China Discrete GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

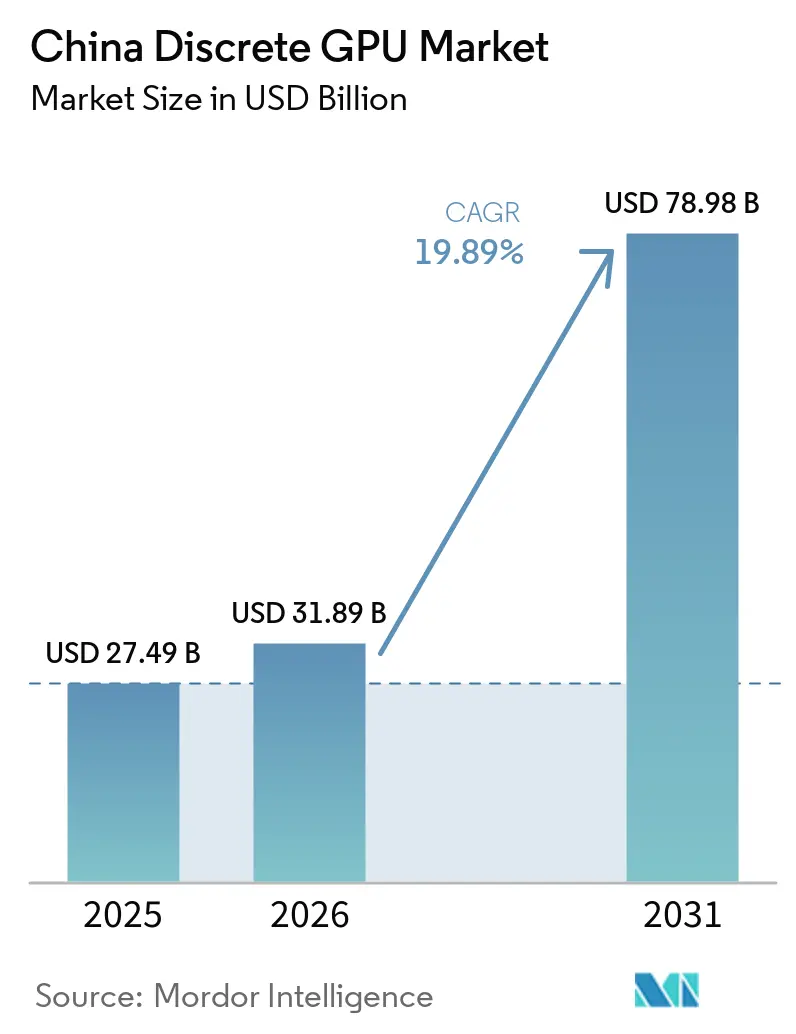

| Base Year Market Size (2025) | USD 27.49 Billion |

| Market Size (2026) | USD 31.89 Billion |

| Market Size (2031) | USD 78.98 Billion |

| Growth Rate (2026 - 2031) | 19.89% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Discrete GPU Market Analysis by Mordor Intelligence

The China discrete GPU market size is projected to expand from USD 27.49 billion in 2025 and USD 31.89 billion in 2026 to USD 78.98 billion by 2031, registering a CAGR of 19.89% between 2026 and 2031. Demand is shifting from consumer-centric gaming cards toward datacenter accelerators that power large-language-model training, cloud-based inference, and automotive autonomy platforms. Domestic hyperscalers are locking in multiyear supply agreements, carmakers are adding high-throughput graphics silicon to electric-vehicle compute stacks, and provincial governments are subsidizing fabrication capacity, all of which raise unit volumes and average selling prices. The market is simultaneously contending with United States export controls that cap performance ceilings and redirect orders toward compliant mid-tier parts, a dynamic that is spurring rapid innovation among domestic fabless designers. Memory architecture is also in flux, with high-bandwidth memory gaining ground on legacy GDDR configurations as training workloads demand bandwidth densities above 3 TB s⁻¹. Collectively, these vectors underpin strong revenue visibility for suppliers able to balance cost, power, and compliance requirements while supporting the evolving software ecosystem.

Key Report Takeaways

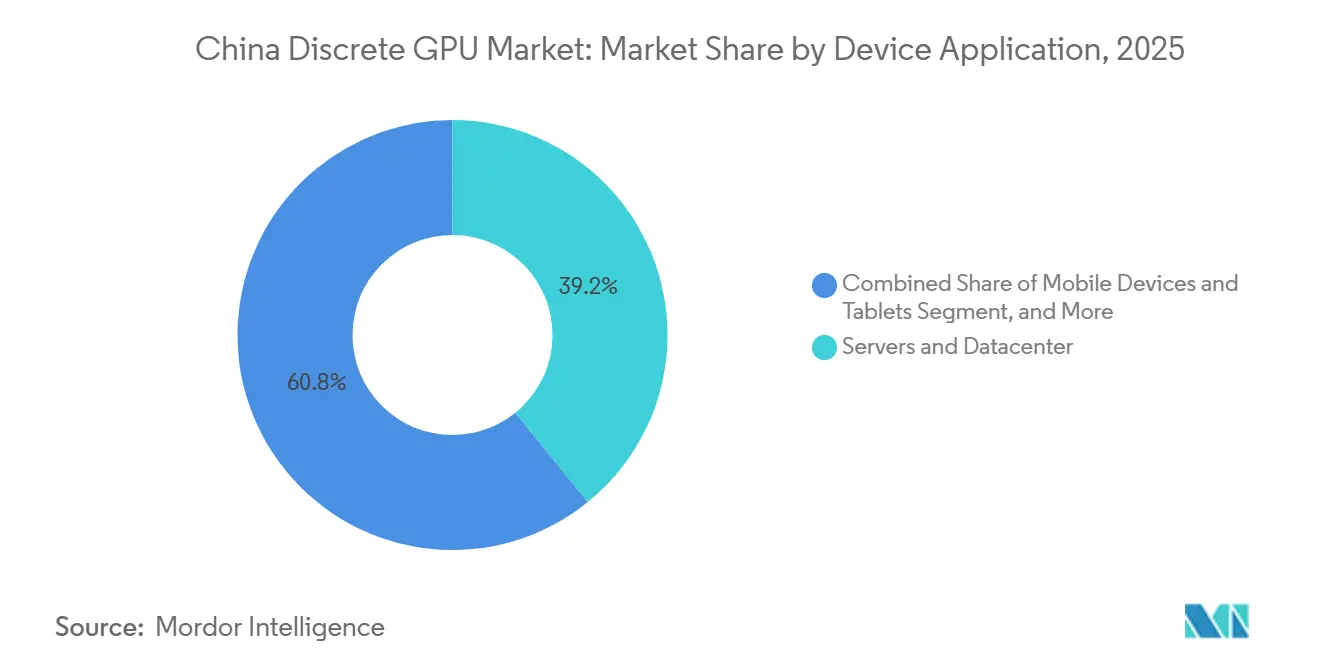

- By device application, servers and datacenter accelerators commanded 39.17% of the China discrete GPU market share in 2025 and are expanding at a 20.53% CAGR through 2031.

- By memory type, GDDR-based boards led with 68.48% of the China discrete GPU market share in 2025, while HBM-equipped products are forecast to grow at a 20.98% CAGR to 2031.

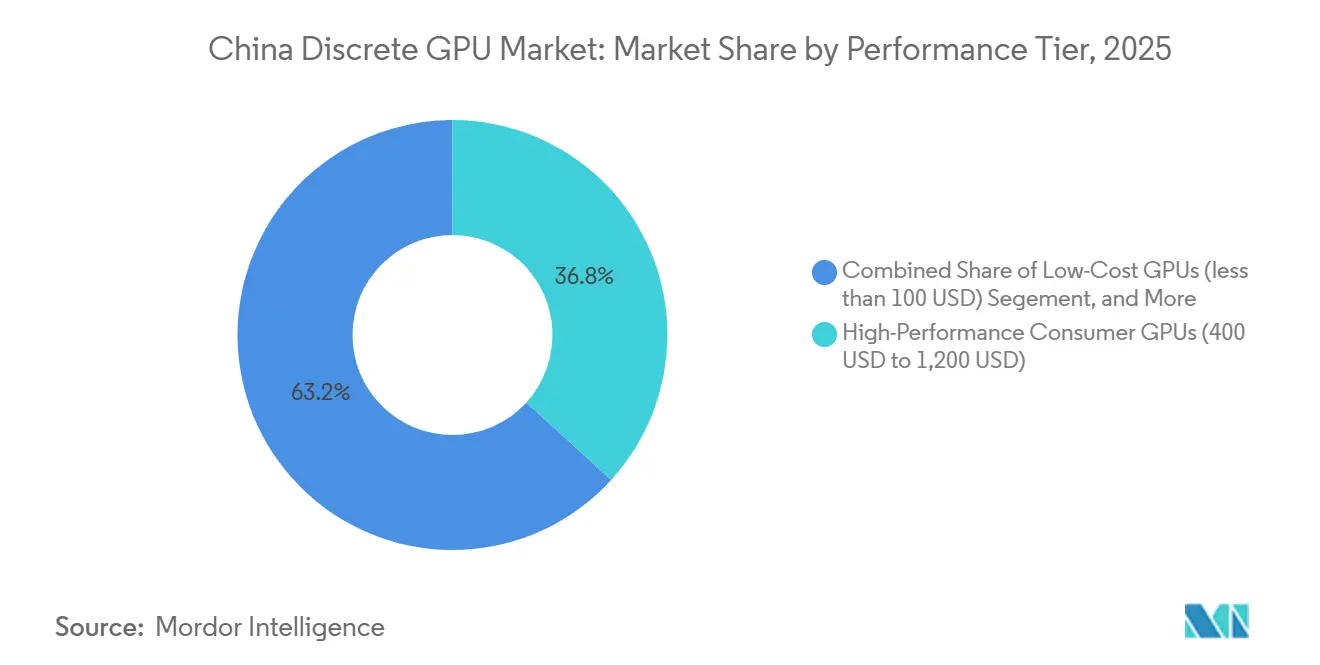

- By performance tier, high-performance consumer cards held 36.77% of the China discrete GPU market size in 2025, and datacenter GPUs priced above USD 1,200 are registering the fastest 20.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for AI Training and Inference Workloads in Chinese Hyperscale Datacenters | +6.8% | Beijing, Shanghai, Shenzhen, Hangzhou | Medium term (2-4 years) |

| Government Incentives for Domestic Semiconductor Self-Reliance and GPU Innovation | +4.5% | National | Long term (≥ 4 years) |

| Continuous Growth of PC Gaming and Esports Ecosystem in China | +3.2% | Tier-1 and tier-2 cities nationwide | Long term (≥ 4 years) |

| Rapid Adoption of Discrete GPUs in Automotive ADAS and Autonomous-Driving Platforms | +2.9% | Shanghai, Guangzhou, Shenzhen | Medium term (2-4 years) |

| Rising Demand from Domestic Cloud-Based GPUaaS Providers Targeting SME AI Workloads | +1.7% | Yangtze River Delta and Pearl River Delta | Short term (≤ 2 years) |

| Expansion of Refurbished GPU Exports Creating Domestic Upgrade Cycle and Price Normalization | +0.9% | Shenzhen electronics clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for AI Training and Inference Workloads in Chinese Hyperscale Datacenters

Hyperscale operators have moved GPU procurement to the top of capital-expenditure priorities. Alibaba Cloud spent USD 53 billion in fiscal 2025 and deployed more than 100,000 accelerators across domestic server halls. ByteDance earmarked USD 23 billion the same year to train its Doubao foundation model, an effort that required roughly 50,000 H100-class chips. Tencent doubled AI-related capex, rolling out new GPU clusters for its Hunyuan model. Baidu’s Ernie 4.0 stack came online with about 20,000 discrete GPUs that delivered OpenAI-comparable performance. These deployments follow multi-year supply contracts that dampen demand cyclicality and encourage joint silicon-software co-design with local vendors to mitigate export-control risks.

Government Incentives for Domestic Semiconductor Self-Reliance and GPU Innovation

China’s National Integrated Circuit Industry Investment Fund Phase III committed CNY 344 billion (USD 47 billion) in 2024, explicitly listing GPU development as a strategic domain.[2]Ministry of Industry and Information Technology, “Integrated Circuit Industry Development Goals 2025-2030,” miit.gov.cn A State Council directive from the same year mandates that half of all government and state-owned enterprise IT procurement source domestic semiconductors by 2027, creating guaranteed demand for homegrown graphics processors.[1]State Council of the People’s Republic of China, “Guidance on Government Procurement of Domestic Semiconductors,” gov.cnShanghai offered CNY 2 billion (USD 280 million) in direct grants to GPU startups during 2025, a model replicated by Shenzhen and Wuhan municipalities. The Ministry of Industry and Information Technology sets an 80% semiconductor self-sufficiency goal by 2030, further aligning fiscal resources with road-map milestones. Talent incentives have attracted more than 3,500 engineers back from overseas positions, enlarging the domestic skills pool required for advanced GPU architecture.

Continuous Growth of PC Gaming and Esports Ecosystem in China

PC gaming hardware revenue reached USD 14.3 billion in 2025 as the installed base grew to 370 million active users. Gaming cafés refreshed rigs with GeForce RTX 4070-class cards to deliver 240-frame-per-second experiences on competitive titles. NVIDIA’s RTX 4090D, engineered to respect performance caps, still sold about 1.2 million units at a USD 1,599 price tag. Domestic vendors are filling the sub-USD 400 bracket, with Moore Threads’ MTT S80 gaining shelf space via Lenovo and Xiaomi desktops. A vibrant secondary market in Shenzhen’s Huaqiangbei district keeps prior-generation GPU prices in check, indirectly shortening upgrade cycles for cost-sensitive gamers.

Rapid Adoption of Discrete GPUs in Automotive ADAS and Autonomous-Driving Platforms

Electric-vehicle makers are installing discrete GPUs in centralized compute boxes to enable Level 3 and higher autonomy. Li Auto shipped 150,000 vehicles using the M100 platform that integrates Orin-class accelerators rated at 254. NIO’s Shenji NX9031 reached volume output in March 2025, combining GPU cores and a neural-processing unit to hit 1,016 TOPS, thereby supporting Navigate on Pilot Plus across 168 cities NIO.COM. XPeng’s Turing chip, fabbed on 7 nm, entered production vehicles in January 2025 and cuts per-car GPU costs by roughly 40%. BYD and NVIDIA agreed to deploy discrete GPUs in premium Yangwang and Denza lines, aiming for 500,000 units annually by 2027. These initiatives are spawning an ecosystem focused on low-power AI inference within 50-watt thermal envelopes and ISO 26262 compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. Export Controls Limiting Access to Cutting-Edge GPU IP and HBM Memory | −4.3% | National | Medium term (2-4 years) |

| Fragmentation of CUDA-Alternative Software Ecosystems Hindering Domestic GPU Adoption | −2.8% | National | Long term (≥ 4 years) |

| Global Semiconductor Supply-Chain Constraints Raising Bill-of-Materials Costs | −2.1% | National | Short term (≤ 2 years) |

| Cooling and Power Infrastructure Limitations in Tier-2 Chinese Datacenters | −1.6% | Tier-2 and tier-3 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

U.S. Export Controls Limiting Access to Cutting-Edge GPU IP and HBM Memory

Revisions to United States export rules in January 2025 introduced performance ceilings that restrict bidirectional transfer rates and floating-point throughput for GPUs bound for China DOC.GOV. NVIDIA responded with H20, L20 and L2 variants that deliver about one-third less training throughput than the H100, yet still consumed 15% of 2025 datacenter revenue.[3]NVIDIA Corporation, “H20 and L2 Product Brief,” nvidia.com AMD’s MI308 navigated a protracted licensing process that delayed broad availability until the third quarter of 2025. Supply pressure intensified after the United States urged SK Hynix and Micron to scale back HBM3 exports, reducing allocations to Chinese buyers by roughly 40%. Domestic firms are experimenting with GDDR6X-based chiplet layouts as stop-gaps, but these alternatives incur higher power draw and cooling overhead.

Fragmentation of CUDA-Alternative Software Ecosystems Hindering Domestic GPU Adoption

A robust hardware road map requires equally mature software, yet domestic alternatives to CUDA remain siloed. Moore Threads’ MUSA, Hygon’s ROCm-compatible fork, and Cambricon’s proprietary tool chain each support different operator libraries, forcing enterprises to refactor code bases for every new deployment. Surveys among cloud service providers indicate that porting a production workload adds as much as 30% to total ownership cost. Open-source groups are working on cross-compilers, but progress is uneven. As long as fragmentation persists, some AI developers prefer lower-performing but familiar NVIDIA boards rather than migrating to domestic accelerators, muting short-term shipment growth for local suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Datacenter Accelerators Extend Leadership

Servers and datacenter accelerators accounted for 39.17% of 2025 revenue in the China discrete GPU market, underscoring the structural shift away from purely consumer graphics boards. The segment benefits from multi-year capacity reservations by Alibaba Cloud, Tencent, ByteDance, and Baidu, each scaling fleets that now exceed a combined 300,000 AI accelerators. This procurement discipline stabilizes quarterly demand and supports vendors that can satisfy compliance rules while offering competitive price-performance ratios. Professional visualization and workstation cards trail datacenter silicon but still monetize creative workflows, capturing roughly 12% of the 2025 total as content studios embrace generative AI in video editing and architectural rendering.

The gaming PC and workstation category remains large by volume, yet its revenue share is slowing as average selling prices plateau. Gaming cafés and home enthusiasts continue to refresh rigs, helped by lower-tier domestic GPUs that deliver esports-class frame rates at sub-USD 400 price points. Automotive GPUs, though starting from a smaller base, are on a steep climb. Annual shipments are projected to top 2 million units by 2027 as Li Auto, NIO, and XPeng push centralized compute boxes into mainstream trims. Edge devices covering industrial vision and retail analytics form a nascent but promising slice, favored by data-localization policies that discourage cloud offloading and thus raise on-premises inference demand.

By Memory Type: HBM Builds Momentum in Training Workloads

GDDR-equipped boards held 68.48% of shipments during 2025, a legacy advantage rooted in gaming and mainstream datacenter deployments where cost per gigabyte still drives bill-of-materials math. However, HBM-based accelerators already dominate the highest ASP band and are forecast to expand at a 20.98% CAGR through 2031, thereby enlarging their slice of the China discrete GPU market size. NVIDIA’s H20 and AMD’s MI308 both employ stacked-memory stacks to hit bandwidth ceilings above 3 TB s⁻¹ within strict power budgets, reinforcing HBM as the default for training clusters priced above USD 10,000.

Suppliers face a delicate balancing act. U.S. pressure on SK Hynix and Micron to limit HBM3 exports has funneled Chinese demand toward Samsung HBM2e, which runs roughly 20% slower. Consequently, Biren and Moore Threads are designing mixed-memory layouts that pair HBM2e with high-speed GDDR6X. Meanwhile, Yangtze Memory Technologies Corporation is racing to build domestic HBM3 capacity, though yield hurdles may delay meaningful volumes until 2027. Until then, cost-sensitive segments will continue to default to GDDR6X, helping that technology retain volume leadership even as HBM grabs value share.

By Performance Tier: Premium Segments Propel Revenue Growth

High-performance consumer cards ranging from USD 400 to USD 1,200 secured 36.77% of the 2025 China discrete GPU market size, helped by esports growth and creator workloads that monetize premium rasterization. Datacenter GPUs priced above USD 1,200 form the fastest expanding tier at a 20.74% CAGR through 2031, reflecting relentless AI training demand. Mainstream GPUs spanning USD 100 to USD 400 remain essential for volume gaming and office productivity; domestic suppliers are aggressively discounting in this band to seed ecosystem adoption.

Low-cost GPUs below USD 100 power embedded inference at the network edge, from retail analytics terminals to smart-city cameras. Price competition is fierce, yet unit growth is healthy in provincial smart-city tenders that require on-premises processing for privacy compliance. The premium consumer bracket is splintering into gaming-specific and creator-optimized SKUs, with NVIDIA’s RTX 4090D commanding USD 1,599 despite export-imposed throughput caps. AMD’s Radeon RX 7900 XTX fills the value gap with a USD 999 street price and unrestricted memory bandwidth, capturing roughly 18% share of that slice. Domestic challengers use chiplet-based cost savings to undercut foreign incumbents, exemplified by Moore Threads’ USD 3,499 MTT S4000 targeting cost-sensitive inference farm operators that accept lower floating-point precision.

Geography Analysis

Eastern provinces remain the demand epicenter for the China discrete GPU market, with Beijing, Shanghai, Zhejiang and Guangdong hosting the vast majority of hyperscale datacenters and automotive R&D campuses. These provinces consumed more than 65% of 2025 unit shipments thanks to cloud adoption and an affluent gamer base. Northern clusters anchored by Tianjin and Hebei are growing double digits on the back of state-backed smart-city pilots that mandate localized AI inference.

Central China, including Hubei and Hunan, is courting GPU suppliers through subsidized land and power tariffs to alleviate congestion in coastal server halls. These provinces also host emerging automotive plants that integrate discrete GPUs in driver-assistance modules, bolstering regional demand diversity. Western regions such as Sichuan and Chongqing continue to trail volume leaders but benefit from renewable energy abundance that reduces datacenter operating costs, making them attractive expansion targets for cloud service providers seeking to lower total cost of ownership.

Cross-border trade flows are inching upward as local manufacturers export refurbished gaming GPUs to South-East Asian markets, freeing domestic slots for upgrades and normalizing resale values at home. Hong Kong remains a critical logistics waypoint for premium datacenter accelerators that must clear compliance checks before mainland customs release. Despite these variations, the overarching theme is that no single province commands an overwhelming China discrete GPU market share, reflecting gradual geographic dispersion as land, power and cooling constraints surface in traditional hubs.

Competitive Landscape

The China discrete GPU market displays moderate concentration, dominated by NVIDIA and AMD at roughly 60% of 2025 datacenter revenue, yet rapidly diluted by state-backed domestic entrants. United States export rules limit flagship silicon and open mid-tier price bands where Chinese designers can compete aggressively. Moore Threads completed an IPO that raised CNY 6.8 billion (USD 950 million), earmarked for 7 nm tape-outs and an expanded software toolkit. Biren Technology drew CNY 3.5 billion (USD 490 million) of Series C capital in February 2026 to finance 5 nm migration and HBM3 integration.

Strategic focus is shifting from raw compute to turnkey platforms that fuse silicon, development frameworks, and cloud provisioning. Huawei’s Ascend ecosystem now anchors Baidu and Tencent training clusters, proving that vertical integration offers a path around CUDA lock-in. Cambricon’s Siyuan 370 aims squarely at inference workloads, underscoring segmentation among compute-intensive and latency-sensitive use cases. Patent disclosures show Biren filing 127 GPU-related inventions in 2025 that optimize chiplet interconnects, a hedge against HBM supply risks.

Policy is central to share redistribution. The 50% domestic procurement mandate for public sector IT will redirect about USD 4 billion of annual GPU outlays to local suppliers by 2027. Foreign incumbents are countering through joint ventures and knowledge-transfer agreements to retain strategic customers. For example, NVIDIA secured conditional clearance to ship a limited number of H200 derivatives to select hyperscalers. This hybrid coexistence creates a two-speed market in which domestic brands flourish in government and automotive accounts while NVIDIA and AMD preserve a presence among multinational cloud tenants that still rely on mature CUDA workflows.

China Discrete GPU Industry Leaders

NVIDIA Corporation

Huawei Technologies Co. Ltd. (HiSilicon, Ascend

Advanced Micro Devices Inc.

Intel Corporation

Biren Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Moore Threads entered a strategic alliance with Alibaba Cloud to co-develop inference accelerators aimed at e-commerce recommendation engines, targeting a 40% latency reduction in Taobao and Tmall workloads.]

- February 2026: Biren Technology raised CNY 3.5 billion (USD 490 million) in Series C financing led by China Reform Holdings to fund 5 nm GPU R&D and HBM3 integration.

- January 2026: NVIDIA obtained conditional approval from the United States Department of Commerce to ship up to 10,000 H200-derivative GPUs per year to compliant Chinese hyperscalers.

China Discrete GPU Market Report Scope

A discrete GPU, or discrete graphics processing unit, is a dedicated hardware component designed exclusively to handle graphics rendering and parallel computational tasks, operating independently from the central processing unit (CPU) with its own dedicated video memory (VRAM) and power circuitry.

The China Discrete GPU Market Report is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, and Other Embedded and Edge Devices), Memory Type (GDDR-based GPUs, and HBM-based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-Based GPUs |

| HBM-Based GPUs |

| Low-Cost GPUs (less than 100 USD) |

| Mainstream GPUs (100 USD to 400 USD) |

| High-Performance Consumer GPUs (400 USD to 1,200 USD) |

| Data Center / AI Accelerator GPUs (greater than 1,200 USD) |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Memory Type | GDDR-Based GPUs |

| HBM-Based GPUs | |

| By Performance Tier | Low-Cost GPUs (less than 100 USD) |

| Mainstream GPUs (100 USD to 400 USD) | |

| High-Performance Consumer GPUs (400 USD to 1,200 USD) | |

| Data Center / AI Accelerator GPUs (greater than 1,200 USD) |

Key Questions Answered in the Report

How large will the China discrete GPU market be by 2031?

The China discrete GPU market size is forecast to reach USD 78.98 billion by 2031, growing at a 19.89% CAGR from 2026.

Which device application contributes the most revenue today?

Servers and datacenter accelerators lead with 39.17% of 2025 revenue due to hyperscale AI training demand.

What memory technology is gaining popularity in training clusters?

High-bandwidth memory is advancing at a 20.98% CAGR through 2031 as AI workloads need bandwidth above 3 TB s⁻¹.

How are automotive manufacturers using discrete GPUs?

Electric-vehicle makers such as Li Auto, NIO and XPeng embed GPUs in centralized compute boxes to enable Level 3-plus autonomy, pushing annual automotive GPU shipments toward 2 million units by 2027.

Page last updated on: