South Korea Automotive Chassis Dynamometers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 13.35 Million |

| Market Size (2030) | USD 16.67 Million |

| Growth Rate (2025 - 2030) | 4.54% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Automotive Chassis Dynamometers Market Analysis by Mordor Intelligence

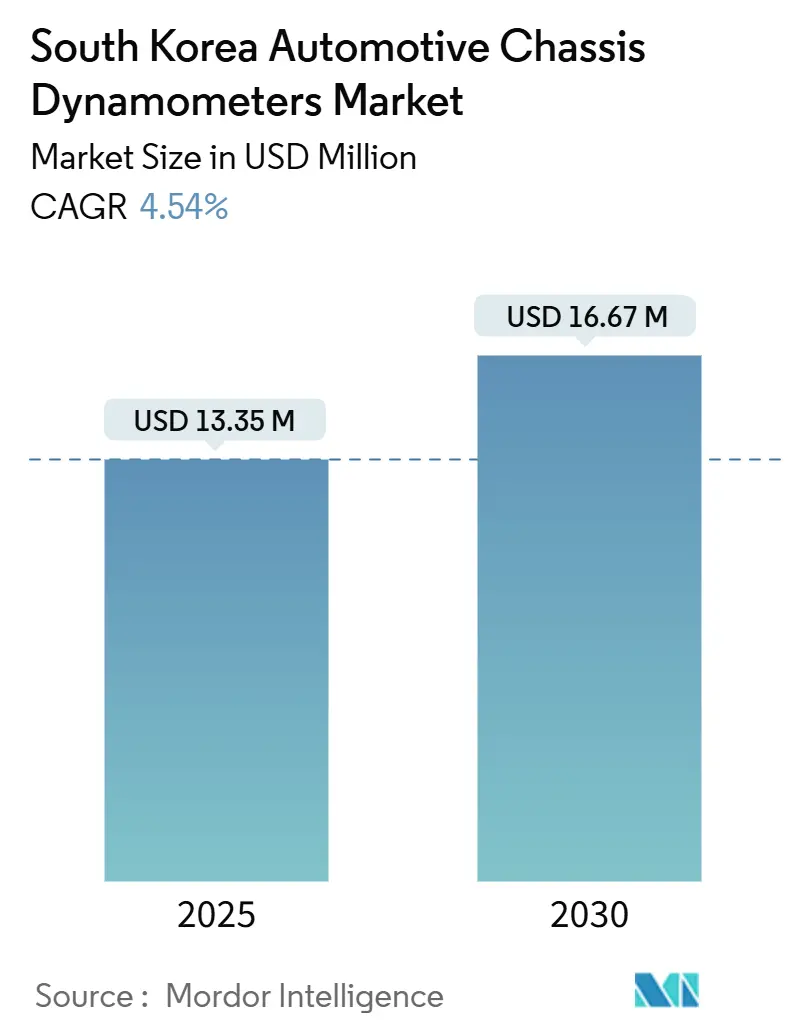

The South Korea automotive chassis dynamometers market size stands at USD 13.35 million in 2025 and is poised to reach USD 16.67 million by 2030, advancing at a 4.54% CAGR over the forecast period. This steady expansion reflects ongoing modernization of the nation’s testing ecosystem amid tightening emissions norms, rapid electrification, and rising demand for high-precision validation. Stringent Euro-6d and K-RDE regulations are compelling local automakers to upgrade legacy test benches, while escalating electric-vehicle (EV) penetration is amplifying the need for battery-to-wheel efficiency measurements. New product launches and larger R&D footprints by Hyundai and Kia are anchoring equipment demand, and global suppliers are enriching their South Korean presence through acquisitions and joint programs. At the same time, capital-intensive multi-axle rigs and digital-twin simulation options create a nuanced investment calculus that tempers absolute growth.

Key Report Takeaways

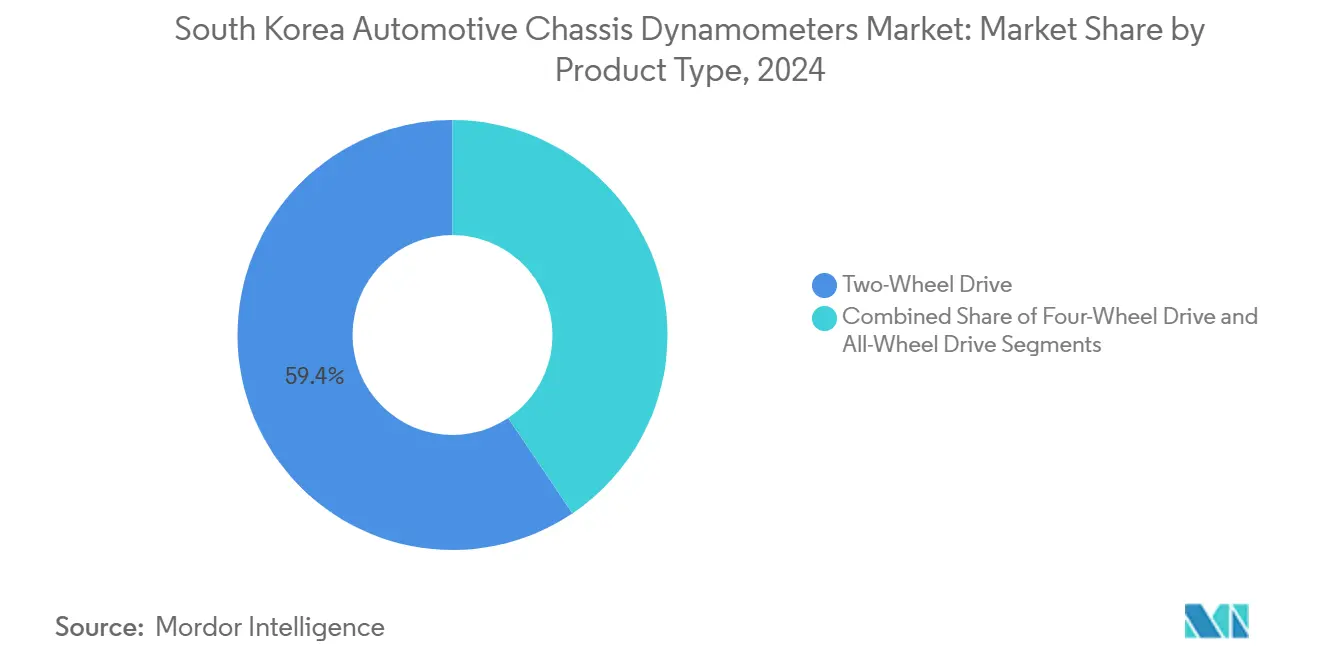

- By product type, Two-Wheel Drive systems commanded 59.42% of the South Korea automotive dynamometer market share in 2024, while All-Wheel Drive rigs are projected to expand at a 5.84% CAGR to 2030.

- By application, emissions testing held 47.13% revenue share of the South Korea automotive dynamometer market size in 2024; electric and autonomous component testing is forecast to surge at a 16.67% CAGR through 2030.

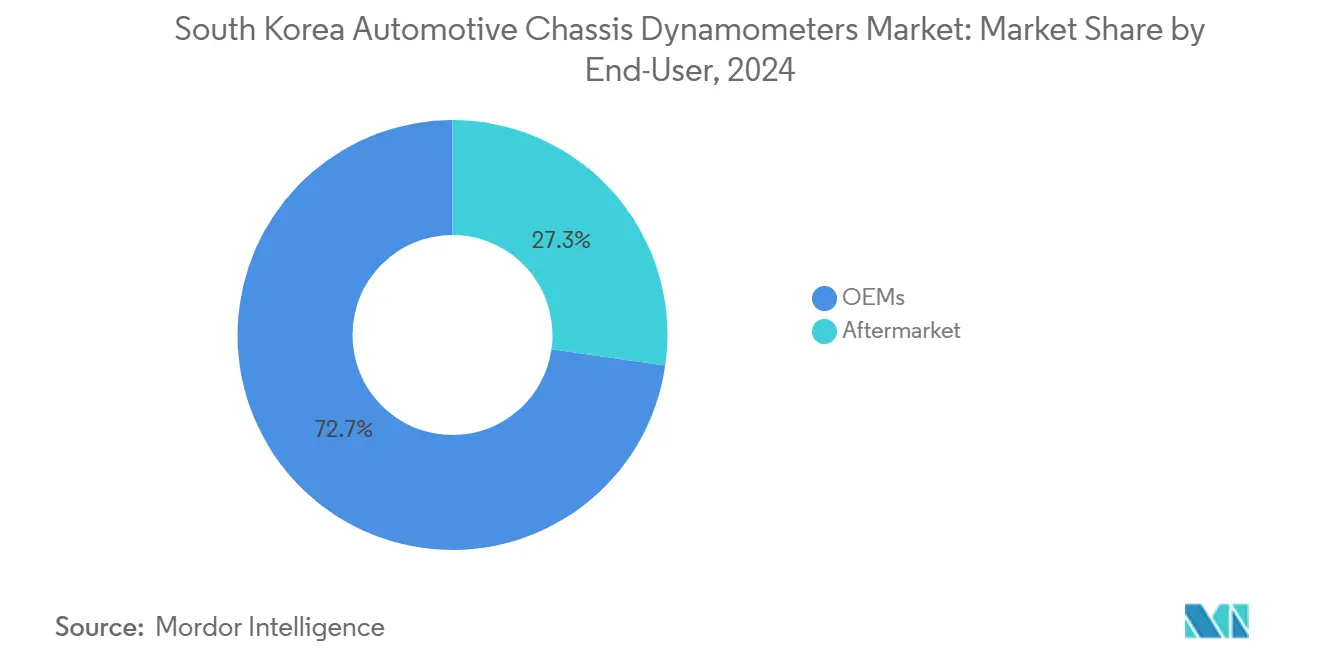

- By end-user, OEM facilities controlled 72.74% share of the South Korea automotive dynamometer market in 2024, whereas the aftermarket is registering the quickest rise at a 6.76% CAGR over the outlook period.

- By propulsion, internal-combustion programs accounted for 63.52% of the South Korea automotive dynamometer market size in 2024; battery-electric validation is set to lead with a 15.24% CAGR to 2030.

Future direction is shaped by developments occurring across multiple countries and regions, with South korea contributing to the overall trajectory. The outlook on worldwide automotive chassis dynamometers market reflects how these are expected to evolve collectively.

South Korea Automotive Chassis Dynamometers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Euro-6d and K-RDE Emissions Mandates | +1.1% | Seoul, Gyeonggi, Ulsan, Busan | Short term (≤ 2 years) |

| Autonomous Vehicle Rollout | +0.9% | Ulsan, Gyeonggi, Seoul | Medium term (2-4 years) |

| R&D Facility Expansion | +0.7% | Ulsan, Gyeonggi, Chungcheong | Medium term (2-4 years) |

| Digital-Twin Correlation | +0.5% | Seoul, Gyeonggi, Daejeon | Long term (≥ 4 years) |

| Battery-to-Wheel Efficiency Labs | +0.5% | Chungcheong, Gyeonggi, Ulsan | Medium term (2-4 years) |

| Hydrogen FCEV Certification Subsidies | +0.4% | Ulsan, Gyeonggi, Seoul | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Euro-6d and K-RDE Emissions Mandates

Regulatory alignment with the European Union has raised precision requirements for exhaust measurement and introduced on-road verification, forcing test centers to adopt chassis dynamometers capable of replicating real-driving emissions cycles. Field studies show that many late-model diesel cars exceed laboratory NOx limits during urban operation, underscoring the urgency of more representative load profiles. Manufacturers are therefore installing higher-resolution torque transducers, faster transient control loops, and integrated particulate analyzers to close the lab-to-road gap. As compliance audits tighten in Seoul and provincial fleets, demand for dual-axis and climate-conditioned cells is rising, cementing a multi-year growth runway for premium dynamometers.

Electrification and Autonomous Vehicle Rollout

Government plans to deploy 4.2 million EVs by 2030 and expand the public charger base five-fold require robust validation of electric drivetrains, regenerative braking, and battery durability. Hyundai’s USD 1.5 billion EV-dedicated plant in Ulsan, scheduled for 2026 start-of-production, exemplifies the scale of local capacity additions. Autonomous programs hosted at test beds such as K-City further necessitate hardware-in-the-loop interfaces that link vehicle sensors to real-time load machines. As software-defined vehicles become mainstream, suppliers that can mesh dynamometer data streams with digital-twin models stand to capture outsized share of incremental spend.[1]Korean-German Energy Partnership Team, "Battery Electric Vehicles for the Provision of Short-Term Flexibility", energypartnership-korea.org

OEM R&D Facility Expansion in Korea

South Korea’s leading automakers are reorganizing their engineering divisions to accelerate next-generation platform development. The creation of advanced vehicle-platform groups and newly announced electrification research centers has concentrated procurement of chassis, engine, and e-motor dynamometers inside Ulsan and Gyeonggi clusters[1]. Clustered demand allows suppliers to streamline service networks, yet it also intensifies competitive bidding on customized rigs, software integration, and long-term maintenance contracts.

Digital-Twin Correlation Need for Virtual Validation

Local electronics firms have reported 40% productivity improvement after pairing physical measurements with simulation models, prompting automakers to seek similar efficiencies in vehicle development. Dynamometer vendors are consequently embedding open data protocols and high-speed cloud gateways that feed virtual environments in near real time. Such capabilities lower prototype counts and shorten test cycles, translating into recurring service revenues for equipment suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex of Multi-axle Dynos | -0.7% | Seoul, Gyeonggi, Ulsan | Short term (≤ 2 years) |

| Powertrain-in-the-loop Substitutes | -0.5% | Seoul, Gyeonggi, Daejeon | Medium term (2-4 years) |

| Urban Lab Space Constraints | -0.5% | Seoul, Busan, Incheon | Short term (≤ 2 years) |

| Skilled Operator Shortage | -0.4% | Ulsan, Gyeonggi, Chungcheong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cap-ex of Multi-axle High-speed Dynos

The substantial capital investment requirements for advanced multi-axle dynamometer systems are creating significant barriers to market expansion, costing well above USD 3 million, excluding building retrofits and emission analyzers. The high depreciation rates and technical obsolescence risks associated with rapidly evolving testing standards further compound the capital expenditure burden. Smaller laboratories struggle to justify these outlays, especially as depreciation schedules shorten due to rapid software updates. Financial incentives have therefore become pivotal for sustaining the South Korea automotive dynamometer market amid rising technical thresholds.

Rise of Powertrain-in-the-loop Substitutes

The emergence of sophisticated simulation technologies and powertrain-in-the-loop (PIL) testing methodologies is creating competitive pressure on traditional dynamometer applications. Simulation suites capable of modeling driveline loads with high fidelity are being adopted during early design phases, trimming physical test hours. South Korean companies' increasing adoption of digital twin technologies is demonstrated by LG Innotek's integration with Ansys for virtual simulations. Although regulations still require final chassis validation, the shift to virtual workflows reduces total dyno cell-hours and pressures suppliers to pivot toward hybrid testing solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: AWD Systems Drive Premium Testing

The AWD sub-segment is forecast to register a 5.84% CAGR, outpacing the mature 2WD category that nevertheless sustains 59.42% of the South Korea automotive dynamometer market share. Demand stems from sport-utility and premium sedan platforms that rely on torque-vectoring and complex energy-recovery strategies. High-end rigs featuring synchronized roller sets and rapid acceleration gradients attract pricing premiums of 30% compared with dual-roller 2WD benches.

Within the South Korea automotive dynamometer market size for product types, manufacturers are upgrading existing 2WD lines with modular hardware to accommodate future AWD conversions, safeguarding asset utilization. Growth in AWD also reflects export priorities. Korean automakers ship a rising portion of all-wheel models to North America and Northern Europe, where weather and performance preferences reinforce the AWD mandate. As duty cycles diversify to include snow-load profiles, test routines require broader tractive-effort envelopes, lifting uptake of variable-inertia flywheel stacks and active cooling systems.

By Application: Electric Testing Accelerates Beyond Emissions

Emissions testing still anchors expenditure because Euro-6d and K-RDE compliance demands high-precision chassis cells, giving the segment 47.13% revenue weight in 2024. Laboratories are upgrading roller accuracy, transient torque control, and gas-analysis suites to pass tightening spot audits in Seoul and Ulsan. Yet growth momentum is shifting toward electric and autonomous component validation, which is projected to climb 16.67% a year as automakers roll out 800-V drivetrains and advanced driver-assistance features. The technical leap from passive exhaust capture to bi-directional power absorption and real-time sensor feeds is prompting a wave of retrofit orders for battery-to-wheel rigs.

The new validation focus benefits suppliers that can integrate dynamometer data with model-based development and over-the-air update workflows. Demand for thermal-management chambers, regenerative-braking duty cycles, and high-speed CAN gateways is strongest in Gyeonggi, where software-defined-vehicle teams iterate rapidly on control logic. Autonomous pilots at K-City are also driving purchases of low-inertia hub dynos capable of replicating micro-speed maneuvers. As EV volumes mount, emissions cells migrate to maintenance mode while electric test benches log extended utilization hours, lifting overall aftermarket service revenue.

By End-User: Aftermarket Gains as OEMs Dominate

Original-equipment manufacturers (OEMs) controlled 72.74% of 2024 spend because vertically integrated R&D centers bundle powertrain, chassis, and durability labs on single campuses. Hyundai and Kia alone account for 90% of domestic vehicle output, so their multi-year upgrade programs shape baseline demand curves. Purchasing decisions emphasize turnkey delivery, software openness, and 24-hour onsite support, favoring global suppliers with deep local engineering benches. Capital allocations are now tilting toward electrification cells and hydrogen safety chambers, but legacy engine benches remain essential for export-bound nameplates.

The aftermarket, while smaller, is expanding 6.76% annually as contract-test houses, certification bodies, and university labs fill capability gaps for tier-2 suppliers. Shared facilities inside new industrial complexes in Chungcheong lower entry barriers by offering time-based leasing models on high-speed dynos. Independent operators differentiate through flexible scheduling, custom reporting, and pay-per-use software licenses that appeal to startups and component makers. Increasing regulatory audits of in-use vehicles are also boosting demand for periodic verification services, strengthening aftermarket growth prospects through 2030.

By Propulsion Type: BEV Testing Surges as ICE Stabilizes

nternal-combustion programs still dominate with 63.52% of 2024 revenue because gasoline and diesel engines underpin export contracts to regions where electrification trails domestic adoption. Test cells for ICE platforms focus on transient NOx reduction, turbocharger durability, and alternative-fuel blends, maintaining steady if flat purchase volumes. Regulatory certainty and proven workflows keep depreciation risk low, so many labs opt for refurbishment rather than new-build projects. Despite steadiness, ICE benches now share floor space with dual-purpose rigs designed for later conversion to electric modes.

Battery-electric vehicle (BEV) validation is the clear growth engine, forecast to sprint at 15.24% CAGR through 2030 as national targets call for 4.2 million EVs on the road. High-torque, low-rpm e-motors require dynamometers with wide constant-speed envelopes and millisecond-level control resolution. Cell makers’ battery-to-wheel efficiency labs in Gyeonggi and Ulsan are specifying sub-0.1% speed-accuracy hubs, driving premium pricing and longer service contracts. Parallel investment in hydrogen fuel-cell SUV programs adds niche demand for low-pressure hydrogen supply systems, although volumes remain modest relative to BEV ramp-ups.

Geography Analysis

Ulsan anchors the South Korea automotive dynamometer market with the nation’s largest cluster of assembly plants and R&D centers. The recently announced EV-dedicated facility is driving incremental orders for e-axle and environmental chambers. Suppliers often co-locate service depots nearby to guarantee sub-24-hour response times demanded by just-in-time production schedules. Local universities collaborate with industry on joint calibration projects, further deepening regional expertise.

Gyeonggi Province functions as the nation’s engineering backyard. Proximity to Seoul’s design studios enables agile iteration between software teams and physical test cells, while favorable tax incentives have lured several tier-1 component makers. Upcoming battery parks and semiconductor fabs generate spillover demand for power-electronics dynamometers and precision wafer-test equipment. The provincial government’s mobility-cluster blueprint envisions dedicated lanes for autonomous pilots, adding an edge-case validation requirement that benefits high-speed hub dynos[2]Invest Korea, “Korea’s Future Car Industry, Continual Growth by Actively Responding to Domestic and Global Changes,” investkorea.org.

A third growth pole is emerging across Chungcheong, where a 550,000 m² industrial complex will host shared labs tailored to small and mid-size suppliers. Coupled with a USD 4.6 million electromagnetic-interference chamber in neighboring Cheongju, the region is positioning itself as a specialist node for sensor-fusion and ADAS calibration. Such diversification eases capacity bottlenecks in congested coastal metros and spreads employment gains inland.

Analysis of the automotive chassis dynamometers market by Mordor Intelligence spans multiple other regional evaluations across Europe, supported by country-level insights for Japan, India, China, and United States, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Global incumbents command the high-end of the market through broad portfolios, proven safety credentials, and strong Korean engineering teams. HORIBA deepened its local footprint by acquiring wafer-inspection firm EtaMax in April 2025, extending reach into power-semiconductor quality control for EV inverters. AVL leverages early-mover advantage in electrified-drivetrain testing and turnkey lab builds that integrate hardware-in-the-loop software. MAHA specializes in high-throughput chassis rolls for inspection stations and dealership service lanes.

Competition now centers on software integration, data-analytics add-ons, and lifecycle service. Vendors with open APIs that sync physical measurements to digital-twin platforms win bids from software-defined-vehicle teams in Gyeonggi. Subscription-based maintenance, remote calibration, and operator-training packages are replacing one-time hardware sales as key profit drivers. Local machine builders are entering niche segments such as compact hub dynos for university research, but steep certification requirements limit rapid scaling.

Strategic alliances with automakers and battery firms are intensifying. Suppliers co-develop specialized rigs, such as 800-V e-axle benches or hydrogen leak-detection chambers, to secure multi-year service agreements. Government grants aimed at hydrogen and autonomous validation favor companies willing to localize production of safety enclosures and high-speed actuators. Although price sensitivity exists in the aftermarket, customization needs and stringent accreditation keep margins resilient for established players.

South Korea Automotive Chassis Dynamometers Industry Leaders

-

HORIBA Ltd.

-

AVL List GmbH

-

MAHA Maschinenbau Haldenwang GmbH

-

Mustang Dynamometer

-

Power Test LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: MINI Korea launched “Proactive Care,” a remote diagnostics service that analyzes vehicle data and schedules preventive maintenance actions.

- April 2025: HORIBA completed the acquisition of EtaMax Co., expanding its portfolio into compound-semiconductor wafer inspection, a critical enabler for high-efficiency EV power modules.

- January 2024: Hyundai Motor and Kia overhauled their R&D organization, creating the Advanced Vehicle Platform Division to accelerate software-defined vehicle programs.

South Korea Automotive Chassis Dynamometers Market Report Scope

| Two-Wheel Drive (2WD) |

| Four-Wheel Drive (4WD) |

| All-Wheel Drive (AWD) |

| Powertrain Testing |

| Emissions Testing |

| Fuel-Efficiency Analysis |

| Electric and Autonomous Component Testing |

| Research and Development |

| Others |

| OEMs |

| Aftermarket |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| By Product Type | Two-Wheel Drive (2WD) |

| Four-Wheel Drive (4WD) | |

| All-Wheel Drive (AWD) | |

| By Application | Powertrain Testing |

| Emissions Testing | |

| Fuel-Efficiency Analysis | |

| Electric and Autonomous Component Testing | |

| Research and Development | |

| Others | |

| By End-User | OEMs |

| Aftermarket | |

| By Propulsion Type | Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| Fuel-Cell Electric Vehicles |

Key Questions Answered in the Report

How large is the South Korea automotive dynamometer market in 2025?

The market stands at USD 13.35 million in 2025.

What is the expected CAGR for South Korean dynamometers through 2030?

The market is projected to expand at a 4.54% CAGR.

Which product configuration is growing the fastest?

All-Wheel Drive systems lead with a projected 5.84% CAGR.

Why is electric-component testing gaining momentum?

Rapid EV adoption and stringent battery-efficiency targets are driving a 16.67% CAGR in this application segment.

Which region generates the highest demand for dynamometers?

Ulsan, home to Hyundai’s main complex and a new EV plant, represents the largest demand hub.

Page last updated on: