Highway Products India)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Ministry of Road Transport & Highways approved the 80-kilometer Hyderabad-Panaji highway corridor (National Highway-167) project worth Rs. 3,175 crore (USD 381 million) under Hybrid Annuity Mode. This project will require approximately 160 kilometers of crash barriers along both sides of the highway, plus additional crash cushions at toll plazas and interchanges.

- February 2026: The 8.9 kilometer Indora-Dighori Flyover in Nagpur reached 73% completion. The Rs. 998 crore (USD 120 million) project uses Ultra-High Performance Fiber-Reinforced Concrete (UHPFRC) parapets for edge protection instead of traditional steel guardrails, showing a trend toward premium barrier materials on urban elevated roads.

- January 2026: The 343-kilometer 5.3-kilometer Bengaluru-Kadapa-Vijayawada Economic Corridor (National Highway-544G) was completed, setting four Guinness World Records for construction speed. The project includes 17 interchanges, 10 wayside amenities, and a 5.3 kilometer tunnel—all requiring continuous crash barrier installation for safety. The project was built by NHAI and concessionaire M/s Rajpath Infracon Pvt. Ltd.

- December 2025: Vibhor Steel Tubes Limited commissioned (started operations at) a new greenfield manufacturing facility in Sundargarh, Odisha to produce metal crash barriers. This facility will help the company serve highway projects in Eastern and Central India more efficiently.

India Roadside Safety Barriers Construction Market Report Scope

| Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) |

| Cable Barrier Systems |

| Crash Cushions & Impact Attenuators |

| Others (Motorcyclist protection systems, hybrid/specialty barriers, emerging safety solutions) |

| Steel |

| Concrete |

| Plastic & Composite |

| Others (Aluminum, rubber-based materials, composite blends, recycled materials) |

| Highways & Expressways |

| Urban Roads & Streets |

| Bridges & Flyovers |

| Others (Rural roads, industrial/private roads, parking areas, tunnels, temporary traffic zones) |

| New Installation |

| Renovation / Retrofit / Repair |

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Chennai |

| Kolkata |

| Rest of India |

| By Product Type | Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) | |

| Cable Barrier Systems | |

| Crash Cushions & Impact Attenuators | |

| Others (Motorcyclist protection systems, hybrid/specialty barriers, emerging safety solutions) | |

| By Material | Steel |

| Concrete | |

| Plastic & Composite | |

| Others (Aluminum, rubber-based materials, composite blends, recycled materials) | |

| By Application | Highways & Expressways |

| Urban Roads & Streets | |

| Bridges & Flyovers | |

| Others (Rural roads, industrial/private roads, parking areas, tunnels, temporary traffic zones) | |

| By Installation Type | New Installation |

| Renovation / Retrofit / Repair | |

| By Cities | Mumbai Metropolitan Region |

| Delhi NCR | |

| Pune | |

| Bengaluru | |

| Hyderabad | |

| Chennai | |

| Kolkata | |

| Rest of India |

Key Questions Answered in the Report

How fast is the India roadside safety barriers construction market expected to grow through 2031?

Market turnover is projected to rise from USD 0.81 billion in 2026 to USD 1.17 billion by 2031, implying a 7.69% CAGR.

Which product dominates current demand?

Metal guardrails led with 49.1% share in 2025 because they remain the most cost-effective and crash-tested option for four-lane highways.

Where is the quickest regional growth likely to occur?

The Hyderabad region should post the fastest 8.71% CAGR as new HAM corridors and an outer-ring-road expansion double its fenced network length.

Why are crash cushions attracting attention?

NHAI now prescribes impact attenuators at toll plazas and median openings, lifting crash cushion demand at an expected 8.19% CAGR up to 2031.

How are regulations shaping supplier selection?

Since December 2024, every metal-beam rail must carry QR-coded traceability and NATRAX crash-test proof, consolidating orders among accredited manufacturers.

Page last updated on: