Cloud Project Portfolio Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

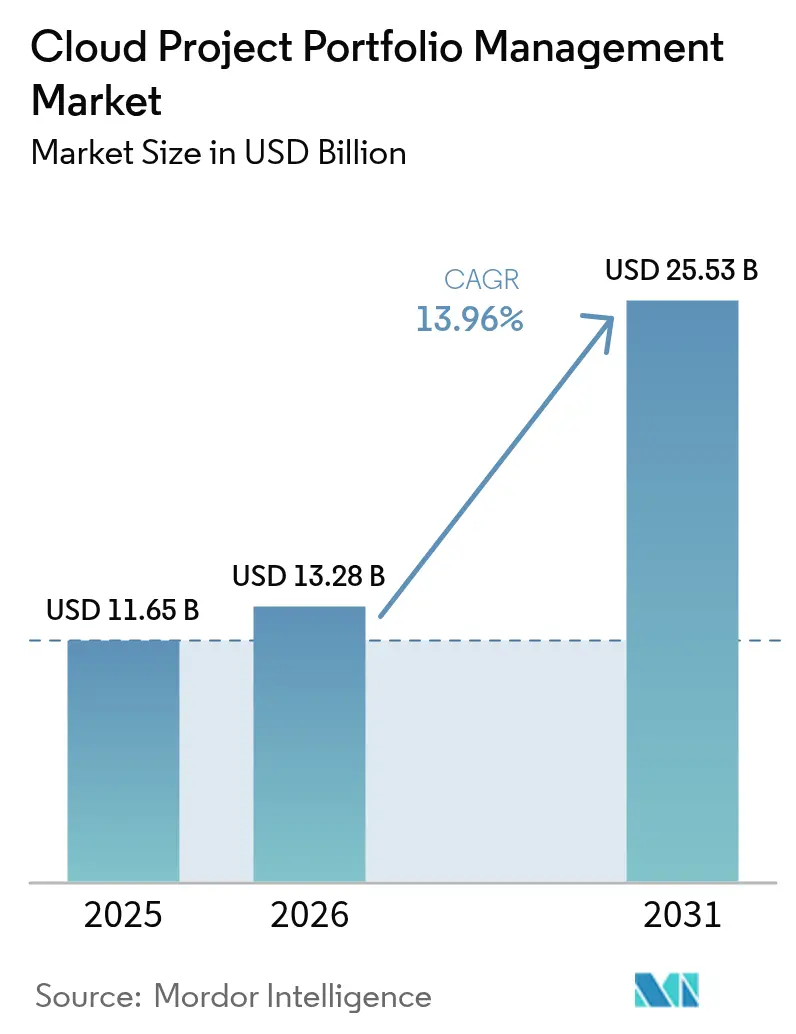

| Market Size (2026) | USD 13.28 Billion |

| Market Size (2031) | USD 25.53 Billion |

| Growth Rate (2026 - 2031) | 13.96% CAGR |

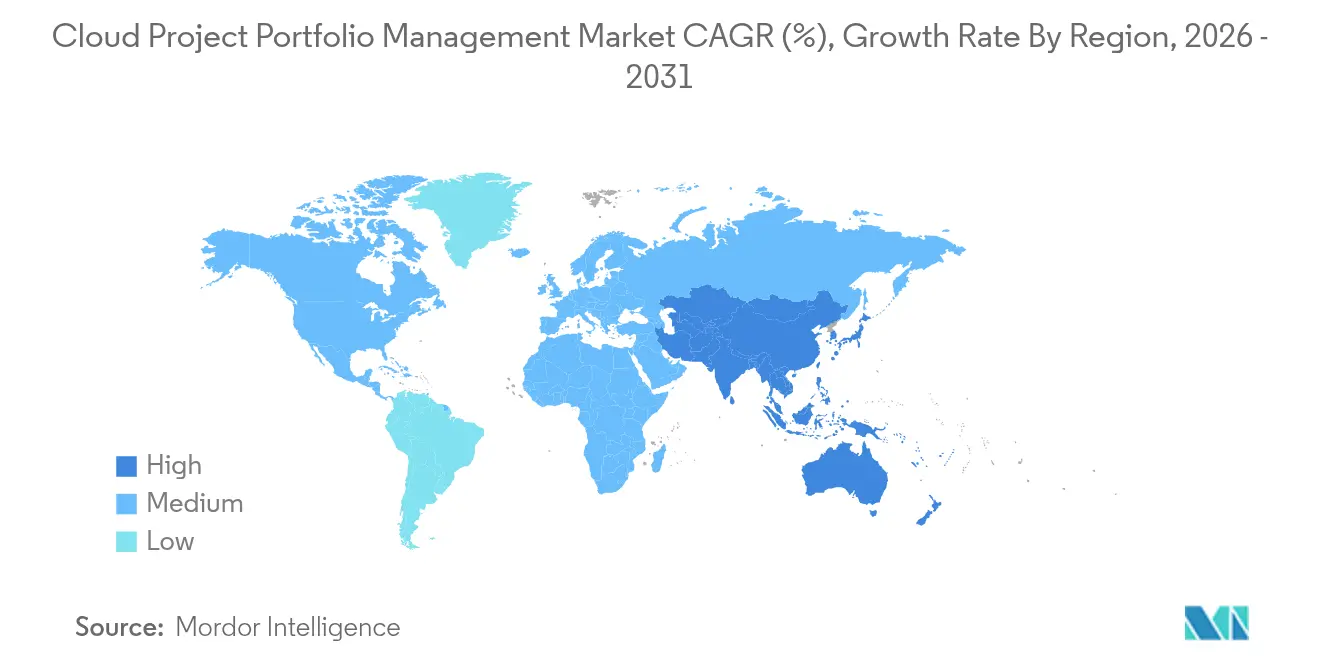

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Project Portfolio Management Market Analysis by Mordor Intelligence

The cloud project portfolio management market size was valued at USD 11.65 billion in 2025 and estimated to grow from USD 13.28 billion in 2026 to reach USD 25.53 billion by 2031, at a CAGR of 13.96% during the forecast period (2026-2031). Rapid adoption of artificial intelligence, convergence of FinOps workflows, and the need to orchestrate hybrid workforces underpin the expansion of this software category. Demand accelerates in manufacturing settings where Industry 4.0 programs generate intricate, multi-vendor initiatives that require unified project oversight. Large enterprises still anchor spending; however, small and medium enterprises are scaling deployments quickly as subscription pricing removes IT-infrastructure hurdles. Deployment patterns show a pivot toward hybrid cloud estates that blend on-premise data stewardship with cloud-native analytics, while regional dynamics reveal Asia-Pacific closing the gap with North America on the strength of government-backed digitization investments. Competitive intensity is shaped by AI-first, cloud-native vendors that challenge incumbent enterprise software suppliers through predictive resource planning and real-time collaboration functions.

Key Report Takeaways

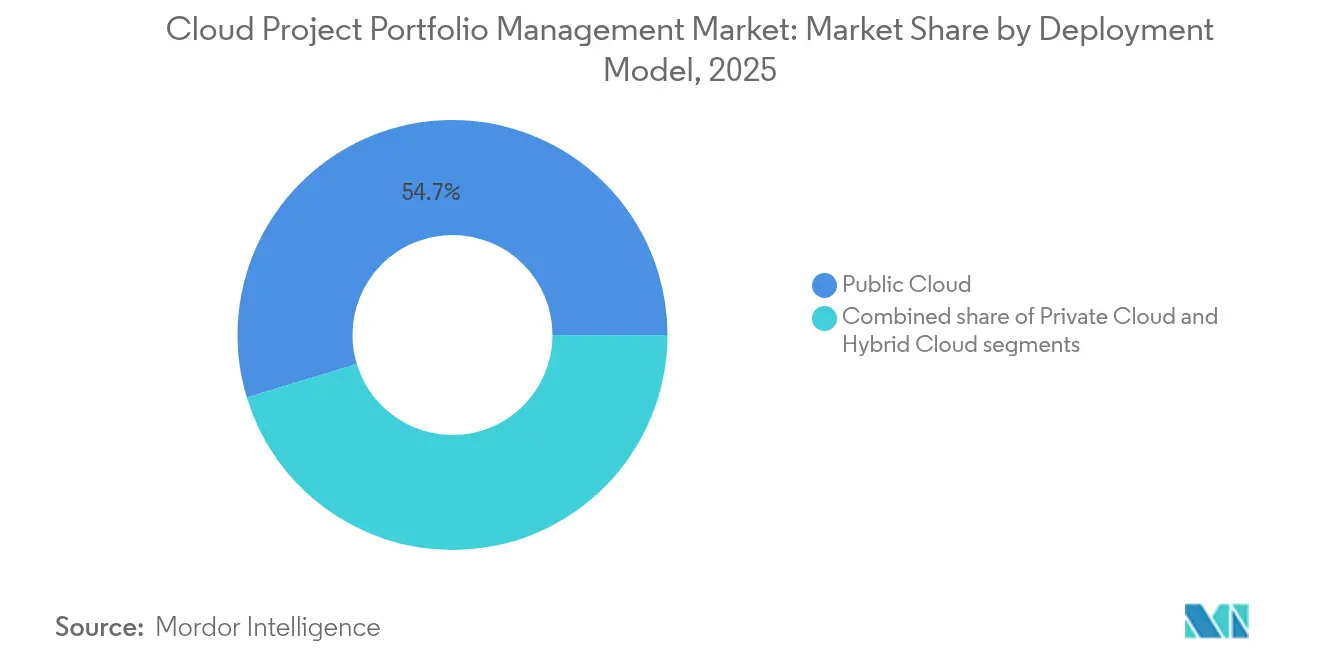

- By deployment model, public cloud led with 54.70% revenue share in 2025; hybrid cloud is projected to grow at a 15.05% CAGR to 2031.

- By application, portfolio management held 45.20% of the cloud project portfolio management market share in 2025, while resource management is advancing at a 14.65% CAGR through 2031.

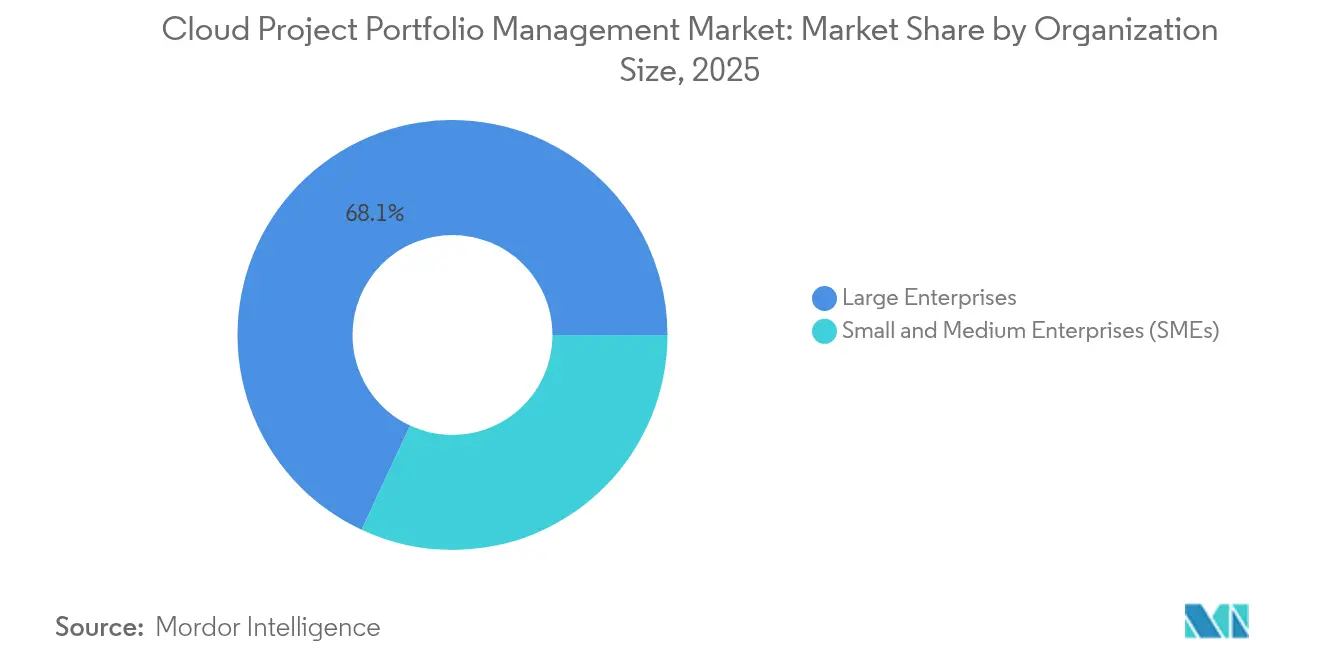

- By organization size, large enterprises captured 68.05% of the cloud project portfolio management market size in 2025; SMEs are forecast to expand at a 15.35% CAGR between 2026 and 2031.

- By industry vertical, IT and telecommunications accounted for 35.20% revenue share in 2025; manufacturing is forecast to grow at a 14.12% CAGR through 2031.

- By geography, North America led with 37.10% revenue share in 2025, whereas Asia-Pacific is set to record a 14.40% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Project Portfolio Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing BYOD and mobile-first workforce | +2.1% | Global, North America and EU focus | Short term (≤ 2 years) |

| Higher adoption of cloud analytics | +2.8% | Asia-Pacific core, North America spill-over | Medium term (2-4 years) |

| Shift toward hybrid / remote work models | +3.2% | Global, developed markets | Medium term (2-4 years) |

| Need for real-time portfolio visibility and ROI optimization | +2.5% | North America and EU, expanding Asia-Pacific | Short term (≤ 2 years) |

| FinOps-driven cost-governance integration | +1.9% | Global, cloud-mature firms | Long term (≥ 4 years) |

| AI-powered predictive project-health scoring | +2.7% | North America and EU early adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing BYOD and mobile-first workforce

Sixty-one percent of project management professionals now operate remotely at least part-time. Mobile access has therefore shifted from convenience to a baseline requirement. Enterprises migrating from desktop-centric tools prioritize responsive interfaces, biometric security, and offline sync to ensure continuity in travel or low-bandwidth scenarios. Technology and professional-services firms adopt mobile-optimized suites fastest because billable time hinges on instantaneous status updates. Vendors that embed push notifications and voice commands differentiate by allowing field engineers and consultants to react without opening laptops. As device diversity grows, platform compatibility becomes a decisive buying criterion for IT procurement leaders.

Higher adoption of cloud analytics

Organizations analyze historical project artifacts to forecast completion probabilities, flag resource bottlenecks, and quantify risk exposure. Machine-learning modules embedded in cloud project portfolio management market offerings accelerate this shift from descriptive dashboards to predictive insights. Enterprises running multi-year transformation programs benefit most, because statistical models surface interdependencies hidden in spreadsheets. Moreover, cost allocation accuracy improves when embedded analytics trace actual labor and infrastructure usage. Executives thus base prioritization decisions on empirical performance rather than intuition, which raises portfolio throughput and budget fidelity.

Shift toward hybrid/remote work models

Hybrid arrangements reshape collaboration norms by blending agile and predictive methodologies across time zones. Digital whiteboards, embedded video conferencing, and shared document repositories now ship as standard modules in cloud project portfolio management market platforms. Organizations that unify task, resource, and financial views inside the same interface avoid the silos that previously plagued distributed teams. Asynchronous communication features, such as threaded context within Gantt views, maintain momentum when colleagues are offline, while automated reminders enforce sprint cadences. The trend cements long-term demand for cloud-native suites that deliver identical experiences on desktop and mobile endpoints.

Need for real-time portfolio visibility and ROI optimization

Boards and CFOs demand continuous insight into strategic alignment, burn rates, and resource utilization. Modern dashboards ingest live data streams from DevOps, HR, and finance systems, translating them into heat-maps that flag projects at risk of schedule or budget overrun. Automated variance alerts reduce reliance on manual status reporting, freeing project managers to focus on remediation. Integrating earned-value analysis with scenario planning lets executives rebalance investment toward initiatives with superior return potential. As a result, platforms that combine financial and operational metrics achieve higher retention among Fortune 500 clients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent security and privacy concerns | -1.8% | Global, high in EU and Germany | Short term (≤ 2 years) |

| Vendor lock-in across multi-cloud ecosystems | -1.4% | North America and EU | Medium term (2-4 years) |

| Lack of unified data taxonomies for AI models | -1.1% | Global | Long term (≥ 4 years) |

| Emerging ESG-reporting complexity | -0.9% | EU-led, expanding | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent security and privacy concerns

Seventy-one percent of German cloud executives cite high cybersecurity anxiety when shifting project data off-premise[1]IBM Security, “Cloud Security Index 2025,” ibm.com. Industries handling intellectual property or patient records often keep sensitive artifacts on-site, resorting to hybrid configurations that restrict external access. Fragmented international regulations such as GDPR add compliance overhead and force data-residency checks during portfolio planning. Though major vendors invest in zero-trust architectures and region-specific data centers, breach headlines still sway risk-averse boards. Consequently, procurement cycles elongate and pilot scopes narrow in financial services and healthcare.

Vendor lock-in across multi-cloud ecosystems

Eighty-five percent of enterprises operate workloads on two or more public clouds yet struggle to orchestrate them coherently. Proprietary workflow engines risk trapping metadata within a single provider, complicating exit strategies. Organizations therefore prioritize platform-agnostic tools built on open APIs and portable containers. Suppliers that certify interoperability with AWS, Azure, Google Cloud, and Oracle gain traction, particularly among conglomerates that inherit heterogeneous stacks via mergers. Absence of standardized cost-allocation tags across clouds further reinforces buyer hesitation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Cloud Drives Strategic Flexibility

Hybrid architectures recorded a 15.05% CAGR and continue to outpace other models as enterprises balance sovereignty with elasticity. The cloud project portfolio management market size for hybrid deployments is forecast to represent USD 10.06 billion by 2031, reflecting the segment’s strategic importance. Regulated industries prefer to process sensitive artifacts on-premise while streaming anonymized telemetry to cloud analytics engines for capacity planning. Hybrid suites integrate VPN orchestration, policy-based workload placement, and AI-assisted latency optimization, enabling project teams to place data where compliance and cost objectives align.

Vendor roadmaps reveal deeper support for edge nodes that synchronize intermittently yet preserve full functionality in disconnected scenarios. Automotive and defense contractors, for example, leverage offline-first capability to run simulations in secure facilities, later syncing progress to global stakeholders. Public cloud retains the broadest ecosystem and 54.70% revenue share, but hybrid’s growth trajectory underscores a shift toward mixed tenancy. Private cloud remains relevant for firms requiring complete tenant isolation; however, capital expenditure and talent demands curb its uptake. As cloud maturity rises, the cloud project portfolio management market sees heightened demand for policy engines that automate optimal workload distribution.

By Application: Resource Management Gains Strategic Priority

Resource management software is expanding at a 14.65% CAGR, outstripping portfolio governance modules. In 2025, portfolio management commanded 45.20% of revenue, yet capacity-planning pain points elevate resource-centric features in buying criteria. The cloud project portfolio management market share for resource management solutions reached 22.10% in 2025 and is expected to climb steadily. Predictive staffing algorithms match skills with sprint deliverables, reducing idle time and minimizing expensive contractor reliance. Professional services firms report margin lifts after adopting AI-driven allocation that quantifies probability-weighted utilization scenarios.

Integrated skills matrices and learning-path suggestions further connect talent development with delivery outcomes. Demand management, time tracking, and financial control modules converge into unified suites, creating a single source of truth for workforce and cost data. Vendors embedding natural-language chatbots simplify resourcing decisions for non-technical managers. Meanwhile, portfolio governance remains essential for strategic alignment, especially in conglomerates funding hundreds of concurrent initiatives. Yet the fastest value capture often occurs when under-resourced teams promptly redeploy staff to high-impact milestones, explaining the segment’s momentum.

By Organization Size: SMEs Accelerate Cloud Adoption

Small and medium enterprises exhibit a 15.35% CAGR as intuitive interfaces and pay-as-you-go pricing democratize enterprise-grade functionality. The segment accounted for 31.95% of the cloud project portfolio management market size in 2025 and will approach parity with large enterprises by 2031. Templates that pre-configure workflows for marketing launches or software sprints cut setup times from months to days. MDPI survey data indicates SMEs cite faster time-to-value and lower administrative overhead as top reasons for cloud migration.

Startups often leapfrog legacy on-premise stacks entirely, deploying single-sign-on and API integrations via marketplace click-through. Vendors respond by bundling onboarding services and community forums that substitute for large IT departments. Large enterprises still spend more in absolute terms due to customization, security reviews, and global rollouts, but their CAGR lags as many have already modernized their flagship portfolios. Hybrid governance boards at multinationals now pilot lightweight tools in business units, borrowing usability lessons from SME-oriented products to rejuvenate employee engagement.

By Industry Vertical: Manufacturing Leads Digital Transformation

Manufacturing adoption is climbing at a 14.12% CAGR, propelled by digitized supply chains and complex product lifecycles. Automotive and aerospace engineers coordinate firmware updates, mechanical design, and compliance artefacts across suppliers, making real-time visibility critical. The cloud project portfolio management market size for manufacturing is projected to exceed USD 3.92 billion by 2031. Digital twins, additive manufacturing projects, and smart-factory retrofits introduce interdependencies that traditional spreadsheets cannot manage.

IT and telecommunications remained the largest spenders with a 35.20% share in 2025, citing software-release cadences and customer experience initiatives. Healthcare, life sciences, and public sector players deploy the platforms to maintain audit trails and unify grant-funded research. Vendor roadmaps increasingly include industry-specific accelerators, such as validated templates for ISO 13485 medical device compliance. This vertical tailoring shortens sales cycles and creates stickiness by embedding regulatory nuance directly in workflow logic.

Geography Analysis

North America led the cloud project portfolio management market with a 37.10% share in 2025. United States operators in finance, aerospace, and technology anchor high-value enterprise rollouts, while Canada’s natural-resources firms implement cloud suites to manage capital-intensive projects. Mexico’s manufacturing corridors adopt the software to coordinate near-shore production schedules with US buyers. Mature SaaS penetration, robust 5G coverage, and deep reskilling programs sustain regional demand; nonetheless, heightened scrutiny on data residency keeps hybrid and sovereign-cloud options in focus.

Asia-Pacific is the fastest-growing theatre at a 14.40% CAGR through 2031. China’s state-backed digital-economy programs incentivize local manufacturers to migrate engineering workflows to the cloud. Indian service integrators embed project portfolio management into client delivery frameworks, accelerating toolchain standardization. Japanese and South Korean conglomerates integrate factory-floor IoT telemetry with portfolio dashboards to compress time-to-market for electronics. Rapid submarine-cable expansion and hyperscaler datacenter investment lower latency, encouraging real-time collaboration across ASEAN project teams.

Europe maintains steady mid-single-digit growth. German automotive giants enforce stringent data-sovereignty controls that favor regional providers and hybrid deployment. United Kingdom enterprises in life sciences pursue cloud suites to track multistage clinical trials under MHRA oversight. France, Italy, and Spain add momentum via public-sector modernization funds. Nordic firms prove early adopters of AI-infused resource scheduling, aligning with their advanced digital-government agendas. Regulatory complexity, including GDPR and forthcoming AI Act provisions, extends vendor qualification cycles but ultimately drives premium pricing for compliant offerings.

Competitive Landscape

Competition is moderate with a blend of diversified software titans and cloud-native specialists. Microsoft, Oracle, and SAP capitalize on installed ERP footprints to cross-sell integrated portfolio modules. Oracle’s collaboration with Microsoft to host Oracle Database@Azure illustrates the market’s push to simplify multi-cloud operations[3]Oracle Corporation, “Oracle Database@Azure Press Release January 2025,” oracle.com. Atlassian, Smartsheet, and monday.com pursue ease of use and rapid iteration, often landing in departmental budgets before expanding enterprise-wide.

Differentiation centers on embedded AI and extensibility. Atlassian’s Rovo launch integrates knowledge discovery and generative answers, positioning the firm to upsell predictive workflow automation. ServiceNow invests in regional partners, such as inMorphis, to localize generative-AI features for banking and telecoms. Vendors are also layering no-code builders so domain experts can tailor intake forms, approval gates, and KPIs without IT tickets. Open API ecosystems remain pivotal as clients demand bi-directional sync with DevOps, HRIS, and finance systems to maintain data congruence.

White-space exists in industry-specific compliance accelerators and edge-aware orchestration that harmonizes factory-floor data with cloud analytics. Mergers and acquisitions and strategic partnerships will likely intensify as platform players acquire AI start-ups to advance schedule-risk forecasting. Enterprises evaluating vendors rank cyber-security certifications, roadmap transparency, and customer success maturity alongside feature depth. Market leaders with expansive support footprints and flexible deployment options hold an advantage as regulatory landscapes tighten.

Cloud Project Portfolio Management Industry Leaders

Broadcom Corporation

Hewlett Packard Enterprise Development LP

Changepoint Corporation

Clarizen, Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Microsoft and Oracle extended their alliance via Oracle Database@Azure, offering co-located databases for unified workload management and lower latency.

- January 2025: Atlassian surpassed USD 5 billion in annual run-rate revenue, citing 30% year-over-year subscription growth and more than 1 million monthly active AI users.

- November 2024: Atlassian posted 21% Q1 FY25 revenue growth to USD 1.188 billion, highlighting the launch of Rovo and Atlassian Focus for enterprise knowledge orchestration.

- May 2024: ServiceNow invested in inMorphis to deepen coverage in India and ASEAN while co-developing generative-AI modules for finance and telecoms.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cloud project portfolio management (CPPM) market as subscription-based software platforms delivered through public, private, or hybrid clouds that let organizations plan, prioritize, fund, execute, and monitor multiple projects from a single digital workspace. These suites bundle modules such as portfolio analytics, resource and capacity planning, financial governance, and real-time collaboration features, and they are licensed on a per-user or usage tier basis.

Scope exclusion: on-premise PPM installations, stand-alone task trackers, and pure professional-services revenue sit outside our CPPM boundary.

Segmentation Overview

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Application

- Portfolio Management

- Demand Management

- Project Management

- Resource Management

- Other Applications

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Industry Vertical

- BFSI

- Healthcare and Life Sciences

- IT and Telecommunications

- Manufacturing

- Government and Public Sector

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed CPPM product managers, PMO heads across North America, Europe, and Asia-Pacific, and cloud infrastructure consultants. These conversations verified adoption triggers, average seat prices, churn patterns, and regional budget seasonality, filling data gaps that public sources could not illuminate.

Desk Research

We began by mapping the vendor and demand landscape through freely available tier-1 sources such as US Bureau of Labor Statistics IT staffing series, Eurostat cloud adoption rates, OECD ICT spend data, and industry association white papers from PMI and the Cloud Native Computing Foundation. Company 10-Ks, product release notes, and investor presentations added pricing and user-base signals. Where deeper firmographics were vital, analysts tapped D&B Hoovers and Dow Jones Factiva for historic revenue splits.

Trade press portals, patent abstracts via Questel, and customs shipment hints for hardware-linked SaaS gateways helped us cross-check deployment footprints. The resources cited illustrate our approach; numerous additional references were consulted for validation and clarification.

Market-Sizing & Forecasting

A top-down build starts with worldwide enterprise software outlays, from which we carve the CPPM spend pool by applying tracked SaaS penetration, share-of-wallet, and hybrid-cloud uptake ratios. Supplier roll-ups, sampled average selling price times active seat estimates, and channel checks provide a selective bottom-up lens, allowing us to adjust totals when variance exceeds tolerance. Key model drivers include: 1) annual cloud IT spend per employee, 2) share of remote knowledge workers, 3) average CPPM license cost, 4) hybrid-cloud adoption rate, and 5) frequency of Agile program reviews. A multivariate regression projects each driver, and scenario analysis captures upside from AI-embedded modules. Any data void in the roll-ups is bridged with regional interpolation anchored to verified subscription counts.

Data Validation & Update Cycle

Outputs pass sequential variance reviews and anomaly flags before sign-off. Models are refreshed every twelve months; interim reruns trigger when material events, large vendor M&A or abrupt pricing reshuffles, shift market dynamics. A final analyst sweep ensures clients always receive the most current view.

Why Mordor's Cloud Project Portfolio Management Baseline Commands Reliability

Published CPPM figures can differ widely because firms choose distinct functional scopes, pricing assumptions, and refresh cadences.

Three recurring gap drivers stand out: some publishers fold broader work-management or PSA revenues into CPPM, others limit geography to North America, while a few rely on vendor revenue reporting instead of end-user spending, thereby embedding currency and accounting lags.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.65 B (2025) | Mordor Intelligence | - |

| USD 18.54 B (2025) | Global Consultancy A | Includes collaboration suites and PSA modules |

| USD 6.80 B (2024) | Research Publisher B | Counts only North American subscription spend |

| USD 9.45 B (2024) | Industry Journal C | Uses vendor revenue reports without currency realignment |

These contrasts show why decision-makers seeking a balanced, transparent baseline rely on Mordor Intelligence: our scope mirrors actual CPPM utility, our variables are traceable, and our annual update cadence keeps the numbers fresh and reproducible.

Key Questions Answered in the Report

What is the current value of the cloud project portfolio management market?

The market is valued at USD 13.28 billion in 2026 and is expected to reach USD 25.53 billion by 2031.

Which deployment model is growing fastest?

Hybrid cloud deployments post the quickest rise with a 15.05% CAGR due to their balance of data control and cloud scalability.

Why are SMEs adopting these platforms rapidly?

Subscription pricing, quick onboarding, and pre-built templates eliminate the infrastructure and expertise barriers that once limited SME access.

How does AI improve project health monitoring?

AI engines parse historical data and real-time signals to assign risk scores, predict schedule slips, and recommend corrective staffing actions.

What restrains broader adoption in regulated industries?

Heightened security and privacy requirements plus data-sovereignty rules compel cautious, often hybrid, deployment strategies.

Who are the leading vendors in this space?

Microsoft, Oracle, SAP, Atlassian, Smartsheet, and monday.com lead, with newcomers specializing in AI-driven features and industry-specific compliance modules.

Page last updated on: