North America Roadside Safety Barriers Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

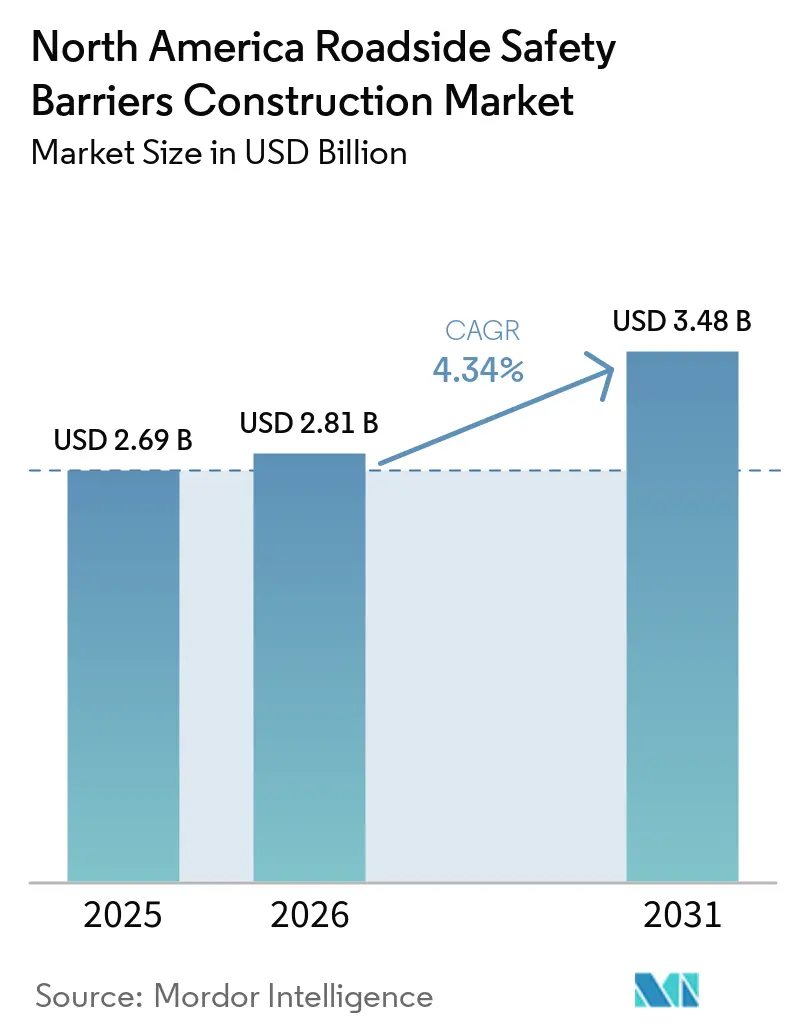

| Base Year Market Size (2025) | USD 2.69 Billion |

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 3.48 Billion |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

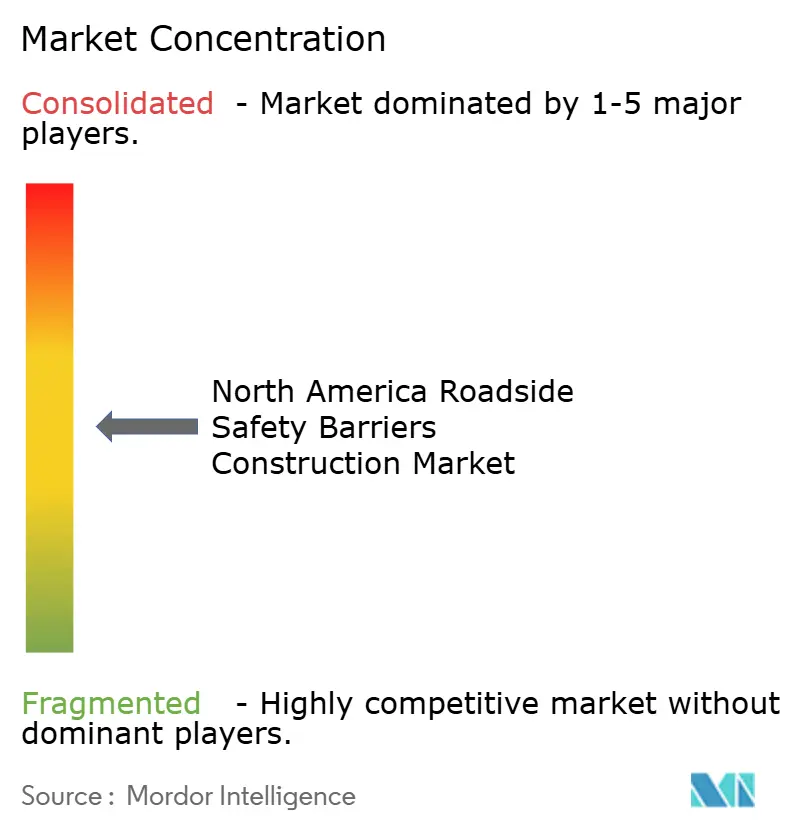

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Roadside Safety Barriers Construction Market Analysis by Mordor Intelligence

The North America Roadside Safety Barriers Construction Market size is expected to increase from USD 2.69 billion in 2025 to USD 2.81 billion in 2026 and reach USD 3.48 billion by 2031, growing at a CAGR of 4.34% over 2026-2031. Three key factors are influencing demand: federally supported highway funding, mandatory compliance with the Manual for Assessing Safety Hardware (MASH) 2016 standards, and stricter work-zone protection regulations. Allocations from the Federal Infrastructure Investment and Jobs Act are driving a sustained multi-year backlog of projects involving guardrails, median barriers, and bridge parapets. Meanwhile, state Departments of Transportation (DOTs) are focusing on improving safety in high-crash rural corridors. Pilot programs using composite and smart materials are challenging the cost advantage of steel, while rental fleets are increasingly adopting portable systems to meet the new positive-protection requirements. Competitive dynamics remain moderate, as long-established suppliers face rising input costs and certification delays, which hinder the timely introduction of new products.

Key Report Takeaways

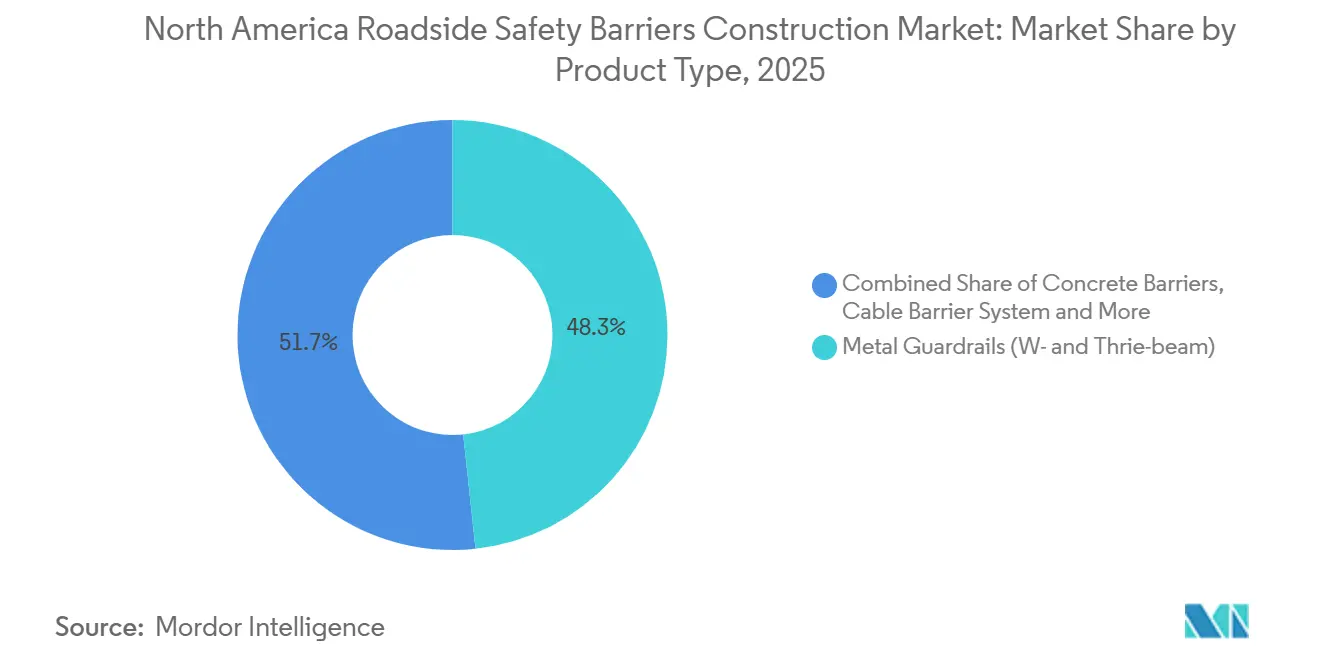

- By product type, metal guardrails captured 48.3% of the North America roadside safety barriers construction market share in 2025; cable barrier systems are projected to grow at 4.91% CAGR between 2026 and 2031.

- By material, steel held 57.6% of the North America roadside safety barriers construction market share in 2025; plastic and composite materials are projected to grow at 5.10% CAGR between 2026 and 2031.

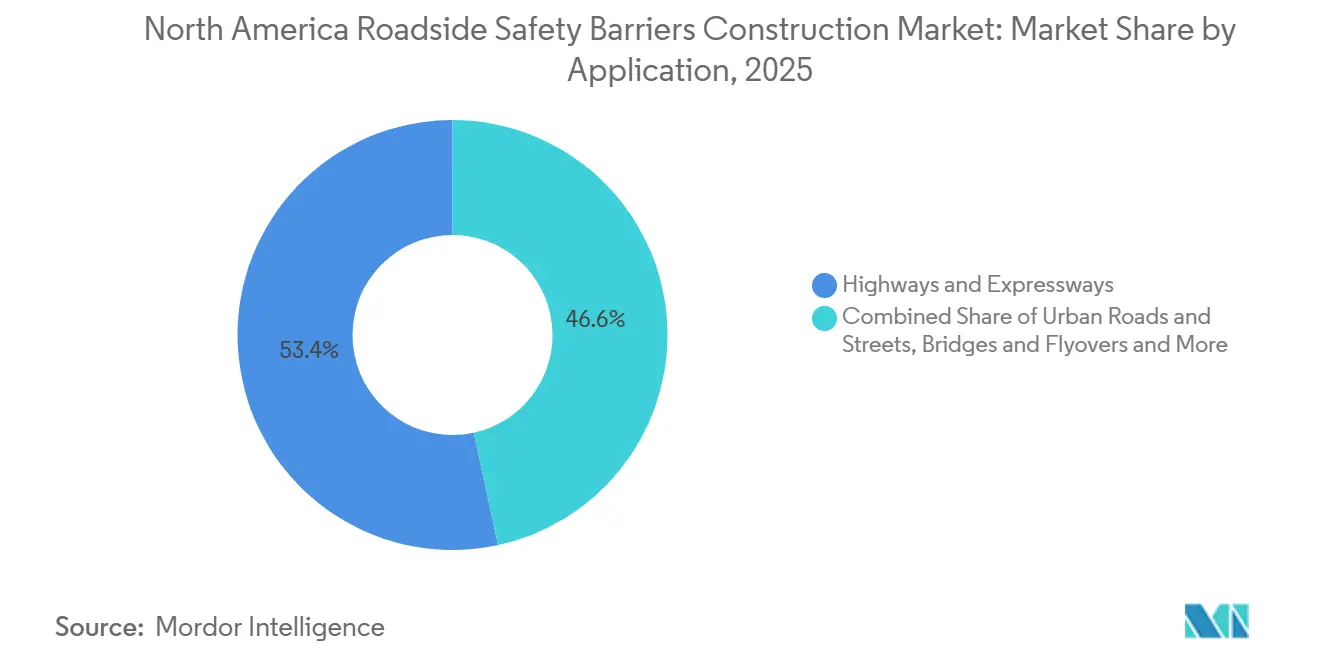

- By application, highways and expressways commanded 53.4% of the North America roadside safety barriers construction market share in 2025; bridges and flyovers are projected to grow at 5.23% CAGR between 2026 and 2031.

- By installation, renovation, retrofit, and repair, captured 61.1% of the North America roadside safety barriers construction market share in 2025; new installations are projected to grow at 4.89% CAGR between 2026 and 2031.

- By country, the United States accounted for 82.3% of the North America roadside safety barriers construction market share in 2025; Mexico is projected to grow at 5.50% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Roadside Safety Barriers Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IIJA-funded highway programs are accelerating guardrail, median barrier, and bridge parapet installations | +1.3% | United States | Medium term (2–4 years) |

| Mandatory MASH compliance deadlines are driving large-scale replacement of legacy roadside hardware | +1.1% | United States, Canada | Short term (≤ 2 years) |

| State DOT safety programs prioritizing high-crash corridors, increasing barrier deployment volumes | +0.9% | United States, Canada | Medium term (2–4 years) |

| Ongoing interstate rehabilitation and widening projects, expanding median and roadside barrier demand | +0.7% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Work-zone safety regulations across the US and Canada are sustaining temporary barrier usage in roadworks | +0.5% | United States, Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IIJA-Funded Highway Programs Accelerating Guardrail, Median Barrier, and Bridge Parapet Installations

Record federal expenditures serve as the primary driver for the North America roadside safety barriers construction market. The Highway Safety Improvement Program budget is set to increase to USD 3.49 billion in fiscal 2026, while the Bridge Formula Program contributes USD 5.5 billion annually, supporting projects that previously lacked state funding. Notable progress is evident in California, where a USD 33.2 million barrier upgrade on State Route 49 was completed in January 2026, and 28 miles of cable median barriers were installed on Interstate 80 in 2025. Pennsylvania’s USD 259 million Interstate 80/Interstate 99 interchange project, primarily funded through Bipartisan Infrastructure Law formula grants, incorporates higher-containment MASH Test Level 4 systems, demonstrating how federal funding influences product standards. Similar funding allocations are directed toward Utah’s US-6 and various Midwest corridors, ensuring sustained workloads for fabricators and installers over multiple years.[1]Federal Highway Administration, “Bipartisan Infrastructure Law Funding,” fhwa.dot.gov .

Mandatory MASH Compliance Deadlines Driving Large-Scale Replacement of Legacy Roadside Hardware

The transition from the National Cooperative Highway Research Program 350 standard to MASH 2016 is requiring Departments of Transportation (DOTs) to replace or retrofit hardware that no longer meets updated crash-test standards. The compliance deadline for most states is December 31, 2026, creating tighter project timelines. For instance, Caltrans has prohibited the use of legacy Type K portable barriers on projects advertised after this date. High-tension cable systems highlight the challenges of certification, as by late 2025, only one supplier had achieved full MASH 16 Test Level 4 approval for both flat ground and 4:1 slopes. Consequently, contractors are facing difficulties in securing compliant inventory, while rental fleets are retiring thousands of linear feet of outdated stock, driving near-term demand significantly above historical levels.[2]California Department of Transportation, “SR-49 Safety Enhancement Project Completion Notice,” dot.ca.gov.

State DOT Safety Programs Prioritizing High-Crash Corridors Increasing Barrier Deployment Volumes

Vision Zero and Target Zero initiatives at the state level complement federal funding with locally focused crash-reduction objectives. Indiana has installed over 550 miles of cable barriers, with an investment exceeding USD 34 million by 2025, and has planned additional work on Interstate 74 for summer 2026. Louisiana achieved 726 miles of median cable protection by 2025, reporting a 100% reduction in fatal crossover incidents. Pennsylvania installed 29 miles of cable barriers on Interstate 81 and other routes, resulting in a 90% decrease in similar crashes[3]Pennsylvania Department of Transportation, “Median Cable Barrier Program,” penndot.pa.gov. These data-driven programs prioritize spending on corridors with the highest crash rates, ensuring that barrier projects not only enhance safety metrics but also serve as visible political achievements.

Ongoing Interstate Rehabilitation and Widening Projects Expanding Median and Roadside Barrier Demand

Interstate highways constructed during the 1960s and 1970s now require extensive rehabilitation, including lane widening and adjustments for higher design speeds, necessitating stronger containment systems, often made of concrete or cable. Alberta has allocated USD 3.5 billion for such projects beginning in 2026, incorporating barrier procurement into all widening contracts. Similarly, California’s Interstate 80 and Mexico’s federal toll-road modernization projects combine lane expansions with the installation of upgraded or entirely new barriers. Upcoming large-scale projects, such as the Gordie Howe International Bridge, provide a binational framework aligning Canadian and U.S. MASH standards, enabling suppliers to distribute testing costs across a broader market base.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy state DOT approvals and certification processes are delaying barrier system deployment | -0.6% | United States and Canada (state/provincial DOT jurisdictions) | Short term (≤ 2 years) |

| High steel prices and installation costs are increasing total project budgets for barrier systems | -0.4% | United States, Canada, Mexico (global steel markets) | Medium term (2–4 years) |

| Logistics and contractor capacity constraints are slowing the execution of large-scale replacement programs | -0.3% | United States (rural corridors), Canada (northern regions), Mexico (emerging markets) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lengthy State DOT Approvals and Certification Processes Delay Barrier System Deployment

Each new barrier model undergoes extensive evaluations, including crash tests, independent laboratory assessments, and state engineering reviews, which can take 12 to 18 months to complete. With individual states imposing additional specifications, manufacturers incur high costs for repeated testing and documentation, delaying market entry. The cable-barrier segment highlights these challenges: by 2025, only four approved suppliers were active in the market, each navigating distinct requirements for materials, splices, or post-spacing across various jurisdictions. Contractors securing bids before obtaining local product approval often face expensive delays, while Departments of Transportation (DOTs) experience budgetary backlogs as they wait for compliant hardware to become available.

High Steel Prices and Installation Costs Increasing Total Project Budgets for Barrier Systems

The Florida Department of Transportation's (DOT) 2025 Steel and Rebar Escalation Study has projected the price of structural steel to reach USD 5.03 per pound in 2026, approximately 30% higher than the 10-year average. Since steel can constitute up to 15% of the direct costs in barrier projects, price increases during extended procurement cycles can create significant budgetary challenges. In fixed-price contracts, fabricators face limited ability to pass on surcharges, which can reduce profit margins and potentially deter participation in smaller projects. Although concrete barriers have higher initial costs—USD 105.14 per linear foot compared to USD 30.94 for W-beam guardrails—their substantially lower maintenance costs could make them more favorable in life-cycle cost analyses if input price inflation persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cable Systems Gain Median-Barrier Share

Metal guardrails accounted for 48.3% of the North America roadside safety barriers construction market share in 2025. These guardrails are predominantly used on rural highways where the right-of-way width is limited. However, cable systems are gaining traction rapidly. Cable systems, which provide a dynamic deflection of 6-8 feet, are projected to grow at a compound annual growth rate (CAGR) of 4.91% through 2031. For instance, Gibraltar installed 432,960 feet of cable in Alberta within 45 days, demonstrating the appeal of swift deployment for agencies managing increasing traffic volumes. Concrete, the second-largest product category, is primarily used for bridge parapets and urban medians where minimal deflection is essential. Crash cushions and attenuators, though niche products, are increasingly incorporating modular and reusable designs to reduce life-cycle costs.

The North America roadside safety barriers construction market for cable systems is expected to grow as Departments of Transportation (DOTs) replicate successful outcomes observed in states like Louisiana and Indiana. These states reported up to a 100% reduction in fatal crossover incidents following the installation of cable systems. Additionally, portable steel barriers, such as HighwayGuard™, are blurring the distinction between permanent and temporary products, further expanding the cable and hybrid category. Future growth could accelerate if more states align their specifications, facilitating large-scale production and faster MASH certification.

By Material: Composites Challenge Steel’s Lifecycle Economics

Steel accounted for 57.6% of the material market share in 2025, reinforcing its dominance in W-beam, Thrie-beam, and cable applications. However, composite and recycled-plastic alternatives, which are still in the early stages of adoption, are projected to grow at a compound annual growth rate (CAGR) of 5.10% through 2031, outpacing the overall market growth rate. Field trials indicate that fiber-reinforced polymer posts offer corrosion resistance and reduce routine maintenance costs. Additionally, an Internet-of-Things-enabled expanded polystyrene concrete hybrid, which is 30% lighter than standard concrete, provides real-time impact alerts to maintenance crews, reducing the need for frequent inspections.

Rising steel prices and zinc-galvanizing surcharges have shifted attention to total ownership costs. Research from UC Davis indicates that concrete barriers achieve cost parity with steel options after approximately 15 years when maintenance expenses are factored in. If composite systems can achieve cost competitiveness within a shorter timeframe, they may redefine industry specifications. Increasing patent activity, such as high-density polyethylene (HDPE) tube crash cushions with adjustable energy absorption, highlights ongoing research and development efforts that could drive a shift away from metal-based solutions over the forecast period.

By Application: Bridge Parapets Outpace Median Installations

In 2025, highways and expressways accounted for 53.4% of application revenues. However, bridges and flyovers represent the fastest-growing segment, with a projected CAGR of 5.23% through 2031. The USD 5.5 billion annual Bridge Formula Program mandates states to rehabilitate numerous structurally deficient bridges, each requiring high-containment MASH Test Level 4 or 5 parapets. A notable example is the Gordie Howe International Bridge, which features TL-5 concrete barriers spanning 1.5 miles of elevated deck.

Urban arterials, while smaller in revenue terms, are gaining increased focus as cities adopt Vision Zero principles. The need for shorter deflection zones and proximity to pedestrians drives the preference for concrete and hybrid systems. Additionally, municipalities are increasingly incorporating crash cushions at intersections. Wildlife-crossing integrations in New Mexico highlight the potential for future multi-objective barrier designs that address both safety and ecological considerations.

By Installation Type: Retrofit Demand Dominates Greenfield

Renovation, retrofit, and repair activities accounted for 61.1% of the projected 2025 revenues in the North America roadside safety barriers construction market. Many decades-old interstate corridors and rural two-lane routes require barrier upgrades before additional lanes can be constructed. For example, Pennsylvania’s USD 5.2 million retro-cable project on Interstate 81 involved the installation of 29 miles of new barriers without increasing road capacity. Retrofit projects are increasingly adopting higher-containment systems, which has led to a rise in the average cost per mile.

Although new-build installations currently represent a smaller share, they are expected to grow at a CAGR of 4.89% as projects funded by the IIJA, such as lane additions, bridge replacements, and Mexico’s paradores integrales, are implemented. Alberta’s USD 3.5 billion highway twinning initiative and Mexico’s USD 1 billion truck-stop upgrade plan also allocate significant budgets for barriers. Suppliers offering integrated solutions, including design, products, and IoT monitoring services, are well-positioned to benefit from this growth in greenfield projects.

Geography Analysis

The United States is projected to account for 82.3% of the North America roadside safety barriers construction market share in 2025. Federal Highway Administration allocations of USD 3.494 billion for Highway Safety Improvement and USD 5.5 billion for bridge upgrades provide multi-year funding visibility. California utilizes its USD 3 billion annual gas-tax revenue to expedite projects such as State Route 49 and Interstate 80, while Pennsylvania directs BIL formula funds toward complex interchange redesigns requiring high-containment parapets. Indiana and Louisiana have demonstrated significant safety improvements, reporting double-digit percentage reductions in median-crossover crashes following large-scale cable barrier installations.

Canada maintains steady contributions, supported by the Build Communities Strong Fund’s USD 37.7 billion 10-year plan and Alberta’s USD 6.1 billion allocation for highways and bridges. The rapid deployment of cable barriers across 323 miles in Alberta during 2025 highlights the effectiveness of composite contracting models in minimizing lane closures. WorkSafeBC’s endorsement of concrete as the positive-protection standard in 2025 reflects consistent specification trends across Canadian provinces.

Mexico, while currently smaller in market size, is expected to grow at a 5.50% CAGR through 2031. The draft PROY-NOM-037-SICT2-2025 barrier standard aligns national regulations with United Nations fatality-reduction targets, creating a predictable pipeline of upgrade projects for federal and toll corridors. Investments in paradores integrales and the closure of 118 irregular highway accesses are driving spending on barriers and crash cushions. Additionally, the adoption of technology-intensive solutions such as dynamic arches and plate recognition systems is generating ancillary demand for crash-worthy support structures, expanding the market beyond traditional barriers.

Competitive Landscape

The North America roadside safety barriers construction market is moderately fragmented, with the five largest suppliers accounting for a significant share of total revenue. Established manufacturers such as Valtir, Valmont Industries, Lindsay Corporation, Hill & Smith, and Gregory Industries have maintained long-term relationships with state Departments of Transportation (DOTs), providing them with an advantage in approvals and certifications. Recent product launches, such as Valtir’s HighwayGuard MDS portable steel barrier, which offers sub-1-inch dynamic deflection and can be installed in approximately one hour, highlight the growing importance of rapid-deployment capabilities. These features are increasingly essential for rental fleets to comply with the Federal Highway Administration’s 2024 positive-protection rule.

Vertical integration remains a key strategic approach in the market. Nucor, North America’s largest recycled-steel producer, is expanding its Towers & Structures business to ensure a stable supply of raw materials for poles, sign supports, and barrier components. Similarly, Valmont’s in-house galvanizing network enables the company to mitigate the impact of zinc-price fluctuations, helping to protect gross margins despite ongoing volatility in spot metal costs. Additionally, private-equity involvement, such as Monomoy Capital Partners’ 2022 acquisition and rebranding of Trinity Highway Products as Valtir, indicates increasing consolidation within the rental and temporary-barrier segment, which still includes numerous regional operators.

Market differentiation is increasingly centered on life-cycle value. Composite and Internet-of-Things (IoT)-enabled barriers are gaining traction in pilot projects due to their potential for reduced maintenance requirements and faster post-impact inspections. Hill & Smith’s integration of Smart Cushion attenuators with Gregory Industries guardrails simplifies procurement processes for contractors while increasing value per linear foot installed. Furthermore, patent activity in areas such as high-density polyethylene (HDPE) crash cushions and expanded-polystyrene concrete hybrids suggests that traditional steel systems will face growing competition from advancements in material science over the forecast period.

North America Roadside Safety Barriers Construction Industry Leaders

Valtir, LLC

Valmont Industries

Lindsay Corporation (Barrier Systems)

Hill & Smith Inc.

Gregory Highway (Gregory Industries)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The North Carolina Department of Transportation awarded Contract DL00380 for the State Road 1529 Bridge No. 262 replacement over First Broad River in Cleveland County, following Hurricane Helene damage in September 2024. The project requires MASH-compliant bridge parapets and guardrails with completion scheduled for October 2027, demonstrating federal-state coordination on disaster recovery infrastructure.

- January 2026: California Department of Transportation completed a USD 33.2 million barrier upgrade project on State Route 49, installing cable median barriers and concrete parapets across 18 miles of rural highway. The project combined federal HSIP funding with state SB1 revenues to reduce cross-centerline crashes by an estimated 40%.

- January 2026: Valtir deployed its HighwayGuard™ MDS portable steel barrier system on Florida State Road 50 at Alafaya for a utility trench protection project. The MASH-tested rental barrier achieved 0.98-inch deflection and was installed in under 1 hour, meeting new federal work-zone positive protection requirements.

North America Roadside Safety Barriers Construction Market Report Scope

| Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) |

| Cable Barrier Systems |

| Crash Cushions & Impact Attenuators |

| Others (Motorcyclist protection systems, hybrid/specialty barriers, emerging safety solutions) |

| Steel |

| Concrete |

| Plastic & Composite |

| Others (Aluminum, rubber-based materials, composite blends, recycled materials) |

| Highways & Expressways |

| Urban Roads & Streets |

| Bridges & Flyovers |

| Others (Rural roads, industrial/private roads, parking areas, tunnels, temporary traffic zones) |

| New Installation |

| Renovation / Retrofit / Repair |

| United States |

| Canada |

| Mexico |

| By Product Type | Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) | |

| Cable Barrier Systems | |

| Crash Cushions & Impact Attenuators | |

| Others (Motorcyclist protection systems, hybrid/specialty barriers, emerging safety solutions) | |

| By Material | Steel |

| Concrete | |

| Plastic & Composite | |

| Others (Aluminum, rubber-based materials, composite blends, recycled materials) | |

| By Application | Highways & Expressways |

| Urban Roads & Streets | |

| Bridges & Flyovers | |

| Others (Rural roads, industrial/private roads, parking areas, tunnels, temporary traffic zones) | |

| By Installation Type | New Installation |

| Renovation / Retrofit / Repair | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will barrier construction spending be in North America by 2031?

The North America roadside safety barriers construction market is projected to reach USD 3.48 billion by 2031, up from USD 2.81 billion in 2026.

Which country drives the greatest demand?

The United States accounted for 82.3% of 2025 spending, supported by Infrastructure Investment and Jobs Act funding and state Vision Zero programs.

What segment delivers the highest growth rate?

Bridges and flyovers lead with a 5.23% CAGR, driven by the USD 5.5 billion annual Bridge Formula Program targeting structurally deficient spans.

How do MASH standards affect procurement?

DOTs must retire or retrofit hardware failing MASH 2016 crash tests by December 31, 2026, creating a near-term replacement cycle and favoring compliant products.

Are composite barriers ready for large-scale use?

Pilot deployments indicate fiber-reinforced polymer and EPS-concrete hybrids reduce corrosion and inspection costs, but large-scale adoption depends on further MASH validation and cost competitiveness with steel.

Page last updated on: