Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

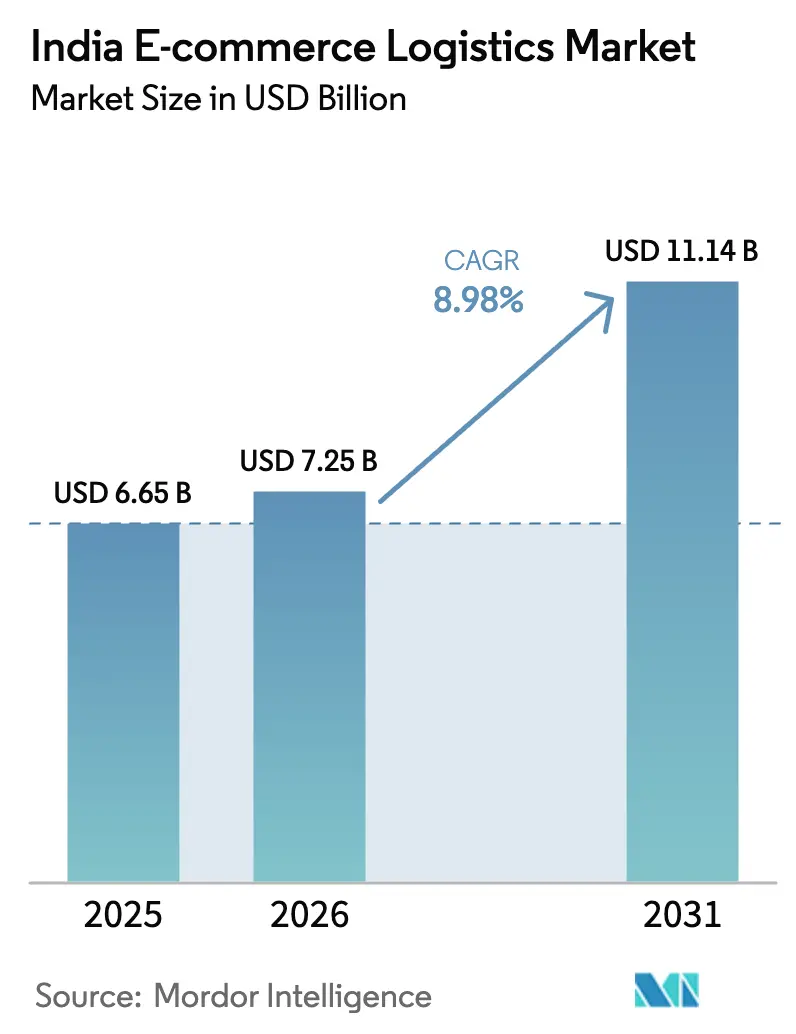

| Base Year Market Size (2025) | USD 6.65 Billion |

| Market Size (2026) | USD 7.25 Billion |

| Market Size (2031) | USD 11.14 Billion |

| Growth Rate (2026 - 2031) | 8.98% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India E-commerce Logistics Market Analysis by Mordor Intelligence

The India E-commerce Logistics Market size was valued at USD 6.65 billion in 2025 and estimated to grow from USD 7.25 billion in 2026 to reach USD 11.14 billion by 2031, at a CAGR of 8.98% during the forecast period (2026-2031).

The expected trajectory mirrors India’s pivot from conventional distribution to technology-enabled fulfillment ecosystems that serve an ever-wider digital consumer base. Value-added services, quick-commerce infrastructure, and rail-based express corridors are reshaping competitive parameters, while government programs such as PM Gati Shakti and the Dedicated Freight Corridor continue to lower structural cost barriers. The Open Network for Digital Commerce (ONDC) is opening capacity for smaller logistics providers, reducing platform dependency, and raising service-quality expectations. Consolidation momentum is evident as scale players integrate automated sorting, predictive analytics, and sustainable fleets to protect margins and deepen regional coverage.

Key Report Takeaways

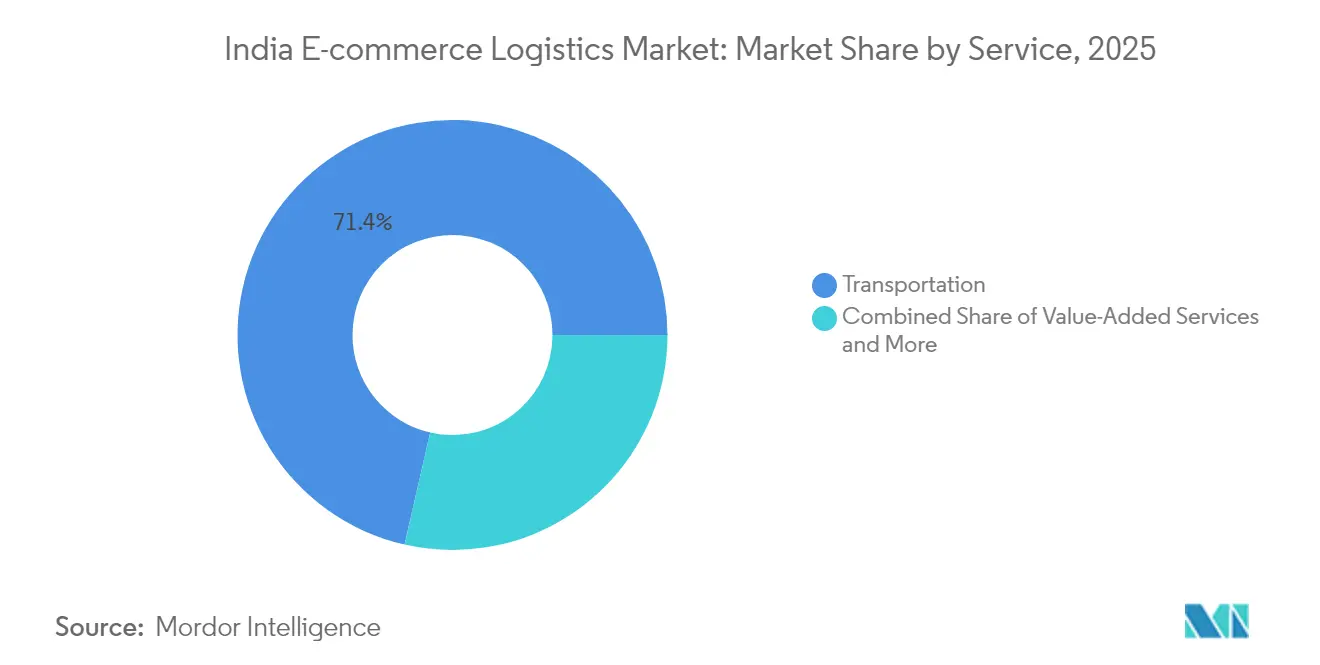

- By service, Transportation held 71.42% of the India e-commerce logistics market share in 2025 and value-added services are expected to advance at a 7.11% CAGR through 2031.

- By business model, the B2C segment captured 62.58% of the India e-commerce logistics market size in 2025, while C2C shows the fastest expansion at 6.42% CAGR to 2031.

- By destination, domestic deliveries accounted for 90.35% of the India e-commerce logistics market size in 2025; cross-border logistics is forecast to climb at a 6.69% CAGR between 2026 and 2031.

- By delivery speed, standard delivery commanded 50.62% of the India e-commerce logistics market share in 2025; same-day services are set to grow at a 6.09% CAGR to 2031.

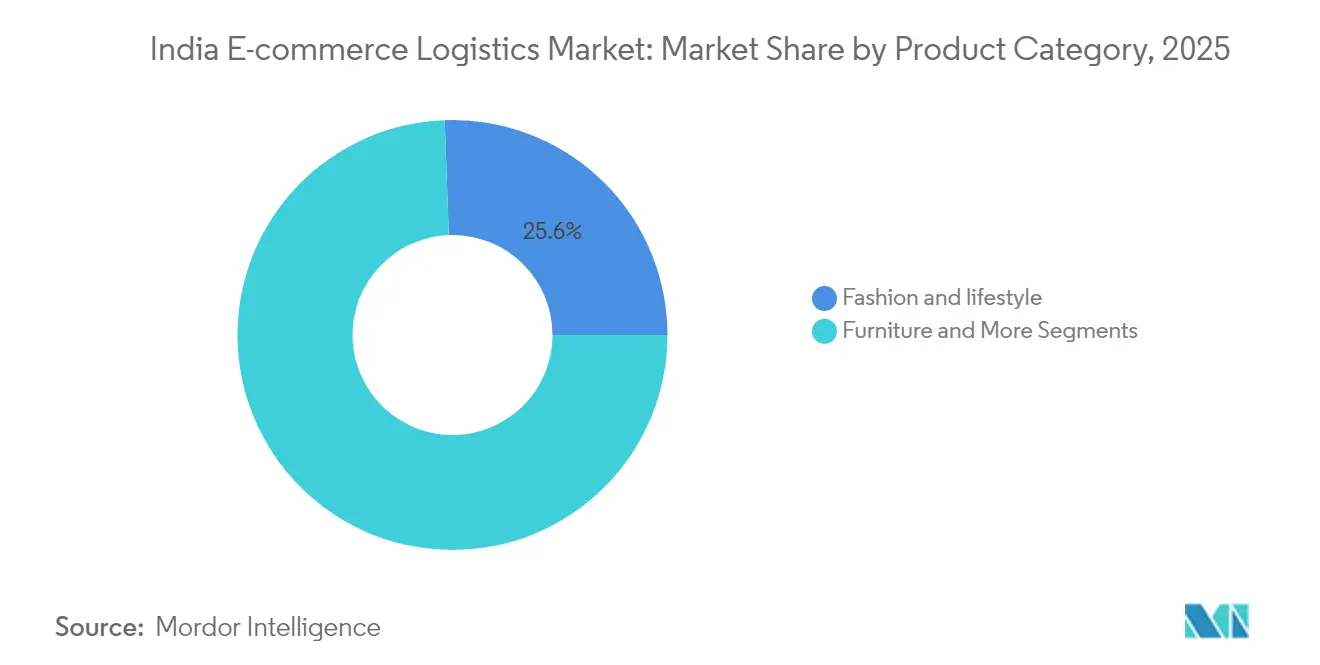

- By product category, fashion & lifestyle held 25.58% share of the India e-commerce logistics market size in 2025 and is rising at a 6.41% CAGR through 2031.

- By city tier, tier 3 and below cities represented 40.48% of the India e-commerce logistics market in 2025, underscoring successful digital penetration outside metropolitan areas.

- By region, North dominated with 21.78% share in 2025; West is projected to post a 6.58% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India E-commerce Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ONDC-driven MSME onboarding | +1.8% | National, with early gains in Tier 2/3 cities | Medium term (2-4 years) |

| D2C brand proliferation | +1.5% | Urban centers expanding to semi-urban markets | Short term (≤ 2 years) |

| Same-day/quick-commerce boom | +2.1% | Metro cities with spillover to Tier 2 | Short term (≤ 2 years) |

| UPI & digital-payments ubiquity | +1.2% | National, accelerated in rural areas | Long term (≥ 4 years) |

| Rail-based express cargo corridors | +0.9% | Western and Eastern corridors primarily | Long term (≥ 4 years) |

| Growth of social-commerce platforms | +1.4% | National, stronger in regional language markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ONDC-Driven MSME Onboarding

ONDC removes platform silos, enabling logistics firms to serve multiple seller ecosystems through standardized APIs that cut integration costs and elevate asset utilization. The model especially benefits tier 2 and tier 3 markets where traditional e-commerce reach was limited, spurring fresh revenue channels while forcing incumbents to compete on transparency and service quality. Transaction volumes on ONDC have scaled nationwide, confirming its role in democratizing logistics access[1]Department for Promotion of Industry and Internal Trade, “ONDC Concept Paper,” dpiit.gov.in.

D2C Brand Proliferation

Direct-to-consumer labels demand integrated inventory management, personalized packaging, and agile returns, pushing providers to invest in automation and predictive analytics. SKU proliferation coupled with seasonal surges raises complexity, yet the premium on consumer experience allows higher margins through specialized value-added services. This trend strengthens the adoption of warehouse management systems that synchronize multi-node fulfillment and support differentiated pricing.

Same-Day / Quick-Commerce Boom

Hyperlocal fulfillment has shifted from novelty to baseline expectation in metro zones. Dark stores and micro-fulfillment centers positioned within 3-5 kilometers of residential clusters require capital-intensive real estate and sophisticated routing software. Larger players leverage funding access, while niche hyperlocal specialists capture category-specific growth in groceries, electronics, and fashion. Automated sorting and AI-guided path optimization sustain service levels despite rising order volumes[2]Bloomberg News Desk, “Quick-commerce players accelerate infrastructure rollout,” bloomberg.com.

UPI and Digital-Payments Ubiquity

Unified Payments Interface diminishes cash-on-delivery friction, improving working-capital cycles and delivery success rates. UPI volumes exceeded 20 billion transactions in August 2025, with e-commerce forming a growing share[3]National Payments Corporation of India, “UPI Statistics August 2025,” npci.org.in. Real-time settlements allow smaller logistics vendors to meet enterprise standards, and embedded financial services generate new revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-optimal rural road & warehousing infra | -1.4% | Rural and semi-urban areas, Eastern states | Long term (≥ 4 years) |

| High product-return / COD ratio | -0.8% | National, more pronounced in Tier 2/3 cities | Medium term (2-4 years) |

| Draft e-commerce rules & data-localisation costs | -0.6% | National, higher impact on cross-border operations | Medium term (2-4 years) |

| Stricter ESG & decarbonisation compliance | -0.4% | Urban centers and industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sub-Optimal Rural Road & Warehousing Infrastructure

Connectivity gaps increase per-shipment costs and elongate delivery windows in rural markets. Warehousing shortages restrict temperature-sensitive and bulky product categories, limiting SKU variety. Government road initiatives continue to narrow the gap, yet infrastructure development trails e-commerce demand[4]Ministry of Rural Development, “Pradhan Mantri Gram Sadak Yojana progress update,” pmgsy.nic.in. Reverse logistics complexities further raise costs where transport options remain sparse.

High Product-Return / COD Ratio

Elevated return-to-origin levels inflate reverse logistics expenditure, and cash-on-delivery orders intensify payment-collection risk. Fashion categories drive the highest returns, requiring AI-driven quality checks and specialized processing hubs. Smaller providers face working-capital pressure from multiple delivery attempts and delayed settlements, making technology investments essential for margin protection.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Services Capture Premium Demand

Transportation generated 71.42% of the India e-commerce logistics market share in 2025, and the Value-Added Services segment CAGR stands at 7.11% to 2031. Providers offering branded packaging, kitting, and inspection enjoy strong pricing power. Transportation faces commoditization, but road haulage still offers the volume backbone for the India e-commerce logistics market. Rail improvements shorten transit times for bulk shipments, and air freight remains critical for time-sensitive cross-border parcels.

Technology-driven automation in warehousing cuts error rates and supports scale, while AI-enabled quality control allows providers to expand without proportional cost escalation. These capabilities sustain customer-retention strategies and create competitive barriers.

By Business Model: B2C Remains the Center of Gravity

The B2C segment contributed 62.58% to the India e-commerce logistics market size in 2025 and continues to set service-level benchmarks. The C2C corridor, propelled by social-commerce activity, is advancing at a 6.42% CAGR (2026-2031) and demands professional tracking, insurance, and support for individual entrepreneurs. B2B shipments offer stability but yield lower technology differentiation opportunities.

B2C growth aligns with rising quick-commerce expectations and widespread smartphone adoption, compelling providers to refine last-mile networks and customer-communication tools. Social-commerce expansion amplifies the need for scalable micro-fulfillment solutions that meet individualized seller requirements.

By Destination: Domestic Dominance with Cross-Border Upside

Domestic deliveries dominated with 90.35% of the India e-commerce logistics market size in 2025, reflecting India’s vast internal consumption. Cross-border services, while smaller, are growing at a 6.69% CAGR through 2031 as exporters leverage customs digitization under the National Single Window System.

Unified Goods and Services Tax compliance supports nationwide distribution, and new economic corridors shorten domestic transit. For international sellers, specialized customs brokerage and multimodal solutions enable premium pricing and erect entry barriers.

By Delivery Speed: Standard Keeps Cost Leadership

Standard delivery controlled 50.62% of the India e-commerce logistics market in 2025. Consolidated routing sustains the lowest per-unit cost, appealing to price-sensitive consumers. Same-day delivery, though niche, grows at a 6.09% CAGR (2026-2031) as affluent metro shoppers pay for convenience.

Next-day serves the middle ground, while >5-day “Others” absorb bulk, non-urgent traffic through rail and sea. Route-optimization algorithms help shorten windows without linear cost growth, nudging the market toward faster norms without compromising profitability.

By Product Category: Fashion Drives Service Innovation

Fashion & lifestyle retained a 25.58% share of the India e-commerce logistics market size in 2025 and leads growth at a 6.41% CAGR (2026-2031). High return ratios compel investment in reverse logistics facilities and AI-based recommendation engines. Electronics logistics commands higher insurance and security layers, whereas foods & beverages rely on cold-chain assets that few competitors can match.

Personal care enjoys predictable demand and lower returns, supporting efficient capacity planning. Furniture requires bulky goods handling and assembly options, opening another specialization avenue.

By City Tier: Tier 3 Penetration Reshapes Network Design

Tier 3 and below cities formed 40.48% of the India e-commerce logistics market in 2025, fueled by vernacular interfaces and data-affordable connectivity. Hub-and-spoke extensions, local entrepreneur partnerships, and alternative pickup points allow cost-effective outreach despite lower shipment density. Tier 1 volumes remain high but face saturation, while tier 2 balances growth potential with infrastructure readiness.

Geography Analysis

The North retained 21.78% of the India e-commerce logistics market in 2025, benefiting from established manufacturing clusters and multimodal corridors. Delhi NCR acts as a central gateway, and newly sanctioned Multi-Modal Logistics Parks strengthen throughput. Western Dedicated Freight Corridor sections are already cutting transit times and enhancing capacity.

The West is the fastest-growing region at 6.58% CAGR (2026-2031), leveraging Maharashtra’s diversified consumer base and Gujarat’s port-centric export focus. Integrated sea-land solutions support international parcel flows, and special economic zones add industrial demand.

Competitive Landscape

India e-commerce logistics market competition remains fragmented, yet is consolidating. Acquisitions such as Delhivery’s purchase of Ecom Express underscore the trend toward scale integration and national network extension. Leaders invest in AI-powered route optimization, automated sorting, and warehouse robotics to improve cost-to-serve metrics.

Three strategic strata define the landscape. National players combine extensive networks with full-stack services. Regional specialists focus on territory or vertical depth, often providing temperature-controlled or bulky-goods handling. Technology-driven startups capture hyperlocal and quick-commerce niches.

Sustainability variables enter bidding tables as ESG compliance tightens. Electric vehicle fleets, solar-powered hubs, and carbon-tracking dashboards differentiate service offerings and attract enterprise contracts. Providers with capital to adopt green technology early gain an advantage.

India E-commerce Logistics Industry Leaders

Delhivery

Ekart Logistics

XpressBees

Blue Dart Express

DTDC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Delhivery announced the acquisition of Ecom Express for Rs 1,407 crore (USD 169 million), subject to Competition Commission clearance – consolidation aimed at leveraging overlapping customer bases.

- January 2025: FedEx introduced FedEx Surround in India, offering AI-enabled near real-time shipment visibility for enterprise clients.

- January 2025: Blue Dart opened a 250,000 sq ft hub in Bijwasan, Delhi, with automated sorting and rooftop solar aligned with PM Gati Shakti targets.

- September 2024: DHL eCommerce affirmed a EUR 250 million (USD 260 million) India investment plan to expand hubs, fleet capacity, and local acquisitions by 2030.

India E-commerce Logistics Market Report Scope

E-commerce logistics refers to the transportation, warehousing, and distribution services the logistics company provides to an online retailer.

The Indian e-commerce logistics market is segmented by service (transportation, warehousing, inventory management, and value-added services (labeling, packaging, etc.)), business (B2B and B2C), destination (domestic and international/cross-border), and product (fashion and apparel, consumer electronics, home appliances, furniture, beauty and personal care products, and other products (toys, food products, etc.)). The report offers market size and forecasts in value (USD) for all the above segments.

By Service

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing & Fulfilment | |

| Value-Added Services (Labelling, Packaging, Kitting) |

By Business Model

| B2C |

| B2B |

| C2C |

By Destination

| Domestic |

| Cross-border (international) |

By Delivery Speed

| Same-day (less than 24 h) |

| Next-day (24–48 h) |

| Standard (3-5 days) |

| Others (more than 5 days) |

By Product Category

| Foods & Beverages |

| Personal & Household Care |

| Fashion & Lifestyle (accessories, apparel, footwear) |

| Furniture |

| Consumer Electronics & Household Appliances |

| Other Products |

By City Tier

| Tier 1 |

| Tier 2 |

| Tier 3 and Below |

By Region (India)

| North |

| South |

| East |

| West |

| Central |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing & Fulfilment | ||

| Value-Added Services (Labelling, Packaging, Kitting) | ||

| By Business Model | B2C | |

| B2B | ||

| C2C | ||

| By Destination | Domestic | |

| Cross-border (international) | ||

| By Delivery Speed | Same-day (less than 24 h) | |

| Next-day (24–48 h) | ||

| Standard (3-5 days) | ||

| Others (more than 5 days) | ||

| By Product Category | Foods & Beverages | |

| Personal & Household Care | ||

| Fashion & Lifestyle (accessories, apparel, footwear) | ||

| Furniture | ||

| Consumer Electronics & Household Appliances | ||

| Other Products | ||

| By City Tier | Tier 1 | |

| Tier 2 | ||

| Tier 3 and Below | ||

| By Region (India) | North | |

| South | ||

| East | ||

| West | ||

| Central |

Key Questions Answered in the Report

How big will the India e-commerce logistics market be by 2031?

It is projected to reach USD 11.14 billion, growing at a 8.98% CAGR from 2026 to 2031.

Which service segment holds the largest share?

Transportation commanded 71.42% of market share in 2025, driven by the surge in e-commerce shipments and the growing need for faster, last-mile delivery solutions.

What region is expanding the fastest?

The West is growing at 6.58% CAGR, supported by port infrastructure and industrial diversification.

How are quick-commerce models affecting logistics networks?

Same-day demand drives dark-store investments and AI-based route optimization, pushing capital toward hyperlocal fulfillment.

What is the main barrier to rural e-commerce expansion?

Inadequate road and warehousing infrastructure increases delivery costs and complicates reverse logistics workflows.

Why are returns a significant challenge in fashion logistics?

High sizing-related returns trigger expensive reverse logistics, prompting providers to build dedicated processing hubs and predictive quality systems.

Page last updated on: