Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

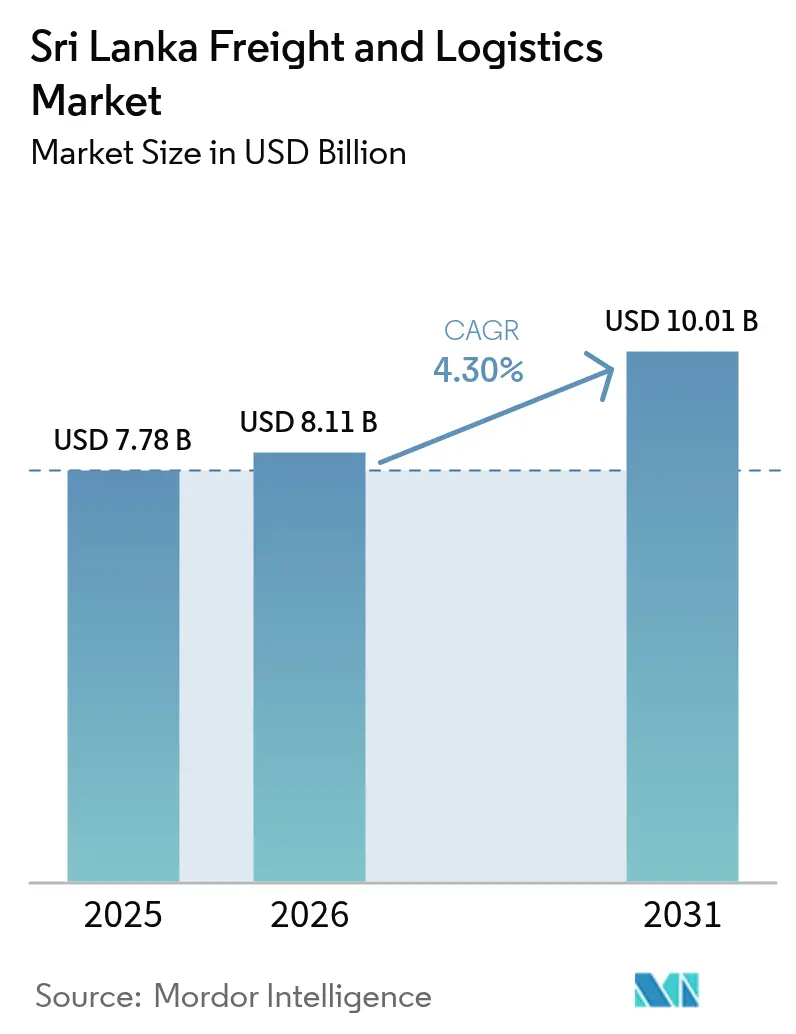

| Base Year Market Size (2025) | USD 7.78 Billion |

| Market Size (2026) | USD 8.11 Billion |

| Market Size (2031) | USD 10.01 Billion |

| Growth Rate (2026 - 2031) | 4.30% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sri Lanka Freight And Logistics Market Analysis by Mordor Intelligence

The Sri Lanka freight and logistics market size is expected to grow from USD 7.78 billion in 2025 to USD 8.11 billion in 2026 and is forecast to reach USD 10.01 billion by 2031 at 4.3% CAGR over 2026-2031. This trajectory underscores the pivotal role of the Sri Lanka freight and logistics market in the Indian Ocean’s maritime corridors as port expansions, integrated logistics parks, and end-to-end digital customs platforms raise operating efficiency and throughput. Modernization at Colombo and Hambantota, the move toward value-added warehousing, and a surge in cross-border e-commerce collectively reinforce revenue growth, while supportive trade agreements diversify shipment profiles and encourage new third-party logistics models. Strategically, operators that embrace data-driven route optimization, partner with integrated port-park clusters, and hedge against currency volatility are best positioned to capture incremental volumes and margin improvements.

Key Report Takeaways

- By logistics function, freight transport captured 64.12% of Sri Lanka's freight and logistics market share in 2025; courier, express, and parcel (CEP) services are forecast to expand at a 5.20% CAGR between 2026-2031.

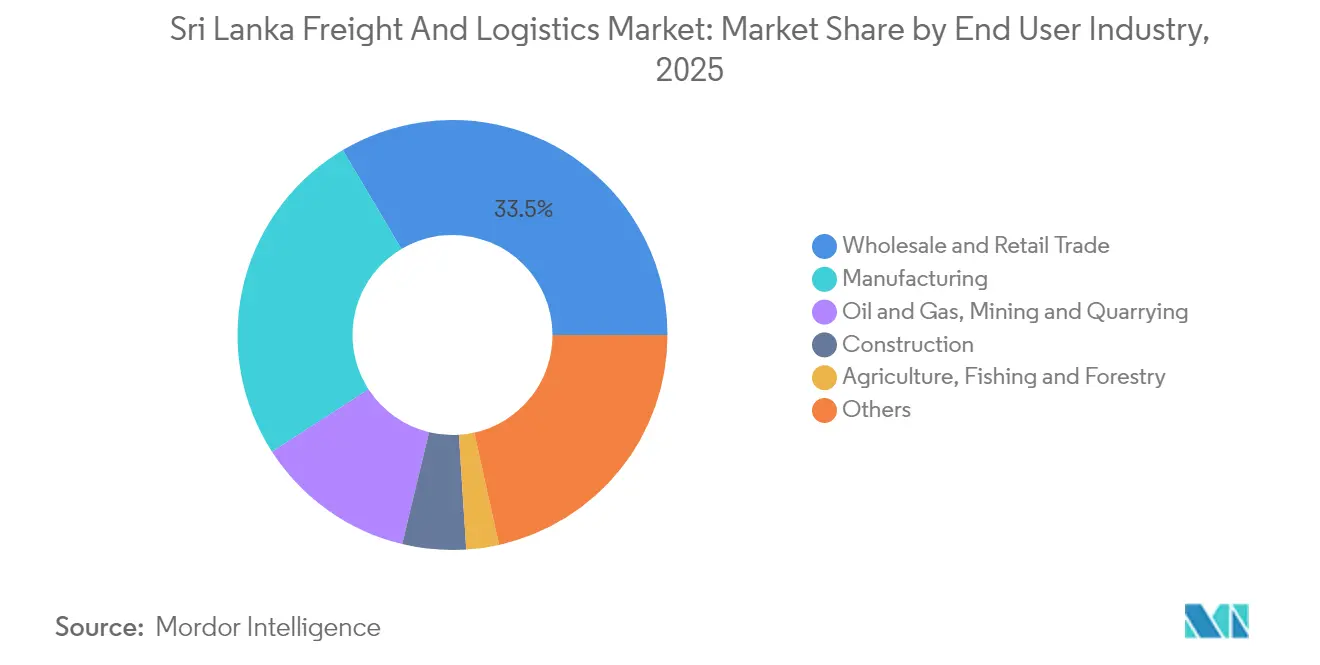

- By end user industry, wholesale and retail trade led with a 33.52% of the Sri Lanka freight and logistics market size in 2025, while manufacturing records the highest projected CAGR at 4.96% between 2026-2031.

- By CEP type, domestic parcels accounted for 62.48% revenue share in 2025, whereas international parcels are expected to grow at a 5.35% CAGR between 2026-2031.

- By freight forwarding mode, sea and inland waterways retained 50.22% of the revenue share in 2025, yet air freight forwarding is projected to grow at a 4.37% CAGR between 2026-2031.

- By freight transport mode, road freight transport represented 66.96% of revenue share in 2025, while air freight transport is expected to grow at a CAGR of 4.90% between 2026-2031.

- By warehousing and storage, non-temperature controlled facilities commanded 91.54% of the revenue size in 2025 and temperature controlled is projected to grow at 4.12% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sri Lanka Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of regional transshipment and hub port status boosts connectivity | +1.1% | Colombo and Hambantota | Medium term (2–4 years) |

| Growing investment in integrated logistics parks and inland container depots (ICDs) | +0.9% | Western Province and urban centers | Long term (≥ 4 years) |

| Rising international trade flows driving market demand | +1.0% | Major port cities and corridors | Short term (≤ 2 years) |

| Colombo Port City SEZ incentives attract strategic business investments | +0.7% | Western Province | Medium term (2–4 years) |

| Accelerated adoption of digital customs through ASYCUDA World | +0.6% | Nationwide | Short term (≤ 2 years) |

| Development of Palaly Airport multimodal transshipment corridor enhances connectivity | +0.5% | Northern Province | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Regional Transshipment and Hub Port Status Boosts Connectivity

Sri Lanka’s central location on East-West trade lanes positions the Sri Lanka freight and logistics market to absorb cargo diverted from congested regional hubs. The development of the Eastern Container Terminal and the USD 800 million Colombo West International Terminal adds 3.6 million TEU of annual capacity, enabling carriers to deploy larger vessels and cut turnaround times[1]“Eastern Container Terminal Development,” Sri Lanka Ports Authority, slpa.lk. Competitive feeder tariffs and synchronized hinterland connections bolster throughput, although maintaining low service charges remains essential vis-a-vis Singapore and Dubai. Hambantota complements Colombo by providing deep-draft alternatives for energy cargoes and vehicle transshipments, thereby broadening route flexibility and lowering congestion risk during peak seasons.

Growing Investment in Integrated Logistics Parks and Inland Container Depots (ICDs)

Integrated logistics parks that blend bonded warehousing, customs, distribution, and light processing are shifting revenue pools away from pure port handling toward bundled supply-chain solutions. Initiatives in Horana and Muthurajawela connect directly to expressways and rail spurs, reducing container dwell times and easing Colombo gate congestion. Operators exploit shared infrastructure, ro-ro ramps, value-added packaging lines, and 24/7 customs outposts to improve asset utilization and service differentiation. The chief hurdle remains high upfront capital outlays; nevertheless, PPP structures with 30-year concessions are unlocking foreign direct investment and stabilizing tariff trajectories for tenants.

Rising International Trade Flows Driving Market Demand

Total merchandise trade rebounded to USD 30.6 billion in 2024, lifting freight forwarding, customs brokerage, and multimodal demand. The Sri Lanka-Thailand Free Trade Agreement eliminates duties on 80% of tariff lines, catalyzing containerized flows of electronics, automotive parts, and processed foods[2]“Sri Lanka–Thailand FTA,” Ministry of Trade, trade.gov.lk. E-commerce marketplaces deepen parcel density, compelling CEP networks to deploy zonal sort centers and dynamic line-haul routing. To capitalize, forwarders digitalize booking and visibility platforms, which mitigates documentation errors and accelerates invoice cycles. The upside potential rests on synchronized capacity additions across roads, ICDs, and cold chain nodes to match rising TEU and parcel volumes.

Colombo Port City SEZ Incentives Attract Strategic Business Investments

Tax holidays, duty-free equipment imports, and single-window approvals inside the Port City SEZ attract regional head offices and value-added distribution centers. Logistics firms benefit from co-located grade-A warehouses linked to automated quay cranes and expressway exits, cutting total landed costs and enabling cross-docking within four hours of vessel discharge. Execution risks include shifting regulatory directives and the need for harmonized policy between onshore and SEZ jurisdictions to avoid duplicate compliance steps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High port and logistics service charges continue to challenge competitiveness | −1.0% | Colombo and major ports | Short term (≤ 2 years) |

| Currency depreciation and rising import costs impact margins | −0.8% | Nationwide | Short term (≤ 2 years) |

| Forex shortages hamper fleet maintenance and operations | −0.7% | Nationwide | Medium term (2–4 years) |

| Policy volatility creates uncertainty in terminal privatization | −0.6% | Major port facilities | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Port and Logistics Service Charges Continue to Challenge Competitiveness

Elevated terminal handling, storage, and ancillary tariffs erode cost competitiveness and divert relay cargo toward cheaper hubs. While new automation lowers per-box operating costs, recoveries are frequently passed to users through higher published tariffs, negating efficiency gains. Currency depreciation aggravates the issue because most fees are dollar-denominated. Without a calibrated tariff regime, volume growth may stall despite capacity expansions.

Currency Depreciation and Rising Import Costs Impact Margins

A weakening rupee inflates local currency prices for imported trucks, yard equipment, and fuel, compressing margins across the Sri Lanka freight and logistics industry. Smaller fleets that rely on short-term overdrafts confront a liquidity shock as debt service on USD loans escalates[3]“Exchange-Rate Policy 2024,” Central Bank of Sri Lanka, cbsl.gov.lk. Hedging options remain limited, prompting operators to prioritize preventive maintenance, retrofit older assets, and optimize route assignment to conserve cash.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Accelerates Trade Diversification

Wholesale and retail trade captured 33.52% of the Sri Lanka freight and logistics market share during 2025; whereas the manufacturing industry is forecast to progress at a 4.96% CAGR (2026-2031), supported by export-processing zones, electronics assembly, and apparel value-addition. This pace outstrips wholesale and retail trade, which, although still the largest, advances more modestly on maturing urban consumption. Oil & gas, mining, and quarrying are anchored in petroleum imports and mineral exports that require specialized handling. Construction activity hinges on port and highway projects that simultaneously raise logistics demand and improve network reach. Agriculture, fishing, and forestry contributed the least, with cold-chain uptake expanding on seafood exports. Collectively, these dynamics diversify revenue streams within the Sri Lanka freight and logistics market and limit overreliance on any single end-use cluster.

Further momentum arises from FDI-funded industrial parks that leverage tariff-free inputs under new FTAs. Multinational OEMs appoint local 3PLs for inbound raw-material consolidation, stitched apparel returns, and regional parts distribution, broadening contract durations. Service providers integrate quality inspection, JIT inventory feeds, and bonded consolidation into single invoices, expanding wallet share. E-commerce is also reshaping wholesale distribution, as omnichannel retailers outsource fulfillment and returns management, boosting nationwide LTL and last-mile volumes. Consequently, higher manufacturing activity multiplies cross-dock moves, pallet rentals and temperature-controlled transfers, underpinning resilient capex in warehouses and fleet renewals.

By Logistics Function: Freight Transport Dominates Traditional Corridors

The freight transport segment commands 64.12% of the revenue share in 2025 because transshipment volumes flow chiefly through trucking haulage, feeder shipping, and barge moves. Concurrently, courier, express, and parcel (CEP) is expected to grow at a 5.20% CAGR during 2026-2031, supported by digital retail momentum and SME exports. Freight forwarding sustains relevance by navigating complex rules-of-origin matrices and multi-port itineraries.

Stakeholders redouble focus on service bundling: transport providers add customs desks, while forwarders lease buffer warehouses, morphing into lead-logistics players. Warehouse capacity constraints spur mezzanine retrofits, automated vertical lifts, and satellite cross-docks to extend service footprints nearer consumption nodes. Integrated contracts that guarantee door-to-door lead times lure manufacturers seeking single-invoice solutions. As a result, the lines between traditional freight transport, forwarding, and value-added services blur, fostering scale advantages for omnichannel operators.

By Courier, Express, and Parcel (CEP): International Growth Accelerates

Domestic CEP accounted for 62.48% of revenue share in 2025, thanks to dense Colombo–Kandy–Galle urban triangles and same-day delivery pledges by marketplace platforms. International CEP, however, is expected to grow faster at a 5.35% CAGR (2026-2031) as Lankan consumers tap overseas sellers and cottage exporters fulfill micro-orders to diaspora markets. Firms deploy bonded bulk clearances where multiple low-value parcels ride a single airway bill, reducing per-unit brokerage fees.

Regulatory clarity around de minimis thresholds and digital customs fosters strides in cross-border flows. Service providers introduce pre-paid duty options and mobile tracking in Sinhala and Tamil, raising customer adoption. Yet the new 2025 VAT on selected e-commerce categories forces carriers to enhance classification accuracy. Those mastering automated HS-code allocation and API-based duty payments gain market share as parcel counts rise.

By Warehousing and Storage: Temperature Controlled Expansion Accelerates

Non-temperature space dominates at 91.54% of revenue share in 2025, but cold-chain demand jumps as vaccine imports, dairy processing, and seafood exports require sub-8°C integrity, with a projected CAGR of 4.12% between 2026-2031. Developers build multi-compartment chambers with 24-hour diesel back-up and humidity monitoring, yet capital intensity and energy tariffs challenge ROI. Joint ventures with multinationals supply operational know-how, while government duty waivers on reefer panels spur uptake.

Operators market pay-per-use pallet slots and GMP-compliant packing rooms, enticing SMEs locked out of build-to-suit leases. Value-added kitting, labeling, and blast-freezing supplement storage fees. Real-time temperature logs accessed via cloud platforms boost compliance with EU and FDA standards, enhancing export competitiveness for processed seafood.

By Freight Transport Mode of Transport: Maritime Infrastructure Drives Volumes

Road freight transport captured 66.96% revenue share in 2025 and remains essential for last-mile coverage despite higher cost per ton-km; efficiencies are sought via telematics and graduated toll rebates for Euro 6 trucks. Air freight transport, moving significant freight volume and expected to grow at a CAGR of 4.90% between 2026-2031, sustains premium yields, catalyzing freighter up-gauges at Bandaranaike International Airport and regional charters for live seafood. Axle-load limits and circuitous routes restrain rail freight’s contribution; modernization projects plan heavier sleepers and container wagons to shift clinker and grain inland. Pipelines ferry tons of petroleum, offering cost stability and bypassing road congestion. Collectively, modal integration remains a priority: synchronized port gate booking for trucks, scheduled rail shuttles to ICDs, and dredged barge channels along the Kelani River promise throughput gains.

By Freight Forwarding: Sea and Inland Waterways Routes Maintain Dominance

Sea and inland waterways freight forwarding retained a 50.22% revenue share in 2025 due to cost efficiency for garments, tea, and rubber exports. Air freight forwarding, though smaller, registers a 4.37% CAGR (2026-2031) fueled by pharma consignments, electronics spares, and high-value perishables requiring sub-48-hour transit. Hybrid “sea-air” offerings via Dubai and Kuala Lumpur optimize cost-to-speed ratios, and forwarders bundle LCL consolidations at Colombo ICDs to fill freighters ex-Dubai. Road and rail forwarding remains constrained by island geography but stands to gain once roll-on, roll-off links with South India materialize. Digitally enabled freight marketplaces match cargo with empty truck legs, lifting backhaul utilization. Forwarders that deploy real-time visibility dashboards and predictive ETA alerts, once reserved for integrators, differentiate services and add extended liability coverage.

Geography Analysis

Western Province dominates throughput, driven by Colombo Port, the expressway grid, and 67% of GDP-linked consumption. Surging TEUs there highlight the centrality of the Sri Lanka freight and logistics market to global East-West lanes. However, congestion and land scarcity elevate land prices, propelling investors to satellite ICDs in Pannala and Horana. Southern Province gains from Hambantota’s deep draft and automotive transshipments that bypass Colombo’s peaks, yet hinterland rail links lag. The Eastern Province sees uplift as the USD 61.5 million refurbishment of Kankesanthurai Port links with Indian coastal services, broadening connectivity to Chennai markets.

Southern Province benefits from Hambantota Port’s deep draft, which now attracts roll-on roll-off car carriers and bulk energy cargo that bypass Colombo during peak congestion. Despite the capacity, limited rail and highway links into the hinterland keep utilization below 50% of the designed throughput, constraining the Sri Lanka freight and logistics market size captured by the region. In the north, India’s USD 61.5 million refurbishment of Kankesanthurai Port and the planned Palaly air-sea corridor promise direct connectivity to Tamil Nadu that can shorten lead times for seafood exporters. Eastern Province remains export-oriented in tea and minerals but faces seasonal cyclone disruptions that inflate trucking insurance premiums each fourth quarter.

Northern Province, historically peripheral, will gain fresh impetus once the Palaly air-sea-road corridor matures, reducing Colombo dependency for perishable seafood exports. Central Province’s mountainous topography inflates diesel consumption and axle wear, narrowing payload economics; yet expressway extensions are slated to improve gradients and cut travel time. Monsoonal flooding in Eastern and Southern lowlands remains a seasonal risk, compelling forwarders to pre-position stock in elevated ICDs. Across the island, ASYCUDA’s uniform deployment reduces regional disparities by enabling electronic submission from any province, although telecom connectivity gaps persist in remote districts.

Competitive Landscape

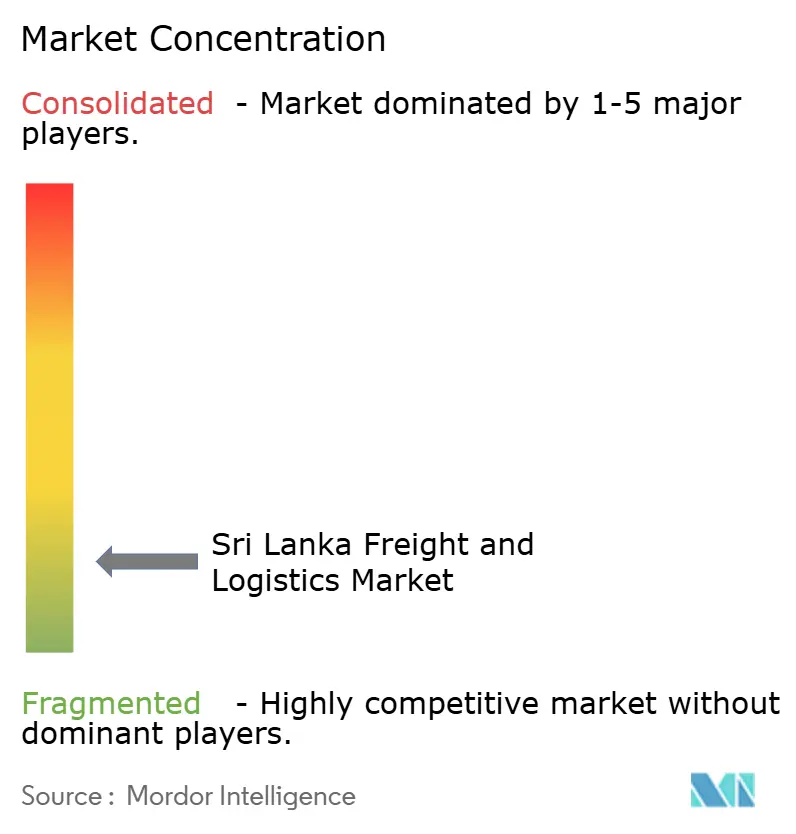

The market is fragmented; however, global consolidation reshapes competitive dynamics as DSV completes the EUR 14.3 billion (USD 15.8 billion) DB Schenker acquisition, forging the world’s largest 3PL with an enhanced Asia-Pacific footprint. Scale economies grant rate leverage on main-lane carriers and IT budget for predictive analytics out of reach for smaller incumbents. Domestic stalwarts, John Keells Logistics, Hayleys Advantis, and Expolanka Freight, retain customer loyalty through localized problem-solving and bonded trucking fleets that navigate provincial nuances.

Differentiation hinges on technology: South Asia Gateway Terminals’ integration with TradeLens blockchain slashes document processing, while Maersk’s new 100,000 ft² Wattala warehouse offers digital twin visibility. Temperature-controlled logistics and last-mile e-commerce delivery are coveted white spaces; players that secure land near expressway ramps and deploy electric vans position themselves for premium margins. Nevertheless, high port costs compress profitability, forcing alliances and slot-chartering agreements to share capacity risk.

Policy unpredictability on terminal privatization injects caution into long-horizon investments. Operators hedge by leasing rather than owning yard gear and advocating for fixed concession terms. Talent retention emerges as a differentiator; firms institute graduate trainee programs and data science labs to nurture supply-chain specialists, keeping attrition below regional averages.

Sri Lanka Freight And Logistics Industry Leaders

Hayleys Advantis, Ltd.

John Keells Logistics (Pvt), Ltd.

Aitken Spence Group (Including Ace Express International Pvt., Ltd.)

DHL Group

A.P. Moller - Maersk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV A/S closed its EUR 14.3 billion (USD 15.78 billion) acquisition of DB Schenker, vaulting to global leadership in contract logistics and forwarding.

- January 2025: CMA CGM Group confirmed a USD 25 million expansion of its Colombo terminal, featuring automated gantry cranes and AI-driven container stacking.

- April 2024: Maersk opened a 100,000 ft² export-consolidation warehouse in Wattala, augmenting end-to-end 3PL offerings.

- April 2024: Aitken Spence Logistics inaugurated a 100,000 ft² container freight station in Mabole with multimodal links.

Sri Lanka Freight And Logistics Market Report Scope

Freight refers to the transportation of goods through air, rail, and roadways. Logistics refers to the overall process of managing how resources are acquired, stored, and transported to their destination.

Sri Lanka's freight and logistics market is segmented by end-user industry (manufacturing and automotive, oil and gas, mining, and quarrying, agriculture, fishing, forestry, construction, and distributive trade) and by function (freight transport, warehousing, freight forwarding, and value-added services).

The Sri Lankan freight and logistics market report offers the market size and forecast value (USD) for all the above segments.

The report provides a comprehensive background analysis of the Sri Lankan freight and logistics market, covering current market trends, market dynamics, technological updates, and detailed information on various segments and the industry's competitive landscape. Additionally, the COVID-19 impact has been incorporated and considered during the study.

End User Industry

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

Logistics Function

| Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | ||

| Freight Forwarding | By Mode of Transport | Air |

| Sea and Inland Waterways | ||

| Others | ||

| Freight Transport | By Mode of Transport | Air |

| Pipelines | ||

| Rail | ||

| Road | ||

| Sea and Inland Waterways | ||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | ||

| Other Services | ||

| End User Industry | Agriculture, Fishing, and Forestry | ||

| Construction | |||

| Manufacturing | |||

| Oil and Gas, Mining and Quarrying | |||

| Wholesale and Retail Trade | |||

| Others | |||

| Logistics Function | Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | |||

| Freight Forwarding | By Mode of Transport | Air | |

| Sea and Inland Waterways | |||

| Others | |||

| Freight Transport | By Mode of Transport | Air | |

| Pipelines | |||

| Rail | |||

| Road | |||

| Sea and Inland Waterways | |||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled | |

| Temperature Controlled | |||

| Other Services | |||

Key Questions Answered in the Report

What is the value of the Sri Lanka freight and logistics market in 2026?

The market is valued at USD 8.11 billion in 2026.

How fast is the market expected to grow through 2031?

It is forecast to expand at a 4.30% CAGR (2026-2031), reaching USD 10.01 billion by 2031.

Which logistics function is expanding the quickest?

Courier, express and parcel services show the fastest expected growth at a 5.20% CAGR between 2026 and 2031.

Why are integrated logistics parks important?

They decongest ports, bundle warehousing with customs and distribution, and cut total logistics costs.

What role does ASYCUDA World play in trade facilitation?

The platform processes 95% of customs declarations electronically, reducing clearance to under six hours.

How will the DSV–DB Schenker merger impact Sri Lanka operators?

The enlarged entity gains scale and IT capabilities, intensifying competition for complex multimodal contracts.

Page last updated on: