Germany Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

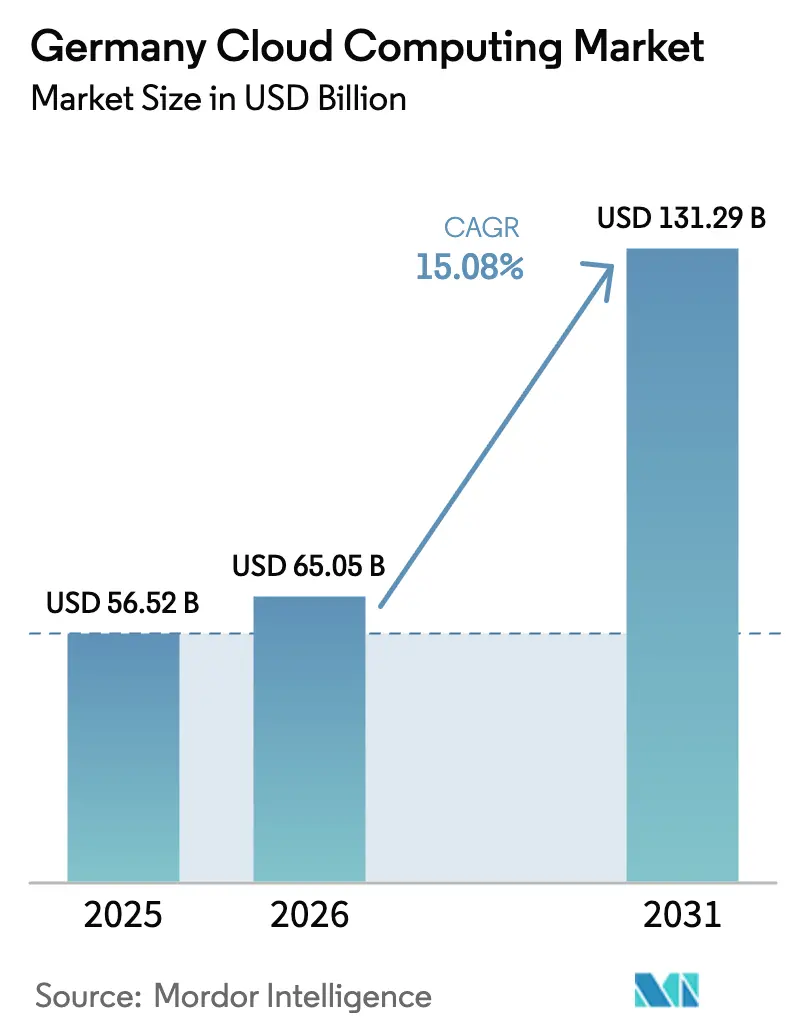

| Base Year Market Size (2025) | USD 56.52 Billion |

| Market Size (2026) | USD 65.05 Billion |

| Market Size (2031) | USD 131.29 Billion |

| Growth Rate (2026 - 2031) | 15.08% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Cloud Computing Market Analysis by Mordor Intelligence

The Germany cloud computing market size is expected to grow from USD 56.52 billion in 2025 to USD 65.05 billion in 2026 and is forecast to reach USD 131.29 billion by 2031 at 15.08% CAGR over 2026-2031. A wave of SAP S/4HANA migrations, due before the 2027 cutoff, is prompting thousands of firms to overhaul infrastructure and accelerate cloud spending.[1]ASUG News + Views, “Q4 and FY 2024: SAP Surges as Cloud Revenue Soars,” asug.com The pursuit of digital sovereignty is reshaping vendor selection as German buyers insist on in-country hosting, encryption-key custody and BSI C5 compliance, pushing hyperscalers into multibillion-euro capacity expansions.[2]Germany Trade & Invest, “Microsoft to Invest Billions in Germany,” gtai.de Hybrid architectures are rising fastest because they keep sensitive data in local facilities while sending GPU-hungry AI workloads to regional hyperscale zones. Elevated electricity prices are raising the relative attractiveness of shared platforms over self-managed data centers, further tilting demand toward the Germany cloud computing market.[3]SMARD, “Entwicklung der Industriestrompreise,” smard.de

Key Report Takeaways

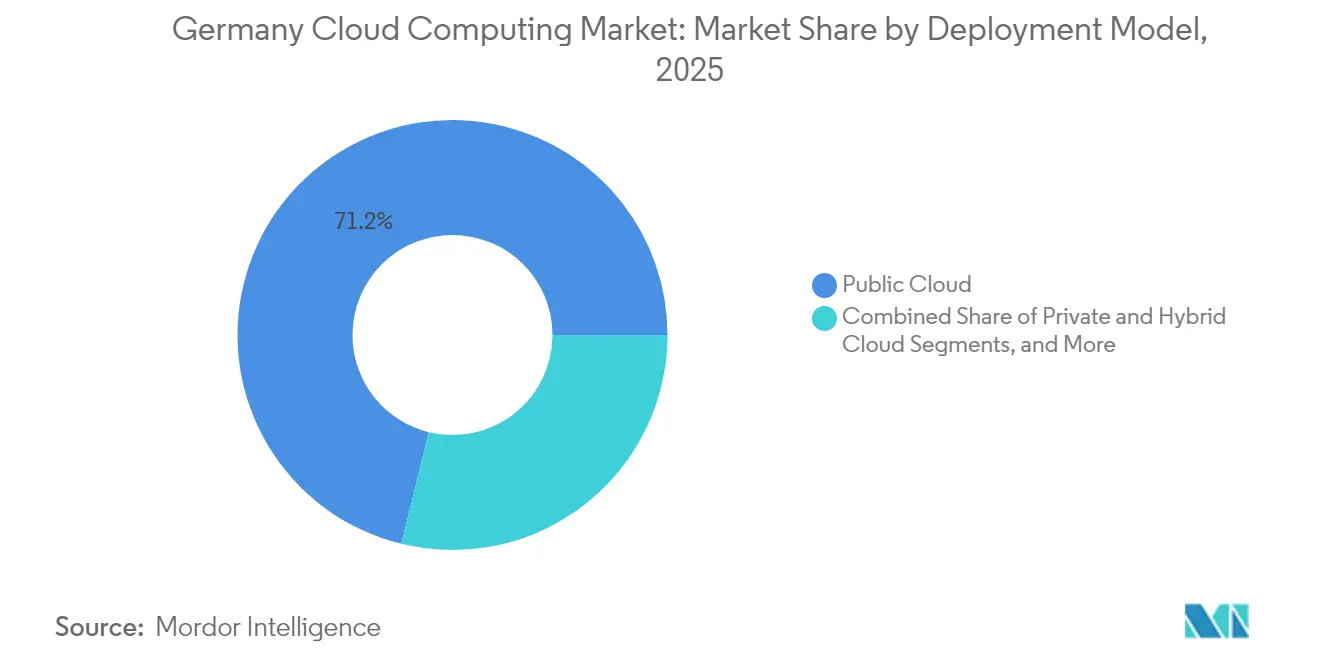

- By deployment model, public cloud held 71.18% of the Germany cloud computing market share in 2025, whereas hybrid cloud is forecast to grow at an 17.60% CAGR through 2031.

- By service model, Software-as-a-Service captured 47.88% share in 2025; Platform-as-a-Service is projected to expand at a 16.74% CAGR to 2031.

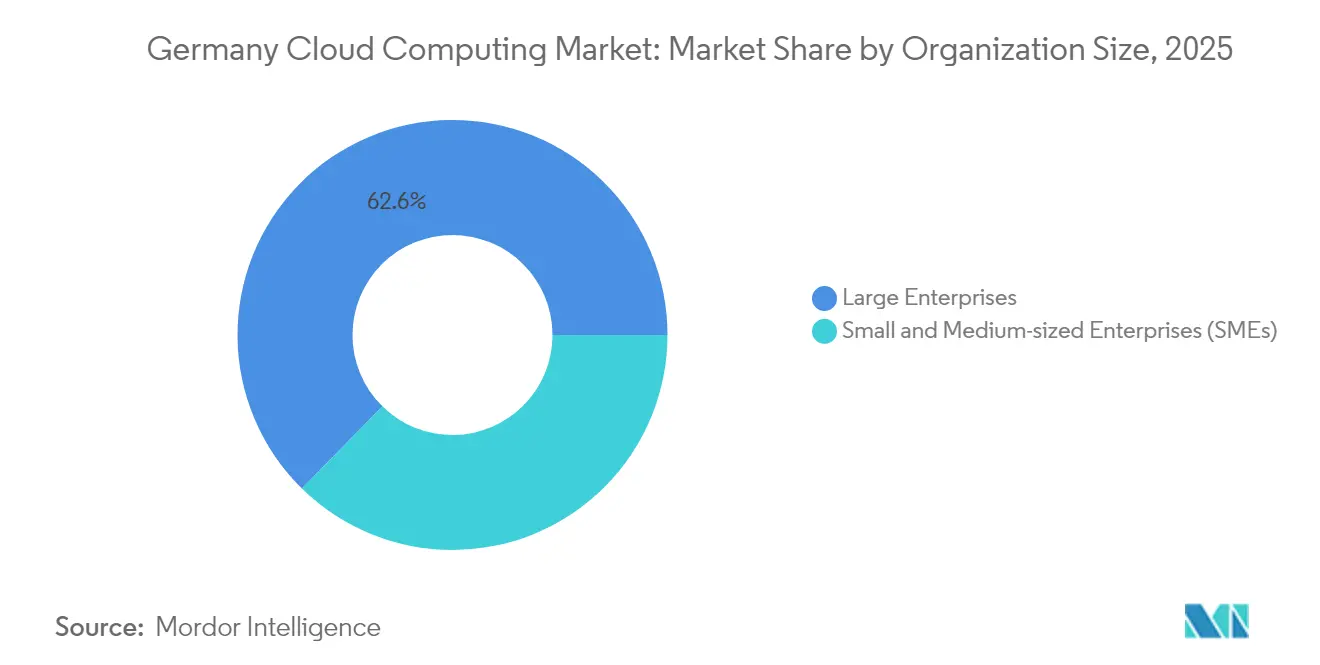

- By organization size, large enterprises controlled 62.65% of spending in 2025, while small and medium enterprises are expected to advance at a 19.01% CAGR over the forecast window.

- By end-user industry, information technology and telecom led with 21.22% share in 2025; healthcare is set for the fastest climb at an 17.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

National developments in Germany connect differently with activity unfolding across other parts of the world. In the global cloud computing market coverage, Mordor Intelligence integrates these into a single analytical framework.

Germany Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide digital-transformation initiatives | +3.20% | National focus in NRW and Baden-Württemberg | Medium term (2-4 years) |

| Enterprise multi-cloud and hybrid strategies | +2.80% | National, early adopters in Frankfurt finance hub | Medium term (2-4 years) |

| AI and ML workload boom | +4.10% | Clusters in Munich, Frankfurt, Berlin | Short term (≤2 years) |

| SAP S/4HANA migration deadline | +2.70% | Highest impact in manufacturing regions | Short term (≤2 years) |

| Government subsidies for sustainable green data centers | +1.90% | National, strongest in renewable-energy regions | Long term (≥4 years) |

| Automotive OEM shift to software-defined vehicle cloud back-ends | +1.40% | Stuttgart, Munich, Wolfsburg automotive clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nationwide Digital-Transformation Initiatives Drive Public-Sector Demand

Federal programs that digitize citizen services are propelling sovereign-ready offerings. Government agencies increasingly specify in-country hosting and client-side encryption as baseline requirements, shifting demand toward providers able to certify BSI C5 controls.[4]Microsoft News Center, “Sovereign Cloud Platform for German Administration,” microsoft.com Funding lines attached to these programs reduce the budget risk of cloud migration, enabling ministries to modernize legacy platforms in a single procurement cycle. Hyperscalers have responded with dedicated sovereign regions and partnership models that ring-fence operational access, helping the Germany cloud computing market penetrate sensitive workloads once reserved for on-premises environments. The resulting pipeline supports a durable revenue runway over the medium term, especially for local operators that already meet stringent residency mandates.

Enterprise Adoption of Multi-Cloud and Hybrid Strategies Reshapes Vendor Relationships

Fifty-five percent of large German firms use hybrid deployments and another 52% pursue cloud-first policies, signalling a decisive shift toward multi-vendor portfolios. Buyers distribute workloads to avoid lock-in and to align each application with the optimal compliance or latency profile. Partnerships such as Deutsche Telekom’s SAP2SKY initiative with Google Cloud highlight a pattern where national carriers front-end hyperscale capacity while preserving local data processing. Demand for cloud-management platforms and integration services is climbing as IT teams juggle credential brokering, observability and spend control across two or more providers. This development broadens the Germany cloud computing market by creating service opportunities beyond raw compute and storage.

AI and ML Workload Boom Demands GPU-Rich Infrastructure

Roughly half of SAP’s Q4 2024 cloud contracts contained explicit AI components, underscoring surging demand for graphics-accelerated clusters. Enterprises need high-density GPU instances for generative-AI training, natural-language inference and computer-vision pipelines. Hyperscale’s are racing to open AI-centric regions, while domestic providers invest in liquid cooling and renewable-powered facilities to contain energy draw. Manufacturers integrate edge servers that perform inference inside factory walls yet rely on cloud back ends for model training and lifecycle management, reinforcing hybrid adoption. The AI wave therefore multiplies infrastructure spending and raises the technical entry bar, consolidating growth into providers that can finance next-generation data centers within the Germany cloud computing market.

SAP S/4HANA Migration Deadline Spurs Cloud Moves

The 2027 end-of-maintenance date forces enterprises to pick between costly on-premises upgrades or a direct shift to managed cloud ERP. German manufacturers and Mittelstand suppliers increasingly opt for RISE or GROW packages that include hyperscale hosting, accelerating bookings for infrastructure, middleware and services. Migration projects trigger broader workload refactoring, often rolling in analytics, security and collaboration suites. Consulting firms and managed-service providers field specialized squads to hit tight conversion windows, tightening the labour market and raising billable rates. The race to compliance feeds sustained double-digit expansion in the Germany cloud computing market through the short term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity costs | -2.10% | National, acute in industrial states | Short term (≤2 years) |

| Shortage of cloud-native talent | -1.80% | Berlin, Munich, Frankfurt tech corridors | Medium term (2-4 years) |

| Stringent German data-residency rules (BSI C5, Schrems II) | -1.30% | National, varying by industry | Long term (≥4 years) |

| Legacy ISV on-prem licensing lock-ins in Mittelstand | -0.90% | Traditional manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Electricity Costs Tighten Data-Center Economics

Industrial power prices averaged 16.77 cents per kWh in 2024, among the highest in Europe, squeezing margins for compute-intensive facilities. GPU racks driving AI workflows consume up to five times more energy than traditional servers, magnifying sensitivity to tariff swings. Large operators hedge via long-term renewable contracts, whereas smaller colocation players face profit compression that could prompt consolidation. Enterprises compare rising utility bills for self-hosted hardware against predictable cloud consumption fees, tilting budgets toward outsourced capacity within the Germany cloud computing market. Over the short term, power-price volatility remains a headwind on in-country expansion plans, particularly for newcomers lacking scale.

Shortage of Cloud-Native Talent Constrains Implementation Velocity

Germany recorded 149,000 unfilled IT roles in 2024, with vacancy spans averaging 7.7 months. Skills gaps are most acute in Kubernetes administration, DevOps automation and AI-platform engineering, prolonging internal project timelines and increasing the appeal of managed services. Mid-sized firms often outsource build-and-run responsibilities to bridge staffing deficits, widening addressable revenues for consultancies yet dragging on adoption of complex hybrid patterns. Wage inflation for cloud architects raises total cost of ownership calculations, partially offsetting price advantages of hyperscale resources. Unless training pipelines expand, the talent bottleneck could temper the otherwise robust trajectory of the Germany cloud computing market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Setups Emerge as the Compliance Sweet Spot

Hybrid architectures contributed a modest slice in 2025 but are projected to climb at an 17.60% CAGR, outpacing every other deployment option in the Germany cloud computing market. Although public platforms still represented 71.18% of spending, many regulated enterprises now keep production data in certified German facilities and move bursty analytics to hyperscaler zones. This pattern balances residency mandates with elastic capacity and underpins the Germany cloud computing market size outlook.

Private clouds remain relevant for niche workloads in banking and defense that demand absolute isolation and bespoke cryptography. Automotive OEMs design software-defined vehicles that stream telemetry into cloud back ends while caching safety-critical logic at the edge, reinforcing hybrid value propositions. Energy-efficiency legislation prompts data-center operators to market waste-heat recovery and renewable sourcing, boosting the attractiveness of off-premises options. As SAP projects transition from piloting to cut-over, enterprises frequently adopt a phased hybrid model before decommissioning legacy hardware, extending demand well beyond initial migration years.

By Service Model: PaaS Adoption Tracks AI and Edge Requirements

Software-as-a-Service captured 47.88% of revenue in 2025, but Platform-as-a-Service is growing fastest at a 16.74% CAGR as developers need container orchestration, event streaming and GPU microservices that reduce build time. The Germany cloud computing market size for PaaS is rising as manufacturers deploy predictive-maintenance pipelines that ingest shop-floor sensor data and dispatch insights to maintenance crews. Telcos apply PaaS-based AI agents to autonomously fine-tune radio networks, proving the model’s value in high-availability settings.

Infrastructure-as-a-Service remains foundational but is increasingly consumed through managed-service overlays that package security, observability and cost governance. SaaS momentum continues in ERP, CRM and human-capital suites as subscription models free capital for innovation. Vendors now bundle business applications with pre-configured AI co-pilots, anchoring customers to higher-margin tiers. Interoperability between SaaS, PaaS and IaaS layers surfaces as a procurement criterion, favouring platforms that unify billing and access controls across the Germany cloud computing market.

By Organization Size: SMEs Push Cloud-First Adoption Curves

Large enterprises wielded 62.65% of 2025 spending, yet SMEs will post a 19.01% CAGR through 2031, adding vibrancy to the Germany cloud computing market. Smaller firms typically sidestep mainframe and proprietary-hardware baggage, enabling faster pivot to serverless and containerized stacks. SaaS suites give these companies immediate access to enterprise-grade features without capital intensity, accelerating competitiveness against larger rivals.

Conversely, big corporations navigate multi-year programs that untangle sprawling legacy estates while preserving service continuity. Many extend on-premises support contracts even as they adopt cloud for new workloads, creating dual-stack complexity. System integrators carve lucrative niches by orchestrating these hybrid landscapes, while hyperscalers court SMEs with simplified onboarding and localized support bundles. As both cohorts expand usage, the Germany cloud computing market benefits from a blended pipeline of quick-win deals and transformational mega-projects.

By End-User Industry: Healthcare Leads Growth While IT & Telecom Dominates Spend

Information technology and telecom commanded 21.22% of 2025 revenue, reflecting the sector’s twin role as supplier and early adopter in the Germany cloud computing industry. Providers roll out network-automation and customer-experience platforms atop their own clouds, feeding a self-reinforcing spend loop. Healthcare, meanwhile, will record an 17.98% CAGR, fuelled by telemedicine scaling, electronic-health-record mandates and AI-assisted diagnostics.

Automotive clusters in Bavaria and Baden-Württemberg leverage cloud to coordinate over-the-air updates and digital-twin simulations, intertwining operational technology with IT systems. Manufacturing plants deploy edge gateways linked to centralized analytics for real-time quality control, deepening industrial-sector reliance on the Germany cloud computing market. Financial institutions adopt cloud risk-management engines yet maintain stringent encryption-key custody, demonstrating that compliance and modernization can coexist. Public-sector workloads migrate under sovereign frameworks, while universities provision burst compute for research projects, rounding out a broad vertical mix.

Geography Analysis

Frankfurt Rhine-Main anchors Germany’s data-center capacity thanks to its dominant internet exchange, accounting for more than a third of current megawatt inventory. Bavaria’s tech ecosystem, clustered around Munich, champions automotive and semiconductor cloud use, spurring specialized GPU deployments. North Rhine-Westphalia hosts dense manufacturing that drives demand for hybrid setups linking factory floors to regional availability zones. Baden-Württemberg’s engineering heritage fosters early adoption of digital-twin and edge-AI projects that depend on low-latency connectivity.

Data-center capacity is projected to climb from 2,700 MW in 2024 to 4,800 MW by decade end, propelled by EUR-scale announcements from Amazon Web Services, Microsoft and Alphabet. Providers increasingly site facilities near renewable-energy corridors to comply with efficiency mandates and meet corporate sustainability pledges. 5G rollouts and campus networks enable distributed computing nodes, a shift that disperses workloads beyond Frankfurt into secondary metros. T-Systems’ EdgAir hubs exemplify these micro-regions that link field devices to central clouds with single-digit-millisecond latency.

Regional electricity-cost differentials influence site selection as operators weigh grid tariffs against fiber density and tax incentives. Emerging sovereign-cloud campuses in Berlin and Bonn serve federal agencies, anchoring demand in political centers. Collectively, these patterns establish a multi-cluster fabric that supports the diverse latency, compliance and resilience needs that underpin the Germany cloud computing market.

Mordor Intelligence's coverage of the cloud computing market extends across other regions including Europe, Asia, and South America, while country-specific intelligence is also available for Spain, France, India, Brazil, South Korea, and Nigeria, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The landscape shows moderate concentration, with U.S. hyperscalers leading but European challengers expanding fast. Amazon disclosed EUR 16.6 billion of German infrastructure commitments through 2030, underpinning network, security and renewable-energy projects. Microsoft pledged EUR 3.2 billion to double cloud capacity and stand-up AI-optimized regions tailored to sovereignty requirements, including key-custody models for public agencies. Google deepened its partnership with Deutsche Telekom, migrating the carrier’s SAP estate and co-developing data-ecosystem services that pre-integrate with Gemini generative models.

STACKIT and IONOS frame digital sovereignty as a premium feature, capitalizing on enterprises wary of extra-territorial access claims. STACKIT’s recruitment of Google Cloud’s former country manager signals intent to scale enterprise sales and AI services. Inquiries to European providers reportedly rose 250% during 2024 amid geopolitical uncertainty, indicating latent demand for non-U.S. alternatives. Edge-focused specialists such as German Edge Cloud cater to Industry 4.0 workloads that require latency below 10 milliseconds inside production halls, giving them a defensible niche.

Strategic alliances shape go-to-market differentiation. SAP’s GROW on AWS compresses ERP deployment timelines and bundles generative-AI extensions. T-Systems integrates sovereign Azure offerings with its managed-security stack to win federal workloads. Oracle pairs GPU clusters with AMD’s advanced nodes to court AI developers. Collectively, these maneuvers intensify competition and push all players to balance compliance, performance and cost within the Germany cloud computing market.

Germany Cloud Computing Industry Leaders

Alibaba Group Holding Limited

Amazon Web Services (AWS)

Google LLC

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Deutsche Telekom extended its Google Cloud alliance through 2030, migrating SAP workloads and launching an AI-driven One Data-Ecosystem platform.

- February 2025: Microsoft committed EUR 3.2 billion to expand AI capacity and train 1.2 million citizens, targeting North Rhine-Westphalia.

- January 2025: Friedhelm Loh Group merged subsidiaries under German Edge Cloud to deliver GAIA-X-compliant edge-cloud solutions.

- December 2024: SAP and Amazon Web Services launched “GROW with SAP on AWS” to accelerate Cloud ERP rollouts.

Germany Cloud Computing Market Report Scope

Cloud computing provides on-demand access to computer resources, particularly data storage and processing power, without requiring direct management by the user. Computing resources, including physical and virtual servers, data storage, networking capabilities, application development tools, software, and AI-powered analytics, are now accessible over the Internet with a pay-per-use pricing model.

The Report Covers Germany Cloud Computing Companies. The market is segmented by Type (Public Cloud, Private Cloud, Hybrid Cloud), Organization Type (SMEs, Large Enterprises), End-User Industries (Manufacturing, Education, Retail, Transportation, Logistics, Healthcare, BFSI, Telecom, and IT, Government, and Public Sector). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| Education |

| Retail |

| Transportation and Logistics |

| Healthcare |

| Banking, Financial Services and Insurance (BFSI) |

| Information Technology and Telecom |

| Government and Public Sector |

| Utilities |

| Media and Entertainment |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| By Organization Size | Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Industry | Manufacturing |

| Education | |

| Retail | |

| Transportation and Logistics | |

| Healthcare | |

| Banking, Financial Services and Insurance (BFSI) | |

| Information Technology and Telecom | |

| Government and Public Sector | |

| Utilities | |

| Media and Entertainment |

Key Questions Answered in the Report

How large is the Germany cloud computing market in 2026?

The Germany cloud computing market size is valued at USD 65.05 billion in 2026.

What is the expected growth rate for German cloud spending through 2031?

Aggregate spending is projected to rise at a 15.08% CAGR to USD 131.29 billion by 2031.

Which deployment model is expanding fastest among German enterprises?

Hybrid cloud leads, advancing at an 17.60% CAGR as companies blend data residency with scalable off-premises compute.

Why is healthcare adoption accelerating?

Telemedicine rollouts, electronic-health-record mandates and AI-enabled diagnostics push healthcare workloads to compliant clouds, driving an 17.98% CAGR.

How does the SAP S/4HANA deadline affect demand?

The 2027 cutoff forces firms to choose cloud-hosted ERP, creating a sizable migration wave that boosts infrastructure and services revenue.

What competitive advantage do sovereign-cloud providers claim?

They highlight BSI C5 certification, client-side encryption and in-country hosting, meeting stringent German data-sovereignty requirements.

Page last updated on: