China Roadside Safety Barriers Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

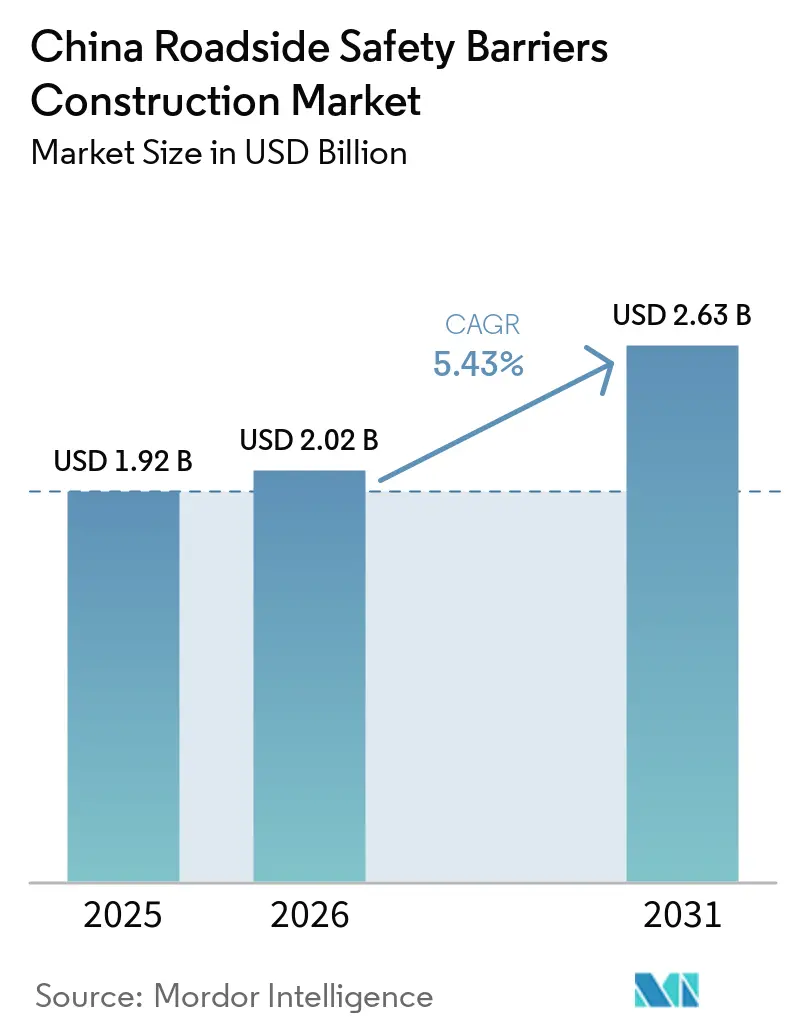

| Base Year Market Size (2025) | USD 1.92 Billion |

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.63 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

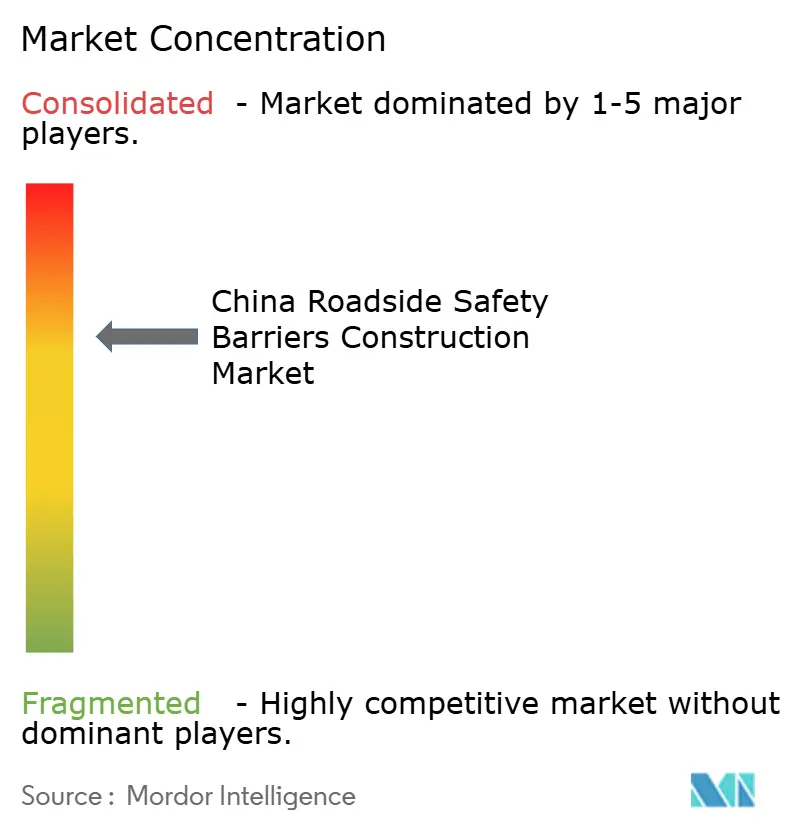

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Roadside Safety Barriers Construction Market Analysis by Mordor Intelligence

The China Roadside Safety Barriers Construction Market size is projected to be USD 1.92 billion in 2025, USD 2.02 billion in 2026, and reach USD 2.63 billion by 2031, growing at a CAGR of 5.43% from 2026 to 2031. National expressway expansion, a growing vehicle fleet, and mandatory compliance with the new GB/T 31439-2025 crash-test standards are the key drivers of this consistent growth. Provincial budgets continue to support large-scale civil projects, as the 14th Five-Year Plan allocated over USD 2.58 trillion for transport infrastructure, ensuring steady, multiyear demand for new guardrails and retrofit initiatives. While advanced cable and composite systems are being introduced in specific corridors, conventional metal guardrails remain the foundation of the roadside safety barriers construction market in China due to the widespread availability of compatible installation equipment among contractors. Competition is increasing as both domestic and international suppliers strive to certify higher-grade steels and smart, sensor-enabled barrier systems.

Key Report Takeaways

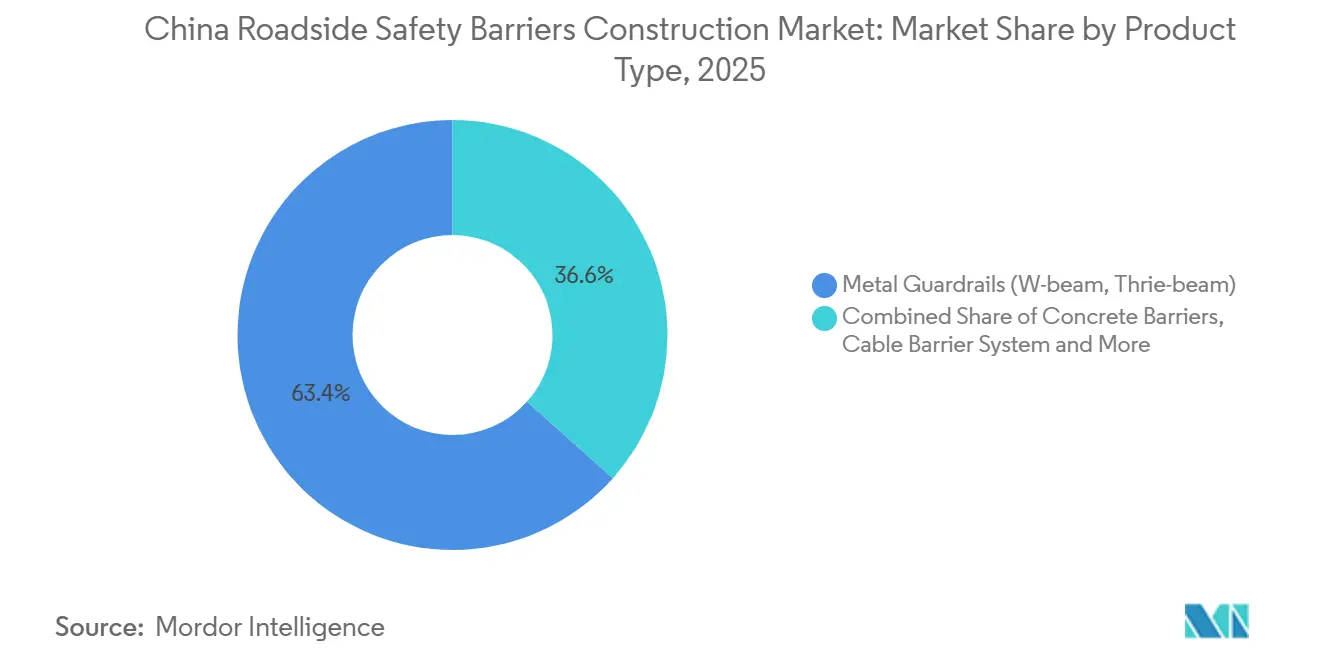

- By product type, metal guardrails captured 63.4% of the China roadside safety barriers construction market share in 2025, while cable barrier systems are projected to expand at a 6.05% CAGR between 2026 and 2031.

- By material, steel commanded 70.3% share of 2025 spending, whereas fiber-reinforced polymer composites are forecast to register a 6.21% CAGR between 2026 and 2031.

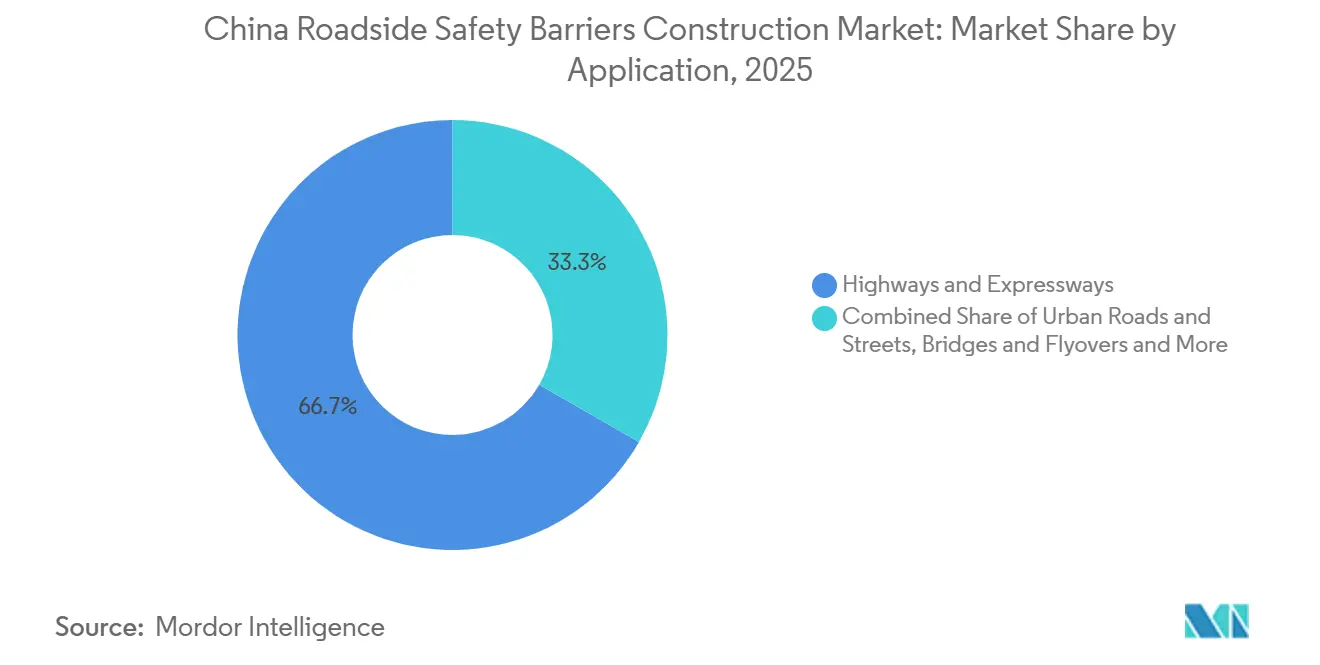

- By application, highways and expressways accounted for 66.7% of the 2025 market, yet bridge and flyover installations are expected to advance at a 6.35% CAGR between 2026 and 2031.

- By installation type, new projects represented 71.2% of the 2025 China roadside safety barriers construction market size, but retrofit activity is on track for a 5.89% CAGR between 2026 and 2031.

- By city, Beijing led with 19.8% of 2025 demand, while Chengdu is anticipated to post the fastest 6.58% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Roadside Safety Barriers Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of national expressways and intercity highway networks | +1.5% | Nationwide, peak activity in Hebei, Sichuan, Guangdong, and Hunan | Medium term (2–4 years) |

| Strong government emphasis on road-safety upgrades | +1.3% | Nationwide, early adopters in Beijing, Shanghai, and Guangzhou | Short term (≤ 2 years) |

| Rising vehicle ownership and traffic volumes | +1.0% | 103 cities with >1 million vehicles | Medium term (2–4 years) |

| Growth of freight corridors and industrial transport routes | +0.8% | Chongqing–Chengdu, Yangtze River Delta | Long term (≥ 4 years) |

| Modernization of existing highways with higher-grade safety systems | +0.7% | Retrofit focus in Shanxi, Guizhou, Henan, Fujian | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of National Expressways and Intercity Highway Networks

China achieved record-high expansions of high-speed roadways in 2025, with projects already funded for 2026-2028 expected to sustain installation activities. In Hebei province alone, over USD 16.9 billion is allocated for new road construction next year, driving demand for barriers across six ongoing and seven new expressway sections. New lanes require continuous median and shoulder protection, meaning that each kilometer of roadway constructed directly correlates to increased demand for guardrails or cable systems. Provinces predominantly opt for standard W-beam barriers due to their proven crashworthiness, while flexible multi-rope cable solutions are increasingly specified for long, sweeping curves. This steady project pipeline provides manufacturers with clear volume forecasts, prompting them to localize production near emerging expressway hubs[1]Ministry of Transport, “GB/T 31439-2025 Guardrail Specification,” mot.gov.cn .

Strong Government Emphasis on Road-Safety Upgrades

GB 5768.9-2025, set to take effect in 2026, strengthens national regulations for traffic devices in accident-prone areas and increases the minimum crash-worthiness standards. Several provinces have promptly allocated funds for guardrail retrofits. Guizhou, Henan, Shanxi, and Fujian collectively spent over USD 5.5 million to replace sub-standard guardrails on critical expressways. Shanxi has taken an additional step by introducing DB 14/T 3328-2025, a local specification for low-carbon alloy steel, designed to ensure a service life of 25-30 years for new installations. Stricter barrier regulations are closely tied to reduced fatality targets, leading to robust enforcement and making compliance a mandatory criterion for bids. Suppliers with pre-certified products now hold a competitive advantage in provincial tenders[2]Ministry of Industry and Information Technology, “GB 5768.9-2025 Technical Standard,” miit.gov.cn .

Rising Vehicle Ownership and Traffic Volumes

China's registered automobile stock reached 366 million units in 2025, of which over 43 million were heavy battery-electric vehicles, which impose greater impact loads on roadside structures. Urban corridors around cities such as Beijing and Chengdu require reinforced Thrie-beam or cable systems to handle the increased traffic volume and speeds. The Jingxiong Expressway serves as a prominent example, utilizing an intelligent precast beam line alongside upgraded SB-grade barriers to reduce lane-closure durations and mitigate congestion. As provincial safety budgets are aligned with vehicle registrations, the regions with the highest vehicle densities receive priority for barrier upgrades, creating a cycle that drives consistent replacement demand.

Growth of Freight Corridors and Industrial Transport Routes

Dedicated truck lanes along the Chongqing-Shenzhen and Shandong east-west corridors are now accommodating larger and heavier cargo, requiring designers to test barriers against 18-ton vehicles traveling at 60 kilometers per hour. Hebei's plan to retire 10,000 old diesel trucks and introduce 5,000 electric heavy trucks by 2026 is expected to increase the average curb weight. Freight logistics companies are advocating for expedited project timelines, leading contractors to prefer modular steel or composite systems, which can be installed two to three times faster than traditional cast-in-place concrete. Consequently, the China roadside safety barriers construction market is directly benefiting from logistics policies aimed at alleviating bottlenecks in inland freight channels[3]Ministry of Commerce of the People’s Republic of China, “Hebei to Build Zero-Carbon Freight Corridors in 2026,” mofcom.gov.cn.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs of installing and maintaining advanced barrier systems | -0.6% | Mostly Tier-3 cities and rural roads | Short term (≤ 2 years) |

| Pricing pressure in large-scale public road projects | -0.5% | Provincial tenders nationwide | Medium term (2–4 years) |

| Regional inconsistency in material quality and installation practices | -0.3% | Provinces with fragmented contractor bases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Costs of Installing and Maintaining Advanced Barrier Systems

Smart cables or composite barriers are 15-40% more expensive per kilometer than traditional galvanized steel, posing a challenge for counties with limited capital budgets. Despite their greater energy-absorption capacity, decision-makers often prioritize immediate needs, such as resurfacing or bridge repairs, over the higher upfront costs. Operating expenses are also higher, as tensioned wire-rope lines require calibrated retensioning, and sensor-equipped modules incur server fees and periodic software updates. Additionally, recent increases in rebar and wire prices have affected fixed-price contracts signed in 2024, leading several local agencies to postpone upgrades by 1 or 2 fiscal years. Without changes to subsidy formulas that account for lifecycle savings, these premium solutions are likely to remain limited to high-profile corridors.

Pricing Pressure in Large-Scale Public Road Projects

In most provinces, barrier construction projects are still awarded to the lowest qualified bidder, leading to compressed profit margins, often in the single digits, for large-scale projects such as the 176-kilometer Weizou Expressway. The absence of a material-price-escalation clause places the risk of raw steel price volatility on suppliers, making them hesitant to propose innovative but more expensive designs. Consequently, suppliers may reduce steel grades or coating thicknesses after securing contracts, negatively impacting long-term performance. While contractors with extensive vertical integration can absorb these pressures, smaller, design-focused innovators often avoid tendering altogether, hindering the adoption of new technologies. Unless bidding criteria shift to prioritize total cost of ownership, price competition will continue to limit profitability in the construction market for roadside safety barriers in China.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Metal Guardrails Anchor Demand, Cable Lines Accelerate

Metal guardrails accounted for 63.4% of the China roadside safety barrier market share in 2025 and remain the standard choice for most new expressway projects. These W-beam and Thrie-beam units are manufactured from Q235B or Q355B steel and are compatible with the post-pounding equipment commonly used by contractors. With replacement installations achievable at a rate of 250-350 meters per crew-day, these guardrails are considered cost-effective and schedule-efficient by agencies. Ongoing supplier investments in thicker zinc-aluminum coatings and precise pre-punched slot tolerances have significantly reduced corrosion-related issues, further solidifying metal guardrails' dominance in the market.

Cable systems represent the fastest-growing sub-segment, with a projected compound annual growth rate (CAGR) of 6.05% through 2031. Their flexibility makes them particularly suitable for tight curves and narrow medians. Multi-rope arrays can withstand higher-energy impacts and can be quickly repaired after collisions by retensioning the wires rather than replacing damaged panels. Products such as Trinity Highway’s ArmorWire and Valmont’s ArmorGuard portable sections have successfully passed MASH TL-4 tests, providing provinces with reliable options for freight corridors. Although the initial capital cost per meter is approximately 20% higher than that of W-beam guardrails, lifecycle studies indicate repair costs are 15-20% lower, making cable systems an attractive choice for areas where minimizing lane closures is a priority.

By Material: Steel Dominates While Composites Capture Trials

Steel accounted for 70.3% of the China roadside safety barrier construction market in 2025 due to its consistent quality and compliance with GB/T 31439-2025 mechanical standards. Q355B sections, with a yield strength of 422 megapascals, are now priced only 3% higher than Q235B, leading more provinces to adopt the stronger grade. Additionally, zinc-aluminum-magnesium coatings extend the time-to-red-rust by 30% compared to pure zinc, reducing the frequency of repainting. These advancements ensure that steel remains a key component in transport agencies' procurement budgets.

Composites are projected to grow at a CAGR of 6.21% through 2031, driven by their non-corrosive properties, 25% higher impact absorption, and up to 30% lighter weight compared to steel, which simplifies logistics in mountainous regions of western China. Fiber-reinforced polymer posts were first used on the double-deck Shiziyang Link, where high salt-spray levels would typically cause metal corrosion. Pilot contracts often include 5-kilometer test sections to evaluate wear before broader adoption. If durability results continue to be favorable, the market share of composites could increase significantly, particularly for coastal bridges and tunnels where corrosion-related costs are higher.

By Application: Expressways Rule, Bridge Projects Gain Pace

Highways and expressways accounted for 66.7% of application demand in 2025, highlighting the strong correlation between new lane construction and barrier procurement. Each kilometer of newly constructed roadway requires two parallel safety barriers, prompting contractors to secure W-beam inventory months in advance of pavement installation. Additionally, the inclusion of built-in shoulder widths on new routes accommodates portable crash cushions and impact attenuators, which were less common a decade ago, thereby increasing accessory spending per kilometer.

Bridge and flyover projects represent the fastest-growing segment, with a projected CAGR of 6.35% through 2031. Large-scale structures, such as the 2,180-meter-span Shiziyang Link, are transitioning from tower construction to deck completion. These double-deck designs require transition barriers between upper and lower traffic levels and often include composite or movable median units to manage reversible-lane traffic. This complexity increases the average barrier value per meter by 25-35% compared to flat-grade sections, creating significant revenue opportunities for suppliers with specialized molds and curved post templates.

By Installation Type: New Projects Lead, Retrofits Gather Steam

New construction accounted for 71.2% of the China roadside safety barriers construction market size in 2025, driven by ongoing efforts in provinces to complete the national expressway grid. Contractors coordinate guardrail installations with paving crews to expedite lane openings, with the standard W-beam meeting strict commissioning deadlines. However, retrofit activities are growing at a compound annual growth rate (CAGR) of 5.89%, supported by life-extension mandates from the Ministry of Transport, which aim to achieve a maximum defect ratio of 2% by 2026.

Retrofit projects increasingly specify low-carbon alloy steel with nano-epoxy coatings to achieve a 25-year design life, effectively doubling the replacement interval. Hebei’s pilot recycling program has shown that old posts can be re-rolled into spacer blocks, reducing the carbon footprint by up to 15% and fostering a secondary steel market. As environmental scorecards become part of bid evaluations, retrofit contractors capable of certifying recycled materials may gain a competitive advantage.

Geography Analysis

In 2025, Beijing accounted for 19.8% of China's market share for roadside safety barrier construction. This was largely due to the city's allocation of central subsidies to high-visibility projects such as the Jingxiong Expressway Phase II. This 12.5-kilometer corridor, with 70% of its length elevated, required custom deck-to-ramp transition barriers and prefabricated beam cages to minimize nighttime closures. Additionally, Beijing has been piloting smart incident-detection platforms, reducing emergency response times to under two minutes and setting a performance benchmark for other cities.

Shanghai, Guangzhou, and Shenzhen form a mature coastal triangle characterized by replacement-heavy demand. Shanghai’s 17-kilometer double-deck Zhoudeng Expressway, set for completion in 2026, will feature movable median barriers, enabling operators to reverse all six lanes on one deck during typhoon evacuations. Guangzhou’s recently completed Yanta Bridge employs SB-grade median units on universal wheels, allowing a two-person crew to reposition them within 120 seconds. This highlights the growing political support for movable systems. Furthermore, these coastal cities are conducting composite material trials in sea-spray corridors, where steel coatings are prone to rapid degradation.

Chengdu is projected to achieve the fastest market growth, with a 6.58% CAGR forecast through 2031. This growth is driven by major projects such as the 240-kilometer Chengnan expansion and the ongoing 337-kilometer Chengdu–Chongqing freight corridor, which is being widened from four to eight lanes. In 2025, Sichuan province added over 500 kilometers of expressway, incorporating Thrie-beam barriers rated for 18-ton trucks on mountain descents. Western provinces, which often rely on night-shift construction to maintain daytime traffic flow, are increasingly adopting modular cable or composite segments that can be replaced within a single closure window. Additionally, Chengdu's strategic focus on integrating advanced safety technologies and materials into its infrastructure projects further supports its rapid market growth.

Outside major urban hubs, Tier-3 provinces continue to prioritize cost, resulting in the extended use of older W-beam barriers beyond their design life. However, the Ministry's 98% intactness rule is expected to accelerate the replacement of these outdated systems, bringing them into compliance before 2030.

Competitive Landscape

Domestic manufacturers such as Shandong Guanxian Huiquan, HuaAn Traffic Facilities, and Wuhan Dachu compete alongside multinational subsidiaries like Valmont China, Trinity Highway Suzhou, and Hill & Smith Barrier Shanghai. The updated GB/T 31439-2025 standards, which require higher energy absorption, provide an advantage to firms with in-house crash test rigs and MASH certifications. For instance, Shandong Guanxian Huiquan has invested USD 20 million in a static-dynamic rig capable of simulating car impacts at 110 kilometers per hour, reducing certification lead times by 30 days.

To remain competitive, companies are focusing on vertical integration, digitalization, and lifecycle-service offerings. Henan Transportation Investment Group’s new plant, with a capacity of 160,000 tons per year, integrates panel pressing, hot-dip galvanizing, and epoxy-powder topcoating, thereby reducing logistics time. Tongxingbao Holdings has signed a USD 39 million digital transformation contract to incorporate cloud analytics into barriers, enabling agencies to access live condition dashboards. Additionally, Hunan’s Transport Science Research Institute has invested USD 2.1 million in a vehicle-road-cloud start-up to develop sensors that self-report impact severity and location, a feature now included in select bridge decks.

Price competition remains a key factor in procurement, underscoring the importance of scale as a critical advantage. Valmont’s Ezy-Guard line features knock-down posts that allow 30% more meters to be shipped per container, reducing freight costs for remote western locations. Trinity Highway utilizes its Suzhou MASH test corridor to localize ArmorWire content above 65%, avoiding import tariffs. Meanwhile, smaller composite manufacturers are gaining traction in coastal bridge tenders by offering 25-year corrosion guarantees, which mainstream steel suppliers cannot match. Overall, competition in the market is intense but balanced, maintaining moderate levels of market concentration.

China Roadside Safety Barriers Construction Industry Leaders

Jiangsu Guoqiang Singsun Energy Co., Ltd.

Wuhan Dachu Traffic Facilities Co., Ltd.

Hebei Tianchuang Pipe Co., Ltd.

Shandong Baimiao New Materials Co., Ltd.

Shandong Safebuild Traffic Facilities Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Shiziyang Link's West Bridge towers topped out in Guangdong, marking a critical milestone for the 35-kilometer, double-deck expressway crossing the Pearl River Estuary with a 2,180-meter main span—set to become the world's longest double-deck suspension bridge upon completion in 2028 and requiring specialized transition barriers between upper (8 lanes, 100 kilometers per hour) and lower (8 lanes, 80 kilometers per hour) deck levels.

- January 2026: Shandong's S36 Linteng Expressway (140.77 kilometers, RMB 28.6 billion, USD 3.9 billion) opened to traffic, requiring continuous W-beam and cable-barrier installation along median and shoulder zones to serve the Linyi-Tengzhou corridor.

- January 2026: Qingyun Expressway Yuecheng–Yunfu New Area bridge-tunnel section (approximately 8.1 kilometers, six lanes) deployed a smart safety platform integrating video analytics, automatic number-plate recognition (ANPR), and lane-level guidance signs, achieving 97.9% automatic detection accuracy for stopped vehicles and reducing emergency-response time from 30 minutes to under 2 minutes.

- December 2025: Shandong commenced construction on the Weizou Expressway Yiyuan-Zoucheng section (176.1 kilometers, RMB 19.66 billion, USD 2.7 billion), with barrier procurement expected to begin in Q2 2026 and cable barrier systems planned for curved mountain sections.

China Roadside Safety Barriers Construction Market Report Scope

| Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) |

| Cable Barrier Systems |

| Crash Cushions & Impact Attenuators |

| Others (Motorcyclist Protection, Hybrid, Emerging) |

| Steel |

| Concrete |

| Plastic & Composite |

| Others (Aluminum, Rubber, Recycled Blends) |

| Highways & Expressways |

| Urban Roads & Streets |

| Bridges & Flyovers |

| Others (Rural, Industrial/Private, Parking, Tunnels, Temp Zones) |

| New Installation |

| Renovation / Retrofit / Repair |

| Beijing |

| Shanghai |

| Shenzhen |

| Guangzhou |

| Chengdu |

| Rest of China |

| By Product Type | Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) | |

| Cable Barrier Systems | |

| Crash Cushions & Impact Attenuators | |

| Others (Motorcyclist Protection, Hybrid, Emerging) | |

| By Material | Steel |

| Concrete | |

| Plastic & Composite | |

| Others (Aluminum, Rubber, Recycled Blends) | |

| By Application | Highways & Expressways |

| Urban Roads & Streets | |

| Bridges & Flyovers | |

| Others (Rural, Industrial/Private, Parking, Tunnels, Temp Zones) | |

| By Installation Type | New Installation |

| Renovation / Retrofit / Repair | |

| By Major Cities | Beijing |

| Shanghai | |

| Shenzhen | |

| Guangzhou | |

| Chengdu | |

| Rest of China |

Key Questions Answered in the Report

How big will the China roadside safety barriers construction market be by 2031?

Forecasts place it at USD 2.63 billion, up from USD 2.02 billion in 2026.

Which product captures the most market share today?

Metal guardrails account for 63.4% of 2025 spending.

What is the fastest-growing product category?

Cable barrier systems are projected to rise at a 6.05% CAGR through 2031.

Why are composites gaining traction?

Fiber-reinforced barriers avoid corrosion and cut lifetime maintenance costs by up to 30%.

Which city offers the strongest growth outlook?

Chengdu leads with an expected 6.58% CAGR between 2026 and 2031.

How strict are the new Chinese guardrail standards?

GB/T 31439-2025 raises energy-absorption requirements and mandates higher-grade steel, making compliance a core tender prerequisite.

Page last updated on: