China Automotive Chassis Dynamometers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

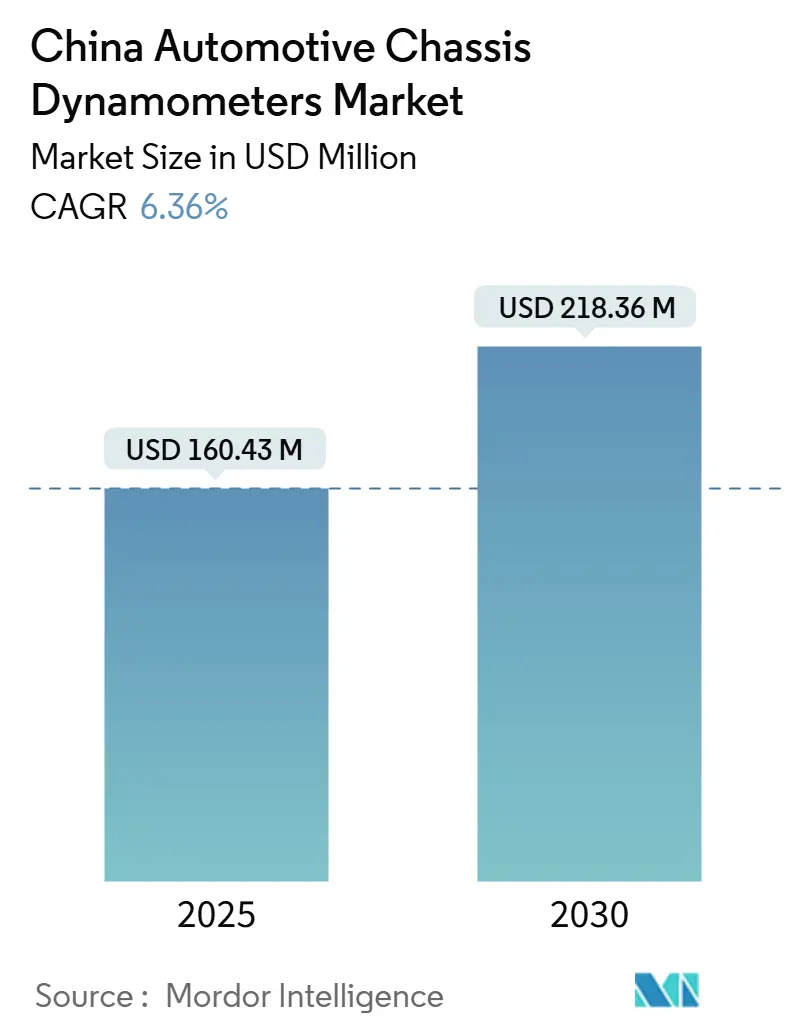

| Market Size (2025) | USD 160.43 Million |

| Market Size (2030) | USD 218.36 Million |

| Growth Rate (2025 - 2030) | 6.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Automotive Chassis Dynamometers Market Analysis by Mordor Intelligence

The China chassis dynamometer market size reached USD 160.43 million in 2025 and is forecast to attain USD 218.36 million by 2030, reflecting a 6.36% CAGR. The China chassis dynamometer market benefits from the country’s rapid new-energy-vehicle (NEV) penetration, a regulatory pivot toward China VI and WLTP-aligned test cycles, and provincial subsidies that favor domestic equipment makers. Electric-vehicle R&D expansion inside original-equipment-manufacturer (OEM) labs, coupled with the integration of artificial-intelligence (AI) driven digital-twin tools, is reshaping test-cell specifications to accommodate both emissions compliance and complex electric-powertrain validation. The China chassis dynamometer market continues to attract investment as OEMs attempt to shorten product-development loops, mitigate supply-chain risks in precision sensors and rare-earth materials, and future-proof facilities for forthcoming hydrogen-fuel-cell platforms. Supply volatility in precision-roller steel and sensor components, as documented by global raw-material exporters, remains the principal operational challenge for international suppliers.

Key Report Takeaways

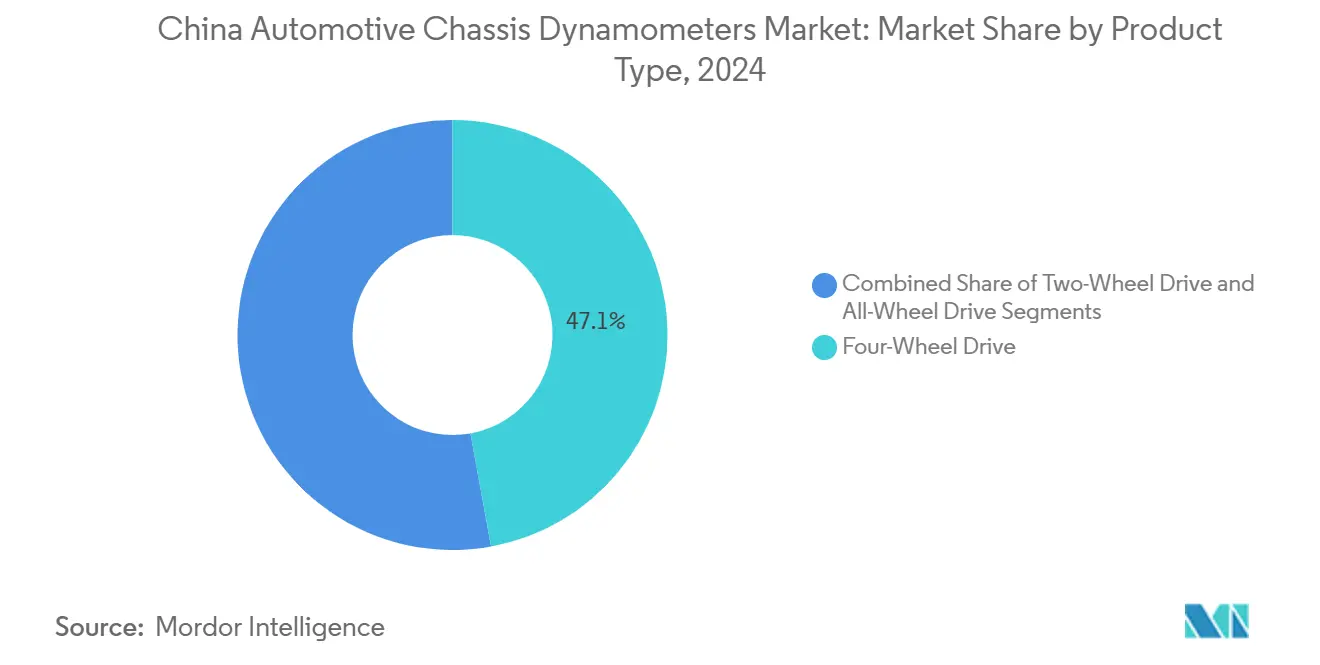

- By product type, four-wheel-drive systems captured 47.13% of China chassis dynamometer market share in 2024, whereas all-wheel-drive configurations are projected to expand at an 8.11% CAGR through 2030.

- By application, emissions testing accounted for a 42.31% slice of China chassis dynamometer market size in 2024, while electric and autonomous component testing are projected to record the highest forecast CAGR at 9.85% to 2030.

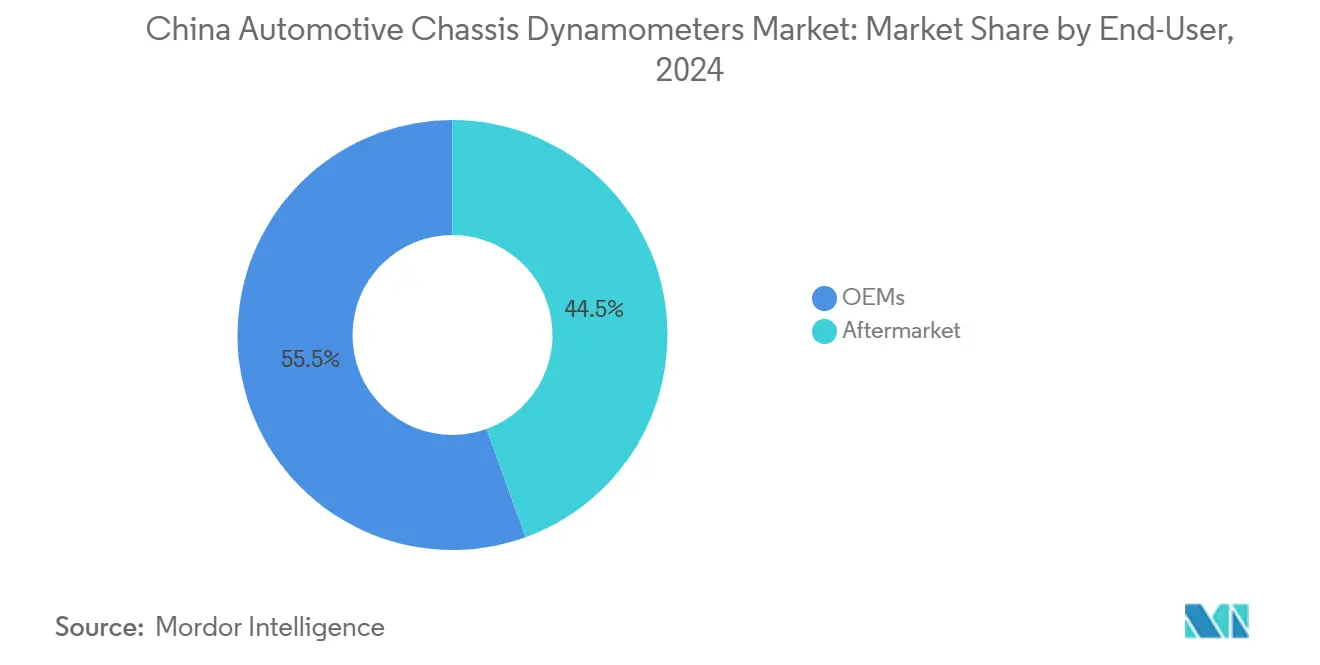

- By end-user, OEM laboratories held 55.53% of China chassis dynamometer market size in 2024 and are projected to lead growth with an 8.73% CAGR through 2030.

- By propulsion, battery-electric-vehicle platforms commanded 39.65% of China chassis dynamometer market share in 2024, whereas fuel-cell-electric vehicles are projected to show the fastest expansion at a 7.67% CAGR through 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with China representing one among them. The global report on automotive chassis dynamometers market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

China Automotive Chassis Dynamometers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid NEV Production Capacity | +1.1% | Guangdong, Jiangsu, Shanghai, Zhejiang | Medium term (2-4 years) |

| In-house R&D Test Cells | +0.9% | Beijing, Shanghai, Guangdong, Anhui | Medium term (2-4 years) |

| Stringent Emission Regulations | +0.8% | National, with early implementation in Beijing, Shanghai, Guangzhou | Short term (≤ 2 years) |

| Digital-twin / NVH-simulation Integration | +0.7% | Beijing, Shanghai, Shenzhen, Suzhou | Long term (≥ 4 years) |

| Aftermarket Performance-tuning | +0.6% | Beijing, Shanghai, Guangzhou, Shenzhen | Short term (≤ 2 years) |

| Subsidies for Test-equipment Makers | +0.4% | Zhejiang, Jiangsu, Guangdong, Anhui | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Ramp-up of NEV Production Capacity (BEV and HEV)

NEV output surpassed 15 million units in 2024, creating urgent demand for high-throughput test bays capable of validating electric powertrains, battery-thermal behavior, and regenerative braking systems. Tier-1 provinces deploy dedicated NEV lines, each requiring chassis dynamometer installations for conformance and quality audits. The China chassis dynamometer market therefore scales directly with NEV assembly volume as factories equip dual-purpose cells that address both conventional and electrified vehicles. Local subsidies reduce acquisition cost gaps between domestic and imported systems, accelerating procurement. The requirement to certify energy-consumption claims under WLTP harmonized cycles further cements chassis dynamometer relevance in China’s electrification roadmap.

OEM Build-out of In-house E-Powertrain R&D Test Cells

Global and domestic automakers now internalize critical electric-powertrain testing to safeguard intellectual property and compress iteration loops. New laboratories integrate four-wheel-drive dynos with high-speed battery emulators, thermal-runaway chambers, and over-the-air update validation rigs. Such facilities often embed AI analytics that detect anomalies across thousands of data channels in real time, curbing downtime and enabling predictive maintenance. Substantial capital allocation underscores the strategic value of test capacity; Daimler’s USD 172 million Beijing center provides an archetype for future installations. As more OEM sites come online, the China chassis dynamometer market captures sustained equipment and service revenues over the medium term.

Stringent China VI and WLTP-Aligned Emission Regulations

China VI protocols require NOx reductions exceeding 60% versus prior standards and mandate road-load validation on chassis dynamometers for all vehicle classes. Alignment with European WLTP procedures standardizes test-bench specifications and elevates measurement precision for both particulate counts and electrical-energy use. Facilities must switch seamlessly between ICE emission probes and high-voltage power-analysis modules, driving demand for hybridized dyno solutions. MIIT’s 2025 automotive standardization agenda further tightens electric-vehicle safety criteria, compelling test-cell upgrades that incorporate battery thermal-runaway containment and high-voltage interlock checks.[1]Qiang Zhang et al., “Digital Twin-Based Gear Fault Diagnosis,” MDPI.COM, mdpi.com

AI-Enabled Digital-Twin / NVH-Simulation Integration Needs

Digital-twin engines paired with chassis dynamometers reconstruct full-vehicle dynamics in the cloud, enabling engineers to run accelerated durability scenarios that would take months on physical tracks. Machine-learning algorithms embedded in control software deliver 99% fault-diagnosis accuracy, reducing unplanned maintenance. As autonomous driving stacks grow, the dynamometer becomes a hardware-in-the-loop platform validating sensor fusion and traction-control logic under repeatable conditions. Suppliers that natively fuse AI, multi-physics simulation, and traditional drive-cycle replication gain competitive edge in the evolving China chassis dynamometer market.[2]Ministry of Industry and Information Technology, “Automotive Standardization Work Points 2025,” GOV.CN, gov.cn

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and OPEX | -1.0% | National, particularly affecting smaller testing facilities | Short term (≤ 2 years) |

| Sensor Supply Chain Volatility | -0.7% | National, with manufacturing concentration in Jiangsu, Zhejiang | Short term (≤ 2 years) |

| Complex Lab-automation | -0.6% | Beijing, Shanghai, Guangdong, Jiangsu | Medium term (2-4 years) |

| Virtual Simulation Reduction | -0.3% | Beijing, Shanghai, Shenzhen technology hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and OPEX of Multi-Axle Dyno Installations

Multi-axle chassis dynamometers that handle torque-vectoring electric all-wheel-drive vehicles demand reinforced flooring, high-capacity electrical feeds, and specialized cooling, pushing acquisition costs well beyond USD 3 million per cell. Operating expenses climb further owing to skilled-labor needs and heightened energy draw during regenerative-braking simulations. Smaller independent labs struggle to recover such investments, slowing equipment turnover cycles and creating a cost barrier that tempers broader China chassis dynamometer market penetration. While provincial grants soften initial outlays, long-term profitability depends on utilization rates that only large OEM or Tier-1 suppliers can guarantee.

Volatility In Precision-Roller Steel and Sensor Supply Chain

China’s export restrictions on rare-earth magnets and the global strain in precision-steel rolling have inflated lead times for rollers and high-resolution torque sensors. International vendors face shipment delays of four to six months, forcing test-cell commissioning schedules to slip and escalating project costs. Domestic manufacturers with proximal access to raw-material sources capitalize on the disruption, improving their share in the China chassis dynamometer market. Nevertheless, recurring supply bottlenecks threaten maintenance cycles, nudging laboratories to pre-stock critical spares at additional carrying cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: All-Wheel Drive Configurations Drive Market Evolution

Four-wheel-drive rigs held 47.13% of China chassis dynamometer market share in 2024, underscoring legacy passenger-car test needs. The segment remains a revenue bedrock, yet the China chassis dynamometer market size for all-wheel-drive systems is projected to expand at an 8.11% CAGR, propelled by electric SUVs and premium platforms that require synchronized torque control on each axle. Provincial labs retrofit existing two-wheel bays with independent-roller units and higher-power absorbers, seeking broader test envelopes. Hardware suppliers respond by introducing modular rollers that swap between FWD, RWD, and AWD layouts in under one hour, keeping bays flexible without ballooning CAPEX. As NEV architectures converge on dual-motor layouts, demand for all-wheel-drive compatibility will likely eclipse traditional four-wheel dominance by 2029.

In parallel, compact two-wheel-drive systems persist for small-car validation, commercial-van programs, and academic research centers with limited budgets. Although their share is forecast to decline incrementally, baseline demand stabilizes on account of fleet-compliance audits and ride-hailing vehicle inspections mandated by municipal regulators. Looking ahead, integrated hub-motor test fixtures may cannibalize some roller-based volume, yet development-phase durability runs and homologation cycles will continue to anchor roller-dyno usage across propulsion types within the China chassis dynamometer market.

By Application: Electric-Vehicle Testing Reshapes Traditional Emissions Focus

Emissions-measurement bays controlled 42.31% of China chassis dynamometer market size in 2024, a testament to the enduring need for particulate and gaseous verification on both pure-ICE and hybrid vehicles. However, the electric and autonomous-component segment is on a 9.85% CAGR trajectory, fueled by battery-degradation studies, motor-efficiency mapping, and over-the-air software validation. The China chassis dynamometer market responds with combined exhaust-gas sampling heads and high-voltage power analyzers that coexist in a single enclosure, cutting change-over time.

Powertrain-durability and fuel-efficiency applications occupy a middle ground, as OEMs harmonize test plans that monitor ICE thermal stresses alongside inverter thermal-runaway thresholds. Research institutes exploit AI to interpret large datasets emanating from multi-axis load cells, advancing state-of-the-art torque-vectoring control. The trend stimulates ancillary demand for dynamometer data-analysis suites, firewall-protected cloud gateways, and cybersecurity audits, service layers that now contribute measurable revenue within the broader China chassis dynamometer market.

By End-User: OEMs Accelerate In-House Testing Capabilities

OEM laboratories commanded 55.53% of China chassis dynamometer market size in 2024 and will outpace other segments with an 8.73% CAGR through 2030. Competitive urgency to safeguard electric-motor intellectual property and drive-cycle algorithms pushes automakers to insource dynamometer capability. Mega-campuses now house dozens of climate-controlled cells with -30 °C cold-start capacity and 4 WD regenerative-braking profiles. This scale unlocks volume discounts from equipment providers but also spawns demand for proprietary automation software, a lucrative after-sales service niche.

Aftermarket tuners, motorsport outfits, and independent emission-test centers maintain a stable slice of the China chassis dynamometer market by serving performance-oriented consumers and regulatory spot checks. These entities prioritize lower-budget chassis dynos, often refurbishing surplus OEM rigs. Government vehicle-replacement incentives funnel additional volume into inspection lanes, especially in Tier-1 cities, creating an annuity revenue stream for service providers that can calibrate both low-emission gasoline engines and 800-V silicon-carbide inverters.

By Propulsion Type: Battery Electric Vehicles Lead Market Transformation

Battery-electric vehicles (BEVs) secured 39.65% China chassis dynamometer market share in 2024, reflecting China’s pole position in global electric-car production. Robust BEV growth drives continuous requests for high-speed, low-coast-down roller assemblies rated above 250 km/h, plus regenerative-energy recovery options that re-feed the grid. The China chassis dynamometer market size attributed to BEV testing therefore scales in lockstep with gigafactory outputs.

Fuel-cell-electric vehicles (FCEVs) log the fastest CAGR at 7.67%, as national hydrogen-development roadmaps translate into pilot fleets across logistics and public-transport sectors. Dynos destined for FCEV labs integrate hydrogen leak-detection sensors, flameproof enclosures, and humidification modules that recreate stack-operating environments. Hybrid-electric models sustain testing demand because WLTP sequences quantify both tailpipe emissions and electrical efficiency, requiring dual-mode measurement rigs. Even though pure internal-combustion engines trend downward, optimization programs aimed at cost-sensitive markets preserve a baseline need for traditional emission-dynamometer testing, extending revenue continuity across propulsion modalities within the China chassis dynamometer market.

Geography Analysis

The eastern coastal belt dominates the China chassis dynamometer market, aligning with automotive manufacturing density and stringent environmental enforcement. Guangdong Province leads both equipment installations and service revenue, leveraging its multi-tier NEV supply chain and municipal subsidies that offset dyno acquisition costs for local OEMs. Facilities in Guangzhou operate 24-hour rotational shifts to process pre-delivery inspections, creating steady after-sales demand for sensor recalibration and roller resurfacing. Neighboring Jiangsu complements this cluster with a precision-manufacturing ecosystem that fabricates high-tolerance rollers and forged load cells, effectively anchoring upstream supply for the wider China chassis dynamometer market.

Shanghai forms a second epicenter, housing global R&D headquarters and start-up incubators that prioritize AI-enabled testing workflows. The metropolis provides RMB 15,000 vehicle replacement incentives through 2025, catalyzing churn in test cycles as fleets upgrade to NEV platforms. Laboratories within Shanghai’s Lingang Free-Trade Zone often incorporate digital-twin dashboards that visualize stress hotspots in real time, accelerating iterative design. Adjacent Zhejiang benefits from spillover demand, especially as indigenous test-equipment makers tap provincial grants aimed at raising domestic content in high-end instrumentation to approximately 75% by 2027. These policies augment the regional share of the China chassis dynamometer market and nurture a talent pool versed in both automation engineering and vehicle dynamics.

Northern hubs contribute specialized momentum. Beijing, China’s de facto automotive policy nerve center, channels research funding toward autonomous-vehicle safety validation, necessitating multifaceted dyno rigs with LiDAR and radar interference chambers. Anhui, propelled by electric-bus and logistics-vehicle production, relies on low-temperature test chambers that replicate plateau conditions prevalent in western routes. Western provinces remain nascent yet are earmarked for capacity migration under national industrial-balanced-development guidelines. As manufacturers pursue redundancy against coastal congestion, these interior regions represent the next frontier for the China chassis dynamometer market.

Mordor Intelligence provides coverage of the automotive chassis dynamometers market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India, South Korea, Japan, and United States incorporating local coverage and market participation, as required.

Competitive Landscape

The China chassis dynamometer market is moderately concentrated, with the top three suppliers collectively holding a subtle market share. HORIBA anchors leadership through its VULCAN 4 x 4 Compact platform, optimized for electric-vehicle torque pulses and energy-regeneration modes while achieving 97% cycle-to-cycle repeatability. Its 2028 strategic roadmap earmarks a new production facility set to boost global capacity by 20%, ensuring faster lead times for Chinese customers.

AVL leverages its PUMA 2 Machine-Learning software to offer closed-loop automation, minimizing human intervention and improving throughput by around 15%. The firm allocates a significant amount of its annual revenue to R&D, positioning it to embed virtual-sensor models that fill data gaps during transient-drive events. Domestic challenger Jiangsu Lanmec accelerates through localized supply chains, cutting average delivery time to a significant level among overseas rivals. Provincial tax credits on indigenous equipment and preferential financing further elevate its bid competitiveness, gradually lifting domestic brands’ influence over the China chassis dynamometer market.

Supply-chain headwinds reshape sourcing strategies across competitors. Rare-earth magnet restrictions inflate torque-sensor costs, prompting vendors to dual-source from emerging suppliers in Jiangxi and Sichuan. Firms also pivot to cloud-based remote-service contracts that deliver real-time health diagnostics, deriving recurring revenue streams while mitigating travel restrictions. As AI features and hydrogen-safety modules become standard, solution breadth, not roller power alone, will determine share gains in the evolving China chassis dynamometer market.

China Automotive Chassis Dynamometers Industry Leaders

HORIBA Ltd.

Jiangsu Lanmec Technology Co., Ltd.

AVL List GmbH

Mustang Dynamometer

AA4C Automotive Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: COSBER began serial production of a 4WD synchronous dynamometer for EV discharge-simulation tests.

- March 2024: ZF Group outlined plans to lift Asia-Pacific sales share from 25% to 30% by 2030, backed by incremental Chinese R&D expenditure.

China Automotive Chassis Dynamometers Market Report Scope

| Two-Wheel Drive |

| Four-Wheel Drive |

| All-Wheel Drive |

| Powertrain Testing |

| Emissions Testing |

| Fuel Efficiency Analysis |

| Electric and Autonomous Component Testing |

| Research and Development |

| Others |

| OEMs |

| Aftermarket |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| By Product Type | Two-Wheel Drive |

| Four-Wheel Drive | |

| All-Wheel Drive | |

| By Application | Powertrain Testing |

| Emissions Testing | |

| Fuel Efficiency Analysis | |

| Electric and Autonomous Component Testing | |

| Research and Development | |

| Others | |

| By End-User | OEMs |

| Aftermarket | |

| By Propulsion Type | Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| Fuel-Cell Electric Vehicles |

Key Questions Answered in the Report

What is the current value of the China chassis dynamometer market?

The market is valued at USD 160.43 million in 2025 and is projected to reach USD 218.36 million by 2030.

How fast is demand for all-wheel-drive dynamometers growing?

All-wheel-drive rigs are forecast to experience an 8.11% CAGR through 2030 as electric SUVs and premium models proliferate.

Which end-user segment buys the most chassis dynamometers in China?

OEM laboratories hold 55.53% of spending and are expanding fastest at an 8.73% CAGR because they are internalizing electric-powertrain testing.

Why are AI-enabled digital-twins important in dynamometer testing?

Digital-twin models combined with machine learning achieve 99% fault-diagnosis accuracy and reduce development cycles, making them integral to modern lab setups.

What supply-chain risks affect dynamometer delivery schedules?

Restrictions on rare-earth magnets and volatility in precision-roller steel extend lead times by up to six months and can raise project costs.

Which propulsion type shows the strongest growth potential?

Fuel-cell-electric vehicles post a 7.67% CAGR, driven by government support for hydrogen mobility pilots in logistics and public transport.

Page last updated on: