United States Roadside Safety Barriers Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

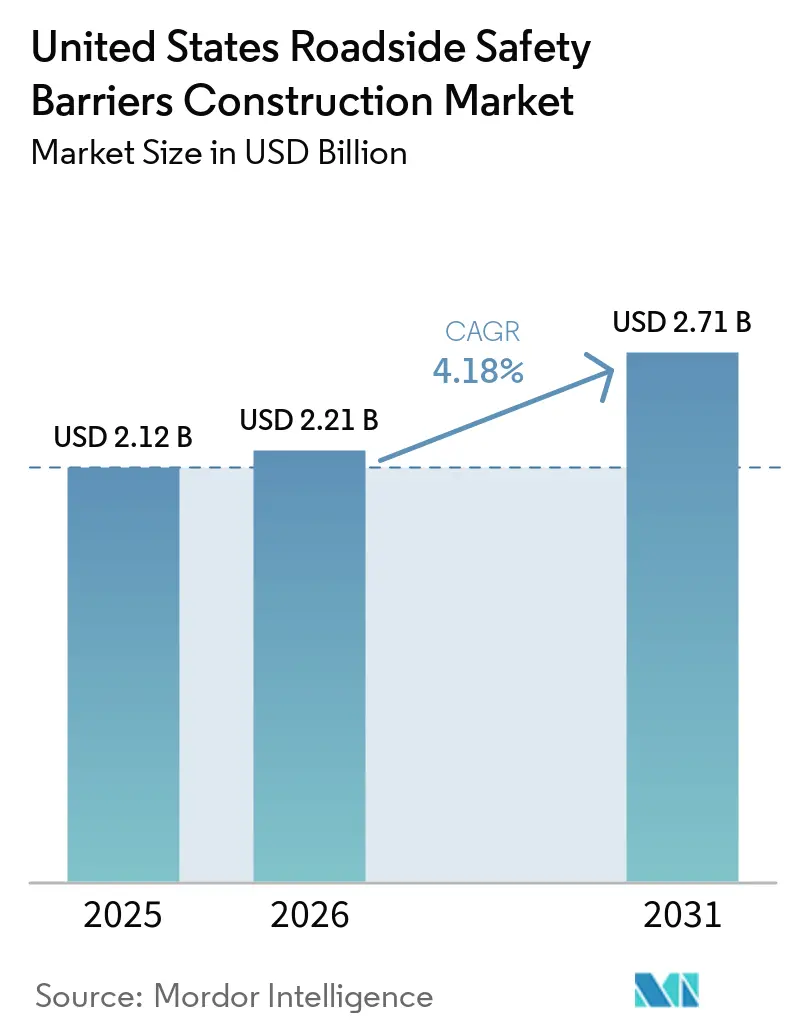

| Base Year Market Size (2025) | USD 2.12 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 2.71 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

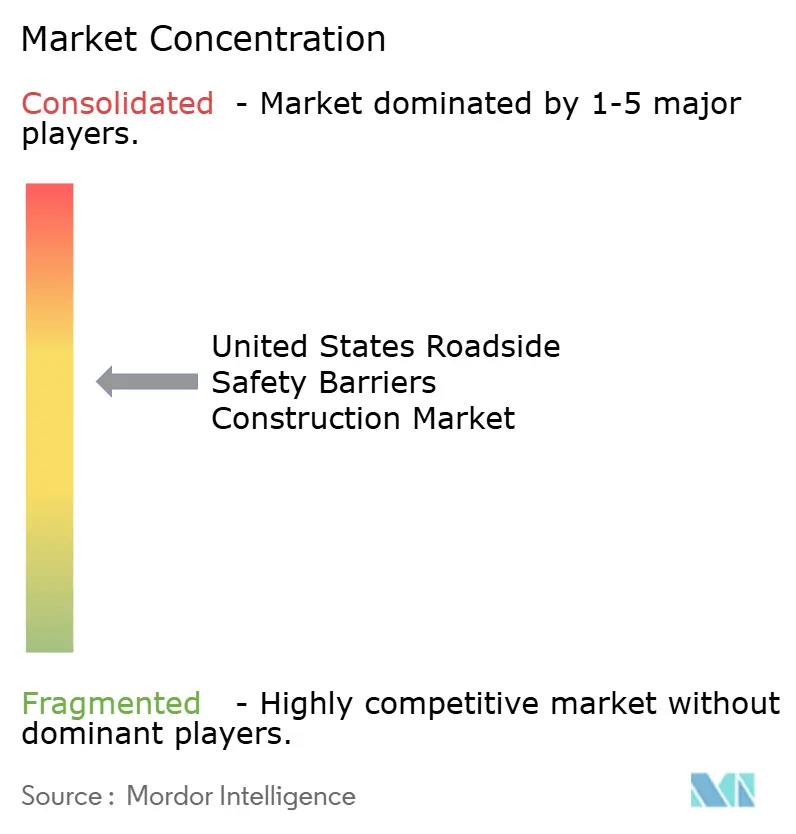

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Roadside Safety Barriers Construction Market Analysis by Mordor Intelligence

The United States Roadside Safety Barriers Construction Market size was valued at USD 2.12 billion in 2025 and is estimated to grow from USD 2.21 billion in 2026 to reach USD 2.71 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031). Federal highway appropriations under the Infrastructure Investment and Jobs Act (IIJA), increased state match funding, and the mandatory replacement of pre-2016 systems as per the Manual for Assessing Safety Hardware (MASH) are driving a multi-year retrofit pipeline. State Departments of Transportation (DOTs) are focusing on high-crash corridors, expediting purchase orders for cable and composite barriers that demonstrate improved performance on median slopes and in corrosive coastal environments. At the same time, material cost volatility, such as an 18% spike in hot-rolled coil steel prices in early 2025, has led several contractors to adopt performance-based maintenance contracts. These contracts help lock in pricing and transfer lifecycle risk to suppliers. Acquisition activity, exemplified by RoadSafe Traffic Systems, highlights that scale and product diversity have become key strategic advantages, surpassing price as the primary differentiator.

Key Report Takeaways

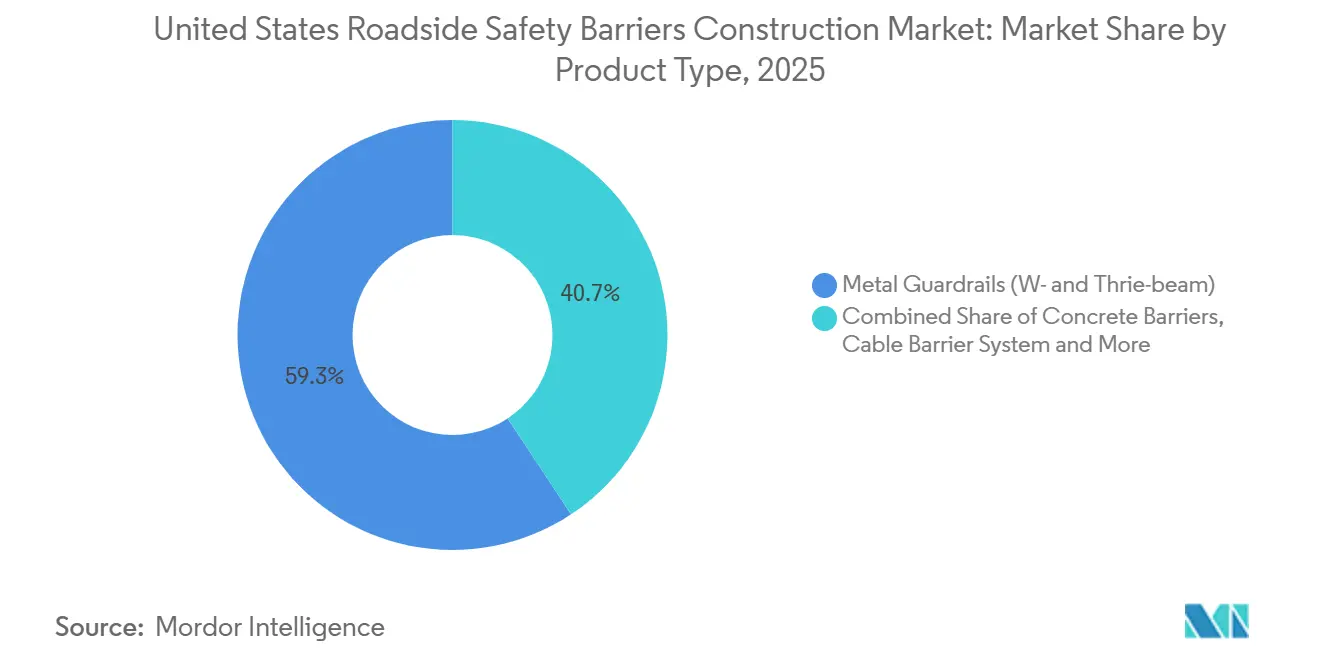

- By product type, metal guardrails held 59.3% of the United States roadside safety barriers construction market share in 2025, whereas cable barrier systems are projected to expand at a 4.89% CAGR between 2026 and 2031.

- By material, steel accounted for 66.4% of the United States roadside safety barriers construction market size in 2025, while plastic and composite formulations posted the fastest forecast growth at 5.16% CAGR between 2026 and 2031.

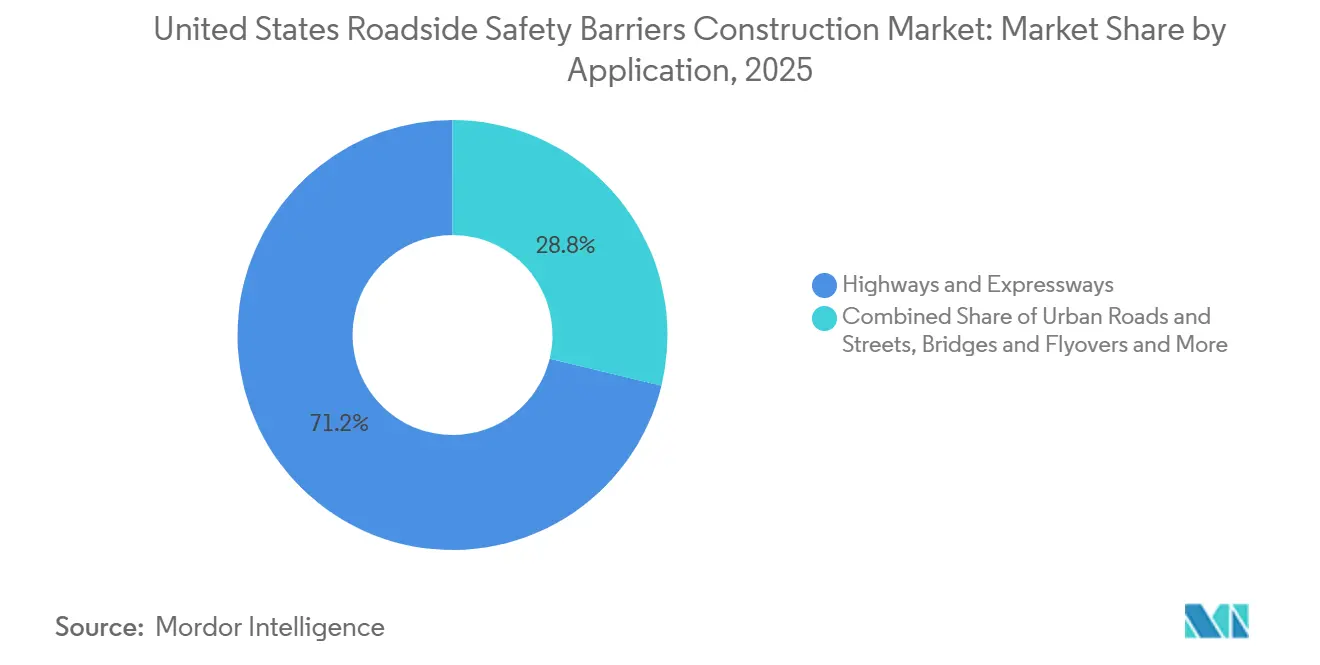

- By application, highways and expressways led with 71.2% revenue contribution in 2025; bridges and flyovers are forecast to record a 5.09% CAGR between 2026 and 2031.

- By installation type, new construction represented 56.7% of 2025 revenue, yet renovation and retrofit activities are advancing at a 4.61% CAGR between 2026 and 2031.

- By State, texas captured 19.6% of 2025 spending, whereas Florida is expected to be the fastest-growing geography with a 5.21% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Roadside Safety Barriers Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing highway modernization and infrastructure upgrade programs | +1.2% | Nationwide, the highest is in Texas, California, and Florida | Long term (≥ 4 years) |

| Strict road safety regulations are making barrier installation mandatory | +1.0% | National Highway System routes | Medium term (2–4 years) |

| High vehicle ownership and traffic density are pushing crash-protection demand | +0.8% | Urban corridors in California, New York, and Illinois | Medium term (2–4 years) |

| Rising public investment in road-safety projects | +0.7% | States with active HSIP grants | Long term (≥ 4 years) |

| Adoption of advanced impact-resistant technologies | +0.5% | Early adoption in California, Texas, and Washington | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ongoing Highway Modernization and Infrastructure Upgrade Programs

The Federal IIJA allocations provide each state with a consistent stream of highway capital funding through fiscal year 2026. Major jurisdictions, such as Texas with its USD 104.2 billion Unified Transportation Program and Florida with its USD 62.5 billion Work Program, are supplementing these funds with state fuel-tax revenues[1]Federal Highway Administration, “Manual for Assessing Safety Hardware Implementation Policy,” fhwa.dot.gov . Due to the high benefit-cost ratios of safety countermeasures, many resurfacing or widening contracts now include the installation of new guardrails or median cables. This trend is significantly expanding the United States roadside safety barriers construction market beyond just greenfield projects. The bundling of such projects helps mitigate the impact of single-program budget fluctuations and ensures steady contractor backlogs throughout the paving season. Bid calendars indicate demand peaks in spring and fall, providing manufacturers with better visibility and enabling steel mills to plan coil production accordingly.

Strict Road Safety Regulations Making Barrier Installation Mandatory

The MASH 2016 cut-off dates prohibited federal reimbursement for non-compliant roadside hardware after December 2019. This requirement compelled Departments of Transportation (DOTs) to inventory, prioritize, and replace outdated systems across all National Highway System routes[2]Federal Highway Administration, “Highway Safety Improvement Program Funding Tables,” fhwa.dot.gov . Currently, only devices with an FHWA eligibility letter can be specified, effectively excluding untested products and solidifying market share for manufacturers with extensive crash-test data. States have incorporated these federal protocols into their standard drawings, ensuring that every resurfacing project automatically includes a barrier review. Collectively, these compliance regulations have transformed barrier turnover from an optional upgrade into a statutory requirement, driving a consistent retrofit cycle through 2031.

High Vehicle Ownership and Traffic Density Pushing Crash-Protection Demand

In 2023, vehicle miles traveled reached 3.26 trillion and continued to increase by 2025, intensifying pressure on urban Interstates that are already operating near capacity. The growing prevalence of heavier light-truck fleets has impacted crash dynamics, prompting Departments of Transportation (DOTs) to adopt Thrie-beam or high-tension cable systems capable of absorbing higher kinetic loads. Additionally, frequent barrier strikes on congested road segments have shortened maintenance cycles from the traditional five-year interval to as little as 18 months. This accelerated wear rate has driven increased demand for replacement rails, posts, and anchorage hardware, contributing to the growth of the aftermarket segment within the United States roadside safety barriers construction market.

Rising Public Investment In Road-Safety Projects

The Highway Safety Improvement Program (HSIP) allocations amounted to USD 3.177 billion in fiscal 2025 and USD 3.246 billion in fiscal 2026, providing states with a dedicated safety fund often directed toward median cable barriers due to their favorable benefit-cost ratios. Additionally, the Safe Streets and Roads for All (SS4A) initiative contributes USD 1 billion annually for local projects, which may include pedestrian-friendly crash cushions or low-deflection concrete walls. As these programs reimburse up to 90% of eligible costs, local agencies that previously lacked budgets for barriers are now entering the procurement process. This expansion has increased the customer base beyond state Departments of Transportation (DOTs), driving overall market growth.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installation, repair, and lifecycle costs | −0.6% | Nationwide, sharper in low-volume rural counties | Medium term (2–4 years) |

| Aging road infrastructure is creating a retrofit backlog | −0.4% | Concentrated in the Northeast and the Upper Midwest | Long term (≥ 4 years) |

| Lengthy approval processes are delaying project starts | −0.3% | Varies by state DOT | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Installation, Repair, and Lifecycle Costs of Barrier Systems

The unit price represents only the initial cost; lane-closure traffic delays often double the actual project expenses on urban Interstates. Additionally, hot-rolled coil price spikes in 2025 led to several bids exceeding engineer estimates[3]U.S. Bureau of Labor Statistics, “Producer Price Index (PPI): Metals and Metal Products—Hot-Rolled Steel Sheet and Strip,” bls.gov/ppi. Cable barriers require periodic re-tensioning, with each cycle necessitating certified crews, specialized jacks, and rolling lane closures, which increase ownership costs. While concrete walls have a longer lifespan, their installation requires cranes, significantly raising mobilization expenses. These economic factors have led some rural districts to delay upgrades on low-traffic alignments, reducing the total addressable mileage during the forecast period.

Aging Road Infrastructure Creating A Retrofit Backlog

The American Society of Civil Engineers rated U.S. roadways at a C- in 2025, identifying an estimated investment gap of USD 786 billion over 10 years. Numerous guardrail installations predating 2000 exhibit issues such as corrosion and foundation failure, while competing for funding with pavement overlays and bridge deck repairs. Since MASH requirements are limited to National Highway System routes, many county roads continue to use outdated hardware, reducing overall safety improvements and extending the timeline for retrofits beyond the projected period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cable Systems Gain on Median Applications

Metal guardrails, primarily W-beam and Thrie-beam, accounted for 59.3% of the United States roadside safety barriers construction market share in 2025. This dominance is attributed to their inclusion in major state standard drawings and their proven crash performance. The popularity of these guardrails is driven by galvanized steel's balance of strength and cost-effectiveness. However, the market is gradually shifting toward high-tension cable systems, which are better suited for handling slopes where rigid concrete barriers are less effective. Cable barriers also offer the advantage of reduced post-strike downtime, as damaged wires can be re-tensioned in less than a day—an essential feature for Interstates carrying over 150,000 vehicles daily. Contractors have adapted by pre-assembling anchor kits off-site, reducing field labor by up to 20% and minimizing work-zone durations.

Cable systems are projected to grow at a compound annual growth rate (CAGR) of 4.89%, the fastest among product segments. States like Texas are replacing grassy median W-beams with three-strand cable systems along the I-35 and I-45 corridors. Meanwhile, portable precast concrete walls remain critical in construction work zones where minimal deflection is required. However, their higher freight and crane costs limit their use on rural highways. In the crash cushion segment, innovation continues to emerge. For instance, TrafFix Devices introduced the non-gating Delta TL-2+ in 2025, targeting urban areas where space constraints prevent the use of traditional sand barrels. Overall, the varying performance requirements based on geography and alignment ensure a diverse product landscape, maintaining a competitive market dynamic through 2031.

By Material: Composites Challenge Steel's Corrosion Dominance

Steel constituted 66.4% of the 2025 revenue in the United States roadside safety barriers construction market, supported by established mills, galvanizing processes, and extensive field data. However, salt spray in coastal states accelerates corrosion, even on hot-dip galvanized coatings. This has led Departments of Transportation (DOTs) in states like Florida and Louisiana to test corrosion coupons, which have reduced service-life estimates to less than 12 years for certain causeways. This accelerated wear is driving the demand for lighter, corrosion-resistant materials.

Composite systems are anticipated to grow at a compound annual growth rate (CAGR) of 5.16%, surpassing all other material categories as sustainability metrics become a key factor in bid evaluations. Transpo Industries has implemented pilot installations of its recycled-plastic guardrails along California’s Highway 1 near Monterey Bay, where steel posts typically corrode within five years due to sea spray. Meanwhile, Nucor’s USD 3.1 billion sheet mill in West Virginia, expected to commence operations by late 2026, aims to counter this trend by reducing domestic coil costs and improving lead times for steel rail fabricators. The competition between advancements in composite materials and cost reductions in steel production is expected to shape material preferences throughout the forecast period.

By Application: Bridge Retrofits Accelerate Faster Than Highway Baseline

Highways and expressways accounted for 71.2% of 2025 installations, highlighting the extensive lane-mile inventory of the Interstate System and the significant reliance on federal reimbursements. Interstate retrofit contracts typically combine MGS W-beam barriers on roadsides with high-tension cables in medians to mitigate cross-median collisions at speeds of up to 70 miles per hour. Due to the need for continuous barriers over extended stretches, installation volumes remain substantial; however, growth is expected to stabilize at low single-digit rates.

In contrast, bridges and flyovers are projected to achieve a 5.09% compound annual growth rate (CAGR) through 2031, marking the fastest growth among application categories. According to the American Society of Civil Engineers, 7.5% of bridges are classified as structurally deficient, and every deck rehabilitation necessitates barrier replacement in compliance with MASH Test Level-4 or Level-5 standards. The inclusion of custom post spacing and deck-edge anchorage increases the average unit value, driving revenue growth despite lower mileage compared to open-road segments. Urban arterial projects further add complexity by incorporating pedestrian fencing and decorative panels, creating high-margin opportunities for fabricators capable of meeting both safety and aesthetic requirements.

By Installation Type: Retrofit Pipelines Extend Beyond New Construction

New installations accounted for 56.7% of the projected 2025 revenue, primarily due to greenfield capacity expansions in Texas and Florida, which continue to dominate bid calendars. Contractors typically install barrier hardware after the final lift paving, enabling a single mobilization and reducing traffic control costs. These operational efficiencies help maintain the dominance of new-build projects, even as the overall network matures.

Retrofit activities, however, are growing at a compound annual growth rate (CAGR) of 4.61%, driven by MASH (Manual for Assessing Safety Hardware) mandates that apply to any pavement overlay on National Highway System mileage. Retrofits yield higher unit margins as they require field crews to remove existing foundations, install new posts, and often conduct work during nighttime hours to minimize daytime traffic disruptions. Additionally, performance-based maintenance contracts are incorporating retrofit requirements, transferring risk to private concessionaires, and promoting bulk purchase agreements with major original equipment manufacturers. As a result, the growing retrofit market is creating a consistent aftermarket revenue stream for suppliers, supplementing what was previously a project-based revenue model.

Geography Analysis

Texas accounted for 19.6% of the total projected 2025 spending, driven by its USD 104.2 billion Unified Transportation Program. This program provides consistent funding for barrier installations along major freight corridors such as I-35, I-45, and I-10, which handle freight volumes exceeding 25,000 trucks per day. Cable systems are the preferred technology for these median-wide layouts due to their lower cost compared to concrete and reduced post-strike maintenance requirements, which are limited to tension adjustments. This approach aligns with Texas’s asset-management priorities, emphasizing rapid roadway reopenings following crashes.

Florida is expected to achieve a compound annual growth rate (CAGR) of 5.21% through 2031, the highest among all states. This growth is primarily attributed to its USD 62.5 billion five-year Work Program, which focuses on rebuilding hurricane-affected coastal infrastructure. In these areas, MASH-compliant composite rails outperform steel due to their superior resistance to salt-spray environments. Additionally, Florida incorporates resilience metrics into procurement evaluations, prioritizing lighter, corrosion-resistant plastics that enable faster installations during limited weather windows.

California, New York, and Illinois collectively represent a second tier of infrastructure investment. California’s State Highway Operation and Protection Program is financing barrier retrofits on older Interstate corridors such as I-5 and I-80, many of which traverse densely populated urban areas. In these regions, concrete walls are used to prevent secondary crashes into adjacent structures. New York’s BRIDGE NY grants are replacing deck-edge Thrie-beams with TL-4 concrete parapets on aging viaducts, while Illinois’ Rebuild Illinois capital plan focuses on upgrading barriers on rural two-lane roads. These upgrades are particularly critical in freeze–thaw zones where timber posts have deteriorated. Collectively, these regional variations highlight the need for tailored strategies, requiring suppliers to maintain regional stocking points and secure state-specific crash-test certifications to remain competitive in the bidding process.

Competitive Landscape

Competition in the market revolves around three primary factors: speed of MASH (Manual for Assessing Safety Hardware) eligibility, material innovation, and acquisition-driven scale. Valtir (formerly Trinity Highway Products) has a robust crash-test portfolio, including the ALPHA DXM Truck-Mounted Attenuator, which received FHWA Letter CC-173 in 2023. This approval allows nationwide specification without additional state testing. Gregory Industries counters by integrating its guardrail lines with Hill & Smith’s Smart Cushion telemetry, which alerts maintenance teams within minutes of an impact. This capability reduces response times and positions the companies as leaders in technology adoption.

Scale economics are evolving as RoadSafe Traffic Systems consolidates regional installers. Its fifteenth acquisition in June 2024 established a nationwide presence, enabling the company to self-perform traffic control, rent temporary concrete walls, and fabricate specialty steel products. Smith-Midland leverages its patented J-J Hooks system to secure multi-year rental contracts for long-term megaprojects, such as the Hampton Roads Express Lanes. This demonstrates that rental models are becoming competitive with outright purchases for temporary infrastructure. Additionally, Nucor’s upcoming West Virginia sheet mill will ensure a stable domestic coil supply, mitigating risks from import disruptions and providing steel-based barrier manufacturers with a pricing advantage over composite alternatives.

Innovation clusters continue to attract smaller specialists. TrafFix Devices introduced the Delta TL-2+ crash cushion in 2025, targeting a 50 miles-per-hour urban niche where space constraints are critical. Transpo Industries leverages sustainability by incorporating recycled ocean plastics into its products, appealing to cities with climate-focused procurement policies. Meanwhile, modular start-ups utilizing 3-D printing to produce composite parapets on-site are showcasing rapid prototype-to-installation capabilities. However, these start-ups still require FHWA approvals before scaling operations nationally. Overall, the competitive landscape remains moderately concentrated but dynamic, with established players defending high-volume steel and concrete product lines while innovators focus on high-margin niche markets.

United States Roadside Safety Barriers Construction Industry Leaders

Valtir (formerly Trinity Highway)

Lindsay Corporation (Barrier Systems)

Valmont Industries Inc.

Hill & Smith Holding USA

Gregory Highway (Gregory Industries)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Smith-Midland Corporation secured a USD 1.84 million contract from the Georgia Department of Transportation for the I-285 project in Atlanta. The company will supply J-J Hooks precast concrete barriers designed for rapid installation during overnight lane closures, minimizing traffic disruption on one of the Southeast's most congested Interstate corridors.

- December 2025: Nucor Corporation commissioned galvanizing (300,000 tons per year) and prepaint (250,000 tons per year) lines at its Crawfordsville, Indiana facility. These lines produce coated steel coils used in W-beam and Thrie-beam guardrail manufacturing, reducing lead times for barrier fabricators serving Midwest state DOTs.

- September 2025: Smith-Midland Corporation won a USD 4 million-plus barrier rental contract for the I-64 Hampton Roads Express Lanes project in Virginia. The multi-year agreement involves deploying precast concrete barriers for work-zone protection during the express lanes construction, demonstrating the growing rental model for temporary traffic control on major infrastructure projects.

- August 2025: Valmont Industries Inc. announced USD 170 million to USD 200 million in capacity expansion investments at its Brenham, Texas and Tulsa, Oklahoma plants. These facilities produce highway safety products including guardrails and barrier systems, with the expansion aimed at meeting growing demand from TxDOT's USD 104.2 billion infrastructure program and other state projects.

United States Roadside Safety Barriers Construction Market Report Scope

| Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) |

| Cable Barrier Systems |

| Crash Cushions & Impact Attenuators |

| Others (Motorcyclist protection, hybrid, emerging) |

| Steel |

| Concrete |

| Plastic & Composite |

| Others (Aluminum, rubber, recycled blends) |

| Highways & Expressways |

| Urban Roads & Streets |

| Bridges & Flyovers |

| Others (Rural, industrial/private, parking, tunnels, temp zones) |

| New Installation |

| Renovation / Retrofit / Repair |

| Texas |

| California |

| Florida |

| New York |

| Illinois |

| Rest of US |

| By Product Type | Metal Guardrails (W-beam, Thrie-beam) |

| Concrete Barriers (Jersey, F-shape) | |

| Cable Barrier Systems | |

| Crash Cushions & Impact Attenuators | |

| Others (Motorcyclist protection, hybrid, emerging) | |

| By Material | Steel |

| Concrete | |

| Plastic & Composite | |

| Others (Aluminum, rubber, recycled blends) | |

| By Application | Highways & Expressways |

| Urban Roads & Streets | |

| Bridges & Flyovers | |

| Others (Rural, industrial/private, parking, tunnels, temp zones) | |

| By Installation Type | New Installation |

| Renovation / Retrofit / Repair | |

| By Geography | Texas |

| California | |

| Florida | |

| New York | |

| Illinois | |

| Rest of US |

Key Questions Answered in the Report

How large will U.S. roadside barrier spending be by 2031?

The United States roadside safety barriers construction market is projected to reach USD 2.71 billion by 2031.

Which product group leads current demand?

Metal guardrails hold a 59.3% share, making them the largest revenue contributor in 2025.

What is the fastest-growing product segment?

High-tension cable barriers show the quickest expansion, rising at a 4.89% CAGR through 2031.

Which state is expected to post the highest growth?

Florida is forecast to achieve a 5.21% CAGR between 2026 and 2031 on the back of hurricane-resilience work.

How do MASH rules affect procurement?

Only MASH-compliant devices with FHWA eligibility letters qualify for federal reimbursement, effectively guiding every state DOT’s approved product list.

Are composite barriers price-competitive with steel?

Upfront costs remain higher, but life-cycle modeling shows composites reach cost parity within 10 years in coastal zones because they avoid corrosion repairs.

Page last updated on: