South America Cloud Computing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

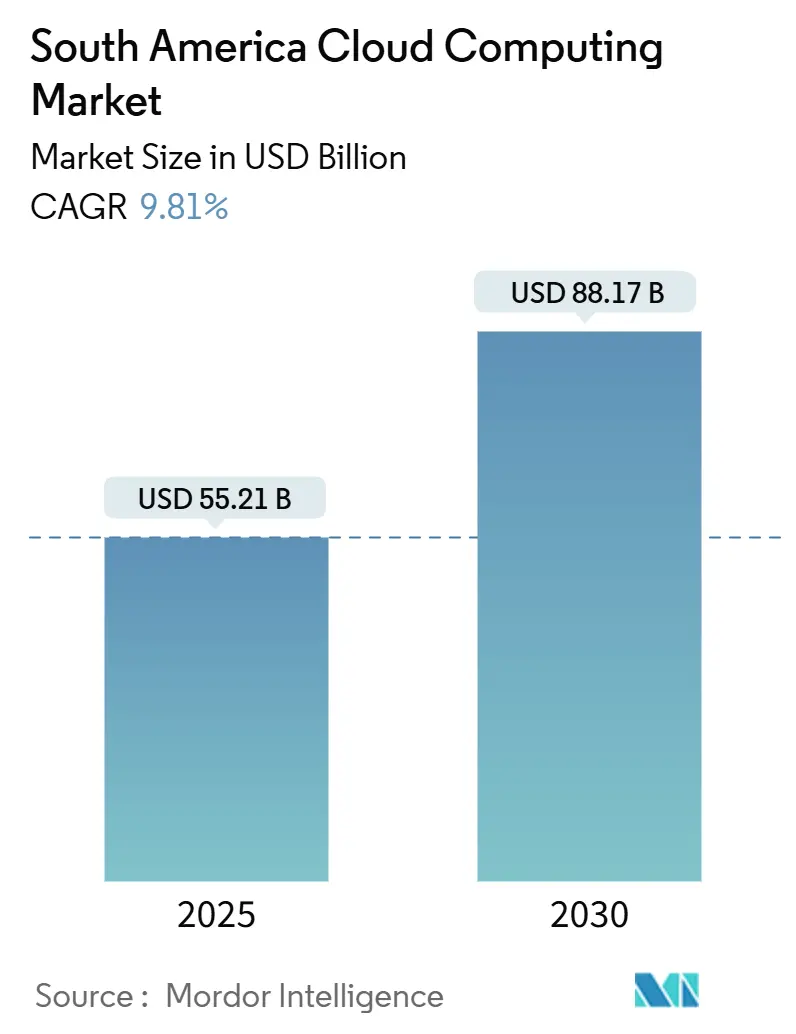

| Market Size (2025) | USD 55.21 Billion |

| Market Size (2030) | USD 88.17 Billion |

| Growth Rate (2025 - 2030) | 9.81% CAGR |

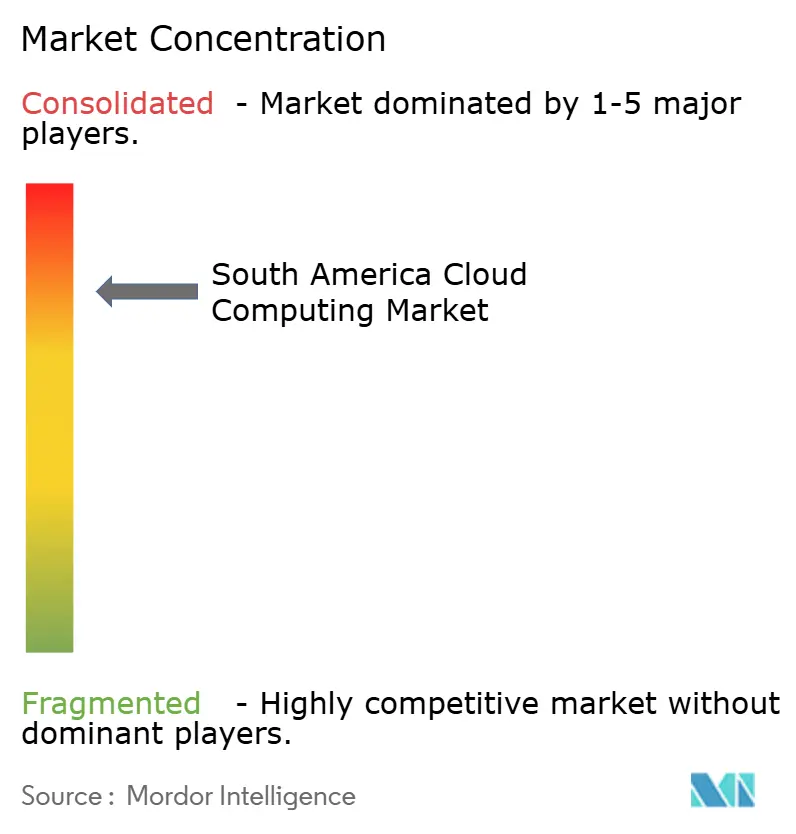

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Cloud Computing Market Analysis by Mordor Intelligence

The South America cloud computing market size stood at USD 55.21 billion in 2025 and is forecast to reach USD 88.17 billion by 2030, reflecting a 9.81% CAGR over the period. The uptrend is driven by record-high capital expenditures for hyperscale data centers, pro-innovation government policies, and widespread enterprise digitalization, which now prioritizes AI-ready cloud platforms over lift-and-shift migrations. Intensifying competition among Amazon Web Services, Microsoft Azure, and Google Cloud has accelerated regional infrastructure rollouts, while sovereign-cloud directives are encouraging hybrid architectures that balance residency compliance with global scalability. Fiber-to-the-home and 5G backhaul investments are removing latency bottlenecks for real-time analytics, and dedicated credit lines are enabling small and medium enterprises (SMEs) to finance cloud adoption at preferential rates. Together, these forces are expanding the addressable base and underpinning sustained demand for cloud platforms across all verticals in the South America cloud computing market.

Key Report Takeaways

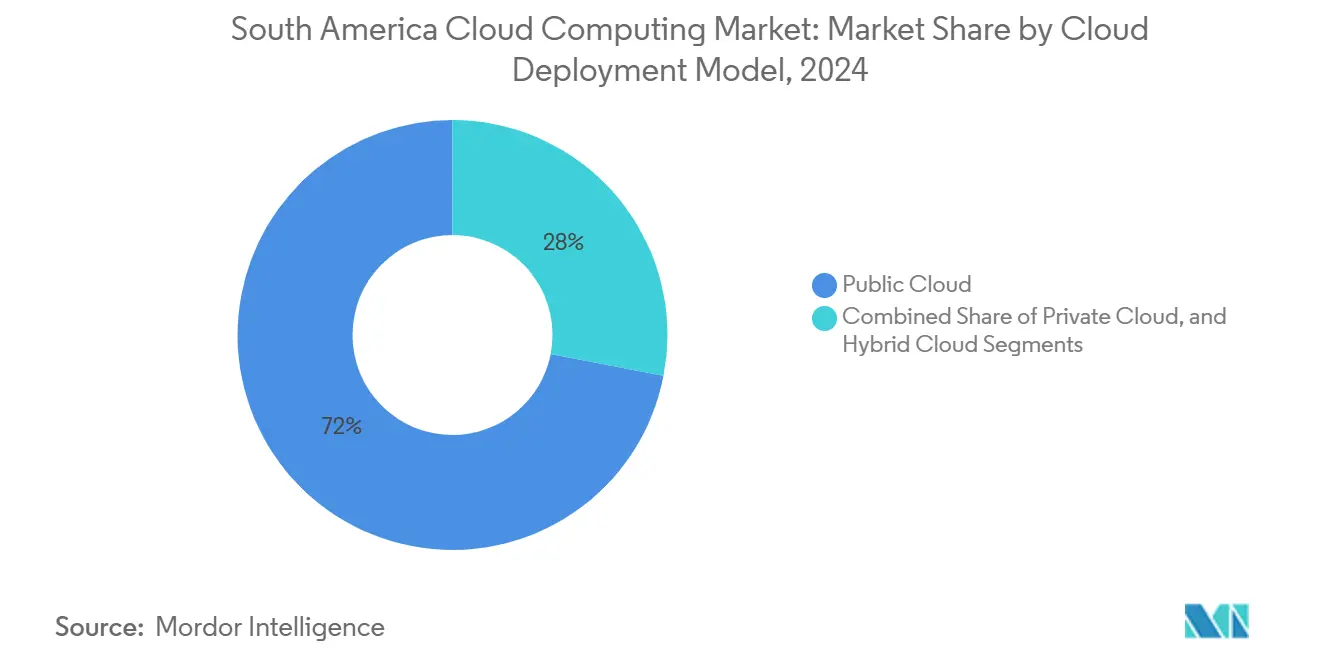

- By cloud deployment model, the public cloud led with 71.97% revenue share of the South America cloud computing market in 2024, while the hybrid cloud is projected to advance at a 11.04% CAGR to 2030.

- By service model, Software-as-a-Service (SaaS) commanded 53.19% share of the South America cloud computing market size in 2024; Platform-as-a-Service (PaaS) is expected to expand at a 10.35% CAGR through 2030.

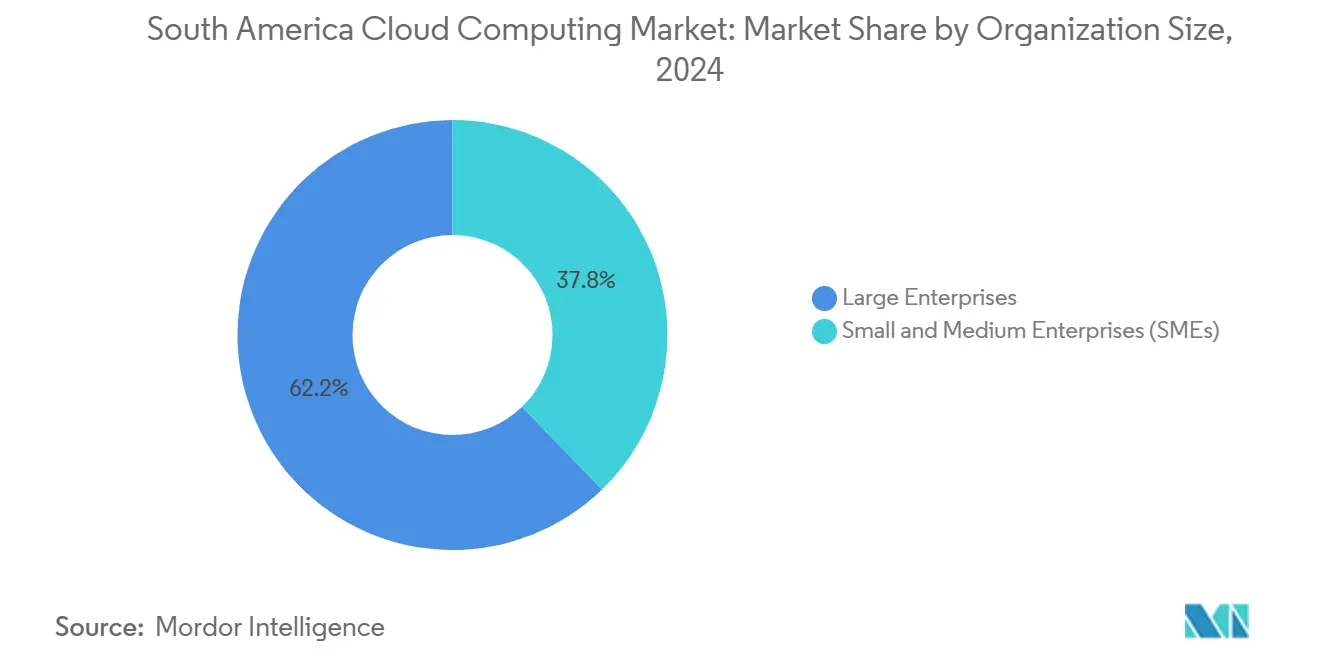

- By organization size, large enterprises accounted for a 62.24% share of the South America cloud computing market in 2024, but SMEs are forecast to grow at a 10.07% CAGR between 2025 and 2030.

- By end-user industry, banking, financial services, and insurance captured 21.13% of the South America cloud computing market share in 2024, whereas retail is poised for a 10.46% CAGR to 2030.

- By geography, Brazil held 42.39% of South America cloud computing market share in 2024; Argentina is predicted to post the fastest 10.71% CAGR over the forecast horizon.

Viewed independently, South america offers depth on regionally local conditions but not full coverage of the overall global system. Mordor Intelligence's coverage on the cloud computing market brings the wider geographic picture into focus.

South America Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated digital transformation initiatives across enterprises | +2.8% | Brazil, Colombia, Argentina, Chile | Medium term (2-4 years) |

| Favorable government policies promoting cloud adoption | +2.1% | Brazil, Argentina, Chile | Long term (≥ 4 years) |

| Rising penetration of high-speed internet connectivity | +1.9% | Brazil Northeast, Colombia, Argentina urban areas | Short term (≤ 2 years) |

| Increasing hybrid and multi-cloud deployment preference | +1.6% | Brazil and cross-border operations | Medium term (2-4 years) |

| Cost efficiency and operational flexibility benefits | +1.2% | SME-focused across region | Short term (≤ 2 years) |

| Expansion of regional data-center footprint by major providers | +1.5% | Chile, Brazil, Uruguay | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital Transformation Initiatives Across Enterprises

Enterprise strategies have evolved from basic workload migration to AI-infused business models, with 73% of South American organizations planning to operationalize AI within the next 12 months. AI workloads require 10-50 times more compute than traditional applications, prompting firms to reserve burst capacity on public clouds, even when data lakes remain on-premises. Brazil’s industrial digitalization roadmap aims to increase smart-manufacturing penetration to 50% of factories by 2033, thereby catalyzing sustained cloud spending. [1]Agência Gov, “Investimentos de R$ 186,6 bilhões impulsionam transformação digital da indústria brasileira,” agenciagov.ebc.com.br

Microsoft’s USD 2.7 billion program in Brazil earmarks AI skilling for 5 million citizens, signaling that hyperscalers view workforce enablement as a demand generator rather than a philanthropic endeavor. As procurement focuses on platform depth, competitive differentiation shifts from raw infrastructure pricing to integrated AI, data, and developer tooling.

Favorable Government Policies Promoting Cloud Adoption

Policy blueprints increasingly reconcile sovereignty with competitiveness. Brazil’s OSIC 15/2024 establishes unified cloud-security rules for federal workloads and clarifies the conditions for cross-border data processing. Argentina’s free-trade zones for data centers offer tax relief that improves project return profiles, while a World Bank-endorsed digital marketplace template standardizes public-sector buying criteria. [2]World Bank, “Transforming government through smart procurement,” worldbank.orgEcuador’s national broadband-AI policy shows smaller economies can replicate the model to channel cloud investment into inclusive growth. [3]BNamericas, “Ecuador's new digital transformation policy,” bnamericas.com Clearer rules lower compliance risk and lengthen payback horizons, thereby reinforcing the growth path of the South America cloud computing market.

Rising Penetration of High-Speed Internet Connectivity

Fiber backbones and 5G densification are closing the urban-rural latency gap. Brisanet has rolled out 61,000 km of FTTH in Brazil’s Northeast and tied 5G holdings to distributed micro-data centers that localize traffic for edge workloads. SBA Communications’ USD 975 million tower buy from Millicom adds 7,000 sites, enhancing last-mile coverage critical to cloud-enabled IoT. V.tal’s USD 1 billion capex plan deepens hyperscale interconnect routes, ensuring that enterprise clouds achieve sub-10 ms performance thresholds essential for predictive analytics workloads. These upgrades directly translate into increased usage intensity, thereby enlarging the addressable base of the South America cloud computing market.

Increasing Hybrid and Multi-Cloud Deployment Preference

Regulatory heterogeneity and vendor lock-in concerns are driving architectures toward hybrid solutions. The Microsoft and Oracle Database@Azure rollout in Brazil South enables regulated industries to maintain their Oracle databases while leveraging Azure analytics within the same facility. Google Cloud’s air-gapped Distributed Cloud option provides Brazilian customers with sovereign AI capability where all training data stays onshore. Financial institutions also cite business-continuity hedging as a reason to avoid single-provider dependence. As hybrid patterns mature, orchestration platforms become pivotal, expanding demand beyond raw compute toward governance and observability tooling within the South America cloud computing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data privacy and security concerns | -1.8% | Brazil LGPD, Argentina sovereignty mandates | Medium term (2-4 years) |

| Limited availability of cloud-skilled workforce | -1.4% | Regional secondary cities, AI and security roles | Long term (≥ 4 years) |

| Latency challenges in rural areas | -0.9% | Brazil interior, Colombia countryside | Short term (≤ 2 years) |

| Complex compliance across multiple jurisdictions | -0.7% | Multinational enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Data Privacy and Security Concerns

Brazil’s LGPD, combined with Banco Central rules for financial data, obliges providers to offer granular visibility into tenancy isolation and encryption processes. Similar but non-identical statutes in Argentina and Chile complicate multiregion architectures. Google Cloud addresses the issue with residency options for Gemini services that never leave Brazilian soil, but such dedicated builds inflate cost structures . Enterprises still cite API vulnerabilities and insider threats as material barriers, slowing migrations in regulated verticals and tempering overall South America cloud computing market expansion.

Limited Availability of Cloud-Skilled Workforce

It is estimated that South America’s digital-skills gap will leave more than 2 million roles unfilled by 2025, throttling project velocity, Microsoft and Google have each launched multi-year skilling programs, yet talent remains concentrated in metropolitan hubs, leaving provincial SMEs with limited access to certified professionals. The shortage is acute for AI engineering and cloud-security architects, where compensation now rivals North American benchmarks. Without accelerated upskilling, deployment timelines will lengthen, dampening the South America cloud computing market near-term uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cloud Deployment Model: Hybrid Strategies Drive Enterprise Modernization

Hybrid systems are reshaping workload placement. Public cloud retains 71.97% share of the South America cloud computing market, chiefly for elastic front-end and analytics workloads. Yet the hybrid segment is forecast to clock an 11.04% CAGR, reflecting regulatory pressures on data custody and the need for low-latency edge processing. Financial institutions and multinationals deploy sensitive data in private instances while bursting to public resources for AI model training, ensuring compliance without sacrificing agility.

Sovereign cloud offerings advance this trend. Google’s air-gapped Distributed Cloud and Microsoft’s local-zone buildouts demonstrate vendor willingness to deliver region-specific services that comply with localization statutes. Such moves broaden the South America cloud computing market size by encouraging previously hesitant sectors like public administration and healthcare to initiate phased migrations.

By Service Model: Platform Services Accelerate Development Velocity

Software-as-a-Service continues to command 53.19% of spending, favored for its quick productivity returns. Platform-as-a-Service, however, is the momentum leader at a 10.35% CAGR as developers pivot to containerized microservices, low-code workbenches, and integrated MLOps frameworks. [4]Globant, “Form 20-F 2024,” globant.comEnterprises want abstracted runtime environments that cut provisioning cycles from weeks to minutes while embedding security guardrails.

PaaS uptake directly increases the size of the South America cloud computing market for AI accelerators and event-driven services. Google’s Vertex AI launch in São Paulo and AWS’s Bedrock generative-AI venue illustrate hyperscale race dynamics. For SMEs, low-code studios enable digital offerings without the need for large in-house engineering teams, thereby democratizing innovation across the region.

By Organization Size: SME Growth Outpaces Enterprise Adoption

Large organizations contributed 62.24% of 2024 revenues, leveraging multi-cloud blueprints to harmonize regional compliance with global service catalogs. SMEs, aided by Brazil’s BNDES credit line that starts at 6.13% for northern regions, will outgrow incumbents at 10.07% CAGR.

As pay-as-you-grow pricing converges with on-premises depreciation curves, the South America cloud computing market share held by SMEs is set to expand. Workforce initiatives such as AWS and Escola da Nuvem’s program to certify 6,000 professionals by 2025 directly target this cohort, bridging adoption hurdles that historically limited cloud penetration outside tier-one cities.

By End-User Industry: Financial Services Lead While Retail Accelerates

Financial-services institutions retained 21.13% share of 2024 revenues, deploying cloud for core-banking modernization, risk analytics and instant-payment rails such as PIX. Retail, buoyed by e-commerce and omnichannel personalization, will log the segment’s fastest 10.46% CAGR, driving demand for recommendation engines and inventory visibility at scale.

Healthcare’s telemedicine surge and manufacturing’s Industry 4.0 projects add further lift to the South America cloud computing market. Government workloads, exemplified by Brazil’s Gov.br serving 155 million registered users, highlight the scale benefits of public-sector adoption and set precedents for neighboring administrations.

Geography Analysis

Brazil, capturing 42.39% of 2024 spending, anchors the regional ecosystem. PIX processes roughly USD 300 billion monthly, underscoring transaction volumes that require resilient cloud back ends. A combined BRL 186.6 billion (USD 36.7 billion) public-private digitalization plan and hyperscale buildouts such as Google’s Trillium TPU deployment ensure Brazil remains the principal hub for AI workloads. Microsoft’s USD 2.7 billion investment further amplifies the talent pipeline and data-center density.

Argentina is the fastest riser at a 10.71% CAGR. Customs-free data-center zones coupled with cybersecurity reforms are enticing providers, while the country’s software-services export base seeds a sophisticated buyer community. Chile’s selection for AWS’s USD 4 billion region and Uruguay’s hosting of Google’s USD 850 million campus illustrate how smaller nations leverage political stability and green-energy profiles to attract hyperscale capital.

Rest-of-South-America markets such as Colombia, Peru and Ecuador benefit from submarine-cable landings that cut inter-POP latency. Equinix’s USD 130 million Santiago expansion and SBA Communications’ tower strategy improve last-mile performance, enabling real-time use cases in sectors like agritech and mining. As connectivity equalizes, regional customers gain the confidence to commit mission-critical workloads to cloud, broadening the South America cloud computing market penetration.

Mordor Intelligence evaluates the cloud computing market across all key regional markets, including North America, Europe, and Asia, with deeper country-level insights covering Brazil, Japan, China, India, South Korea, and Canada.

Competitive Landscape

Market concentration is moderate. AWS, Microsoft, and Google collectively dominate core IaaS and PaaS revenue, but they are increasingly cooperating, as seen in Microsoft and Oracle’s Database@Azure alignment, to offer enterprises integrated stacks rather than forcing lock-in. Regional integrators like Globant capitalize on multi-cloud certifications, capturing 22.1% of South American income from transformation projects that stitch vendor services into tailored roadmaps.

Telecommunications carriers are pivoting to “techco” roles. Brisanet’s 5G plus edge-data-center rollout targets underserved Northeast Brazil, while SBA Communications’ tower acquisitions position it as a backbone player. Sovereign-cloud variants differentiate providers by embedding residency and compliance assurances, and those investing in local upskilling gain procurement preference in public-sector tenders.

White-space opportunities persist in AI-optimized colocation, edge-analytics and vertical-specific SaaS. Private-equity entrants, such as Patria’s USD 1 billion data-center platform, confirm that infrastructure remains a compelling asset class, suggesting that new challengers will enter even as incumbents deepen their footprints. Altogether, competitive dynamics favor ecosystem partnerships that deliver interoperability, trust and local relevance across the South America cloud computing market.

South America Cloud Computing Industry Leaders

Microsoft Corporation

Huawei Technologies Co., Ltd.

Google LLC (Alphabet Inc.)

IBM Corporation

Amazon Web Services (AWS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Patria Investimentos launched a hyperscale data-center platform backed by USD 1 billion.

- May 2025: Amazon Web Services committed USD 4 billion to its first Chile region, operational in H2 2026.

- April 2025: World Economic Forum spotlighted Brazil’s digital public infrastructure progress.

- March 2025: Oracle and Microsoft extended Database@Azure to Brazil South.

South America Cloud Computing Market Report Scope

Cloud computing offers a vast range of computing services over the Internet. These services include servers, storage, databases, networking, software, analytics, and intelligence. Key advantages of cloud computing are accelerated innovation, flexible resource allocation, and economies of scale. Customers generally pay only for the services they use. This approach reduces operational costs, enhances infrastructure efficiency, and enables scaling to meet evolving business demands.

The South America Cloud Computing Market Report is Segmented by Cloud Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Service Model (IaaS, Paas, and SaaS), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (Manufacturing, Education, Retail, Transportation and Logistics, Healthcare, BFSI, Telecom and IT, Government and Public Sector, and Other End-User Industries), and Country (Brazil, Argentina, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| Education |

| Retail |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Other End-User Industries |

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Cloud Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| By Organization Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-user Industry | Manufacturing |

| Education | |

| Retail | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Other End-User Industries | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

How fast is cloud spending growing in South America?

The South America cloud computing market is projected to expand at a 9.81% CAGR from USD 55.21 billion in 2025 to USD 88.17 billion by 2030.

Which country accounts for the largest share of regional cloud revenue?

Brazil captured 42.39% of 2024 spending, underpinned by large-scale public-sector digital services and concentrated hyperscale data-center investments.

Why are hybrid architectures gaining ground?

Enterprises need to keep sensitive data on-premises for compliance while accessing elastic public-cloud capacity for AI and analytics, pushing hybrid deployments to an 11.04% forecast CAGR.

Which service model is growing the fastest?

Platform-as-a-Service is expected to grow at 10.35% CAGR as firms adopt low-code tools and integrated MLOps to speed application delivery.

What is the biggest challenge facing cloud adoption?

A shortage of cloud-skilled professionals, especially in AI engineering and security architecture, is slowing project timelines across secondary cities.

Which vertical shows the strongest future upside?

Retail is forecast to post a 10.46% CAGR through 2030, driven by e-commerce growth and demand for personalized customer experiences powered by cloud analytics.

Page last updated on: