India Automotive Lighting Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.73 Billion |

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

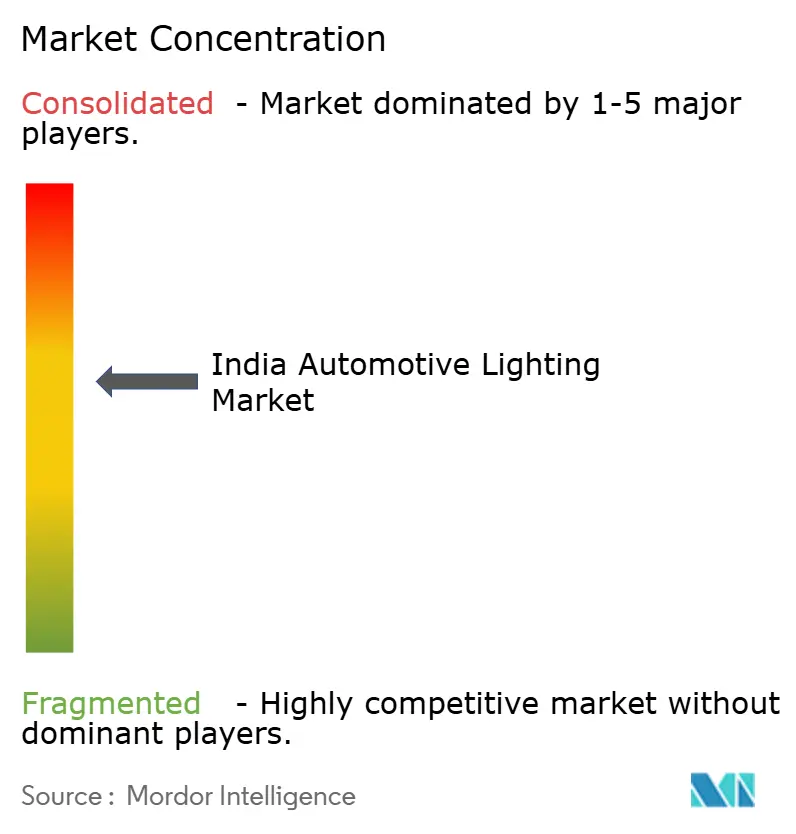

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Automotive Lighting Market Analysis by Mordor Intelligence

The Indian automotive lighting market size was valued at USD 1.73 billion in 2025 and is expected to increase from USD 1.83 billion in 2026 to reach USD 2.44 billion by 2031, growing at a CAGR of 5.87% over 2026-2031. Mandatory domestic-value-addition thresholds under the Production Linked Incentive (PLI) scheme are steering suppliers toward local integration, while energy-efficiency rules that favor light-emitting diodes (LEDs) accelerate technology replacement cycles. Continuing incentives under FAME-II for electric two-wheelers reinforce LED demand because power budgets on battery platforms reward low-wattage lamps. AIS-008 and AIS-012 safety regulations are prompting original-equipment manufacturers (OEMs) to standardize on daytime running lamps and adaptive front lighting, deepening content per vehicle.

Key Report Takeaways

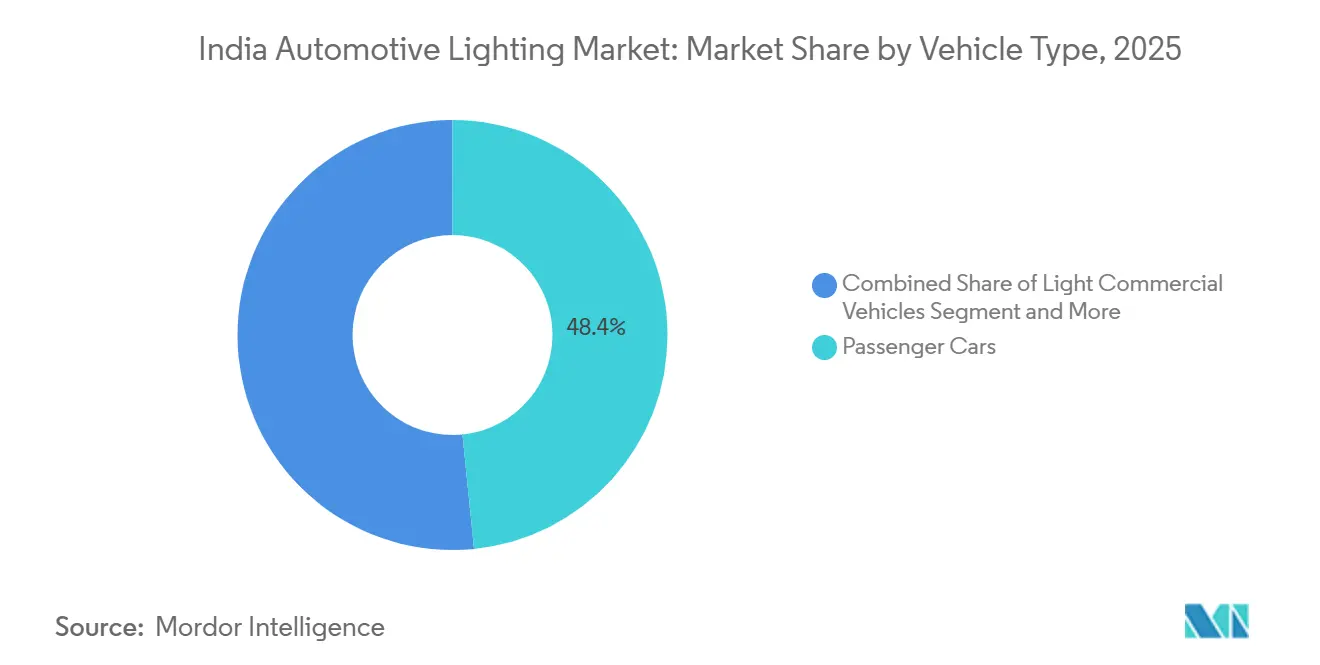

- By vehicle type, passenger cars retained the largest 48.41% of the Indian automotive lighting market share in 2025, while two-wheelers will post the fastest growth at a 6.01% CAGR through 2031.

- By application, exterior lighting led with 63.21% of the Indian automotive lighting market share in 2025, and the same segment is projected to expand at a 6.11% CAGR during 2026-2031.

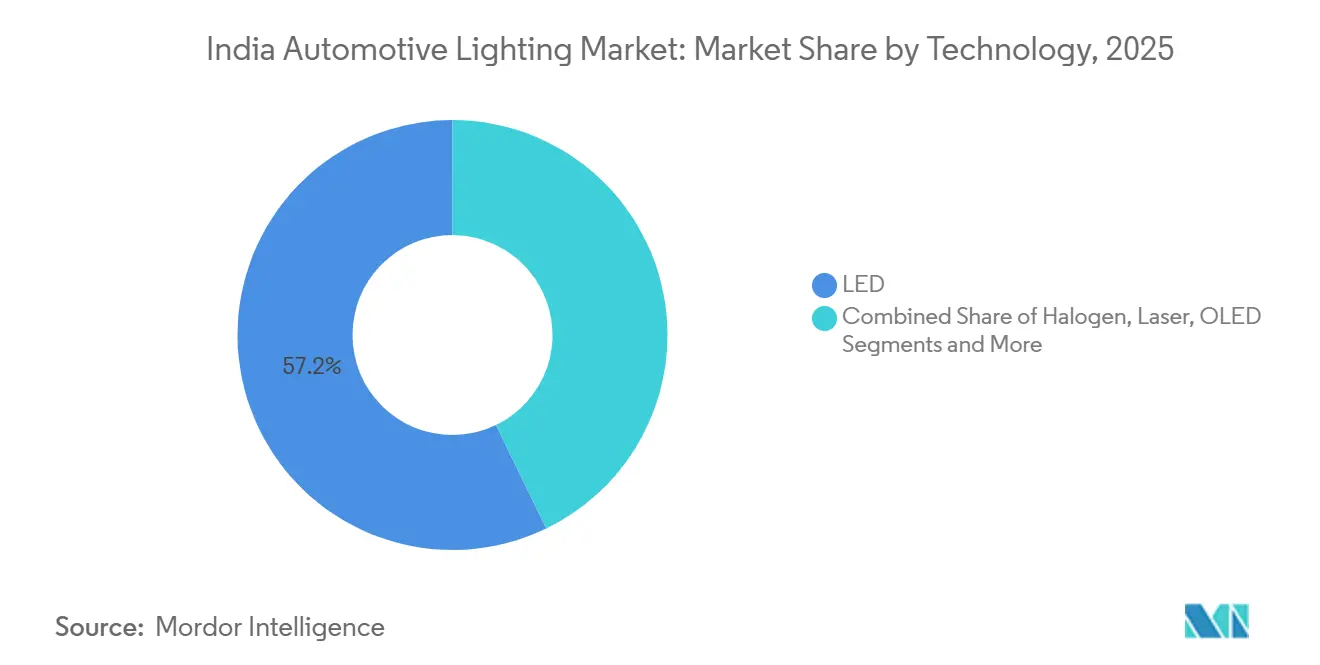

- By technology, LEDs dominated the Indian automotive lighting market with 57.18% of the market share in 2025; laser headlamps are projected to record the highest 6.06% CAGR to 2031.

- By sales channel, OEM sales accounted for 67.73% of the Indian automotive lighting market share in 2025, whereas the aftermarket is forecasted to log a 6.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on automotive lighting market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Automotive Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LED Price Erosion | +1.2% | National, with early adoption in metro cities | Short term (≤ 2 years) |

| AIS-008 / AIS-012 Safety Regulations Enforcement | +1.0% | National, with stricter enforcement in Gujarat, Maharashtra | Medium term (2-4 years) |

| Electrification Push Under FAME-LI | +0.9% | National, concentrated in EV manufacturing hubs | Medium term (2-4 years) |

| Tier-1 Localisation Incentives | +0.8% | Manufacturing clusters in Maharashtra, Gujarat, Tamil Nadu, Delhi NCR | Long term (≥ 4 years) |

| ADAS-Ready Adaptive Lighting | +0.6% | Premium vehicle segments, urban markets | Long term (≥ 4 years) |

| Smart-Corridor Pilots | +0.3% | Pilot corridors, smart cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LED Price Erosion and Energy-Efficiency Mandates

Declining component costs coupled with Bureau of Energy Efficiency thresholds have made LEDs the default fitment across price bands. OEM contracts now specify LEDs even for entry-level scooters to meet candela requirements without thermal penalties. Domestic suppliers that invested in automated surface-mount lines under the PLI scheme are capturing this shift, while halogen demand retreats to legacy replacement channels. The virtuous cost-volume cycle is compressing LED module prices toward parity with halogen assemblies, sealing the latter’s obsolescence.

AIS-008 / AIS-012 Safety Regulations Enforcement

Type-approval audits for headlamps and signaling devices became more stringent in 2025[1]"New Capabilities / Development," ARAI, www.araiindia.com. Tier-one suppliers with in-house photometric tunnels readily comply, whereas gray-market assemblers struggle to certify their products. Enforcement actions have already removed several non-conforming aftermarket lamps from urban retail shelves. Over time, sustained surveillance is expected to marginalize uncertified bulbs, improving lumen stability and color consistency on Indian roads.

Electrification Push Under FAME-LI Boosting 2-W and 4-W LED Fitment

Subsidies that hinge on energy consumption benchmarks oblige electric two-wheeler and passenger-car manufacturers to deploy low-draw lamps. LED daytime running lamps, tail lamps, and backlit instrument clusters therefore ship as standard on most incentive-eligible models. Suppliers are scaling new facilities in lighting clusters around Pune, Chennai, and Sanand to serve this rising baseline. As the subsidy window closes in 2028, the installed LED fleet will have reached critical mass, locking future aftermarket cycles into solid-state technologies.

Tier-1 Localisation Incentives (PLI-Auto and Specs)

The PLI-Auto program disburses bonuses when 50% local value-addition thresholds are met, prompting tier-one suppliers to backward-integrate optics, driver electronics, and housings. Greenfield plants in Gujarat and Tamil Nadu now mold polycarbonate lenses and assemble printed circuit boards on site, trimming import reliance[2]'"INR 90000 Million New Polycarbonate Resins Mfg. Unit in Dahej, Gujarat," New Projects Tracker, www.newprojectstracker.com. Complementary SPECS grants for semiconductor devices encourage pilot lines for LED driver integrated circuits, reducing currency exposure linked to offshore sourcing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High GST Slab | -0.7% | National, affecting premium vehicle segments | Medium term (2-4 years) |

| Prevalence Of Counterfeit Aftermarket Bulbs | -0.6% | National, concentrated in tier-2/3 cities and online channels | Medium term (2-4 years) |

| LED-Driver Semiconductor Shortages | -0.5% | Global supply chain impact, affecting all regions | Short term (≤ 2 years) |

| Low Consumer Awareness In Tier-2/3 Cities | -0.5% | Tier-2 and tier-3 cities, rural and semi-urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High GST Slab and Import Duty on Advanced Lighting Modules

Combined levies exceeding 40% on imported complete units of laser and matrix-LED assemblies are dampening OEM enthusiasm for widespread adoption in the mass segment. While only luxury brands are shouldering the extra costs to provide long-range laser high beams, local joint ventures are hurrying to localize sub-assemblies. Their goal is to make premium features more affordable without the burden of duty inflation.

LED-Driver Semiconductor Shortages

In several northern states, unorganized workshops are pushing uncertified replacements. While these lamps fail to meet photometric standards and reduce reflector lifespan, their affordability lures budget-conscious buyers. Authorities are conducting raids on these illicit stocks, and e-commerce platforms are ramping up authentication efforts to combat this gray market. Looking ahead, as consumers become more aware and QR-based product verification gains traction, sales of counterfeit products are expected to decline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Two-Wheelers Outpace Passenger Cars

Passenger cars constituted the largest 48.41% share of the Indian automotive lighting market in 2025, reflecting broad LED adoption across hatchbacks and sedans. In contrast, two-wheelers will grow the fastest, at a 6.01% CAGR, as newer scooters and motorcycles now feature automatic headlamp-on functions that mandate reliable solid-state lamps. Segment-specific regulations continue to elevate lighting content, making motorcycles a critical volume driver.

The regulatory tailwind encourages suppliers to customize compact LED modules for motorcycles that also meet splash-resistance norms for Indian monsoons. OEM design cycles have therefore shortened, as modular lamp housings allow brands to refresh aesthetics annually. While passenger cars continue to dominate value terms, accelerating scooter electrification firmly embeds two-wheelers in long-term growth narratives, balancing the market’s segment mix without diluting unit profitability.

By Application: Exterior Lighting Dominates, Interior Gains Traction

Exterior functions captured 63.21% of the Indian automotive lighting market in 2025, a lead cemented by daytime running lamps, adaptive front-lighting, and full-width tail bars that double as unmistakable brand signatures. OEM designers treat headlamps as “eyes” that must meet strict beam cutoff regulations while still packaging seamlessly into sculpted fascias. That dual imperative keeps exterior systems at the top of budget lists when engineering choices are made, ensuring incremental upgrades even in carry-over models. The 6.11% CAGR projected for exterior lamps also reflects planned rollouts of wider light bars whose continuous illumination improves conspicuity at dusk and during monsoon downpours.

Interior illumination, although smaller, now serves as a tactile differentiator in connected vehicles and electric cab-ins. Multi-zone RGB strips enable drivers to sync mood lighting with infotainment themes, turning the cabin ambiance into a software-defined experience. Vendors respond by shipping plug-and-play LED rails that integrate diffusers and CAN bus controllers into a single, slim form factor, reducing line assembly time. While exterior systems still dominate total value, expanding cabin-personalization menus ensure that interior orders rise in lockstep with higher trim penetrations. Suppliers see the two streams as complementary rather than competitive, since a single LIN-bus gateway can orchestrate both headlamp leveling and foot-well ambiance.

By Technology: LED Leads, Laser Niche Emerges

LEDs held 57.18% of the Indian automotive lighting market size in 2025, a share earned through a compelling mix of energy savings, compact footprints, and falling dollar-per-lumen costs. Tier-one companies have now standardized surface-mount lines that spit out modular arrays ready for drop-in assembly across cars, scooters, and light trucks. Halogen volumes continue to recede as price parity improves and as photometric rules squeeze legacy bulbs that struggle with heat dissipation at higher candela outputs. Laser headlamps, while still limited to premium imports, are set to clock the fastest 6.06% CAGR through 2031 as domestically tooled optics rein in cost and as adaptive-beam software gains field mileage.

Competitive tension now centers on who can scale advanced driver-assistance integration first. Matrix LEDs already talk to camera modules for automatic high-beam cut-offs, and suppliers are prototyping next-gen controllers that fuse radar data to pre-empt glare in fog. Over-the-air firmware enables continuous improvement, extending product relevance beyond physical production windows. At the opposite end, aftermarket halogen refits linger for legacy vehicles but will taper as solid-state units age into their first replacement cycle. Policy nudges, such as lower GST slabs for domestically built LED chips, may widen the gap as fabricators ramp pilot wafer lines under SPECS incentives.

By Sales Channel: Aftermarket Gains on OEM

OEM fitments accounted for 67.73% of the Indian automotive lighting market share in 2025 because lamps sit on the critical path for type approval and crash-test scheduling. Car companies sign multiyear supply agreements that lock in optical performance and spare-part codes, creating predictable pull for tier-one lines. Yet the aftermarket will edge forward at a 6.08% CAGR to 2031 as the first LED-equipped models sold earlier in the decade age into replacement cycles. E-commerce storefronts accelerate this shift by offering VIN-matched look-ups and doorstep installs that bypass traditional brick-and-mortar shortages in tier-two cities. Organized distributors now bundle QR-code authentication to fight counterfeit inflows, signaling a maturing channel that prizes verified lumen output over rock-bottom price.

The OEM channel remains lucrative, but competitive bids increasingly factor total-cost-of-ownership models that weigh lumen degradation curves and warranty liabilities. Fleet operators, especially in ride-hailing and last-mile delivery, adopt preventive replacement schedules that swell aftermarket unit counts and favor durable LEDs over short-life halogens. Counterfeit clamp-downs by state enforcement agencies further redirect demand to legitimate sellers whose products carry AIS compliance markings. As rural internet penetration rises, even tier-three buyers tap online tutorials to self-diagnose headlamp faults, creating micro-markets for plug-and-play LED conversions.

Geography Analysis

Maharashtra anchors the Indian automotive lighting market with an ecosystem that ranges from raw-material converters to automated final-assembly cells clustered around Pune and Nashik. Multimodal logistics hubs allow just-in-time deliveries to nearby passenger-car plants, trimming inventory carrying costs for bulky headlamp assemblies. The state’s policy of fast-track environmental clearances cuts lead times for line expansions, a key draw for high-precision optical tooling. Neighboring Gujarat has mirrored this success by courting marquee investments in Sanand, where dedicated lighting parks supply both domestic OEMs and export orders bound for Southeast Asia. Tax holidays in the region sweeten capital outlays, ensuring accelerated breakeven timelines for new LED lines.

Tamil Nadu forms the southern pole, leveraging decades-old motorcycle clusters around Chennai and Hosur to specialize in compact LED modules optimized for two-wheeler form factors. State subsidies for skilling programs create a large pool of technicians, easing the adoption of automated surface-mount technology and optical test rigs. Ports at Ennore and Tuticorin streamline component imports when local substitutes remain unavailable, though PLI milestones encourage inbound localization every fiscal year. Karnataka complements this matrix with a concentration of premium OEMs and emerging electric-vehicle start-ups across the Bangalore-Mysore belt. This mix demands adaptive headlamps and ambient interior kits as brand differentiators.

Northern and eastern belts present contrasting challenges and opportunities. Haryana’s proximity to Delhi-NCR passenger-car plants ensures baseline volumes, but legacy halogen demand lingers in agricultural haulage fleets that prioritize upfront cost over energy savings. Uttar Pradesh, Madhya Pradesh, and Bihar remain replacement-heavy territories with higher counterfeit risk due to fragmented retail and weaker regulatory oversight. Nonetheless, rapid smartphone adoption fuels direct-to-consumer LED upgrades that bypass traditional intermediaries, slowly tilting demand toward certified lamps. Further east, emerging highway corridors are home to smart-lighting pilots, such as the Chennai-Tiruchi IoT-based deployment, foreshadowing vehicle-to-infrastructure data loops that will eventually inform adaptive beams.

Competitive Landscape

The Indian automotive lighting market shows moderate concentration, with the top five suppliers shaping core technology roadmaps while leaving room for agile challengers. Lumax, Koito, Varroc, Hella, and Uno Minda collectively bank on long-running OEM contracts that embed them deeply in platform development calendars. Their balance sheets support photometric tunnels and environmental chambers, which are critical for passing AIS audits on the first attempt. Even so, joint ventures, such as Tata AutoComp’s tie-up with Ichikoh, hint at a phase of selective consolidation aimed at pooling optical patents and widening product breadth.

Second-tier contenders target white spaces in micro-LED arrays and OLED tail signatures where big players move more cautiously. Firms like Neolite ZKW secure design wins by offering quicker tooling swaps for mid-cycle facelifts, appealing to OEM studios chasing distinctive light graphics. Start-ups in Gujarat are shifting their focus to solid-state controllers that simplify over-the-air firmware updates, recognizing that software-driven beam shaping may trump raw hardware specs in future tenders. Competition thus broadens from physical lamp assemblies to integrated electronic control units, tightening the handshake between lighting and ADAS domains.

Global strategies ripple into the domestic arena as well. Koito’s medium-term plan to double shipments to non-Japanese OEMs positions its Gujarat plant as an export springboard into ASEAN, thereby raising utilization ceilings faster than India-only demand could. Valeo’s camera-module expansion in Sanand underscores a trend toward sensor-fusion packages that bundle forward-lighting with vision processing, a synergy that premium SUVs already exploit. Meanwhile, Marelli-Motherson’s new Sanand facility showcases edge-to-edge light bars fabricated with 17 mm slim modules that satisfy both stylistic minimalism and aerodynamic efficiency goals.

India Automotive Lighting Industry Leaders

-

UNO Minda

-

Lumax Industries Limited

-

Koito Manufacturing Co., Ltd.

-

Varroc Group

-

HELLA GmbH & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Marelli-Motherson inaugurated a specialized exterior-lighting facility in Sanand, Gujarat, unveiling a cutting-edge edge-to-edge light-bar feature tailored for next-gen passenger vehicles.

- January 2026: Neolite ZKW opened a new facility in Pune, featuring a standalone design center. This center is outfitted for optical simulation, rapid prototyping, and the validation of cutting-edge headlamp designs.

- August 2025: Tata AutoComp and Ichikoh Industries formed a joint venture to acquire Valeo India's lighting business, enhancing their portfolios and entering India's automotive lighting market.

India Automotive Lighting Market Report Scope

The Indian Automotive Lighting Market is analyzed based on vehicle type, application, technology, and sales channel.

By Vehicle Type, the market is segmented into Passenger Cars, Light Commercial Vehicles, Medium & Heavy Commercial Vehicles, and Two-Wheelers. By Application, the market is segmented into Exterior (Headlamps, Taillights, Daytime Running Lights, and Fog Lamps) and Interior (Ambient / Footwell and Roof / Dome Lights). By Technology, the market is segmented into Halogen, Xenon / HID, LED, Laser, and OLED. By Sales Channel, the market is segmented into OEM and Aftermarket.

Market forecasts are provided in terms of Value (USD) and Volume (Units).

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Two-Wheelers |

| Exterior | Headlamps |

| Taillights | |

| Daytime Running Lights (DRLs) | |

| Fog Lamps | |

| Interior | Ambient / Footwell |

| Roof / Dome |

| Halogen |

| Xenon / HID |

| LED |

| Laser |

| OLED |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| Two-Wheelers | ||

| By Application | Exterior | Headlamps |

| Taillights | ||

| Daytime Running Lights (DRLs) | ||

| Fog Lamps | ||

| Interior | Ambient / Footwell | |

| Roof / Dome | ||

| By Technology | Halogen | |

| Xenon / HID | ||

| LED | ||

| Laser | ||

| OLED | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

Key Questions Answered in the Report

How large is the India automotive lighting market in 2026?

The market is valued at USD 1.83 billion in 2026 and is forecast to reach USD 2.44 billion by 2031 and is projected to grow at a CAGR of 5.87% through 2031.

Which vehicle type segment grows fastest within the market?

Two-wheeler lighting records the highest 6.01% CAGR through 2031, helped by mandatory automatic headlamp-on rules.

What technology leads new-vehicle fitment?

LEDs hold the top 57.18% share because they balance energy savings with affordability, whereas laser systems stay niche.

Where are most lighting plants located?

Manufacturing clusters concentrate in Maharashtra, Tamil Nadu, Gujarat, Haryana, and Karnataka, aligning with nearby OEM assembly hubs.

Page last updated on: