Germany Roadside Safety Barriers Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

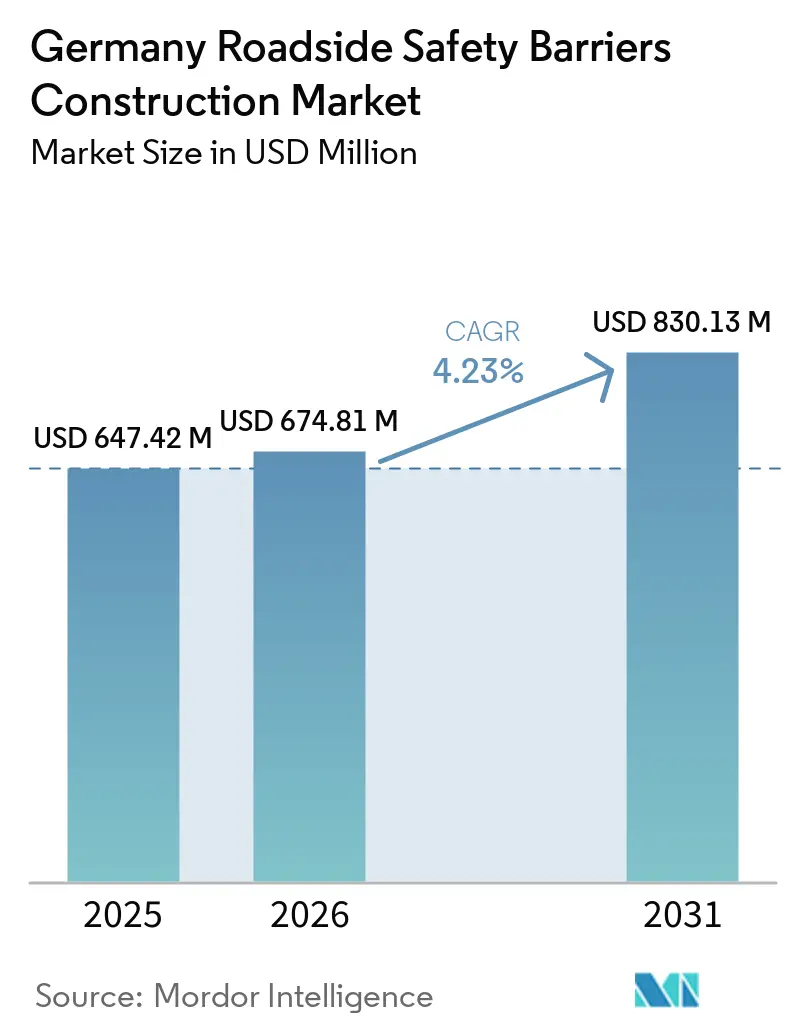

| Base Year Market Size (2025) | USD 647.42 Million |

| Market Size (2026) | USD 674.81 Million |

| Market Size (2031) | USD 830.13 Million |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

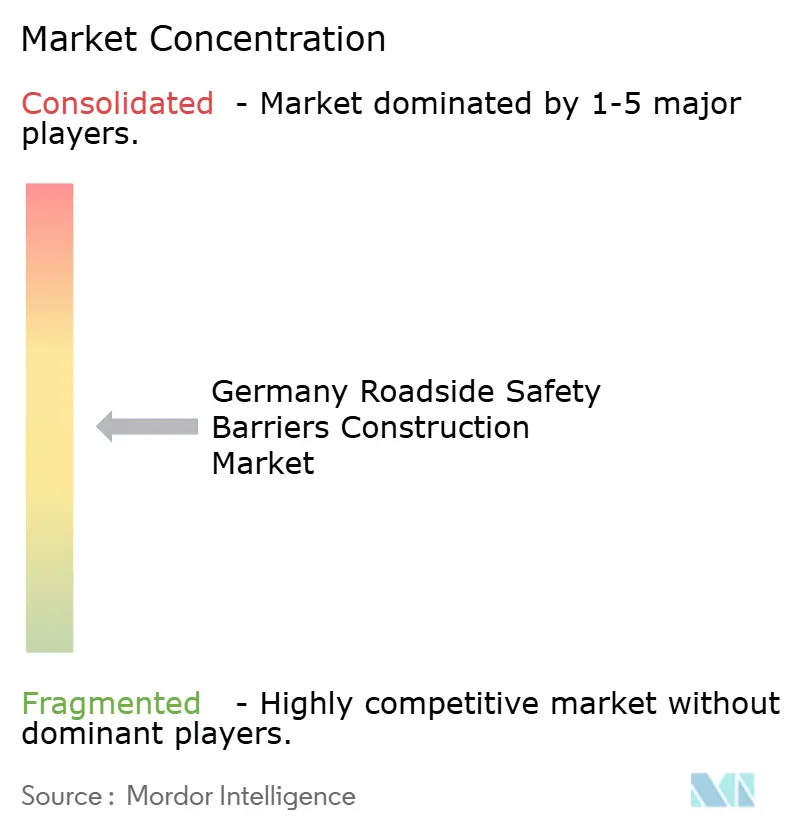

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Roadside Safety Barriers Construction Market Analysis by Mordor Intelligence

The Germany Roadside Safety Barriers Construction Market size is expected to increase from USD 647.42 million in 2025 to USD 674.81 million in 2026 and reach USD 830.13 million by 2031, growing at a CAGR of 4.23% over 2026-2031. Recent funding initiatives for bridge modernization, the nationwide adoption of European standard EN 1317 products, and a consistent backlog of Autobahn rehabilitation projects have sustained demand, even as new road construction remains stagnant. However, procurement delays caused by homologation rules introduce challenges that slightly moderate the overall growth of the Germany roadside safety barriers construction market. Additionally, higher steel prices, labor shortages, and night-shift premiums in urban areas impact profit margins. Despite these pressures, projects are rarely canceled, as safety-critical upgrades are mandatory for federal and municipal road agencies. Innovations in materials, such as lightweight fiber-reinforced polymer (FRP) panels for temporary works, are beginning to influence buyer preferences, favoring systems that reduce closure times and lane-rental costs.

Key Report Takeaways

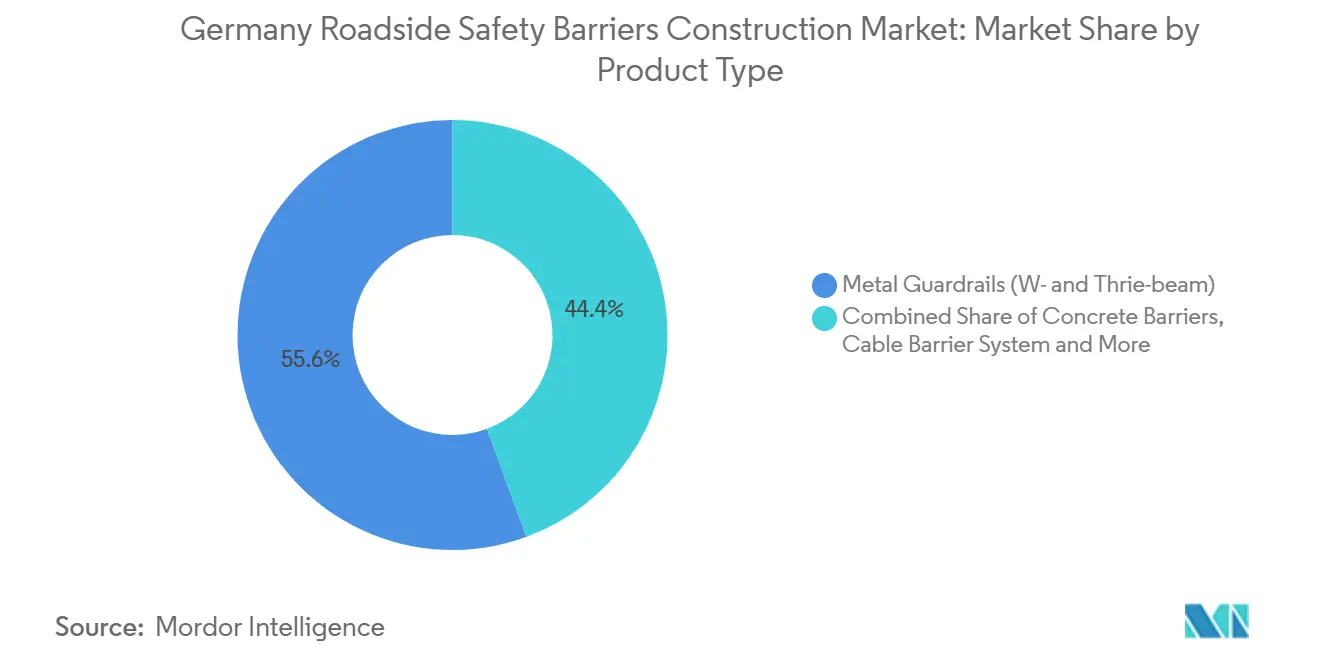

- By Product type, Metal guardrails commanded 55.6% of the Germany roadside safety barriers construction market share in 2025, while cable barriers are forecast to expand at a 4.98% CAGR between 2026 and 2031.

- By Material, Steel captured 65.7% of the Germany roadside safety barriers construction market size in 2025, and plastic-and-composite solutions are projected to grow at 5.21% CAGR between 2026 and 2031.

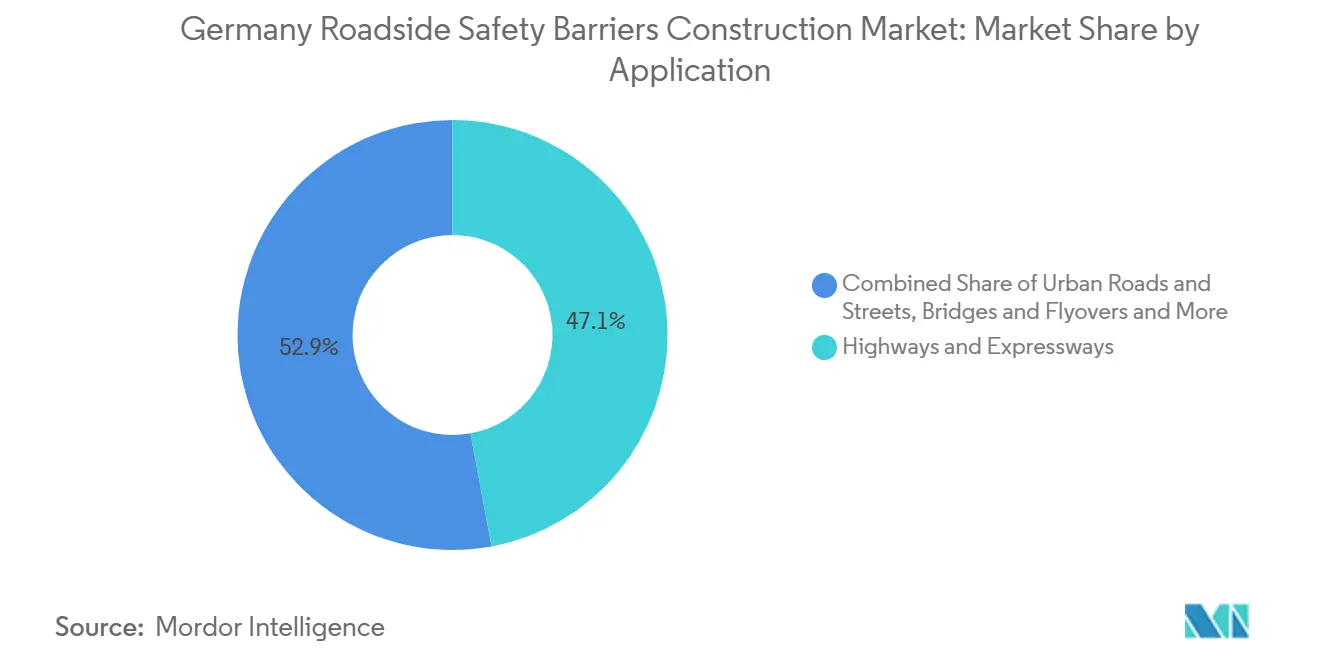

- By Application, Highways and expressways accounted for 47.1% of installations in 2025; bridges and flyovers are advancing at a 5.10% CAGR between 2026 and 2031.

- By Installation, Renovation, retrofit, and repair work represented 65.9% of total installations in 2025, whereas new installations are forecast to rise at 4.79% CAGR between 2026 and 2031.

- By City, Berlin led with 22.5% of installations in 2025; Hamburg is set to post the fastest expansion at a 5.31% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Roadside Safety Barriers Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Autobahn bridge rehabilitation and corridor renewal programs are increasing roadside barrier replacement demand | +1.2% | National, strongest in North Rhine-Westphalia, Bavaria, Baden-Württemberg | Long term (≥ 4 years) |

| EN 1317 compliance requirements are driving the adoption of tested guardrail and containment systems | +0.9% | National | Medium term (2–4 years) |

| High traffic volumes on federal motorways are sustaining demand for median and edge protection barriers | +0.8% | National, peak on A1, A3, A5, A7 freight axes | Long term (≥ 4 years) |

| Road-safety upgrades on bridges, interchanges, and work zones are increasing barrier installation activity | +0.7% | National, early gains in Berlin, Hamburg, Munich | Medium term (2–4 years) |

| Shift toward higher-containment systems supporting upgrades on freight-intensive highway stretches | +0.6% | National, notably A2, A3, A5, A61 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Autobahn Bridge Rehabilitation and Corridor Renewal Programs Increasing Roadside Barrier Replacement Demand

In 2024, a federal audit identified 4,000 Autobahn bridges requiring urgent structural repairs, creating a multiyear demand for edge and pier-protection barriers certified to high-containment levels, such as H4a or H4b[1]Bundesrechnungshof, “Bericht an den Haushaltsausschuss, Brückenmodernisierung,” bundesrechnungshof.de . Each bridge project includes both permanent EN 1317 barriers and temporary work-zone systems, providing suppliers with revenue opportunities throughout the project lifecycle. Delays due to environmental permit approvals often extend the on-site duration of rental barriers, thereby increasing revenue over time. With the bridge renewal backlog exceeding USD 8.7 billion, the Germany roadside safety barriers construction market is expected to experience steady demand well beyond 2030. Contractors offering both precast concrete production and mobile barrier fleets are well-positioned to manage the entire project cycle effectively.

EN 1317 Compliance Requirements Driving Adoption of Tested Guardrail and Containment Systems

Since February 2026, Autobahn GmbH's framework contracts have required EN 1317 certification for all guardrails, concrete blocks, cable arrays, and terminals used on federal routes[2]Autobahn GmbH, “Zahlen, Daten, Fakten 2026,” autobahn.de. This compliance includes standards for working width, vehicle intrusion, and acceleration severity indices, prompting agencies to phase out older rails lacking complete test documentation. Manufacturers such as REBLOC and DELTABLOC command higher prices for low-intrusion H4b blocks, which are suitable for narrow bridge footprints. Additionally, modular add-ons for motorcyclist protection can be attached to existing rails, offering a cost-effective compliance solution for constrained budgets. This policy emphasizes technology-based differentiation and ensures that the roadside safety barriers construction market in Germany remains focused on rigorously tested systems.

High Traffic Volumes on Federal Motorways Sustaining Demand for Median and Edge Protection Barriers

According to Kraftfahrt-Bundesamt toll data, heavy-goods vehicle mileage is projected to reach 1.52 billion kilometers in 2025, reflecting a year-over-year increase of 3.2%[3]Kraftfahrt-Bundesamt, “Mautstatistik 2025,” kba.de . Freight corridors with daily truck counts exceeding 10,000 now automatically qualify for upgrades from medium-containment N2 rails to H2 or H4 arrays. Cable barriers are gaining preference in narrow medians due to their flexible posts, which absorb energy without requiring wider carriageways. Research conducted by the Federal Institute for Materials Research indicates that heavier battery-electric trucks increase impact loads by 15-20%, reducing the service life of older steel rails. In practice, higher axle weights ensure a more consistent replacement cycle, shielding the German roadside safety barriers construction market from broader declines in passenger car traffic.

Road Safety Upgrades on Bridges, Interchanges, and Work Zones: Increasing Barrier Installation Activity

The August 2025 opening of Berlin’s A100 extension introduced a new approach: all interchange gores, gantry bases, and ramp ends are now equipped with redirective crash cushions combined with ITS-enabled warning beacons. Similar designs have been planned for Hamburg’s Elbtunnel retrofit and Munich’s A99 bridge program. While crash cushions are more expensive per meter compared to guardrails, they effectively address high-severity collision points, leading city authorities to rarely reduce their implementation. In work zones, rental barriers equipped with sensor mounts reduce setup times and provide live lane-closure data to the national mobility cloud. By integrating digital safety features with physical barriers, the roadside safety barriers construction market in Germany benefits from dual revenue streams generated by hardware and connectivity solutions.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy approval and specification processes are delaying the deployment of new barrier systems | -0.5% | National | Medium term (2–4 years) |

| High steel, fabrication, and installation costs increase barrier replacement budgets | -0.4% | National, acute around Munich, Frankfurt, Hamburg | Short term (≤ 2 years) |

| Construction sequencing constraints on busy Autobahn corridors are slowing execution and raising traffic-management costs | -0.3% | National, largest on A1, A3, A5, A7, A8 | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lengthy Approval and Specification Processes Delaying Deployment of New Barrier Systems

Before a new product is included on the BASt-approved list, suppliers must undergo comprehensive crash testing and an extensive technical review process, which can take up to two years. Any minor design modification resets the approval timeline. Cities are restricted from purchasing unapproved items, creating a revenue gap for innovators during periods of high marketing expenditure. Smaller companies often license designs from established players to mitigate this gap, which limits competitive diversity. This delay hampers the short-term adoption of composites and hybrid rails, constraining growth in the Germany roadside safety barriers construction market until regulatory processes become more efficient.

High Steel, Fabrication, and Installation Costs Increasing Barrier Replacement Budgets

The construction-steel cost index increased to 108 in 2024, driven by higher energy costs and the implementation of EU carbon tariffs. The cost of a standard W-beam lane, which was USD 260 per meter in 2021, has risen to approximately USD 300, excluding labor and night-shift premiums. Municipal budgets, already strained by inflation affecting other capital programs, occasionally delay mid-priority barrier sections. Contractors attempt to distribute work across multiple fiscal years; however, fragmented project scopes lead to higher mobilization costs. While the immediate financial impact is significant, the life-safety priority of most projects prevents outright cancellations. This trend is expected to affect the Germany roadside safety barriers construction industry over the next one to two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cable Systems Gain on Freight Corridors

Metal guardrails accounted for 55.6% of the Germany roadside safety barriers construction market in 2025, driven by the long-standing use of W-beam and Thrie-beam designs on secondary federal roads. While demand for cable barriers remains smaller in absolute terms, it is projected to grow at a compound annual growth rate (CAGR) of 4.98% through 2031, as freight corridors retrofit narrow medians with flexible H2 or H4b systems. The market size for Germany's roadside safety barrier construction is closely linked to cable installations, particularly in road sections with truck traffic exceeding 10,000 vehicles per day. Suppliers such as Saferoad RRS now offer turnkey kits that include tensioning jacks, anchor sockets, and post-driving rigs, reducing setup time and enabling installations during overnight road closures.

Concrete barriers are primarily used to protect bridge parapets and tunnel portals where zero deflection is required. Precast models, such as the DELTABLOC DB 185AS-A, provide H4b containment with a working width of just 0.60 meters, a critical feature for areas with dense pier clusters in cities like Berlin and Munich. Crash cushions and impact attenuators represent a specialized segment within the Germany roadside safety barriers construction market, growing faster than the overall industry due to the requirement for non-redirective energy absorbers rated at 110 km/h for every new interchange gore. Additionally, pilot programs have begun integrating photovoltaic panels onto concrete surfaces to offset lighting energy consumption, indicating potential new revenue opportunities in future project tenders.

By Material: Composites Challenge Steel Dominance

Steel accounted for 65.7% of the projected 2025 expenditure due to its widespread use in guardrails and the supply chain's extensive experience with galvanizing, hot-dip coatings, and repair kits. However, composite and plastic systems are expected to grow at a compound annual growth rate (CAGR) of 5.21% through 2031, marking the fastest growth among all material categories. This growth in the Germany roadside safety barriers construction market is attributed to modular fiber-reinforced polymer (FRP) panels, such as Brüninghoff’s HEI Protect, which are 40% lighter than steel rails with equivalent ratings and reduce crew requirements to a single truck team. Given that traffic management fees can exceed USD 5,000 per lane-kilometer per day, lighter barriers that minimize closure durations are appealing to both budget planners and safety engineers.

Concrete holds the second-largest market share and is predominantly used in applications requiring long service life and minimal dynamic deflection. High-containment concrete blocks now incorporate polymer fibers to prevent spalling upon impact, ensuring that fragments do not pose secondary hazards. Emerging alternatives include aluminum terminals for lightweight ramps and experimental wood-composite rails currently under evaluation at Fraunhofer. Once the Federal Highway Research Institute (BASt) completes the mandatory ten-year exposure tests, sustainable materials could create a new sub-segment within the Germany roadside safety barriers construction market.

By Application: Bridge Protection Drives Premium Segment

Highways and expressways represented 47.1% of all barrier meters installed in 2025. However, bridges and flyovers are projected to exhibit the highest growth, with a CAGR of 5.10% through 2031. Bridge projects tend to increase average revenue per meter due to the use of H4a or H4b blocks, anchored stainless-steel reinforcement, and low-intrusion profiles designed to protect pier toes. In the German roadside safety barriers construction market, bridge-related projects are dominated by larger suppliers that operate their own precast yards and utilize crane trucks to install 2-ton modules during brief road closures.

Urban arterials, the third-largest segment, often prioritize aesthetic designs, incorporating barriers with noise-damping panels or LED-lit surfaces. Meanwhile, work-zone packages in tunnels and large interchange projects fall under an "other" category but drive advancements in new technology. For instance, ITS-ready panels deployed for the A100 project in 2025 transmitted lane-status data directly to Berlin’s traffic center, demonstrating the compatibility of connected safety hardware with heavy-containment standards.

By Installation Type: Retrofit Dominates, New Build Accelerates

Retrofit and repair accounted for 65.9% of the projected 2025 revenue, highlighting the consistent maintenance demand generated by a mature network, even in the absence of new asphalt installations. Typical activities include replacing outdated W-beam rails with H1 or H2 cable arrays, upgrading old end terminals to energy-absorbing models, and installing motorcyclist skirting boards on high-risk curves. These retrofitting projects often require crews to work across multiple short night shifts, favoring contractors equipped with fast-lift machinery.

New installations are projected to grow at a CAGR of 4.79%, approximately half a percentage point higher than the overall Germany roadside safety barriers construction market. Large-scale projects, such as the USD 782 million A100 extension and the USD 2.3 billion Köhlbrandbrücke replacement, contribute significant contiguous lengths, benefiting manufacturers and rental-barrier providers. Additionally, moveable FRP walls are increasingly used in multiyear work zones and subsequently relocated, enabling agencies to amortize capital costs across multiple sites.

Geography Analysis

Berlin remains the largest buyer in the Germany roadside safety barriers construction market, driven by the USD 782 million A100 eastern leg project, which opened in 2025. This project includes 14 km of H2/H4a edge and median blocks, 22 redirective crash cushions, and an initial set of ITS beacon mounts. The city's procurement strategy ties barrier orders to simultaneous noise-wall and digital-sign packages, favoring suppliers capable of integrating multiple functions into a single profile. Additionally, federal funds allocated for the A12 expansion will add another 10 km of structures, ensuring continued high procurement levels in Berlin. Hamburg's growth is driven by major infrastructure projects, including the USD 2.3 billion Köhlbrandbrücke replacement and Elbtunnel approach works, scheduled for 2027-2028. These projects require H4b blocks rated for 30-ton truck impacts, tunnel-portal crash cushions certified at 110 km/h, and integrated lighting systems. Additionally, port-logistics traffic has created demand for H2 cable-barrier retrofits along the A1 and A7 feeders. This activity supports a 5.31% CAGR, making Hamburg the fastest-growing region in the Germany roadside safety barriers construction market.

Munich and Frankfurt exhibit steady growth, supported by multiyear Autobahn ring renewal projects. In Munich, the A99 Haar bridge package incorporates DELTABLOC DB 185AS-A low-intrusion blocks, while the A9 project combines cable retrofits with motorcyclist-protection boards from Passco. In Frankfurt, significant works are planned for the A66 and A5 corridors between late 2026 and early 2028, with tender calendars already published to allow contractors sufficient preparation time. Regions such as North Rhine-Westphalia, Baden-Württemberg, and Saxony maintain broad-based refurbishment programs, ensuring stable baseline volumes in the Germany roadside safety barriers construction market.

These activities contribute to the overall market's resilience and consistent demand for safety barrier solutions. The combination of large-scale projects in Berlin and Hamburg, steady renewal efforts in Munich and Frankfurt, and ongoing refurbishment across other regions highlights the diverse and sustained growth opportunities within the Germany roadside safety barriers construction market.

Competitive Landscape

Competition in the German roadside safety barriers market is moderate, with DELTABLOC Deutschland, Saferoad RRS, and REBLOC Germany collectively accounting for approximately 35-40% of annual sales. These companies maintain a comprehensive EN 1317-certified product portfolio and deploy mobile crews capable of working night and weekend shifts on short notice. DELTABLOC leads in high-containment concrete barriers, leveraging its patented SafeLink transitions that integrate H4b blocks with third-party rails, minimizing the need for custom taper sections. Saferoad offers a diverse range of products, including W-beam, cable barriers, and crash cushions, and has expanded its market presence with CrashGuard attenuators, which were added to the BASt list in 2024, targeting tunnel portals and interchange gores. REBLOC focuses on low-intrusion VI-class modules, particularly in bridge applications where space optimization is critical.

Second-tier specialists have established niches within the market. Brüninghoff’s FRP HEI Protect barrier, which is 40% lighter than steel alternatives, is preferred for long-duration work zones where frequent repositioning is required. Mobile Schutzwände’s ProTec 161 barrier is popular in rental markets due to its lightweight design, with a mass of 315 kg per meter, allowing transportation on standard flatbeds and reducing haulage costs for multi-site projects. Passco specializes in motorcyclist skirting boards and has enhanced its offerings by bundling clip-on units with refurbishment kits, increasing the value of orders per kilometer. These specialized players contribute to innovation within the industry while providing road agencies with a broader range of options.

Technology advancements, certification timelines, and after-sales support are critical factors shaping competition in the market. Patents related to tensioning mechanisms, fiber-reinforced concrete, and energy-absorption cells provide established players with a competitive edge. Smaller entrants often license crash-test reports to expedite BASt certification. Across the industry, companies are pursuing preventive-maintenance service contracts, which secure customer relationships for 10-15 years and provide stable revenue streams. As roadside safety barriers increasingly incorporate sensors, future competition may shift towards the development of data dashboards, complementing traditional steel and concrete solutions.

Germany Roadside Safety Barriers Construction Industry Leaders

DELTABLOC Deutschland GmbH

Saferoad RRS GmbH

Hill & Smith Ltd (Brifen Germany)

HEINTZMANN Traffic Systems GmbH

Peter Berghaus GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Autobahn GmbH des Bundes – Niederlassung Ost awarded a framework contract for vehicle restraint systems (Fahrzeugrückhaltesysteme) covering 2026–2028 across Saxony, Saxony-Anhalt, and Thuringia, valued at EUR 42 million (USD 45.5 million), encompassing barrier renewal on A4 (km 171.70–114.10, km 171.70–239.20), A9 (km 167.04–196.60), A7 (km 14.30–100.60), and A71 corridors.

- January 2026: Autobahn GmbH – Niederlassung Nordwest awarded two contracts for the AD Kirchheim A7 Ost project: Los 5 (Fahrzeug-Rückhaltesysteme) for vehicle restraint systems and Los 3 (Lärmschutzanlagen) for noise protection installations, indicating integrated barrier-noise wall deployments

- August 2025: The A100 eastern extension in Berlin opened following a EUR 721 million (USD 782 million) investment, incorporating 14 kilometers of bridge-mounted barriers rated H2 and H4a, plus 22 crash cushions at gantry bases and off-ramp gore points.

- May 2025: Kapsch TrafficCom and Autobahn GmbH des Bundes completed Phase 1 of a partnership to deploy 1,000 ITS Roadside Stations (IRS) on mobile barrier panels across 8,600 kilometers of German highways, representing Europe's largest Cooperative Intelligent Transport Systems (C-ITS) project. The system broadcasts roadworks warnings via ETSI/C-Roads-based WLAN, with data integrated into Autobahn GmbH's backend and made available at the National Access Point.

Germany Roadside Safety Barriers Construction Market Report Scope

| Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) |

| Cable Barrier Systems |

| Crash Cushions & Impact Attenuators |

| Others (Motorcyclist protection systems, hybrid/specialty barriers, emerging safety solutions) |

| Steel |

| Concrete |

| Plastic & Composite |

| Others (Aluminum, rubber-based materials, composite blends, recycled materials) |

| Highways & Expressways |

| Urban Roads & Streets |

| Bridges & Flyovers |

| Others (Rural roads, industrial/private roads, parking areas, tunnels, temporary traffic zones) |

| New Installation |

| Renovation / Retrofit / Repair |

| Berlin |

| Munich |

| Frankfurt |

| Hamburg |

| Rest of Germany |

| By Product Type | Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) | |

| Cable Barrier Systems | |

| Crash Cushions & Impact Attenuators | |

| Others (Motorcyclist protection systems, hybrid/specialty barriers, emerging safety solutions) | |

| By Material | Steel |

| Concrete | |

| Plastic & Composite | |

| Others (Aluminum, rubber-based materials, composite blends, recycled materials) | |

| By Application | Highways & Expressways |

| Urban Roads & Streets | |

| Bridges & Flyovers | |

| Others (Rural roads, industrial/private roads, parking areas, tunnels, temporary traffic zones) | |

| By Installation Type | New Installation |

| Renovation / Retrofit / Repair | |

| By Cities | Berlin |

| Munich | |

| Frankfurt | |

| Hamburg | |

| Rest of Germany |

Key Questions Answered in the Report

How large is public spending on German bridge-protection barriers through 2031?

Planned bridge renewals push the Germany roadside safety barriers construction market size tied to bridges toward USD 300 million cumulatively, anchored by thousands of H4b pier-protection modules.

Which product type grows fastest after 2026?

Cable barriers expand at a 4.98% CAGR because freight corridors retrofit narrow medians to higher containment classes.

Why are composite barriers gaining traction?

Fiber-reinforced-polymer panels weigh 40% less than steel, cut lane-closure hours, and meet EN 1317 crash tests, making them attractive for long-duration work zones.

What keeps new designs from reaching the market quickly?

BASt homologation requires full-scale crash tests and technical reviews that often last 18–24 months, delaying procurement eligibility.

Which city will add the most new high-containment blocks by 2031?

Hamburg, driven by the Köhlbrandbrücke replacement and Elbtunnel approaches, is forecast to lead growth with a 5.31% CAGR in installed length.

Page last updated on: