India Electronic Power Steering Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

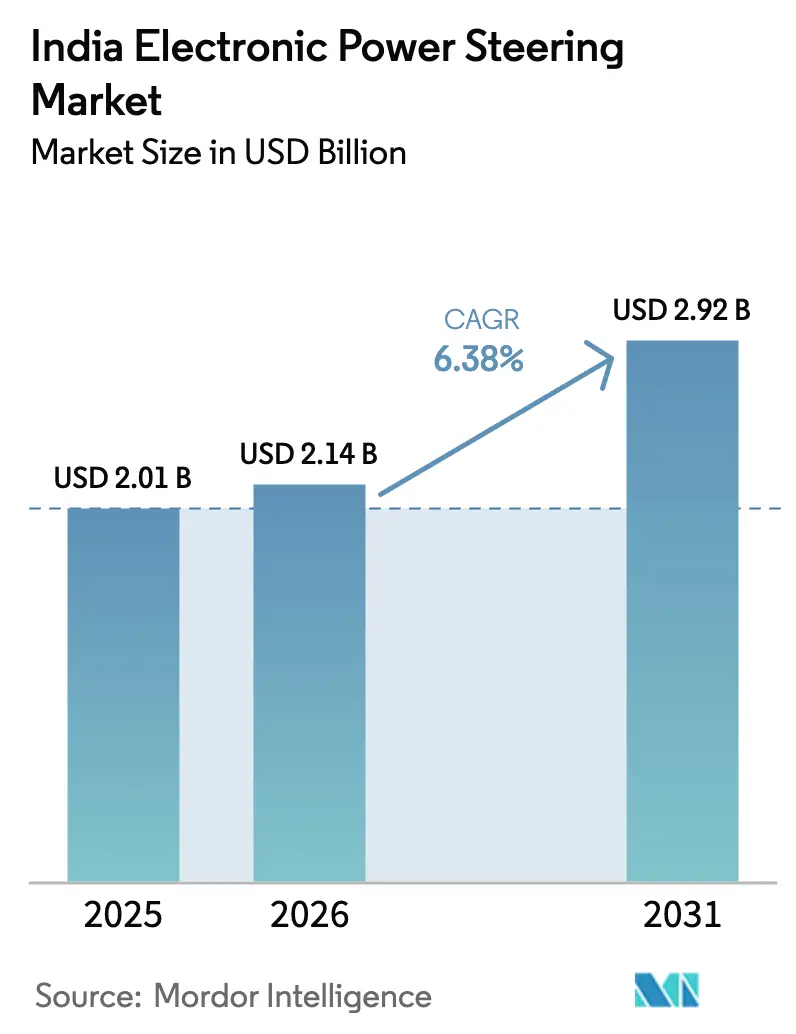

| Base Year Market Size (2025) | USD 2.01 Billion |

| Market Size (2026) | USD 2.14 Billion |

| Market Size (2031) | USD 2.92 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

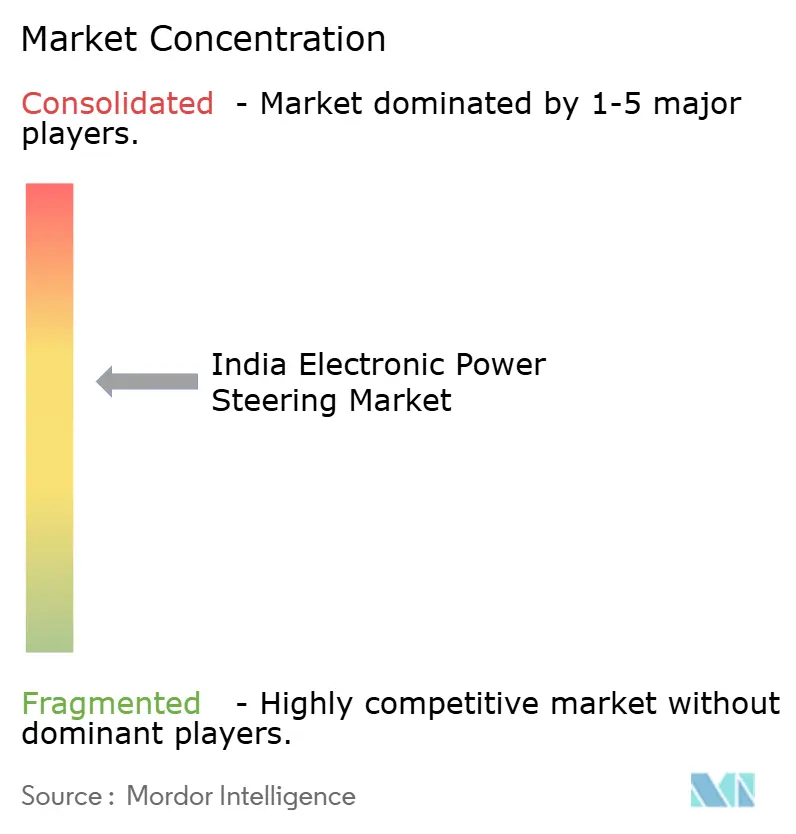

| Market Concentration | Medium |

Major Players_Market_-_Major_Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Electronic Power Steering Market Analysis by Mordor Intelligence

India Electronic Power Steering Market size in 2026 is estimated at USD 2.14 billion, growing from 2025 value of USD 2.01 billion with 2031 projections showing USD 2.92 billion, growing at 6.38% CAGR over 2026-2031. Supported by India’s accelerating push for vehicle electrification, AIS 145 safety mandates, and the Production Linked Incentive program for localized component manufacturing, the market benefits from stronger OEM demand, particularly as passenger-car output grew exponentially in 2024. Rapid SUV penetration, escalating semiconductor partnerships, and scale cost advantages enable wider fitment of column-assist units. At the same time, steer-by-wire pilots highlight a clear path to autonomous functionality. At the same time, higher unit costs versus hydraulic alternatives and imported semiconductor exposure temper the near-term growth trajectory, yet decisive policy moves and ongoing investments by Hyundai, Tata Motors, and Rane Holdings are steadily mitigating these risks.

Key Report Takeaways

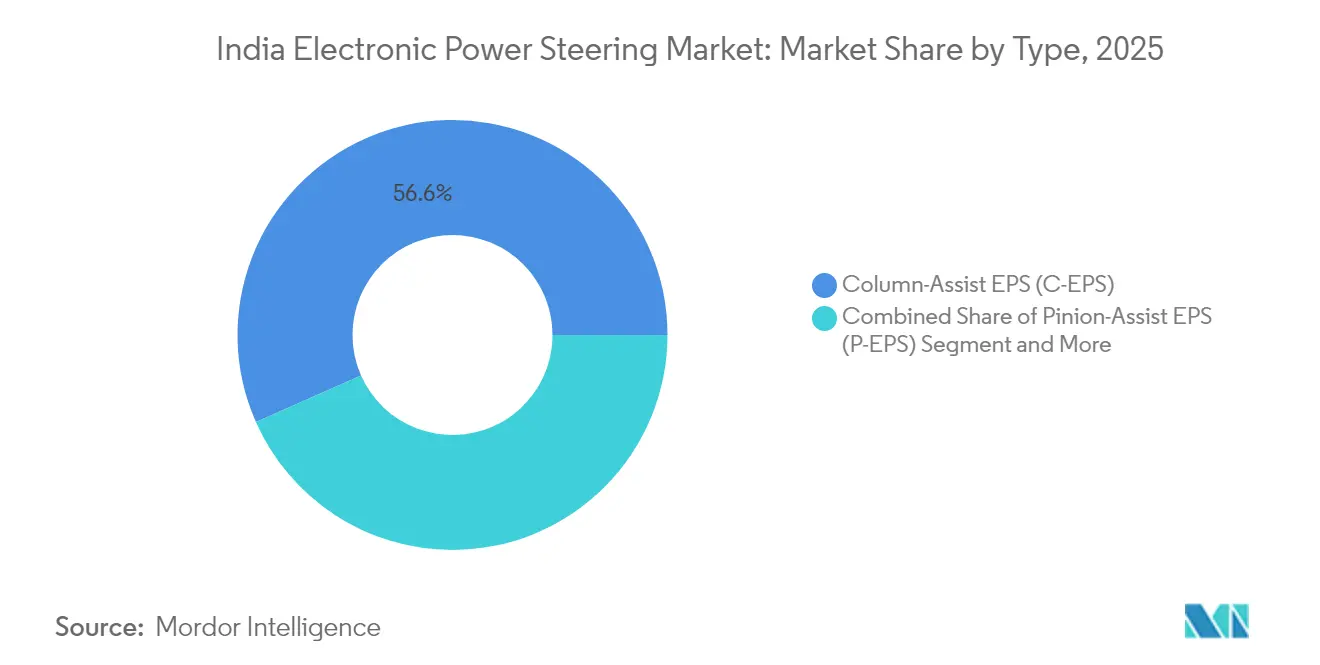

- By type, Column-assist systems held 56.63% of the Indian electric power steering market share in 2025. Integrated steer-by-wire solutions will expand at a 6.45% CAGR during the forecast period (2026-2031).

- By component, steering columns accounted for a 34.74% share of the Indian electric power steering market size in 2025, and electronic control units are advancing at a 6.51% CAGR during the forecast period (2026-2031).

- By vehicle, passenger cars commanded a 72.86% share of the Indian electric power steering market in 2025 and are growing at a 6.52% CAGR during the forecast period (2026-2031).

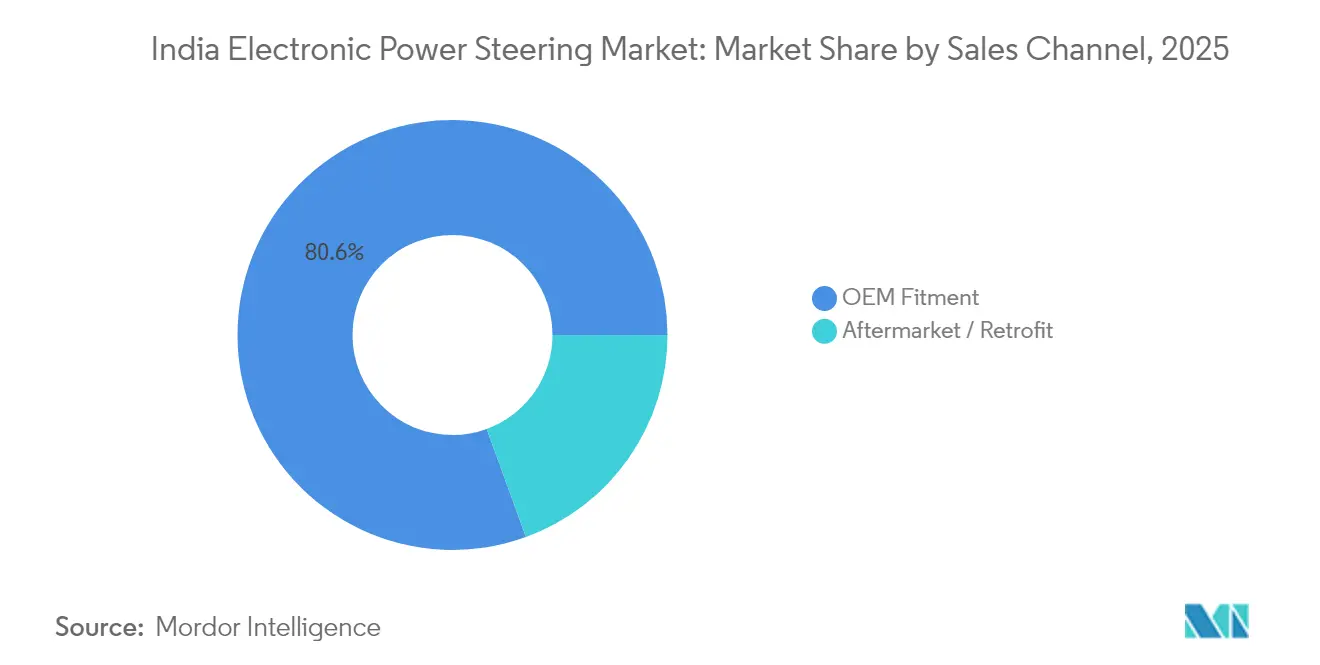

- By sales channel, OEM fitment controlled 80.55% of India's electric power steering market share in 2025; the aftermarket/retrofit channel recorded a 6.46% CAGR during the forecast period (2026-2031).

- By motor technology, BLDC motors accounted for a 62.74% share of the Indian electric power steering market in 2025 and will rise at a 6.49% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Electronic Power Steering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Passenger-Car Output | +1.8% | National, with concentration in Tamil Nadu, Maharashtra, Haryana | Medium term (2-4 years) |

| Stringent Safety Regulations | +1.5% | National implementation | Medium term (2-4 years) |

| Demand For Fuel-Efficient Drivetrains | +1.2% | National, stronger in urban markets | Short term (≤ 2 years) |

| Electrification Of Vehicle PARC | +0.9% | Urban centers initially, expanding to Tier-2 cities | Long term (≥ 4 years) |

| OEM Localisation Push | +0.8% | Manufacturing hubs in South and West India | Medium term (2-4 years) |

| Steer-By-Wire Pilots | +0.3% | Premium vehicle segments in metro cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Passenger-Car Output

Domestic passenger-car assemblies reached 4.3 million units in FY 2024-25, aided by Hyundai’s capacity build-out and Tata Motors’ multiple state expansions [1]“Society of Indian Automobile Manufacturers”, Passenger Vehicle Production Data FY 2025, siam.in. Higher volumes enable suppliers of the Indian electric power steering market to achieve scale benefits that trim per-unit costs and make column-assist systems viable even in compact hatchbacks. As SUVs and MPVs capture a rising share of production, demand for high-torque assistance grows. Regional clustering across Tamil Nadu, Maharashtra, and Haryana facilitates localized supply chains, allowing quicker just-in-time deliveries and higher localization content. CRISIL expects minimal passenger-vehicle output growth in FY 2026, ensuring sustained mid-term demand for electric steering units.

Stringent Safety Regulations (AIS 145, CMVR)

AIS 145 mandated features such as electronic stability control, lane-departure warning, and autonomous emergency steering, which only require the fine motor control provided by EPS [2]"Automotive Research Association of India”, Automotive Industry Standards 145, araiindia.com . OEMs are therefore accelerating the phase-out of hydraulic units regardless of incremental cost. Updated CMVR rules impose tighter steering-response benchmarks, further tipping the scales toward electronic control. Commercial-vehicle OEMs, historically reliant on hydraulic setups, are piloting electric solutions to comply. ECU demand also rises because these safety features need higher processing capacities, creating a feed-through boost for semiconductor content per vehicle.

Demand for Fuel-Efficient Drivetrains

Electric power steering eliminates the hydraulic pump’s parasitic losses, improving fuel economy by a minimal margin critical for OEMs meeting CAFE Phase II targets. EPS supports regenerative braking and precise control during electric-only operation in hybrid applications, further driving its use. Rising fuel prices elevate consumer sensitivity to mileage, prompting manufacturers to advertise EPS as a tangible efficiency upgrade. Penetration has thus expanded from premium models into mid-segment hatchbacks, especially in city-centric buyer profiles. EPS’s low standby power draw directly extends driving range for battery electric vehicles, underscoring its indispensability.

Electrification of Vehicle Parc

The PM E-DRIVE program channels incentives toward EV supply-chain localization and charging infrastructure, creating a virtuous cycle for adopting India's electric power steering market. EPS is standard in EV architecture because it minimizes battery drain. Fleet operators in metropolitan corridors trial electric light commercial vehicles with EPS to capture lower total ownership costs. Hybrid pickups and delivery vans in Bengaluru and Delhi further illustrate demand diversification beyond passenger cars. The shift also paves the way for software-defined steering functions such as automated parking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Unit Cost Vs HPS | -1.4% | Rural and price-sensitive urban markets | Short term (≤ 2 years) |

| Import-Reliant Semiconductor Supply Chain | -0.8% | National, affecting all OEMs | Medium term (2-4 years) |

| Scarcity Of Tier-2/3 Service Technicians | -0.4% | Tier-2/3 cities and rural service networks | Medium term (2-4 years) |

| Thermal Reliability Under Tropical Climate | -0.3% | Pan-India, acute in coastal and high-humidity regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Unit Cost vs HPS in Entry Cars

Electric power steering costs one-fourth more than hydraulic systems for hatchbacks priced below INR 500,000. Budget-focused rural buyers remain unconvinced by long-term fuel savings, hampering EPS penetration in entry trims. OEM margins already squeezed by rising commodity prices make absorbing the premium challenging. However, domestic fabrication incentives for sensors and BLDC motors under the automotive component PLI are narrowing the gap. Suppliers expect a minimal cost decline within a couple of years as ECU localization scales, bringing parity closer and easing this restraint.

Import-Reliant Semiconductor Supply Chain

Microcontrollers and angle sensors essential for EPS are sourced mainly from Taiwan and South Korea, exposing the Indian electric power steering industry to geopolitical disruptions and currency volatility. The global chip crunch led to OEM production cuts of up to one-fifth, illustrating this vulnerability. Initiatives like Tata-Infineon’s collaborative innovation center in Bengaluru aim to localize design, yet commercial-scale wafer fabs will only go live in few years' time. Until then, Tier-1s must maintain higher inventory buffers and dual-sourcing strategies, adding working-capital strain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Column-Assist Systems Lead Market Evolution

Column-assist solutions captured 56.63% of the Indian electric power steering market share in 2025, reflecting their cost-performance sweet spot across compact and midsize platforms. The segment’s dominance is reinforced by minimal chassis redesign requirements, allowing OEMs to retrofit existing hydraulic platforms swiftly. Rack-assist units cater to premium SUVs where steering precision and higher torque are vital. Pinion-assist designs occupy a niche between the two, particularly in sedan applications where road-feel refinement is prioritized. Although steer-by-wire currently represents less than 1% of installations, its 6.45% CAGR indicates growing OEM attention, with Hyundai and Lexus showcasing concept models at the 2025 Auto Expo. Regulatory acceptance will be the inflection point that elevates adoption rates among mass-market brands.

Second-order benefits also materialize: steer-by-wire removes the steering shaft intrusion, enabling frontal crash-zone energy-absorption redesigns and larger infotainment displays. Suppliers such as JTEKT are developing failsafe algorithms that maintain directional control even if a single actuator fails, addressing latent safety concerns. Once regulatory clarity emerges, especially regarding redundant power supply standards, steer-by-wire will likely encroach on the rack-assist space. The column-assist will underpin cost-sensitive variants, ensuring it remains a mainstay of the Indian electric power steering market.

By Component Type: ECU Sophistication Drives Growth

Steering columns held 34.74% of the Indian electric power steering market in 2025, as every EPS façade requires a mechanical or electronic column. Yet electronic control units will outpace at a 6.51% CAGR through 2031 because ADAS integration needs higher processing headroom. The latest Infineon Aurix microcontrollers support ISO 26262 ASIL-D safety, allowing automotive firmware over-the-air updates that slash recall costs. Torque-and-angle sensors also evolve toward inductive designs, eliminating magnets and enhancing precision.

Over the forecast window, ECU average cost content per vehicle will jump exponentially as software-defined cars gain traction. Domestic suppliers like KPIT and Tata Elxsi provide middleware that reduces time-to-market for new steering functions. Such developments create an ecosystem wherein semiconductor design houses, embedded-software firms, and steering-system manufacturers collaborate under one roof, accelerating product cycles and reinforcing the Indian electric power steering market’s competitiveness.

By Vehicle Type: Passenger Cars Dominate Adoption

Passenger cars controlled 72.86% of the Indian electric power steering market in 2025 and are advancing at a 6.52% CAGR, driven by AIS 145, ride-quality expectations, and the surge of SUV body styles that demand precise torque delivery. Compact SUVs like Tata Nexon and Hyundai Venue now feature EPS, signaling price-down diffusion across all trims. Light commercial vehicles are in earlier adoption phases but show promise as e-commerce requires silent, low-maintenance delivery vans for urban logistics. Medium and heavy commercials retain hydraulic setups because extreme axle loads necessitate higher steering effort; however, dual-assist architectures blending hydraulic base with electric overlay are in prototype testing.

Fleet operators increasingly prioritize longer service intervals and reduced downtime, leading to significant gains in total cost of ownership. CRISIL forecasts a notable increase in the adoption of EPS in new sub-5-ton trucks over the coming years. This shift presents a considerable volume opportunity for India's electric power steering market.

By Sales Channel: OEM Integration Dominates

Factory fitment accounted for 80.55% of the Indian electric power steering market in 2025 because EPS calibration requires vehicle-level software integration and compliance certification. The aftermarket rose 6.46% CAGR as retrofit kits became more standardized, targeting taxi fleets and municipal buses seeking operational savings. Kalyani Powertrain’s conversion kits received Automotive Research Association of India approval in February 2025, bolstering confidence among fleet managers. Nonetheless, regulatory inspection frameworks remain stringent, meaning the aftermarket share is unlikely to surpass one-fourth over the next five years.

OEM preference is also driven by warranty coverage and safety liabilities. Tier-1 suppliers provide end-to-end diagnostics embedded in the vehicle’s central domain controller, which is difficult to replicate in the retrofit channel. As a result, the growth of most volumes in the Indian electric power steering market will still originate from new vehicle assembly lines.

By Motor Technology: BLDC Motors Establish Dominance

BLDC motors commanded a 62.74% of the Indian electric power steering market in 2025 and will rise at a 6.49% CAGR, securing their status as the de facto standard for next-generation EPS. Compared with brushed alternatives, BLDC designs deliver better thermal management and eliminate brush wear, aligning with India’s harsh operating temperatures that often exceed. Permanent magnet costs have moderated because of diversified sourcing from Vietnam and Australia, further narrowing the cost gap. SynRM (synchronous reluctance) pilot projects are underway at Nexteer’s Bengaluru R&D center, touting 2% higher efficiency, but mass adoption hinges on volume scale.

Motor-gearbox integration is another frontier; Sona Comstar’s 3-in-1 EPS drive module reduces footprint by 20% and improves NVH characteristics. Such innovation augments the Indian electric power steering market’s technical maturity and encourages OEMs to deploy EPS even on smaller A-segment cars where under-hood space is constrained.

Geography Analysis

Vehicle production is concentrated in Tamil Nadu, Maharashtra, and Haryana, which collectively house about three-fifths of passenger-car output. Chennai’s corridor, complemented by ancillary clusters in Sriperumbudur and Oragadam, draws column-assist manufacturing due to incentives covering land and stamp-duty reimbursement . Pune’s Chakan and Aurangabad zones benefit from multi-modal logistics that ease ECU imports and dispatches of finished goods. Gurugram-Manesar leverages Maruti Suzuki’s ecosystem, encouraging local Tier-1s such as JTEKT India to establish dedicated EPS lines.

Emerging belts like Gujarat’s Sanand and Karnataka’s Tumakuru are scaling rapidly. Gujarat offers one-fifth capital subsidies for EV-related components, compelling suppliers to hedge geographic risk by setting up satellite units. Tumakuru is earmarked for a semiconductor special-economic zone that directly feeds ECU lines. Andhra Pradesh’s Krishnapatnam port further enables outbound shipments, easing export of EPS sub-assemblies to Southeast Asia.

Regional policy competition has tangible effects on the size of the Indian electric power steering market by state. Tamil Nadu is forecast grow exponentially in terms of incremental passenger-car units by 2030, implying roughly 0.6 million incremental EPS units. Maharashtra’s share will evolve toward premium vehicles, tightening demand for rack-assist and steer-by-wire variants. Meanwhile, Uttar Pradesh, historically low on automotive production, is positioning around Greater Noida to attract EV startups, but the material volume impact will surface only after 2028 when assembly facilities mature.

Competitive Landscape

Global leaders JTEKT, Nexteer, and ZF hold entrenched OEM relationships, supplying significant electric power steering. JTEKT’s Chennai plant added rack-assist line in 2025 to serve Toyota Kirloskar and Maruti Suzuki. Nexteer capitalizes on its software stack, SecureEPS, to lock in long-term programs with Mahindra & Mahindra. ZF, leveraging its Germany-based autonomy roadmap, anchors the premium steer-by-wire segment.

Indian incumbents are closing technology gaps through acquisitions and joint ventures. Rane Holdings’ September 2024 complete takeover of Rane NSK Steering deepened column-assist know-how while establishing access to NSK’s global patent pool. Sona Comstar diversified into torque sensors by acquiring Novelic Serbia, aiming to offer integrated steering, braking, and driveline solutions. Meanwhile, Tata Autocomp is co-developing ECUs with Infineon, positioning for the software-defined vehicle era.

Strategic differentiation increasingly rests on software and semiconductor integration. Infineon’s purchase of Marvell’s Automotive Ethernet unit underscores a pivot toward networked architectures that underpin autonomous steering commands. Tier-1s are thus recruiting over-the-air update specialists and cybersecurity talent, reshaping traditional hardware-centric competencies. Cost-focused players like JBM Auto emphasize frugal engineering, offering simplified EPS kits for budget vehicles seeking to leapfrog hydraulic setups without advanced ADAS requirements.

India Electronic Power Steering Industry Leaders

-

JTEKT Corporation

-

Nexteer Automotive

-

ZF Steering Gear (India) Limited

-

Denso Corporation

-

Mando Automotive India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Infineon Technologies and Tata Elxsi signed an MoU to co-develop EV solutions for the Indian market, aiming to compress design cycles and optimize EPS ECU architectures.

- May 2025: Ather Energy partnered with Infineon Technologies to exploit SiC/GaN devices across light-EV platforms, enhancing charge speed and lowering EPS controller size.

India Electronic Power Steering Market Report Scope

The Indian electric power steering market is segmented by type, component type, and vehicle type.

| Column-Assist EPS (C-EPS) |

| Pinion-Assist EPS (P-EPS) |

| Rack-Assist EPS (R-EPS) |

| Integrated Steer-by-Wire |

| Steering Column |

| Torque & Angle Sensors |

| Electric Motor |

| Electronic Control Unit (ECU) |

| Others (Wiring, Bearings, Housings) |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUVs & MPVs | |

| Light Commercial Vehicles (LCVs) | |

| Medium and Heavy Commercial Vehicles (MHCV) |

| OEM Fitment |

| Aftermarket / Retrofit |

| Brushed DC Motor |

| Brushless DC (BLDC) Motor |

| By Type | Column-Assist EPS (C-EPS) | |

| Pinion-Assist EPS (P-EPS) | ||

| Rack-Assist EPS (R-EPS) | ||

| Integrated Steer-by-Wire | ||

| By Component Type | Steering Column | |

| Torque & Angle Sensors | ||

| Electric Motor | ||

| Electronic Control Unit (ECU) | ||

| Others (Wiring, Bearings, Housings) | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| SUVs & MPVs | ||

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCV) | ||

| By Sales Channel | OEM Fitment | |

| Aftermarket / Retrofit | ||

| By Motor Technology | Brushed DC Motor | |

| Brushless DC (BLDC) Motor | ||

Key Questions Answered in the Report

How large is the Indian electric power steering market in 2026?

The market will reach USD 2.14 billion in 2026 and reach USD 2.92 billion by 2031.

Which vehicle category is driving most EPS demand in India?

Passenger cars, especially SUVs and MPVs, represent 72.86% of fitments and are growing at a 6.52% CAGR.

What regulation is accelerating EPS adoption in India?

AIS 145 safety standards, effective April 2026, mandate electronic stability control and related ADAS features that require EPS integration.

Why are BLDC motors preferred in electric power steering?

BLDC motors offer higher efficiency, zero brush wear, improved thermal tolerance, and quieter operation—attributes vital for the Indian climate and road conditions.

How will semiconductor localization influence EPS costs?

PLI incentives and joint ventures such as Tata-Infineon are expected to cut ECU and sensor costs by 10% before 2027, narrowing the price gap with hydraulic systems.

What is the growth outlook for EPS aftermarket retrofits?

Although smaller, the retrofit channel is projected to expand at a 6.46% CAGR as standardized kits and regulatory clarity emerge.

Page last updated on: