India Container Shipping Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

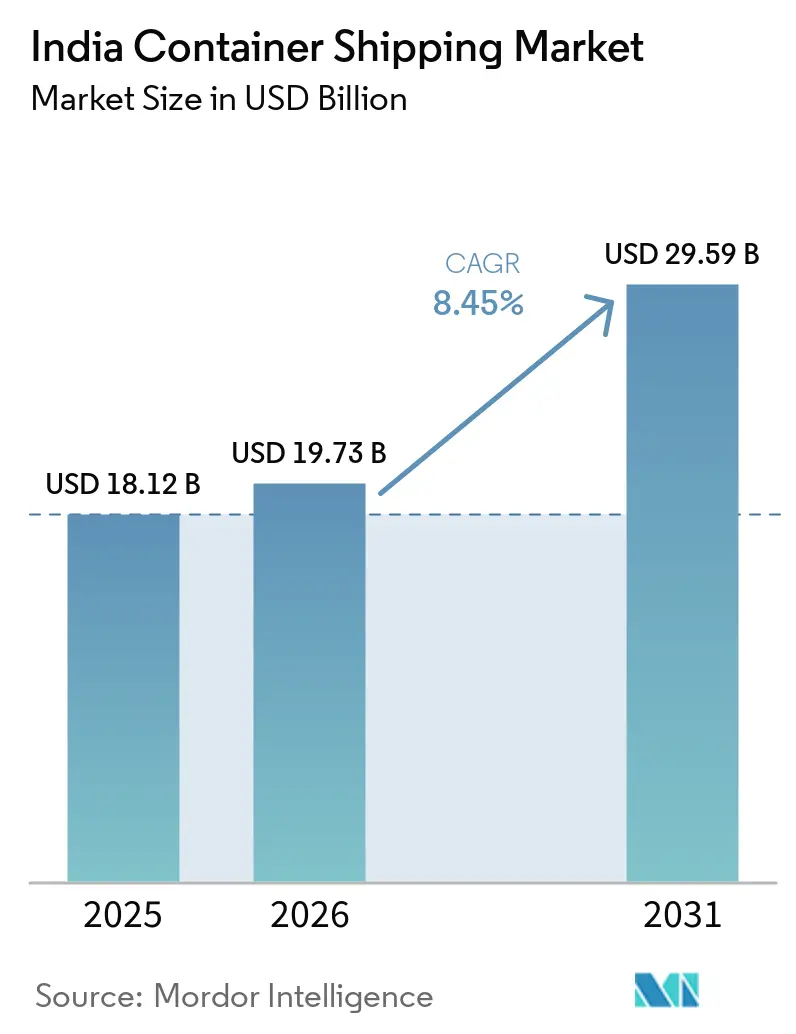

| Base Year Market Size (2025) | USD 18.12 Billion |

| Market Size (2026) | USD 19.73 Billion |

| Market Size (2031) | USD 29.59 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Container Shipping Market Analysis by Mordor Intelligence

The India container shipping market size is expected to increase from USD 18.12 billion in 2025 to USD 19.73 billion in 2026 and reach USD 29.59 billion by 2031, growing at a CAGR of 8.45% over 2026-2031.

India’s cargo base is becoming more container-friendly as manufacturing programs in electronics, pharmaceuticals, and auto components are adding export volumes that previously did not move through container channels. Major ports handled more than 915 million tons of cargo in FY 2025-26, ahead of the annual target, while overall throughput growth and record activity at JNPT showed that container handling is rising faster than the broader cargo system. Rail and port integration is also improving the operating base of the Indian container shipping market, as the completed Dedicated Freight Corridor network is reducing inland transit time and making direct port access more reliable for exporters in North and West India. Competitive behavior is shifting from pure capacity deployment to a broader push on reflagging, terminal access, and multimodal links, giving larger carriers a stronger position in the Indian container shipping market while opening new space for feeders and coastal operators. At the same time, route disruptions in West Asia and tariff pressure on India-United States trade are keeping planning conditions uneven, so growth in the India container shipping market is being supported more by structural trade and infrastructure changes than by stable global shipping conditions.

Key Report Takeaways

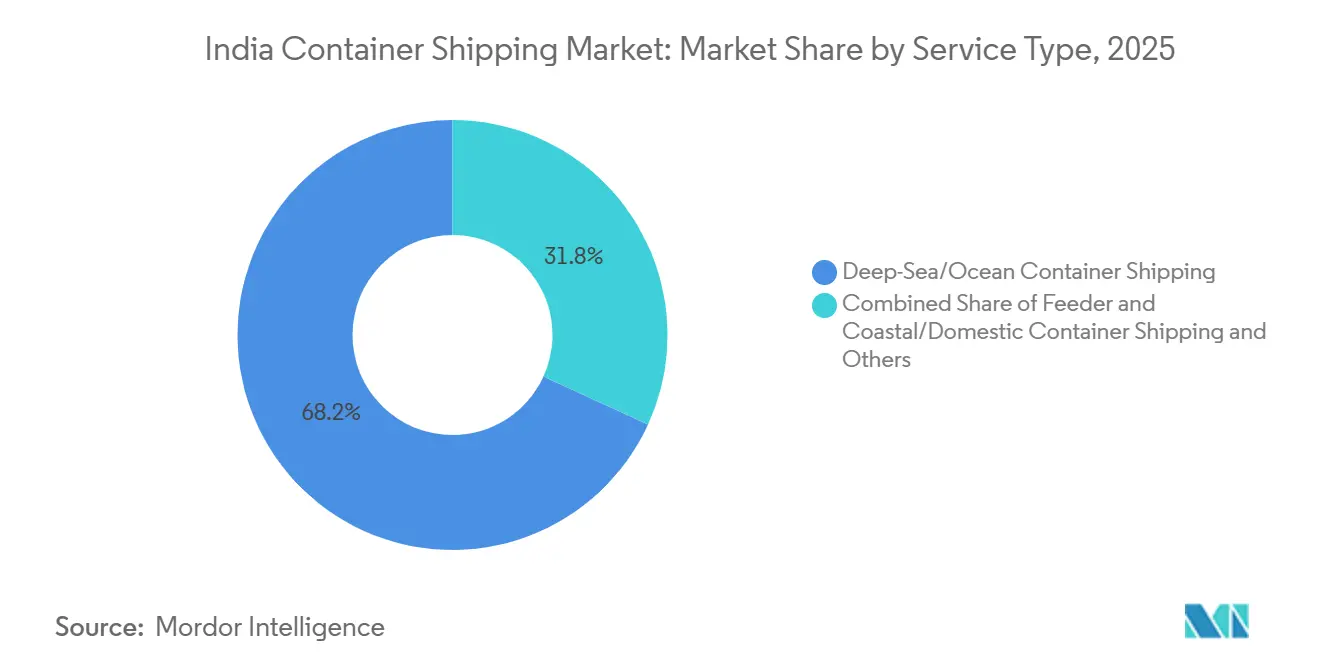

- By service type, deep-sea or ocean container shipping held 68.17% of India container shipping market size in 2025, while feeder and coastal or domestic container shipping recorded the highest projected CAGR at 9.43% through 2031.

- By container type, dry containers accounted for 81.90% of India container shipping market share in 2025, while reefer containers are forecast to grow at a 12.05% CAGR through 2031.

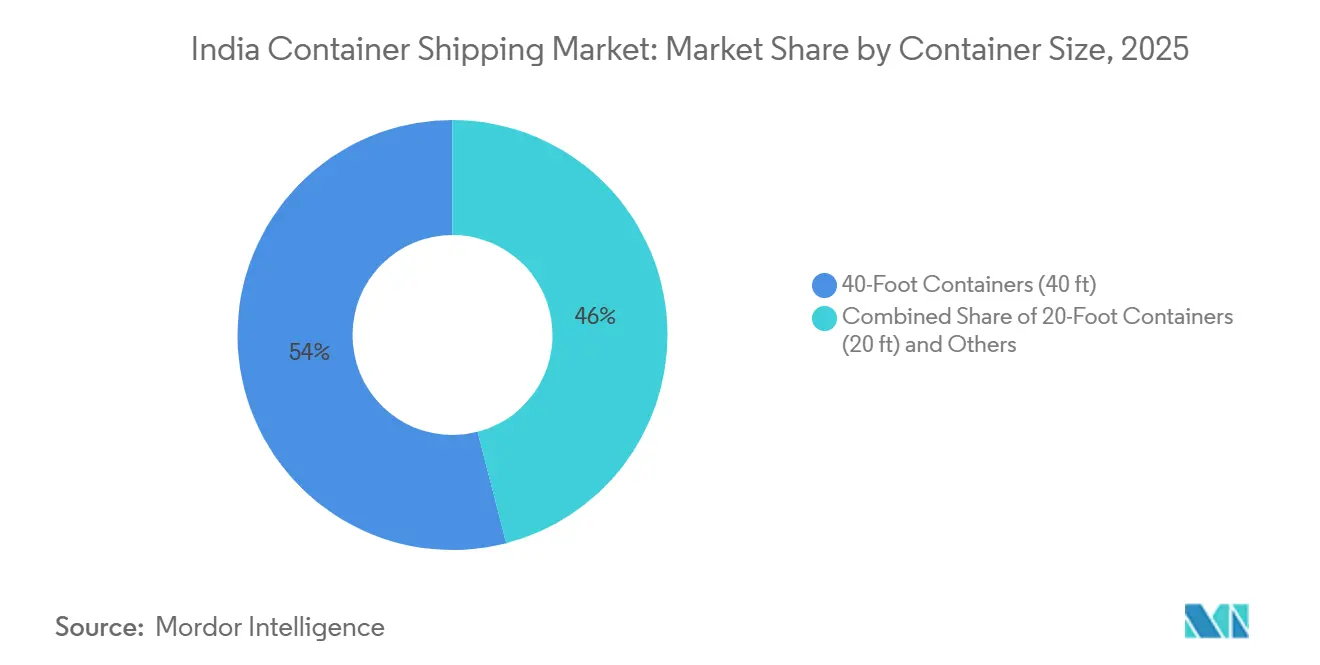

- By container size, 40-foot containers held 54.02% of India container shipping market size in 2025, while 20-foot containers are projected to expand at a 9.71% CAGR through 2031.

- By load type, FCL held 76% of the India container shipping market share in 2025, while LCL is advancing at an 11.45% CAGR through 2031.

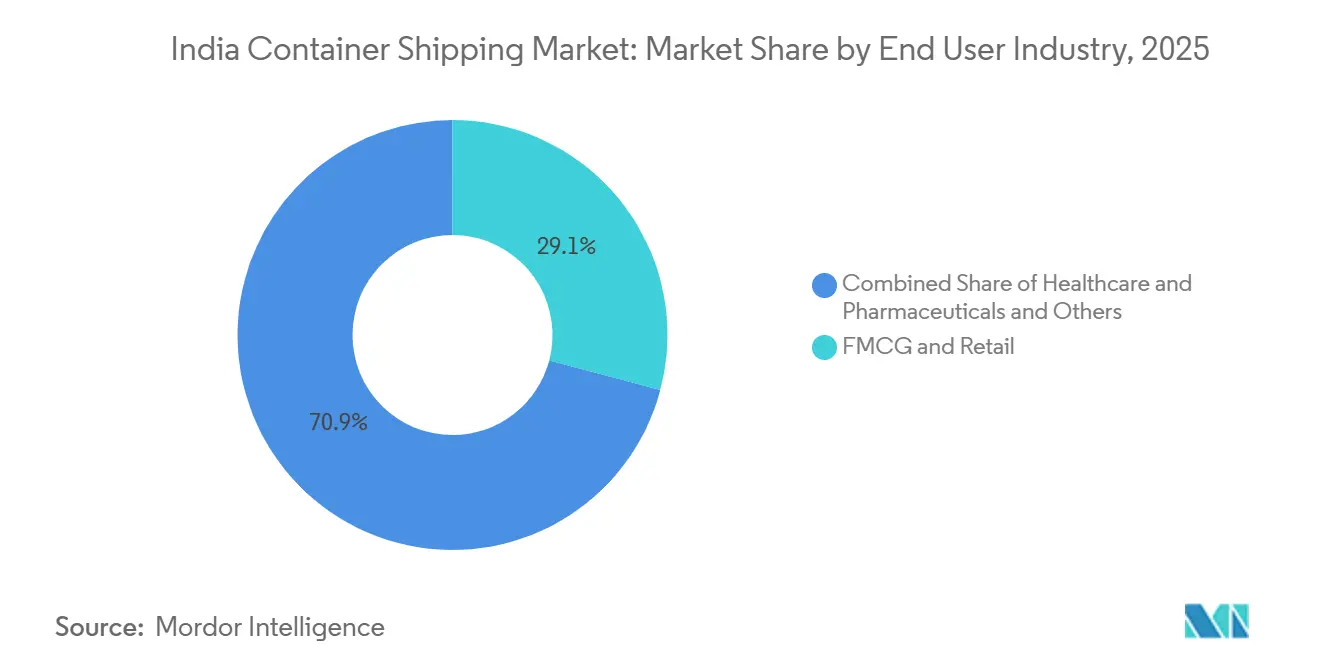

- By end-user industry, FMCG and retail accounted for 29.11% of India container shipping market size in 2025, while healthcare and pharmaceuticals are forecast to expand at a 10.77% CAGR through 2031.

- By geography, West India commanded 38.34% of India container shipping market size in 2025, while South India recorded the highest projected CAGR at 9.77% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Container Shipping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EXIM Containerization Across Key Industrial Corridors | +2.1% | National, with early gains in West and South India | Medium term (2-4 years) |

| Western Dedicated Freight Corridor Commissioning and Port Rail Integration | +1.4% | North-West India and connected inland depots | Short term (≤ 2 years) |

| Capacity Additions at Major West Coast and East Coast Ports | +1.3% | West, South, and East India | Medium term (2-4 years) |

| Transshipment Share Gains Through Coastal and Hub Port Routing | +0.9% | South India first, with spillover to West and East India | Medium term (2-4 years) |

| Foreign Carrier Network Expansion and Service Frequency Uplift | +0.8% | National, led by West Coast terminals | Short term (≤ 2 years) |

| Public Sector Push for Indigenous Container Shipping Capacity | +0.6% | National, with early emphasis on JNPT and coastal routes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising EXIM Containerization Across Key Industrial Corridors

The India container shipping market is benefiting from a steady rise in container use across industrial corridors, as the country still has room to convert more cargo from breakbulk and other modes into containers. Container cargo at Indian ports rose in FY 2025-26, alongside broader cargo growth and rising activity at major gateways. The change is especially visible in manufacturing belts in Gujarat, Tamil Nadu, and Andhra Pradesh, where electronics and auto-component production are driving more export-ready container flows. Record throughput at JNPT also showed that the shift is not limited to one cargo category, as the port handled 8.17 million TEUs in FY 2025-26, posting 11.9% growth. This pattern matters for the India container shipping market because it creates recurring demand from manufacturing supply chains rather than one-time export spikes. It also means future growth is likely to come from more regions and more commodities, broadening the demand base for carriers and terminals[1]Source: PSA India, “The Future of EXIM Trade in India, How PSA Is Enabling Seamless Cargo Movement,” PSA India, india.globalpsa.com.

Western Dedicated Freight Corridor Commissioning and Port Rail Integration

The completion of the Dedicated Freight Corridor network in 2025 improved the logistics base of the India container shipping market by connecting inland production zones more directly with port gates. DFCCIL stated that freight services on the corridor operate at much higher average speeds than legacy rail routes, and the corridor is designed to move far more containers per train than conventional lines. The corridor also supports more predictable inland delivery, which is important for exporters that need fixed sailing windows and for carriers that want stronger vessel utilization. Rail container movement through CONCOR’s network rose to 3.87 million TEUs in FY 2025-26, up 14.2% year over year, indicating that the modal shift is now in practice rather than a policy goal. The first sailing of Maersk’s FI2 service from Shanghai on June 4, 2026, also highlighted the growing role of Pipavav as a rail-linked gateway for North-West Indian shippers[2]Source: A.P. Moller - Maersk, “Maersk to Launch FI2 Ocean Service to Strengthen India-China Trade Connectivity,” The Hindu BusinessLine, thehindubusinessline.com. In the India container shipping market, this rail and port integration is reducing friction in the inland market and strengthening the value of West Coast gateways for both imports and exports.

Capacity Additions at Major West Coast and East Coast Ports

New terminal and berth capacity is giving the India container shipping market more room to handle larger volumes and a wider vessel mix. PSA Mumbai’s Phase 2 terminal became operational in 2025, increasing the complex's total capacity to 4.8 million TEUs and adding modern equipment to support more efficient yard operations. The market is also seeing stronger momentum in South India because deepwater capacity at Vizhinjam is starting to support direct calls from very large vessels, which changes how transshipment can be routed within the country. On the eastern side, new facilities and projects are beginning to reduce the long-standing imbalance in container infrastructure between the West Coast and the East Coast, even though the West Coast still leads by a clear margin. This matters for the India container shipping market because additional capacity does more than absorb cargo growth; it also improves scheduling options and supports service diversification. Over time, these additions will also make it easier for carriers to split cargo flows across multiple ports instead of relying too heavily on a small number of gateways.

Foreign Carrier Network Expansion and Service Frequency Uplift

The India container shipping market is attracting greater attention from global carriers because it offers volume growth, network relevance, and a rising role in Asia-centered trade flows. Hapag-Lloyd signed a letter of intent with the Ministry of Ports, Shipping, and Waterways on March 19, 2026, that covered reflagging, ship recycling, and investment in port infrastructure, and the carrier stated that its India commitments already exceed INR 6,000 crore (USD 700 million). Service additions also increased in 2026, with ONE updating its East-West network and Maersk and other operators expanding India links across Asia-facing trades. More frequent service loops help shippers by reducing waiting time for sailings and expanding options for time-sensitive or lower-volume cargo. They also intensify price and service competition, which can reduce freight pressure for cargo owners while forcing carriers to defend margins through scale and network quality. As a result, the India container shipping market is becoming more strategically important not only as a destination but also as a network node.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strait of Hormuz, Red Sea, Panama Canal, and Geopolitical Route Disruptions | -1.1% | Highest exposure in West India, with secondary effects on transshipment flows in South India. | Short term (≤ 2 years) |

| US Tariff Exposure on Containerized Export Sectors | -0.9% | Export-heavy clusters in West and South India | Short term (≤ 2 years) |

| Rail Haulage Cost Pressure and Inland Dwell Time Inefficiency | -0.5% | North-West India corridor and inland depots | Medium term (2-4 years) |

| West Coast Terminal Congestion and Vessel Slot Constraints | -0.4% | JNPT, Mundra, Kandla, with spillover to nearby ports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strait of Hormuz, Red Sea, Panama Canal, and Geopolitical Route Disruptions

The India container shipping market faced a severe operating shock in early 2026 when the Strait of Hormuz disruption affected trade movement linked to the Gulf and nearby routes. The disruption trapped a large number of ships in the Persian Gulf and sharply raised war-related surcharges for cargo owners, thereby raising transport costs and delaying shipments. The effect was especially visible at West Coast gateways because rerouted and delayed containers increased pressure on handling and dwell times. Longer diversion routes also raised fuel use and extended transit times to Europe and the United States, which hit smaller exporters harder because they have less bargaining power on emergency freight terms. Even with emergency policy support and temporary operational adjustments, the India container shipping market still carries clear exposure to disruptions along the Gulf and Red Sea corridor. This keeps route stability as a major risk for carriers, ports, and exporters through the near term[3]Source: Times of India, “Red Sea Risks Resurface, Exporters Warn of Shipment Delays, Higher Freight and Insurance Costs Amid Middle East Conflict,” Times of India, timesofindia.indiatimes.com.

US Tariff Exposure on Containerized Export Sectors

The India container shipping market also faces demand pressure from tariffs on India-United States trade, as several container-intensive export categories rely on that route. India’s exports to the United States fell 21.8% in January 2026 after the 50% tariff move in August 2025, and the subsequent reduction to 18% only partly eased the pressure. Home textiles, marine products, gems and jewelry, and engineering components are especially exposed because they are heavily containerized and depend on consistent lane demand. Lower vessel utilization on India-United States services also creates a carrier-side problem because lines that deployed extra capacity may not be able to fill it at normal yield levels. That makes service restructuring or redeployment more likely if tariff conditions continue. For the India container shipping market, diversification toward the GCC, ASEAN, and Europe is helping. Still, it does not fully replace the scale or product mix of the United States trade corridor in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Feeder and Coastal Routes Challenge Deep-Sea Dominance

Deep-sea or ocean container shipping held 68.17% of the India container shipping market share in 2025, making it the anchor of the India container shipping market. This position reflects the weight of India’s long-haul export and import lanes to Europe, North America, and East Asia, where large gateways such as JNPT and Mundra remain central to cargo routing. The service type benefits from scale, established schedules, and cargo concentration driven by major manufacturing and consumption flows. Deep-sea demand is also supported by the continued rise in port throughput, with major ports handling more than 915 million tons in FY 2025-26 and JNPT reaching record container activity in the same period. Short-sea activity is still smaller because intra-regional trade patterns around India are not yet as dense as those seen in Southeast Asia.

Feeder and coastal or domestic container shipping is projected to grow at a 9.43% CAGR through 2031, making it the fastest-growing service type in the India container shipping market. Its growth is supported by two linked changes: the rise in Indian transshipment handling and the push to move more domestic cargo by coast rather than road. The market is also seeing direct carrier interest in coastal and feeder activity, as operators look to use India-registered tonnage and local partnerships to improve access to domestic routes. This shift matters because it widens service layers below the mainline trade, giving secondary ports and regional cargo owners more consistent connectivity. In practical terms, feeder growth will make the India container shipping market less dependent on a few direct mainline calls and more flexible in the way cargo moves between hubs and regional ports. It also increases the value of South Indian ports that can connect deepwater transshipment with coastal distribution.

By Container Type: Reefer Growth Reframes the Dry Container Story

Dry containers accounted for 81.90% of the India container shipping market size in 2025, making them the largest container category. This dominance came from the wide range of goods that still move in standard dry units, including FMCG, manufactured products, textiles, and industrial inputs. Dry containers align with India’s current trade structure, as many export and import categories do not require temperature control. They also align well with the scale of FCL movement, which remains the primary load format for larger shippers across long-haul routes. In that sense, dry boxes continue to provide the volume base that keeps the India container shipping market stable across many end-use sectors.

Reefer containers are projected to grow at a 12.05% CAGR through 2031, which is well above the overall pace of the India container shipping market. This faster rise is tied to pharmaceuticals, vaccines, temperature-sensitive ingredients, and a wider cold-chain requirement that is moving beyond agricultural seasonality. Maersk’s dedicated weekly reefer rail service from Hyderabad to Nhava Sheva, launched in May 2026 with CONCOR, showed that this cold-chain buildout is becoming more structured and commercially scalable. As the pharmaceutical export base expands, reefer use is likely to spread from a niche requirement into a more regular part of export planning. That change matters for the Indian container shipping industry because reefer cargo requires higher service complexity, greater demand for specialized equipment, and tighter coordination between inland logistics and port handling. It also means that future value growth may outpace volume growth in this segment, as specialized movement entails higher service content.

By Container Size: 20-Foot Units Regain Ground as Cargo Mix Changes

40-foot containers held 54.02% of India's container shipping market share in 2025, making them the largest size category in the market. Their lead came from FCL-heavy trade lanes where shippers want to maximize booking efficiency on long-distance routes to Europe and North America. These units also suit cargo categories where volume rather than weight sets the shipment limit, such as garments, packaged consumer goods, and many pharmaceutical movements. High-cube 40-foot boxes remain the practical default for many exporters because they support better cargo density per booking without requiring multiple smaller consignments. Other specialized sizes still serve narrower use cases, mainly in project cargo, heavy engineering, and select automotive export flows.

20-foot containers are forecast to grow at a 9.71% CAGR through 2031, which makes them the fastest-growing size segment in the India container shipping market. The rise is linked to two visible changes: more LCL and smaller shipment behavior among MSME exporters, and stronger movement of intermediate goods that do not always justify a 40-foot booking. This is especially relevant for trade with nearby Asian partners, where replenishment cycles can be shorter, and shipment frequency matters more than maximum unit size. Smaller box demand also fits shorter-haul and feeder-connected routes, where flexibility and quicker consolidation matter. In the India container shipping market, this means size demand is becoming more balanced across shipment profiles rather than remaining tied to large FCL exports. It also suggests that cargo planning is shifting from pure scale toward a mix of scale and frequency.

By Load Type: LCL’s Expansion Reflects a Broader Export Base

FCL accounted for 76% of India container shipping market size in 2025, giving it a clear lead in the market. Large exporters prefer FCL because it provides container control, lower unit freight for larger cargo lots, and fewer handling points for sensitive shipments. This aligns well with established sectors such as textiles, automotive components, chemicals, and FMCG, where order volumes are large enough to fill containers regularly. FCL also aligns with the deep-sea orientation of India’s main export routes, where regular sailings and larger volumes support direct full-container movement. As a result, FCL remains the operational backbone of the India container shipping market across the main ports and long-haul trades.

LCL is projected to grow at a 11.45% CAGR through 2031, making it the fastest-growing load type in the India container shipping market. That rise reflects the growing role of smaller exporters, fashion and handloom suppliers, specialty food producers, and direct-to-consumer brands that ship below the full-container threshold. LCL also becomes relevant when exporters need weekly or more frequent shipment schedules but do not have enough cargo for FCL. The wider ability to move both FCL and LCL cargo through more Indian ports under the 2026 customs circular improves route choice and helps cargo bypass some congestion points. Over time, this will make the India container shipping market more accessible to a broader shipper base rather than keeping ocean freight concentrated among larger firms. It also brings more consolidation and deconsolidation activity into the logistics chain, which benefits ports and service providers that can handle higher shipment complexity.

By End-User Industry: Healthcare Gains on a Broad FMCG Base

FMCG and retail held 29.11% of India container shipping market share in 2025, which made it the largest end-user group in the market. This lead came from India’s large role in supplying packaged consumer goods, beverages, and household products to destinations in the GCC, Southeast Asia, Europe, the United States, and the United Kingdom. FMCG cargo supports steady box movement because product cycles are regular and shipment programs tend to be repeatable across the year. The category also benefits from both export and import activity, which helps maintain consistent port throughput and container demand. That keeps FMCG central to the India container shipping market even as other sectors gain momentum.

Healthcare and pharmaceuticals are projected to grow at a 10.77% CAGR through 2031, which makes it the fastest-growing end-user segment in the India container shipping market. The shift is tied to stronger generics production, wider pharmaceutical exports, and the need for more controlled transport conditions for certain formulations and active ingredients. Maersk’s Hyderabad-to-Nhava Sheva reefer rail service is an early sign that carriers and inland operators now see pharma-linked container demand as large enough to support dedicated rail movement. The category is also reshaping service needs, as pharmaceutical cargo often requires more monitoring, tighter timing, and specialized box handling than standard retail flows. For the Indian container shipping industry, this creates a different quality of demand from that driven by FMCG alone. It raises the importance of cold-chain integration, inland scheduling, and port readiness for higher-value cargo.

Geography Analysis

West India held 38.34% of the India container shipping market share in 2025, giving it the largest regional share. The region remains the center of India’s container system because it combines large gateways, established carrier networks, and stronger rail connectivity with inland manufacturing centers. JNPT processed 8.17 million TEUs in FY 2025-26 and posted 11.9% growth, while major port cargo handling at the national level also moved above target during the same period. West India also benefits from the completed freight corridor, which reduces the effective inland distance for containerized cargo moving from Delhi-NCR and nearby industrial belts. That operating advantage is difficult for other regions to match in the near term. It keeps the region central to both deep-sea services and inland cargo collection.

South India is forecast to grow at a 9.77% CAGR through 2031, which makes it the fastest-growing region in the India container shipping market. The region is benefiting from a stronger export base in pharmaceuticals and electronics, as well as from a new transshipment capability that was previously limited in India. This combination is changing South India from a secondary support region into a more active cargo and routing center. The presence of deeper water handling, more port investment, and improving coastal links is widening its role in both international and domestic services. South India also stands to benefit when cargo owners want alternatives to West Coast congestion or longer inland drayage. That is why the region is likely to take a larger share of incremental growth even if West India remains the overall leader.

North India does not function as a seaport region. However, it is still deeply tied to the India container shipping market because its manufacturing belts feed large volumes into West Coast gateways. The Dedicated Freight Corridor has improved that link by making rail-based container movement faster and more reliable. East India is gaining relevance as port projects and rail-sea solutions reduce its historic dependence on foreign transshipment points. At the same time, Central India remains reliant on inland depots and feeder logistics rather than on direct port strength. Together, these shifts suggest that regional growth in the India container shipping market will become more distributed, even though the West will continue to dominate absolute volumes through the forecast period.

Competitive Landscape

The India container shipping market is highly consolidated. Large global alliances account for much of the long-haul capacity deployed on India routes, while MSC remains the leading independent carrier following the 2M breakup in January 2025. This structure gives the biggest lines an advantage in network design, slot access, and the ability to combine India with broader East-West schedules. At the same time, it does not create a closed market because coastal services, regional loops, and specialized cargo movements still leave room for second-tier and niche operators. That balance is why the India container shipping market shows concentration at one layer and fragmentation at another.

One major strategic move came from Hapag-Lloyd, which announced in February 2026 that it had signed a merger agreement to acquire ZIM for more than USD 4.2 billion. Another important move came from the same carrier in India, where its March 2026 letter of intent covered vessel reflagging, ship recycling, and port-related investment, showing that its plan goes beyond simple capacity deployment. Maersk also expanded its inland integration with its dedicated pharma reefer rail service from Hyderabad to Nhava Sheva, linking ocean freight more directly with a high-value export cluster. These examples show that competition in the India container shipping market is now built around network quality, inland reach, and specialized service capability. They also show that investment is shifting toward the places where cargo control and route resilience can be improved.

At the feeder and short-sea level, competition is broader because more operators can enter with regional services, local partnerships, or coastal positioning. Unifeeder’s October 2025 memorandum of understanding with Sagarmala Finance Corporation showed how feeder players are leveraging policy alignment and coastal service development to strengthen their role in India[4]Source: Unifeeder, “Unifeeder & Sagarmala Sign MoU,” Unifeeder, unifeeder.com. ONE’s service network updates and India-linked loops also indicate that schedule design is becoming a competitive tool in the India container shipping market rather than just a background operating choice. The practical result is that carriers with terminal relationships, inland links, and the ability to serve both major and secondary ports will have a stronger position than carriers competing only on basic space supply. That keeps the India container shipping market open to new moves, but it also raises the execution bar for companies that want to win share over the next few years.

India Container Shipping Industry Leaders

Mediterranean Shipping Company (MSC)

A.P. Moller – Maersk

CMA CGM Group

COSCO SHIPPING Lines

Hapag-Lloyd AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Maersk and CONCOR launched India's first dedicated weekly reefer rail service connecting Hyderabad's pharmaceutical manufacturing cluster to Nhava Sheva port on a fixed weekly schedule with 40-foot refrigerated containers.

- April 2026: ONE launched the Japan-Thailand-Vietnam-Indian Subcontinent (JTI) service from April 4, 2026, integrating 3 prior services into a single weekly loop calling at Tokyo, Yokohama, Shimizu, Nagoya, Osaka, Kobe, Cai Mep, Laem Chabang, Singapore, Port Klang, Nhava Sheva, Pipavav, Karachi, and Colombo.

- February 2026: Hapag-Lloyd signed a merger agreement to acquire 100% of ZIM Integrated Shipping Services for USD 35.00 per share, valuing the transaction at over USD 4.2 billion. The deal will lift the combined entity from sixth to joint-third in global fleet capacity, alongside ONE. It will carve out a new Israeli domestic container line with 16 vessels for FIMI, Israel's largest private equity firm.

- October 2025: Unifeeder (DP World) signed an MoU with Sagarmala Finance Corporation (SMFCL) to jointly develop and scale commercially sustainable coastal and short-sea shipping services across India, covering operational excellence, shipping corridors, and DFC integration.

India Container Shipping Market Report Scope

| Deep-Sea/Ocean Container Shipping |

| Short-Sea Container Shipping |

| Feeder and Coastal/Domestic Container Shipping |

| Dry Containers (General Purpose) |

| Reefer Containers |

| 20-foot Containers (20 ft) |

| 40-foot Containers (40 ft) |

| Other Specialized Sizes |

| Full-Container-Load (FCL) |

| Less-Than-Container-Load (LCL) |

| FMCG and Retail |

| Manufacturing and Automotive |

| Healthcare and Pharmaceuticals |

| Electronics and Electrical Equipment |

| Industrial Chemicals and Raw Materials |

| Others |

| North |

| Central |

| West |

| East |

| South |

| By Service Type | Deep-Sea/Ocean Container Shipping |

| Short-Sea Container Shipping | |

| Feeder and Coastal/Domestic Container Shipping | |

| By Container Type | Dry Containers (General Purpose) |

| Reefer Containers | |

| By Container Size | 20-foot Containers (20 ft) |

| 40-foot Containers (40 ft) | |

| Other Specialized Sizes | |

| By Load Type | Full-Container-Load (FCL) |

| Less-Than-Container-Load (LCL) | |

| By End-User Industry | FMCG and Retail |

| Manufacturing and Automotive | |

| Healthcare and Pharmaceuticals | |

| Electronics and Electrical Equipment | |

| Industrial Chemicals and Raw Materials | |

| Others | |

| By Region | North |

| Central | |

| West | |

| East | |

| South |

Key Questions Answered in the Report

What is the expected value of India container shipping by 2031?

The India container shipping market size is projected to reach USD 29.59 billion by 2031, rising from USD 19.73 billion in 2026 at an 8.45% CAGR.

Which service segment is growing fastest in India container shipping?

Feeder and coastal or domestic container shipping is the fastest-growing service type, with a projected CAGR of 9.43% through 2031.

Why is reefer demand rising in India’s container trade?

Reefer containers are forecast to grow at a 12.05% CAGR as pharmaceutical and cold-chain cargo become a larger part of export movements.

Which region leads container shipping activity in India?

West India led with 38.34% of market value in 2025, thanks to major gateways, stronger carrier presence, and better inland rail connectivity.

What is driving LCL growth in India?

LCL is expanding at a 11.45% CAGR because MSME exporters and direct-to-consumer brands are entering ocean freight with smaller, more frequent shipments.

How concentrated is competition among shipping companies in India?

Competition is concentrated in deep-sea mainline services because large alliances shape much of the capacity, but feeder and coastal services remain more fragmented.

Page last updated on: