Japan Automotive Chassis Dynamometers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

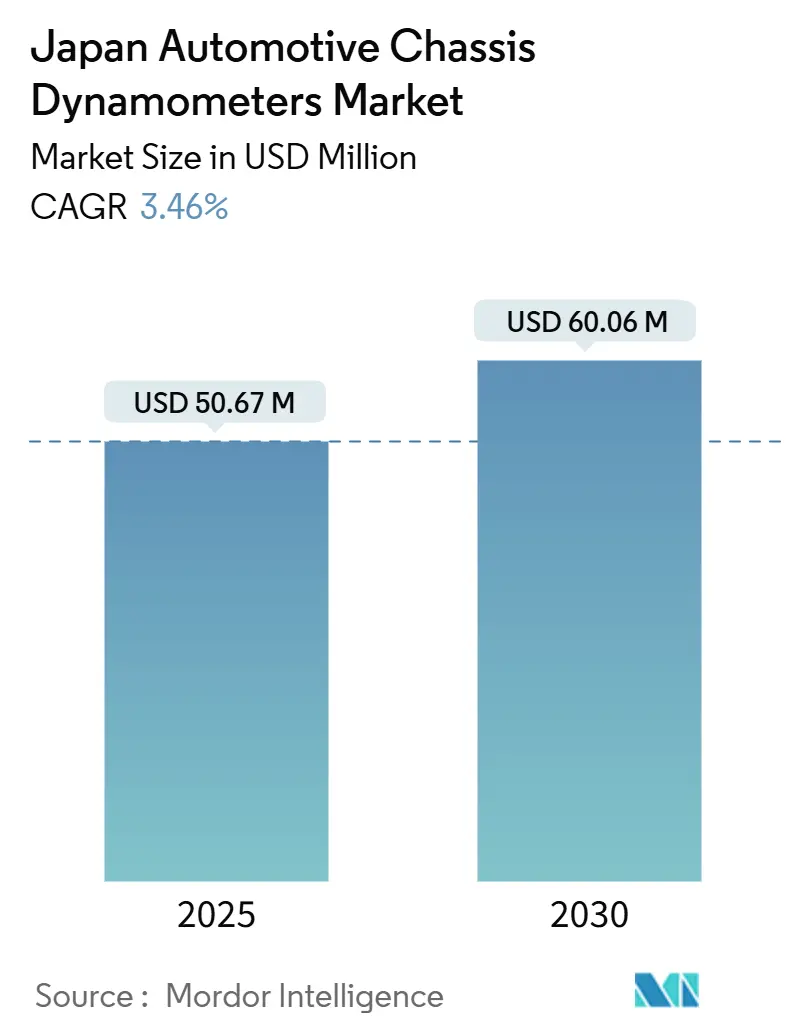

| Market Size (2025) | USD 50.67 Million |

| Market Size (2030) | USD 60.06 Million |

| Growth Rate (2025 - 2030) | 3.46% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Automotive Chassis Dynamometers Market Analysis by Mordor Intelligence

The Japan automotive chassis dynamometers market size stood at USD 50.67 million in 2025 and is forecast to expand to USD 60.06 million by 2030, registering a 3.46% CAGR over the period. This outlook reflects the country’s steady pivot toward electrified mobility while upholding exacting compliance protocols that oblige laboratories, OEMs, and service centers to modernize their chassis test equipment. Electrification now dominates propulsion-system validation requirements, autonomous-driving development is reshaping test-cell specifications, and government subsidies for diagnostic upgrades are lowering adoption barriers for smaller workshops. At the same time, capital intensity, space constraints in metropolitan prefectures, and ongoing semiconductor bottlenecks temper the growth trajectory of the Japan automotive dynamometer testing systems market. Consolidation pressures remain evident as established instrument suppliers expand integrated software-defined test solutions that couple chassis dynamometers with real-time simulation and data analytics platforms.

Key Report Takeaways

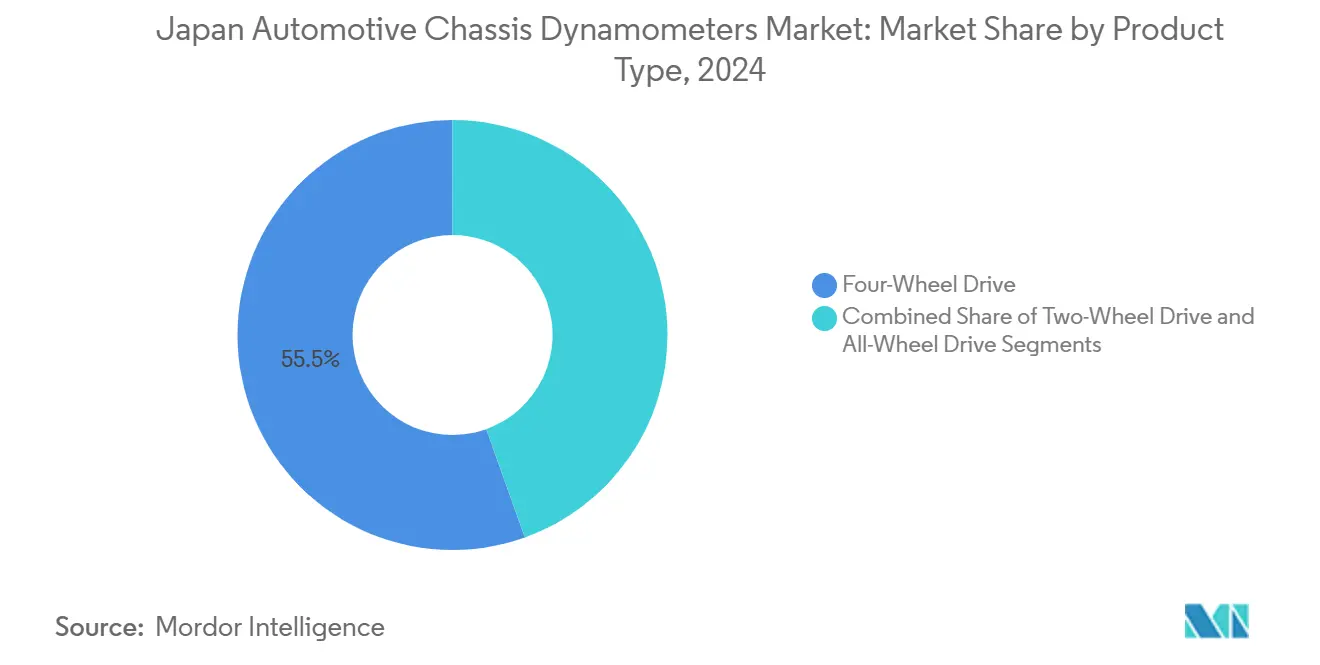

- By product type, four-wheel-drive chassis systems led with a 55.48% revenue share in 2024, while all-wheel-drive configurations are projected to advance at a 7.97% CAGR through 2030.

- By application, emissions testing held 38.18% of Japan automotive dynamometer testing systems market share in 2024; electric and autonomous component testing is projected to rise at a 7.76% CAGR during the forecast window.

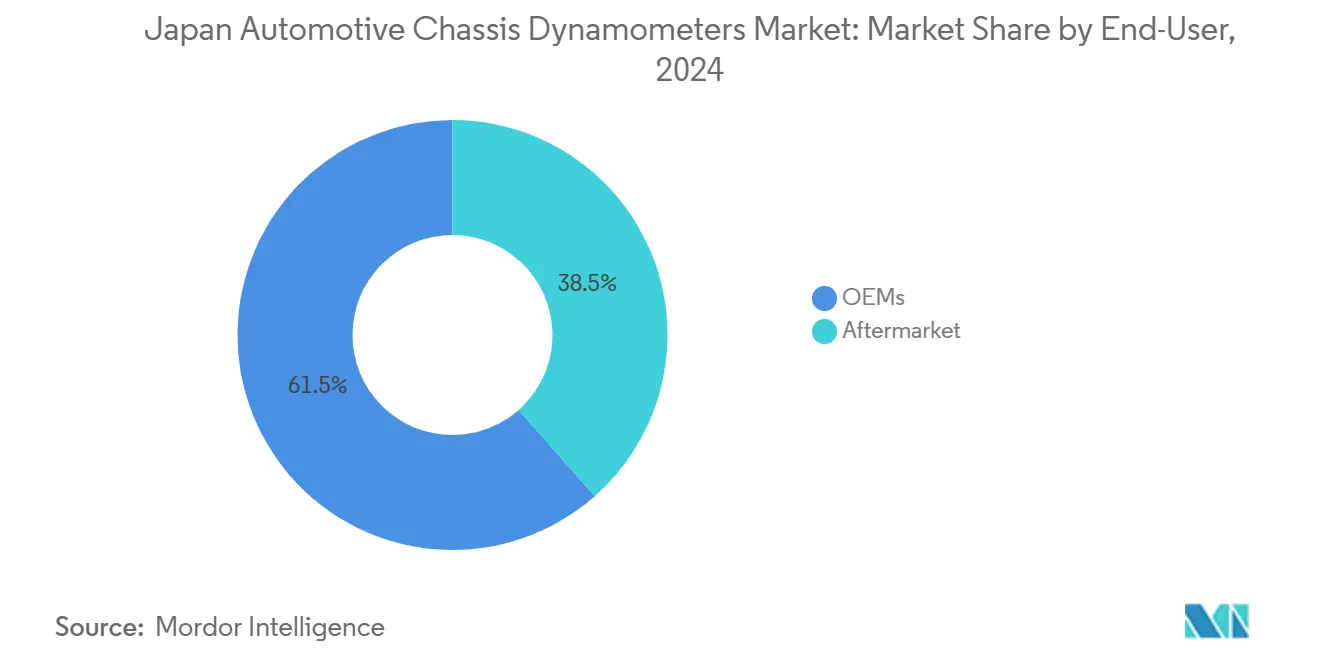

- By end-user, OEM laboratories controlled 61.51% of spending in 2024, yet the aftermarket is expected to log the fastest growth at a 6.94% CAGR to 2030.

- By propulsion type, battery-electric vehicles accounted for 44.93% of test-cell demand in 2024 and are projected to exhibit the highest 5.72% CAGR outlook to 2030.

Japan contributes to a system defined not by any single country or region but by the interaction of many. The global automotive chassis dynamometers market data by Mordor Intelligence represents that combined structure.

Japan Automotive Chassis Dynamometers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| WLTP/WLTC and JC08 Compliance | +1.2% | Tokyo, Osaka, Aichi, Kanagawa | Medium term (2-4 years) |

| Multi-Axle Testing Need | +0.9% | Tokyo, Aichi, Kanagawa, Shizuoka | Long term (≥ 4 years) |

| Mandatory Shaken Inspections | +0.7% | National, concentrated in Tokyo, Osaka, Aichi | Short term (≤ 2 years) |

| Subsidy For 2025 OBD/Scan-Tool | +0.5% | National, early adoption in Tokyo, Kanagawa | Short term (≤ 2 years) |

| Autonomous-Driving Road-Test Approvals | +0.4% | Tokyo, Kanagawa, Aichi, Shizuoka | Long term (≥ 4 years) |

| Hydrogen-Mobility R&D Programs | +0.3% | Fukuoka, Aichi, Tokyo, Kanagawa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter WLTP/WLTC & JC08 Compliance Push

Japan’s phased migration from 10-15 mode to JC08 and subsequently to WLTP protocols has compelled laboratories to invest in higher-precision dynamometers that replicate real-world inertia and aerodynamic loads. The Ministry of Land, Infrastructure, Transport and Tourism enforces weight-class-specific road-load determination procedures that favor suppliers possessing advanced calibration expertise. Older test cells calibrated for legacy cycles are therefore being replaced by systems capable of seamless switching between JC08H, JC08C, and WLTC phases. Compliance requirements extend to detailed data-logging capabilities, driving repeat equipment upgrades as reporting formats evolve. The result is a durable baseline of replacement demand within the Japan automotive dynamometer testing systems market[1]Ministry of Land, Infrastructure, Transport and Tourism, “Automotive Specific Maintenance System,” mlit.go.jp.

Electrification-Driven Need for Multi-Axle Testing

All-wheel-drive battery-electric architectures deliver high instantaneous torque to independent axles, creating a validation gap for traditional single-roller rigs. Dual-axis dynamometers allow synchronized control of front and rear rollers, enabling torque-vectoring, regenerative-braking, and energy-recuperation studies under repeatable laboratory conditions. Japanese manufacturers deploying e-axle units now specify torque capacities approaching 3,000 N·m per roller, prompting a clear migration toward multi-axle rigs with integrated power-absorption buffers. This specification shift positions the Japan automotive dynamometer testing systems market for sustained premium-system demand through decade-end.

Mandatory Shaken Inspections Expand Aftermarket Demand

The Japanese Shaken inspection system, conducted every two years, requires testing of exhaust emissions, speedometer accuracy, and headlight alignment. This mandatory inspection system creates steady demand for portable and basic dynamometer systems across approximately 90,000 automotive service locations in Japan, which must maintain compliance-grade testing equipment. From April 2025 owners may present vehicles up to two months before expiration, smoothing capacity utilization yet retaining aggregate test volumes. Portable simplified chassis dynamometers with DC-motor virtual inertia modules have become the standard aftermarket solution for smaller bays, boosting unit sales among equipment integrators focused on the Japan automotive dynamometer testing systems market.[2]Genichi Uno, "Will households have more leeway and after-sales service be improved? What impact will the revised vehicle inspection system have on users?" JAF Mate Online, jafmate.jp

Government Subsidy for 2025 OBD/Scan-Tool Upgrades

A national subsidy offering up to JPY 160,000 per workshop covers one-third of hardware and training costs for OBD inspection compliance. The first-come, first-served program runs to January 2026 and encourages rural garages to modernize electronic-control diagnostics, indirectly stimulating chassis dynamometer upgrades that interface with these scan tools. Coupled with “Monozukuri” SME productivity grants, the scheme improves cash flow for smaller establishments and enlarges the addressable aftermarket for the Japan automotive dynamometer testing systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cap-Ex and Retrofit Costs | -0.8% | Tokyo, Osaka, Kanagawa, Aichi | Medium term (2-4 years) |

| Space Constraints for Large Dyno Cells | -0.6% | Tokyo, Osaka, Kanagawa, Yokohama | Long term (≥ 4 years) |

| Shift To On-Road RDE Testing | -0.4% | National, early adoption in Tokyo, Aichi | Medium term (2-4 years) |

| Servo-Drive and Semiconductor Shortages | -0.3% | National, supply chain centered in Tokyo | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex & Facility Retrofit Costs

The installation of comprehensive dynamometer systems requires significant capital investment, particularly for advanced multi-axle systems that incorporate sophisticated control systems and precision components. A dual-axis high-speed chassis dynamometer system, equipped with a 250 kW regenerative absorber, climate chamber, and automation software, typically costs over USD 4 million to install. The retrofitting of urban buildings requires reinforced foundations, upgraded switchgear, and new ventilation ducts, which increases project costs. Small private laboratories frequently postpone equipment purchases, which constrains the growth of the Japan automotive dynamometer testing systems market.

Urban Space Constraints for Large Dyno Cells

Japan's metropolitan prefectures rank among the world’s most expensive real-estate markets. Modern chassis dynamometer systems require substantial floor space for proper vehicle positioning, safety clearances, and auxiliary equipment placement, creating spatial constraints that are particularly acute in Tokyo and Osaka metropolitan regions. Test-cell footprints of 150 m², plus blast-proof walls and fire-suppression systems, remain challenging to integrate within multistory buildings. Some operators relocate to suburban industrial parks, trading proximity for space, which prolongs project timelines and raises logistics costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Four-Wheel-Drive Systems Dominate Electric Testing

Four-wheel-drive rigs captured 55.48% of Japan automotive dynamometer testing systems market share in 2024. Their relevance stems from the industry shift toward torque-vectoring hybrids and battery-electric vehicles that split power across two axles. The Japan automotive dynamometer testing systems market size for four-wheel-drive units is projected to expand steadily as OEMs introduce dual-motor SUVs aimed at family and light-commercial segments.

Two-wheel-drive benches still serve legacy ICE models and cost-sensitive workshops but are gradually ceding share. All-wheel-drive systems, engineered for 4 × 4, dual-motor, and torque vectoring applications, represent the fastest-growing subcategory at a 7.97% CAGR. Suppliers are integrating higher-bandwidth torque meters and slip-control algorithms to capture complex traction events during regenerative braking.

By Application: Emissions Testing Leads, Electric Component Testing Surges

Emissions testing retained 38.18% of the Japan automotive dynamometer testing systems market size in 2024, anchored by statutory WLTP conformity for every passenger car type-approval. However, testing of electric and autonomous components is growing at a CAGR of 7.76%, mirroring the country’s electrification roadmap toward 100% electrified sales by 2035. Powertrain efficiency mapping and fuel-economy evaluation remain vital for hybrid vehicles, while research-and-development laboratories increasingly demand climatic chambers, acoustic treatments, and hardware-in-the-loop interfaces.

Suppliers are bundling battery cyclers and inverter test stands with chassis rigs to provide turnkey solutions that shorten prototype cycles. The demand for autonomous component testing systems is increasing in Japan as manufacturers advance their Level 4 autonomous driving development. The Ministry of Economy, Trade and Industry's (METI) planned demonstration experiments in 2025 require advanced laboratory simulation capabilities to validate safety standards.

By End-User: OEMs Lead, Aftermarket Growth Accelerates

OEM laboratories held 61.51% of the 2024 revenue in the Japan automotive dynamometer testing systems market. This dominance stems from their continuous vehicle development activities, production conformity audits, and end-of-line quality checks. These facilities invest in comprehensive testing cells that include emissions benches, climatic conditioning systems, and high-speed data acquisition capabilities.

The aftermarket segment, representing 38.49% of the market in 2024, is growing at a 6.94% CAGR, driven by Shaken inspection requirements and OBD regulations. Independent garages are adopting compact dynamometer systems with cloud-based diagnostics. This trend has encouraged the development of modular roller beds that require minimal foundation work and integrate with vehicle scan-tool workflows.

By Propulsion Type: Battery-Electric Vehicles Drive Testing Innovation

Battery-electric vehicles accounted for 44.93% of test-cell demand in 2024 and are projected to grow at a CAGR of 5.72% through 2030. The Japanese automotive dynamometer testing systems market for BEV validation includes thermal-runaway tests, regenerative-braking energy-recovery cycles, and high-torque repeatability trials. Hybrid electric vehicles and fuel cell electric vehicles require specialized testing protocols to validate their dual-power systems and hydrogen fuel cells.

Hybrid vehicles need blended propulsion load cycles, while fuel-cell vehicles require humidified intake air and high-purity exhaust capture. Internal combustion engine vehicles continue to dominate testing volumes but show declining growth as manufacturers shift investments toward electrification. The Japanese government's clean energy vehicle subsidies of 129.1 billion yen in FY2024 are driving increased electric vehicle adoption and their testing requirements.

Geography Analysis

Tokyo, Aichi, Kanagawa, and Osaka prefectures collectively held the majority of installations in 2024, driven by dense clusters of OEM headquarters, regulatory agencies, and tier-one suppliers. Tokyo’s research corridor hosts flagship verification centers that anchor capital-region demand for the Japan automotive dynamometer testing systems market. Aichi, home to the nation’s largest automaker, exhibits the fastest growth trajectory through 2030 as ongoing 300 billion yen investments at the Technical Center Shimoyama stimulate ancillary test-equipment purchases[3]Toyota Motor Corporation, “Toyota Completes Toyota Technical Center Shimoyama Research and Development Facility for Making Ever-Better Cars,” global.toyota.

Kanagawa and Shizuoka prefectures contribute substantial throughput via supplier ecosystems specializing in electrified powertrain modules, while Osaka serves as the western hub for aftermarket equipment distribution. Urban density in Tokyo and Osaka forces several new cells to relocate to outlying industrial estates where floor-space costs are lower, extending project lead times but enabling larger-format roller beds capable of accommodating long-wheelbase vans and light trucks.

Fukuoka is emerging as a strategic hydrogen-mobility node backed by METI’s Green Growth Fund, attracting fuel-cell component trials that demand explosion-proof dynamometer bays. Kyushu’s broader electronics supply chain further supports battery-pack and inverter testing operations, diversifying regional demand beyond the traditional Chubu-Kanto core. Overall, the Japan automotive dynamometer testing systems market continues to follow vehicle-production footprints, yet policy-driven technology clusters are incrementally redistributing investment toward newer prefectural hubs.

The automotive chassis dynamometers market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe. This is complemented by country-specific insights for South Korea, China, India, and United States, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The competitive arena is highly concentrated. The dominance of the top players arises from decades-long expertise in emissions analysis, mechatronics, and real-time simulation, all of which are essential for modern chassis-dynamometer integration. The latest flagship facility, opened in Kyoto in April 2025, exemplifies how leading vendors combine high-capacity roller beds with energy-management and cloud-analytics layers to slash cycle-time and utility consumption.

Mid-tier competitors pursue collaborative strategies to fill technology gaps. A May 2025 partnership pairs a mechanical-bench specialist with a simulation-software firm to develop vehicle-in-the-loop benches for autonomous-driving inspections. Such alliances broaden portfolios without the capital burden of in-house R&D and illustrate how the Japan automotive dynamometer testing systems market rewards modular, software-centric innovation.

Acquisition activity is also reshaping the field. An April 2025 deal saw a power-measurement instrumentation company acquire an Austrian data-logging specialist, expanding capabilities in high-frequency, multi-channel capture suited to electric-motor inverter validation. Market entrants focusing on portable vibration or NVH meters are carving out niches in maintenance diagnostics, yet the high-cap-ex nature of full-scale dynamometer cells continues to deter widespread fragmentation. Intellectual-property depth, after-sales service infrastructure, and deep customer relationships thus remain decisive competitive moats across the Japan automotive dynamometer testing systems market.

Japan Automotive Chassis Dynamometers Industry Leaders

-

HORIBA Ltd.

-

Meidensha Corporation

-

A&D Company Ltd.

-

AVL Japan K.K.

-

Ono Sokki Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Meitetsu Automotive Maintenance, Aisan Technology, and A-Drive signed an agreement to establish unified service standards for Level 4 autonomous-vehicle upkeep.

- May 2025: Ono Sokki Co., Ltd. launched the VW-3100, a portable three-axis vibration meter, aimed at real-time diagnostics in manufacturing plants.

- May 2025: Equipment makers, MAHA and dSPACE, formed a partnership to build vehicle-in-the-loop benches that merge chassis dynamometers with autonomous-driving simulation environments.

- April 2025: HORIBA opened its Vehicle Test Cell facility in Kyoto with integrated emissions, energy-consumption, and component-evaluation stations designed for multi-energy powertrains.

Japan Automotive Chassis Dynamometers Market Report Scope

| Two-Wheel Drive |

| Four-Wheel Drive |

| All-Wheel Drive |

| Powertrain Testing |

| Emissions Testing |

| Fuel Efficiency Analysis |

| Electric and Autonomous Component Testing |

| Research and Development |

| Others |

| OEMs |

| Aftermarket |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| By Product Type | Two-Wheel Drive |

| Four-Wheel Drive | |

| All-Wheel Drive | |

| By Application | Powertrain Testing |

| Emissions Testing | |

| Fuel Efficiency Analysis | |

| Electric and Autonomous Component Testing | |

| Research and Development | |

| Others | |

| By End-User | OEMs |

| Aftermarket | |

| By Propulsion Type | Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| Fuel-Cell Electric Vehicles |

Key Questions Answered in the Report

How large is the Japan automotive dynamometer testing systems market in 2025?

The market is valued at USD 50.67 million in 2025 and is forecast to reach USD 60.06 million by 2030 at a 3.46% CAGR.

Which product category holds the largest share of test-cell demand?

Four-wheel-drive chassis dynamometers lead with 55.48% of revenue thanks to electrified vehicles requiring independent axle testing.

What is the fastest-growing application area?

Electric and autonomous component testing posts the highest 7.76% CAGR as laboratories validate batteries, inverters, and ADAS functions.

Why is aftermarket demand rising in Japan?

Mandatory Shaken inspections and new OBD requirements are prompting independent garages to purchase compliance-grade chassis dynamometers and diagnostic tools.

Which propulsion type drives future equipment upgrades?

Battery-electric vehicles generate the strongest outlook, claiming 44.93% of current demand and expanding at a 5.72% CAGR through 2030.

How concentrated is supplier competition?

The top five vendors command about 81% of sales, indicating a high concentration that favors firms with integrated test-and-simulation portfolios.

Page last updated on: