India Automotive Chassis Dynamometers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

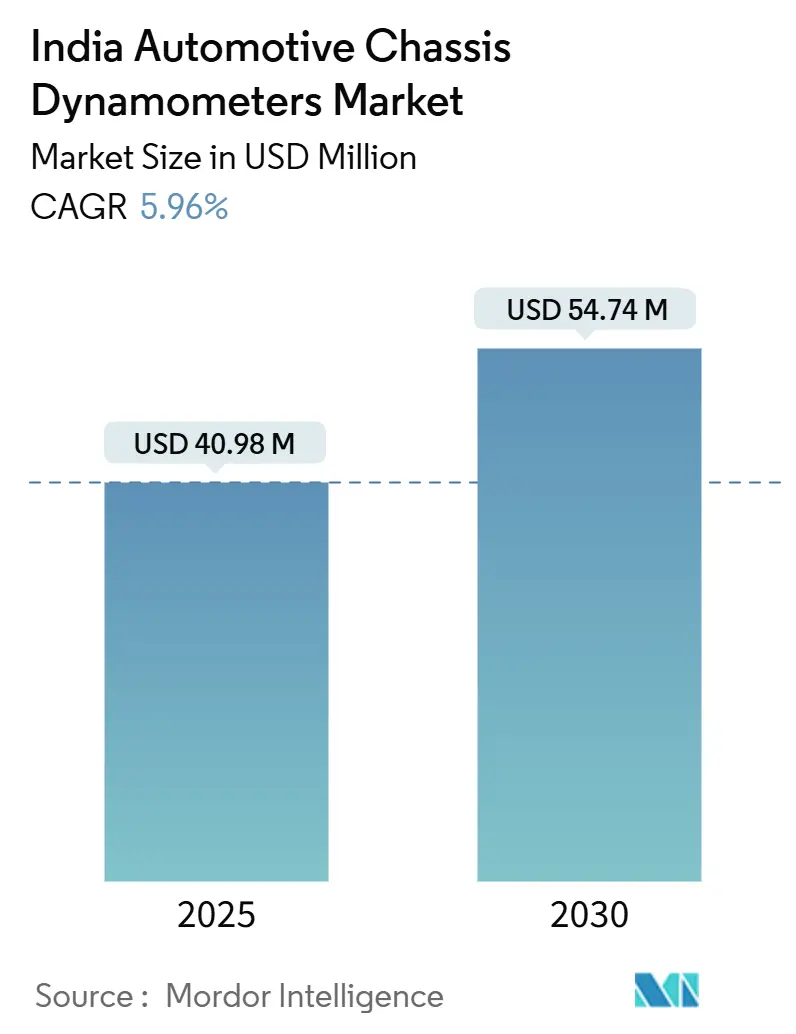

| Market Size (2025) | USD 40.98 Million |

| Market Size (2030) | USD 54.74 Million |

| Growth Rate (2025 - 2030) | 5.96% CAGR |

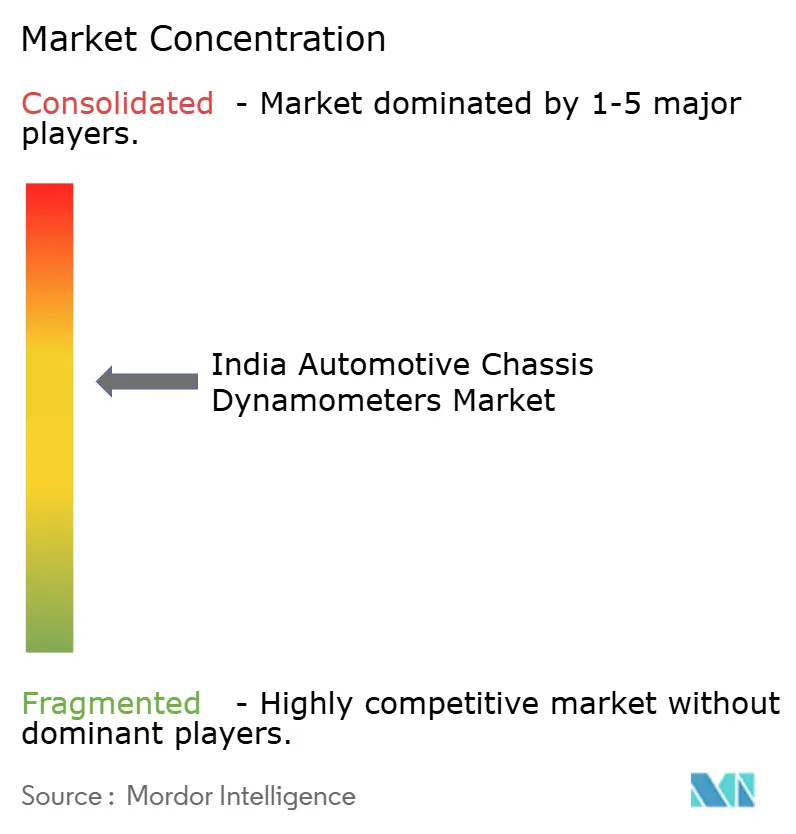

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Chassis Dynamometers Market Analysis by Mordor Intelligence

The India automotive chassis dynamometer market size is valued at USD 40.98 million in 2025 and is forecast to reach USD 54.74 million by 2030, registering a 5.96% CAGR through the period. Regulatory momentum from BS-VI to BS-VII, expanding electric-vehicle (EV) model launches, and growing export‐oriented validation requirements anchor this trajectory as laboratories and proving grounds race to modernize their test cells. Government-funded centers such as NATRAX and ICAT now provide WLTP-compliant facilities that shorten development cycles and attract overseas programs, while OEM R&D outlays have shifted decisively toward electrification. Parallel growth in tier-2 performance workshops enlarges the user base for portable rigs, even as high capital costs and the shortage of trained operators restrain broader adoption. Competitive intensity remains moderate and technology led; cloud-connected remote operation is fast becoming a hygiene factor, creating new service revenue for suppliers that combine hardware and analytics.

Key Report Takeaways

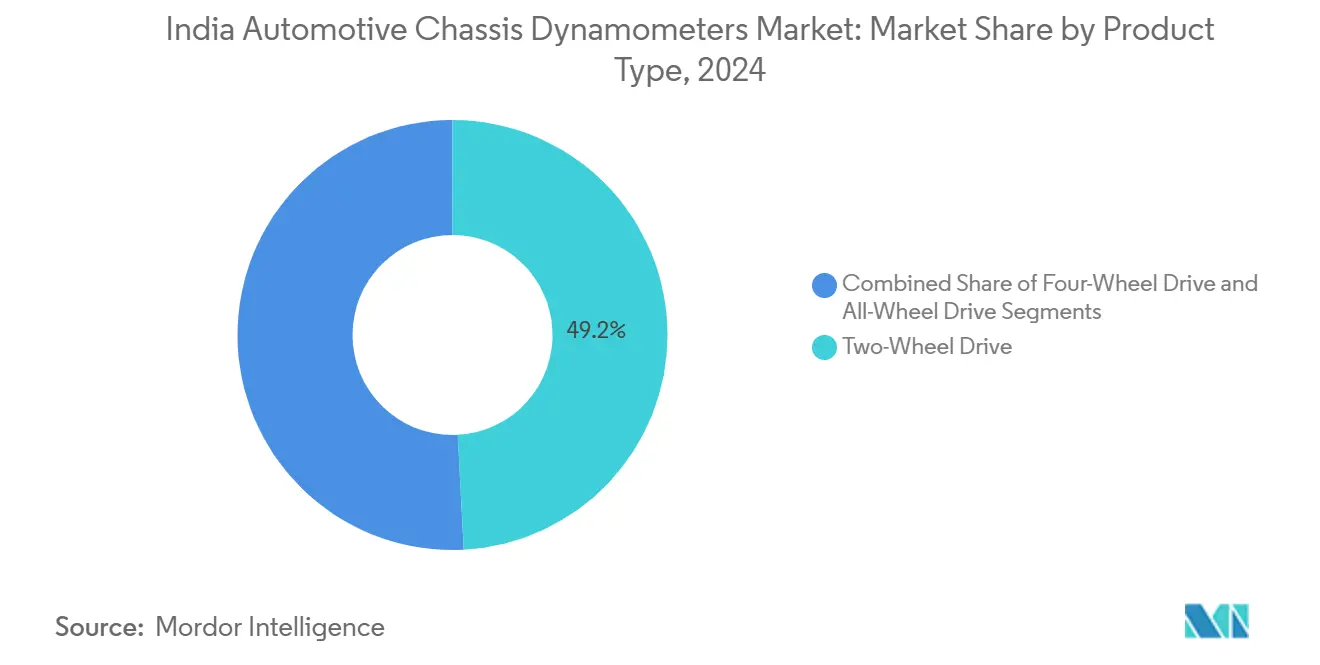

- By product type, Two-Wheel Drive systems led with 49.17% of the India automotive chassis dynamometer market share in 2024; All-Wheel Drive are projected to post the highest 7.66% CAGR to 2030.

- By application, Powertrain Testing captured 34.83% of the India automotive chassis dynamometer market size in 2024 and Electric & Autonomous Component Testing is advancing at a 10.42% CAGR through 2030.

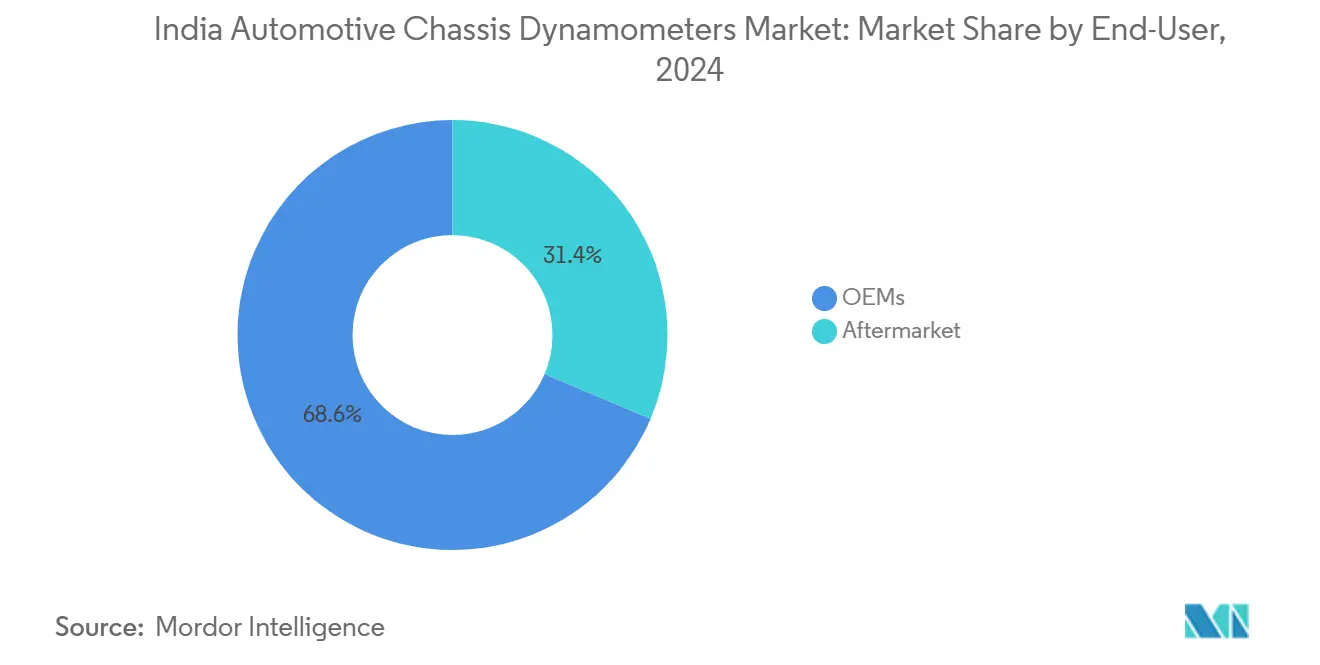

- By end-user, OEMs held 68.63% share of the India automotive chassis dynamometer market size in 2024, while the Aftermarket are projected to record a 7.46% CAGR to 2030.

- By propulsion type, Internal-Combustion Engine vehicles secured 53.26% market share in 2024; Battery Electric Vehicles are projected to expand at a 15.12% CAGR between 2025-2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with India being one of the contributors. Our global automotive chassis dynamometers market size represents that cumulative total.

India Automotive Chassis Dynamometers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter BS-VI - BS-VII Emission Norms | +1.8% | Maharashtra, Tamil Nadu, Karnataka, Gujarat, Haryana | Medium term (2-4 years) |

| EV and Hybrid Model Launches | +1.5% | Maharashtra, Karnataka, Tamil Nadu, Delhi NCR | Medium term (2-4 years) |

| WLTP and Euro-Aligned Testing | +1.2% | Maharashtra, Tamil Nadu, Gujarat, Rajasthan | Long term (≥ 4 years) |

| Government-Subsidized Innovation Hubs | +0.9% | Maharashtra, Haryana, Karnataka, Madhya Pradesh | Long term (≥ 4 years) |

| Aftermarket Performance-Tuning | +0.7% | Maharashtra, Delhi NCR, Karnataka, Punjab | Medium term (2-4 years) |

| Cloud-Connected Dynos | +0.5% | Maharashtra, Karnataka, Tamil Nadu, Telangana | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter BS-VI - BS-VII Emission Norms Accelerate Lab & In-Use Compliance Testing Demand

India’s move toward BS-VII standards, signaled by the transport ministry for 2025-2027 introduction, makes continuous pollutant monitoring mandatory and doubles chassis dynamometer workload as real-driving-emission cycles run alongside traditional lab tests[1]Autocar India Staff, “Real Driving Emissions Norms Explained,” autocarindia.com. OEMs now schedule additional endurance sweeps to calibrate updated OBD systems, while component suppliers validate low-particulate brake materials on inertia rollers. Laboratories in Pune, Chennai, and Bangalore face capacity crunches that sustain long-term equipment orders, prompting test-service providers to lease mobile dynos to smaller firms.

Surge in EV & Hybrid Model Launches Requiring Multi-Propulsion Chassis Validation

Tight EV rollout timelines force manufacturers to characterize regenerative braking, battery thermal behavior, and multi-motor torque splits on chassis rigs instead of engine dynos. HORIBA’s 4×4 compact unit, installed at ARAI in 2024, allows seamless switch between front-, rear-, and all-wheel drive logic, cutting test cell setup time by 30%[2]Automotive Research Association of India, “Indian Emission Regulation Booklet,” araiindia.com. Start-ups in Bangalore integrate cloud dashboards so cell engineers can tune energy-consumption maps remotely, a leap that improves floor utilization for high-value WLTP cycles.

Growing Export Programs of Indian OEMs Needing WLTP & Euro-Aligned Dynamometer Testing

Passenger-car exporters now target Europe and Latin America with powertrains certified under WLTP Class 3 cycles that demand precise road-load force replication. Test centers in Chennai have added altitude simulation fans and humidity-control chambers to serve these programs, capturing contracts from SUVs built in Gujarat. Mahindra’s Born-Electric platform scheduled for 2026 release already banks 200 WLTP cycles, underscoring why exporter pipelines underpin steady capex for advanced rigs.

Government-Subsidised Innovation Hubs Boosting Investment in Vehicle R&D Centres

Capital subsidies under NATRiP unlock 20-35% cost savings for labs that install new chassis dynamometers in Madhya Pradesh and Haryana[3]Press Information Bureau, “A World Class Automotive Testing Centre,” pib.gov.in. The 4,140-acre NATRAX site now runs endurance loops for autonomous shuttles, creating spill-over demand for linked dyno cells that validate over-the-air updates before test-track trials. Government visibility attracts tier-2 vendors who co-locate near these hubs, raising equipment demand beyond the primary OEM base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Maintenance Cost | -1.9% | Uttar Pradesh, West Bengal, Rajasthan, Andhra Pradesh | Medium term (2-4 years) |

| Lengthy Import Lead-Times | -1.2% | Maharashtra, Tamil Nadu, Gujarat, Karnataka | Short term (≤ 2 years) |

| ICE Passenger-Car Sales Slowdown | -0.9% | Maharashtra, Tamil Nadu, Gujarat, Haryana | Short term (≤ 2 years) |

| Shortage Of Skilled Test Engineers | -0.7% | Karnataka, Tamil Nadu, Maharashtra, Haryana | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX & Maintenance Cost Limits Adoption by Tier-2/3 Suppliers

Advanced four-wheel rigs cost upward of USD 1.2 million, putting them beyond the reach of many component vendors that average annual turnovers under USD 40 million. Ongoing maintenance contracts at 6-8% of purchase price weigh on margins, and downtime penalties deter smaller firms from purchasing. Leasing models emerge, yet finance houses still consider used-value recovery uncertain, slowing deal closures in emerging hubs like Sanand and Neemrana.

Lengthy Import Lead-Times for Advanced Four-Wheel-Drive Rigs

Precision roller assemblies and torque transducers still arrive from Europe or Japan. Customs clearance plus local homologation push delivery cycles to 9-12 months, disrupting project gates for new SUV platforms. Domestic machining attempts suffer quality drift, forcing import reliance that locks up buyer capital in advances and letters of credit. Government push for “Make in India” test hardware remains early stage, so schedule risk persists for buyers across states.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Two-Wheel Drive Retains Scale While All-Wheel Drive Accelerates

Two-Wheel Drive rigs dominate thanks to lower price points and suitability for mass-market hatchbacks, yet All-Wheel Drive demand swells with premium crossovers and EVs. The India automotive chassis dynamometer market size for All-Wheel Drive units is projected to climb from USD 10.4 million in 2025 to USD 15.1 million by 2030 at a 7.66% CAGR, reflecting OEM platform shifts. Suppliers respond with modular roller beds that upgrade from 2×2 to 4×4 without civil-work changes, ensuring asset longevity.

Continuous software updates help older 2×2 rigs simulate synthetic rear-axle loads, keeping them relevant for entry platforms and emissions-only tasks. All-Wheel Drive acceleration rewires service footprints too, as tuners pivot from petrol hot-hatches toward dual-motor EVs needing synchronized wheel speed control. This functional leap compels dyno makers to add torque vectoring emulation and fast-switch drives that tolerate 20,000-rpm e-axle speeds. In the medium term, hybrid SUV rollouts are likely to sustain mixed demand for 2×2 emissions runs plus 4×4 powertrain calibration work.

By Application: Powertrain Testing Holds Ground Against Electric Component Surge

Powertrain Testing continues to anchor lab utilization tables because BS-VI OBD updates and BS-VII prep retain engine-dyno style runs on chassis cells for correlation. It commands 34.83% of 2024 revenue but gives ground to Electric & Autonomous Component Testing, whose 10.42% CAGR pushes share from 11% in 2024 to an expected 17% by 2030. Battery-drain sweeps, range validation, and ADAS sensor checks occur under climatic chambers mated to chassis rollers, encouraging labs to invest in multi-physics data acquisition.

Electric component validation widens the client base to battery-pack integrators and lidar start-ups, both keen on quick subsystem checks before track trials. In response, test-service firms bundle sub-hour slot rentals with high-speed data exports, creating new revenue layers that cushion cyclical ICE volumes. The India automotive chassis dynamometer market share for traditional emissions testing thus slips gradually but remains material through 2030 because BS-VII adds brake-particle count protocols.

By End-User: OEMs Seize Scale While Aftermarket Builds Momentum

OEMs own more than two thirds of installed chassis-dyno capacity, driven by mandatory certification cycles and global export ambitions. Multi-line facilities at Pune, Chennai, and Hosur now run three shifts to absorb EV workload, justifying fresh capex on high-speed cooling fans and battery emulators. The segment’s hold softens slightly as performance workshops gain traction; aftermarket rigs grow at 7.46% CAGR, helped by modular eddy-current packages that plug into standard three-phase feeds.

Workshop owners bundle dyno pulls with ECU flash services, leaning on cloud data to benchmark gains. Fleet operators also rent dyno time to audit fuel-economy after overhauls. These users favor subscription pricing, paying per test rather than owning rigs. Suppliers cultivate this pool through mobile units mountable in 40-ft containers, expanding geographic reach to tier-2 cities.

By Propulsion Type: ICE Still Leads but Battery Electric Vehicles Surge

Internal-Combustion Engine vehicles keep 53.26% share in 2024; however, share drops to 41% by 2030 as Battery Electric Vehicles triple their test-cell hours. The India automotive chassis dynamometer market size for Battery Electric validation is on course to jump past USD 12 million by 2030 on a 15.12% CAGR. Hybrid Electric platforms remain bridge technologies that sustain complex testing until 2028, while fuel-cell pilots near Delhi explore hydrogen refueling logistics ahead of scale-up.

BEV testing introduces fresh challenges: brake-regen smoothness, thermal runaway checks, and noise-vibration analysis without combustion masking. Labs equip rigs with high-dynamic torque motors and 1,000 Hz data loggers to capture inverter oscillations. Software updates arrive quarterly, so service contracts now embed over-the-air patch management clauses that cement supplier revenue beyond equipment sales.

Geography Analysis

Maharashtra commands majority share of the India automotive chassis dynamometer market, underpinned by dense OEM clusters in Pune and Nagpur, where HORIBA opened a greenfield plant in July 2024. The state aligns with BS-VII pilot programs and houses India’s largest homologation centre, driving steady CAGR. Laboratories here benefit from proximity to tooling suppliers and engineering talent, shortening commissioning loops.

Tamil Nadu market hold is supported by Chennai’s “Detroit of Asia” stature and state EV incentives that lure battery manufacturers. Recent expansions at ICAT’s coastal annex and private proving grounds near Sriperumbudur created a pipeline for next-gen four-wheel-drive rigs, particularly for export SUVs requiring WLTP coastal-humidity cycles. The region also attracts chipset firms that use chassis rollers for sensor fusion tests on Level-2 ADAS prototypes.

Karnataka contributes significantly, fueled by Bangalore’s convergence of software talent and EV start-ups. R&D centers there retrofit legacy dynos with AI-edge controllers that mirror digital-twin parameters, fostering collaboration with cloud-computing majors. Gujarat's market is anchored by Sanand’s vehicle plants and the state’s policy that refunds 12% of testing-equipment capex within three years. Emerging clusters in Madhya Pradesh and Rajasthan ride on NATRAX’s halo effect, while Uttar Pradesh courts suppliers with land subsidies yet lags due to skill gaps and logistics distance from ports.

Coverage of the automotive chassis dynamometers market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for China, Japan, United States, and South Korea, each shaped by local operating conditions.

Competitive Landscape

The India Automotive Chassis Dynamometer Market exhibits moderate concentration with established global players maintaining technological leadership while facing intensifying competition from emerging automation solutions. The top 5 players differentiate through integrated software suites and local support networks that shorten mean-time-to-repair. Domestic fabricators occupy niches in low-inertia motorcycle rigs but lack the global safety certifications demanded by export programs.

HORIBA’s 2024 Nagpur factory adds local assembly for roller beds and power absorbers, trimming import duty exposure and pushing delivery lead-times below 14 weeks. AVL upgrades its Chennai center with cloud-native test automation that allows European engineers to monitor Indian cells in real time, reinforcing its value proposition for export homologation. Meidensha’s Dynapack line wins orders from EV start-ups by promising 20,000-rpm hub-coupled testing without wheel-slippage risk, a critical factor for torque-rich e-axles.

Competitive battleground shifts toward services: predictive-maintenance analytics, digital-twin correlations, and over-the-air calibration updates now drive recurring revenue. Suppliers partner with telecom operators to secure low-latency links, bundling 5-year data plans with hardware. White-space opportunities appear in portable chassis dynos targeting racing academies and municipal fleets. New entrants leverage open-source control stacks to undercut proprietary systems by 15%, but incumbents counter through extended warranties and bundled training to ease the chronic operator shortage.

India Automotive Chassis Dynamometers Industry Leaders

HORIBA Ltd.

AVL List GmbH

Meidensha (Dynapack)

FEV India Pvt Ltd

Dynaspede Integrated Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: HORIBA inaugurated a hydrogen internal-combustion engine test cell at its Pune technical center, enabling chassis-based H2-ICE validation.

- July 2024: Union minister Nitin Gadkari opened HORIBA’s greenfield Nagpur manufacturing plant, deepening local supply of chassis dynamometers.

India Automotive Chassis Dynamometers Market Report Scope

| Two-Wheel Drive |

| Four-Wheel Drive |

| All-Wheel Drive |

| Powertrain Testing |

| Emissions Testing |

| Fuel-Efficiency Analysis |

| Electric and Autonomous Component Testing |

| Research and Development |

| Others |

| OEMs |

| Aftermarket |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| By Product Type | Two-Wheel Drive |

| Four-Wheel Drive | |

| All-Wheel Drive | |

| By Application | Powertrain Testing |

| Emissions Testing | |

| Fuel-Efficiency Analysis | |

| Electric and Autonomous Component Testing | |

| Research and Development | |

| Others | |

| By End-User | OEMs |

| Aftermarket | |

| By Propulsion Type | Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| Fuel-Cell Electric Vehicles |

Key Questions Answered in the Report

What is the current value of the India automotive chassis dynamometer market?

The market stands at USD 40.98 million in 2025 and is projected to reach USD 54.74 million by 2030.

Which application segment is growing the fastest?

Electric & Autonomous Component Testing shows the fastest 10.42% CAGR through 2030 as EV and ADAS programs expand.

Which region in India will grow the quickest for chassis dynamometers?

Tamil Nadu is forecast to post the highest 6.7% CAGR thanks to its EV supply-chain incentives and export-oriented test centers.

How will BS-VII norms affect demand?

BS-VII standards introduce tighter particulate and OBD requirements, doubling validation cycles and sustaining equipment orders into 2027.

Why are All-Wheel Drive rigs gaining traction?

The rise of premium SUVs and dual-motor EVs requires synchronized roller control for accurate drivetrain testing, driving 7.66% CAGR for All-Wheel Drive systems.

Page last updated on: