India Data Center Processor Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.27 Billion |

| Market Size (2026) | USD 7.19 Billion |

| Market Size (2031) | USD 33.97 Billion |

| Growth Rate (2026 - 2031) | 36.42% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Data Center Processor Market Analysis by Mordor Intelligence

The India data center processor market size is expected to grow from USD 5.27 billion in 2025 to USD 7.19 billion in 2026 and is forecast to reach USD 33.97 billion by 2031 at 36.42% CAGR over 2026-2031. Intense investment in 5G infrastructure, data-localization mandates, and the government’s USD 10 billion semiconductor mission are the primary forces lifting demand for advanced server-class silicon. Accelerated roll-outs of edge computing nodes, the drive for indigenous chip manufacturing, and the rapid scale-up of hyperscale cloud regions add fresh capacity faster than any other major digital economy. Processor vendors are localizing assembly and test operations to mitigate export-control risks, while liquid-cooling solutions are moving from pilot to mainstream adoption to handle AI rack densities. Competitive dynamics are further reshaped by custom silicon projects and RISC-V design activity backed by public incentives.

Key Report Takeaways

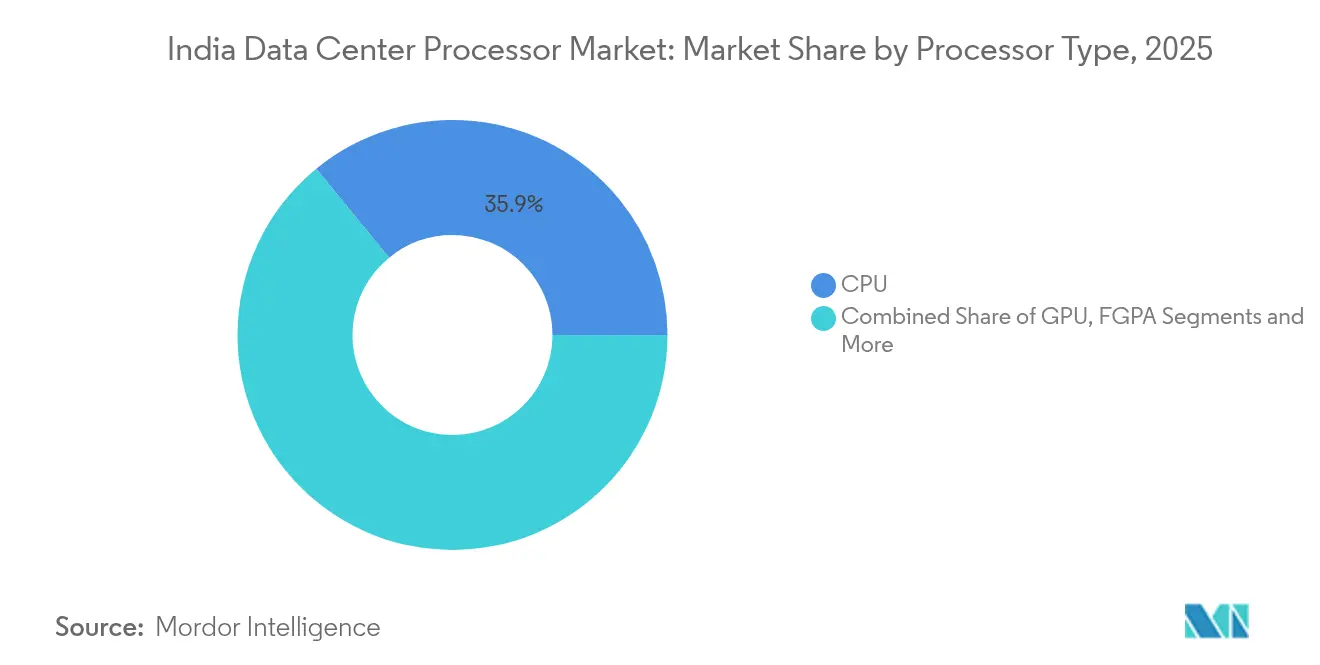

- By processor type, CPU devices held 35.92% of the India data center processor market share in 2025, whereas AI accelerators are projected to expand at a 37.12% CAGR through 2031.

- By application, AI/ML training & inference accounted for a 31.55% share of the India data center processor market size in 2025, while advanced data analytics is expected to progress at a 36.63% CAGR to 2031.

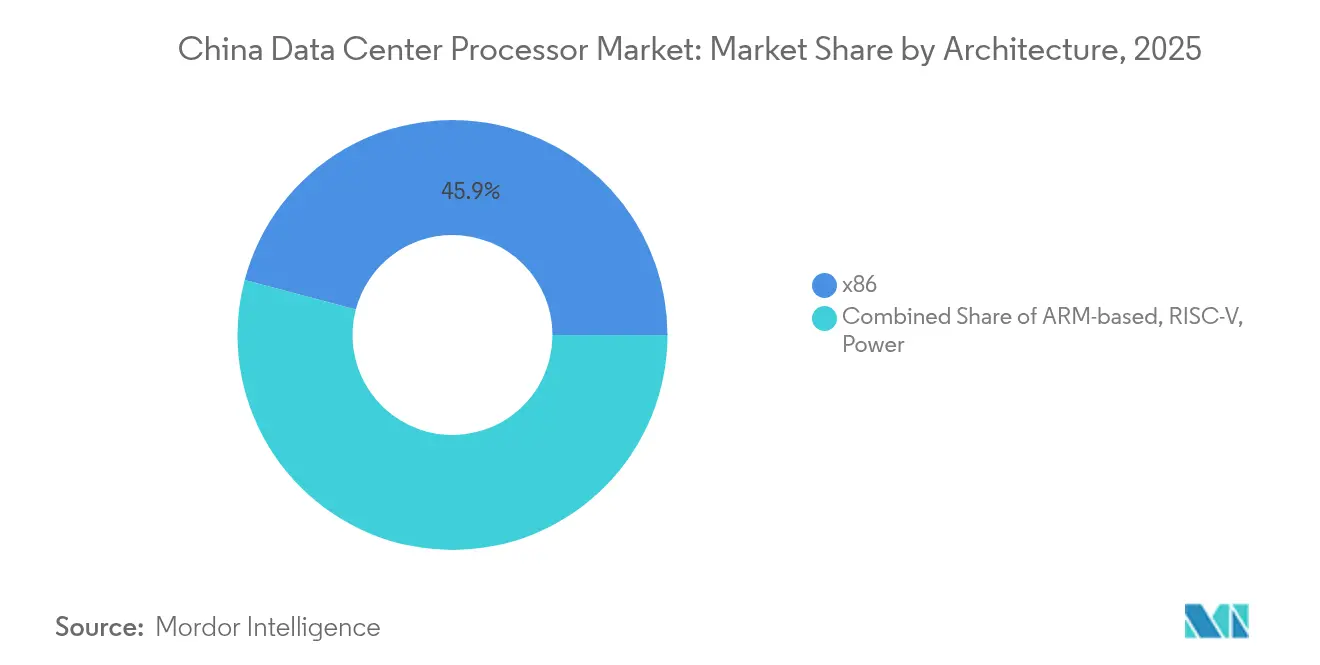

- By architecture, x86 chips led with 45.88% revenue share in 2025; RISC-V is the fastest-growing segment at a 38.07% CAGR.

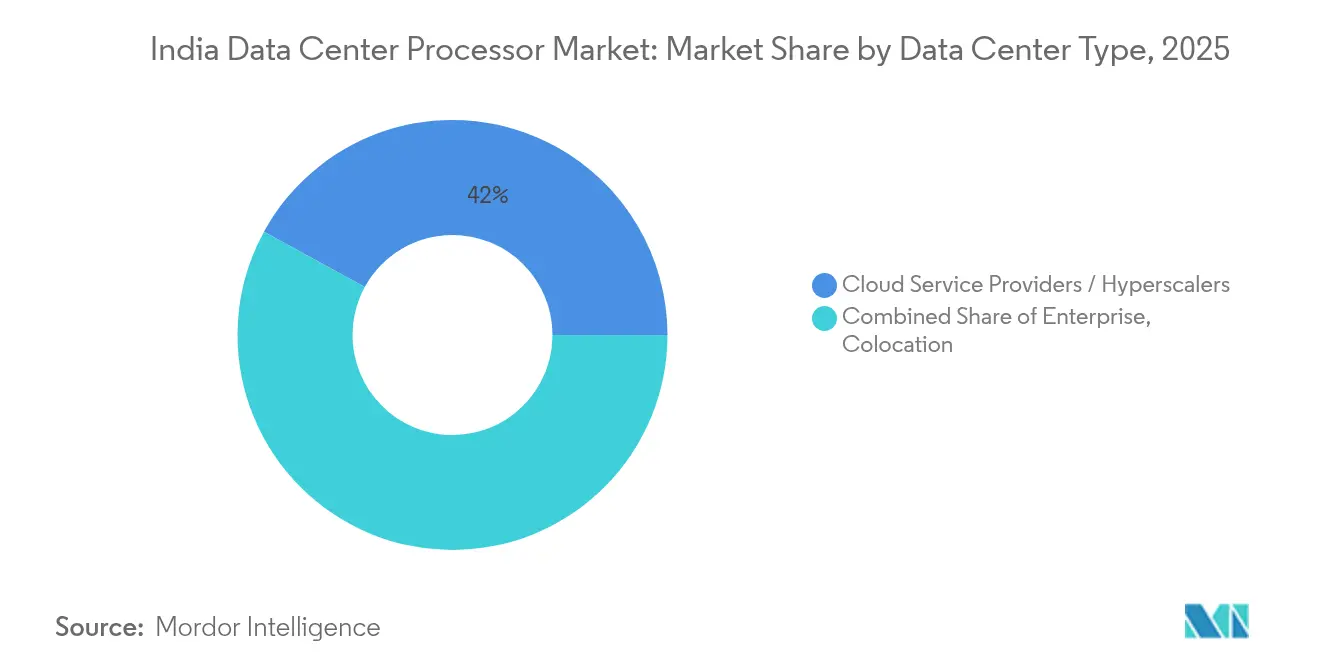

- By data-center type, cloud service providers commanded 42.02% of deployments in 2025, whereas colocation capacity is advancing at a 36.94% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Understanding the full system requires moving beyond India boundaries into a wider international view. Mordor Intelligence captures the global data center processor market scope in its worldwide coverage.

India Data Center Processor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in investments for 5G/6G roll-out catalyzing new data-center builds | +8.5% | National, with early gains in Mumbai, Delhi-NCR, Bangalore | Medium term (2-4 years) |

| Government "Digital India" & connectivity programs expanding compute demand | +7.2% | National, with spillover to tier-2 cities | Long term (≥ 4 years) |

| Hyperscale cloud expansion and rising public-cloud spend within India | +6.8% | Mumbai, Chennai, Bangalore core markets | Short term (≤ 2 years) |

| Data-localization mandates (RBI, DPDP Act) pushing in-country processing | +5.9% | National, particularly BFSI and healthcare sectors | Medium term (2-4 years) |

| PLI-scheme & India Semiconductor Mission lowering TCO for local server-class chips | +4.3% | National, with manufacturing hubs in Gujarat, Karnataka | Long term (≥ 4 years) |

| Rise of home-grown RISC-V / custom AI accelerators optimizing regional workloads | +3.8% | Bangalore, Hyderabad, Pune technology corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Investments for 5G/6G Roll-Out Catalyzing New Data-Center Builds

Reliance Jio’s plan for a 1 GW renewable-powered facility in Jamnagar exemplifies how telecom carriers converge network and compute estate. Edge nodes built to support ultra-low-latency 5G services now require specialized AI accelerators for real-time network optimization, driving incremental silicon demand. Government allocation of USD 1.2 billion under the IndiaAI Mission amplifies infrastructure funding. Operators such as Nxtra Data are adopting liquid immersion cooling to keep racks operating reliably at 50 °C ambient temperatures.

Government “Digital India” & Connectivity Programs Expanding Compute Demand

Central incentives worth INR 12,000 crore for new data centers, combined with legislation that mandates local processing of critical personal data, underpin a sustained pipeline of server installations. [1]Nasscom ,"Nasscom GenAI Foundry Cohort 2: Accelerating India’s GenAI Innovation Ecosystem", nasscom.comState-level policies in Tamil Nadu, Karnataka, and Telangana add land and power subsidies, accelerating regional capacity build-outs. The National Stock Exchange’s ability to process 19.71 billion trades in a single day demonstrates the compute scale now routine for India’s digital economy. Government-to-citizen service portals extend processor footprints into STPI-operated Tier III sites across tier-2 cities

Hyperscale Cloud Expansion and Rising Public-Cloud Spend Within India

AWS’s USD 12.7 billion commitment and Google’s multi-region builds intensify demand for custom silicon tailored to cloud workloads. Marvell’s 6.4 Tbps SiPho engine allows XPUs to attach directly to optics, improving latency and power metrics in hyperscale fabrics. With public-cloud revenue slated to rise from USD 6.5 billion in 2023 to USD 25.5 billion by 2028, cloud operators will keep driving the India data center processor market capacity at double-digit growth

Data-Localization Mandates (RBI, DPDP Act) Pushing In-Country Processing

Banks and global tech firms must deploy domestic compute clusters to comply with RBI and DPDP rules. YES Bank’s Cloudera hybrid analytics platform and Axis Bank’s personalization engine both rely on in-country neural networks to meet strict latency and sovereignty thresholds.[2]Cloudera Inc., “YES Bank Hybrid Analytics Platform Case Study,” cloudera.com Alibaba’s additional cloud region in Mumbai typifies the infrastructure replication compelled by India-specific data rules

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate power & cooling infrastructure outside top metros | -4.2% | Tier-2 and Tier-3 cities nationwide | Short term (≤ 2 years) |

| High capex for leading-edge processors and advanced packaging | -3.8% | National, particularly affecting SME data center operators | Medium term (2-4 years) |

| Heavy reliance on imported components amid export-control risks | -3.1% | National, with supply chain vulnerabilities | Short term (≤ 2 years) |

| Limited renewable-energy supply increasing carbon-compliance costs | -2.7% | National, with acute shortages in industrial corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inadequate Power & Cooling Infrastructure Outside Top Metros

Meeting the projected demand of 40-45 TWh by 2030 requires USD 280 billion in new generation assets, yet secondary markets still grapple with grid bottlenecks. AI racks above 250 kW force operators to invest in liquid cooling or risk derated densities, flexpowermodules.com. Waterless cooling pilots, such as the Mysore site, illustrate emerging engineering responses to scarce resources.

High Capex for Leading-Edge Processors and Advanced Packaging

Supply constraints lengthen delivery of critical components to 70 weeks, prompting operators to over-order and inflating working capital. The x86 Ecosystem Advisory Group formed by Intel and AMD aims to streamline software porting and manage BOM cost escalation.[3]AMD Corporate Blog, “Jio Platforms, AMD Bring Open Telecom AI,” amd.com Production Linked Incentive (PLI) support offsets part of the capex burden, but a full local supply chain will take years to mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processor Type: AI Accelerators Drive Next-Generation Workloads

CPU devices still hold 35.92% of 2025 deployments, underpinning database and ERP workloads that anchor many enterprise stacks. AI accelerators, however, are expanding at a 37.12% CAGR, pushed by hyperscalers standardizing on GPU or ASIC clusters for model training, and by telecom carriers embedding AI in network cores. The India data center processor market size for AI accelerators is on track to triple between 2026 and 2031, powered by indigenous projects such as Krutrim’s ARM¬-based chip aimed at local language models. GPU clusters from NVIDIA continue to dominate turn-key AI infrastructure, aided by partnerships with Reliance and Tata Communications.

FPGA deployments, while niche, enable ultra-low-latency analytics for equities trading. RISC-V AI accelerators such as SiFive’s P870-D, scalable up to 256 cores, underline an open-architecture path toward lower royalty outlays.

By Application: Advanced Analytics Accelerates Enterprise Transformation

AI/ML training & inference continues to capture 31.55% India data center processor market share in 2025, but advanced data analytics is the fastest-moving slice at a 36.63% CAGR. Banks use neural engines to personalize deposit and lending offers in real time, while manufacturers deploy predictive analytics at the edge to reduce downtime. The India data center processor market size for advanced analytics is forecast to exceed USD 10.43 billion by 2031, mirroring the crescendo of structured and unstructured data streams in the economy. High-performance computing clusters are growing in universities, and security-centric workloads gain heft as cyber threats intensify.

Edge AI use cases—from smart cameras in healthcare to anomaly detection on factory floors—demand low-power processors with on-chip encryption. Cisco’s Nexus 7000 consolidation at Kotak Mahindra Bank demonstrates the migration to high-bandwidth fabrics that sustain both analytics and compliance reporting. Active-active hospital data centers built on Huawei infrastructure show healthcare’s pivot toward zero-downtime compute

By Architecture: RISC-V Emerges as a Disruptive Alternative

x86 devices maintain 45.88% share today as legacy compatibility keeps them entrenched in enterprise back-ends, yet RISC-V chips are surging at a 38.07% CAGR. The open ISA trims licensing cost and lets silicon teams customize instruction sets for AI or storage offload.. ARM maintains momentum in cloud and edge servers where power efficiency trumps raw clocks, while POWER architecture retains a presence in select HPC labs.

NVIDIA, Qualcomm, Google, and Samsung co-develop RISC-V IP, signaling mainstream traction. Tenstorrent’s tie-ups with Indian startups accelerate ecosystem tooling, crucial for production deployments.

By Data Center Type: Colocation Facilities Expand Rapidly

Cloud service providers own 42.02% of installed footprints, but colocation racks are rising fast at 36.94% CAGR as enterprises opt for capex-light expansions. The India data center processor market size associated with colocation sites is expected to surpass USD 12.17 billion by 2031. Hybrid strategies blend on-prem nodes for compliance workloads with public-cloud regions for burst capacity. Secondary cities see the sharpest colocation uptake; Pi Datacenters expects available MW capacity outside tier-1 metros to triple within five years.

Geography Analysis

Mumbai, Delhi-NCR, and Chennai account for about major of national capacity owing to dense fiber routes, reliable power, and proximity to financial hubs. These metros continue to attract flagship hyperscale builds, yet rising land costs and sustainability targets push new investors toward adjacent regions.

Tier-2 cities such as Pune, Ahmedabad, and Kochi are emerging nodes for distributed compute. Lower land pricing and improving power reliability draw edge deployment budgets, complementing forthcoming 5G roll-outs. Data Center Dynamics reports that compute providers view these locations as optimal for latency-sensitive IoT use cases, accelerating the geographic spread of processor demand. NASSCOM estimates global edge revenue is growing 54% annually, feeding local silicon consumption for video analytics, AR/VR, and smart-mobility platforms

Mordor Intelligence examines the data center processor market across diverse other regional markets as well, including Asia, while also offering granular country-level perspectives for Japan, South Korea, Saudi Arabia, United States, Canada, Mexico, China, and Netherlands and more.

Competitive Landscape

The India data center processor market features moderate fragmentation. No vendor controls more than half of shipments, giving rise to multifaceted rivalry across x86, ARM, RISC-V, and ASIC segments. Intel and AMD remain incumbents, yet ARM-based Graviton-like designs from hyperscalers dilute x86 wallet-share. NVIDIA wields leadership in AI accelerators and has forged broad alliances with Reliance and Tata Group that bundle silicon, software, and training programs.

Custom silicon momentum is visible in Qualcomm’s renewed CPU initiative, headed by Intel’s former Xeon architect, aimed at energy-efficient servers with confidential computing features. Domestic firms such as InCore Semiconductors and C-DAC/MosChip are leveraging PLI incentives to co-design RISC-V and ARM server processors on advanced TSMC nodes. Marvell differentiates through co-packaged optics and custom HBM stacks that deliver superior performance per watt for hyperscale AI clusters.

India Data Center Processor Industry Leaders

-

Intel Corporation

-

Advanced Micro Devices Inc.

-

NVIDIA Corporation

-

Ampere Computing LLC

-

Arm Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Jio Platforms and AMD, Cisco, Nokia unveiled an Open Telecom AI Platform to create self-optimizing networks.

- March 2025: Texas Instruments introduced the TPS1685 48 V eFuse and GaN power stages exceeding 98% efficiency for data-center rails.

- March 2025: Tata Electronics allied with Himax and PSMC to boost India-made display and ultralow-power AI components.

- January 2025: Reliance began constructing a 1 GW AI-driven data center in Jamnagar using NVIDIA Blackwell processors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the India data center processor market as the yearly spend, in US dollars, on central processing units, graphics processing units, field-programmable gate arrays, and purpose-built AI or network accelerators first installed in enterprise, colocation, and hyperscale facilities inside India. Chips based on x86, Arm, RISC-V, and other architectures that power compute, training, inference, analytics, and security workloads are all in scope.

Scope Exclusion: Processors embedded in edge gateways, telecom base-band systems, personal computers, or consumer devices are excluded.

Segmentation Overview

-

By Processor Type

- GPU

- CPU

- FPGA

- AI Accelerator/ASIC

-

By Application

- Advanced Data Analytics

- AI/ML Training and Inference

- High-Performance Computing

- Security and Encryption

- Network Functions Virtualisation

- Others

-

By Architecture

- x86

- ARM-based

- RISC-V

- Power

-

By Data Center Type

- Enterprise

- Colocation

- Cloud Service Providers / Hyperscalers

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed Bengaluru chip design engineers, procurement heads at Mumbai colocation firms, and cloud architects serving Delhi NCR. They then ran short surveys with OEM channel partners. The dialogues clarified processor mix shifts, attainable price points, and likely adoption timing for new process nodes.

Desk Research

We began with structured desk work that combined Directorate General of Foreign Trade import ledgers, MeitY digital-infrastructure dashboards, Reserve Bank capital-goods data, TRAI subscriber statistics, and National Supercomputing Mission releases to size installed compute and shipment flows. Public filings and investor decks, accessed through D&B Hoovers and Dow Jones Factiva, revealed segment revenues and average selling prices. Specialist bodies such as the India Electronics and Semiconductor Association, WSTS, and IMTMA supplied terminology and production insights. This set is illustrative; many additional secondary references informed validation and clarification.

Market-Sizing & Forecasting

We rebuilt the 2024 baseline through a top-down reconstruction of processor import values and domestic assembly, aligned with data-center build capacity and average processor counts per rack. Selected bottom-up checks using sampled vendor shipments and channel estimates tempered the totals. Key inputs include hyperscaler capex announcements, GPU attach rates per AI rack, core-per-socket progression, node price-erosion curves, semiconductor duty rebates, and the government's plan to procure 10,000 GPUs under the IndiaAI mission. A multivariate regression with these variables projects demand through 2030, and outliers are re-benchmarked before finalization.

Data Validation & Update Cycle

Every interim result passes variance screening against independent KPIs and a senior analyst review before sign-off. Reports refresh once a year, with mid-cycle updates when material policy, price, or supply events occur, so clients receive the freshest calibrated view.

Why Mordor's India Data Center Processor Baseline Stands Firm

Published estimates often diverge because each publisher picks different chip sets, currency bases, and refresh cadences. According to Mordor Intelligence, anchoring on in-country first deployment, rather than shipment origin, is the single biggest driver of size differences.

Differences widen when others cover CPUs only, apply global average prices, or freeze exchange rates. Our model captures the rapid swing toward AI accelerators, updates local ASPs each quarter, and refreshes annually, while some sources depend on one-off surveys.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.27 B (2025) | Mordor Intelligence | - |

| USD 0.60 B (2024) | Regional Consultancy A | excludes GPUs and AI ASICs, values imports at customs rates |

| USD 0.38 B (2024) | Trade Journal B | covers CPUs only, omits domestic assembly output |

| USD 1.68 B (2025) | Global Consultancy C | starts with full server hardware then applies a fixed processor share |

In sum, the disciplined scope selection, variable tracking, and annual refresh cadence adopted by Mordor Intelligence provide a balanced, reproducible baseline that decision-makers can rely on for capital planning and strategy alignment.

Key Questions Answered in the Report

What is the projected size of the India data center processor market in 2031?

It is forecast to reach USD 33.97 billion by 2031, growing at a 36.42% CAGR.

Why is RISC-V important for India?

Open-source RISC-V lets local firms avoid high licensing fees and tailor chips for regional workloads; government-backed projects like Shakti accelerate ecosystem maturity.

Which processor category is expanding the fastest?

AI accelerators/ASICs are forecast to grow at a 37.12% CAGR through 2031, outpacing all other categories.

How do data-localization laws affect processor demand?

RBI and DPDP rules force organizations to process sensitive data on Indian soil, driving new domestic server deployments and lifting processor shipments.

Page last updated on: