Europe Automotive Chassis Dynamometers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

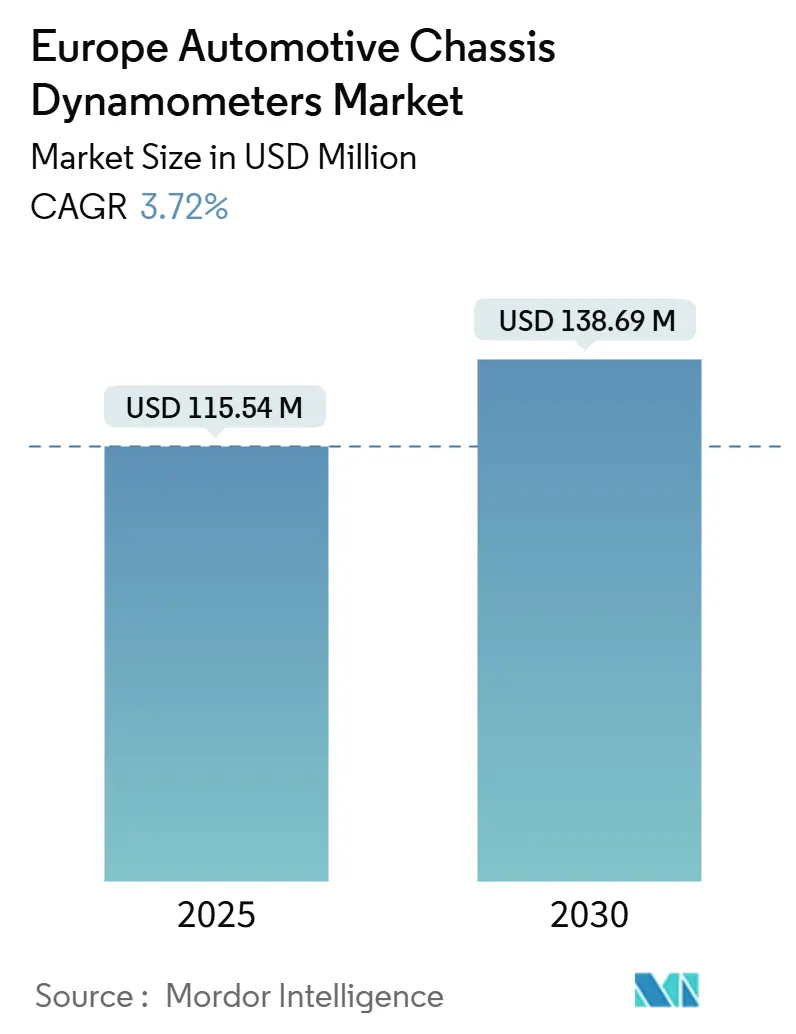

| Market Size (2025) | USD 115.54 Million |

| Market Size (2030) | USD 138.69 Million |

| Growth Rate (2025 - 2030) | 3.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Chassis Dynamometers Market Analysis by Mordor Intelligence

The European automotive chassis dynamometer market size is USD 115.54 million in 2025 and is on course to reach USD 138.69 million by 2030, expanding at a 3.72% CAGR during the forecast period. The European automotive chassis dynamometer market is transitioning from conventional power-train validation toward integrated electrification and automation testing as Euro 7 deadlines approach, electric vehicle (EV) launches accelerate, and original-equipment manufacturers (OEMs) demand real-driving-emissions verification. Investments in low-inertia dynamometers, cloud-linked analytics, and hardware-in-the-loop interfaces underscore growing emphasis on software-defined vehicle architectures. Energy-price volatility inflates laboratory operating expenses, yet stringent regulatory compliance and a widening EV model pipeline ensure stable capital outlays for new test cells. Germany’s manufacturing dominance and sustained R&D budgets anchor regional demand, while fast-growing economies such as the Netherlands spur incremental opportunities for agile technology suppliers across the European automotive chassis dynamometer market.

Key Report Takeaways

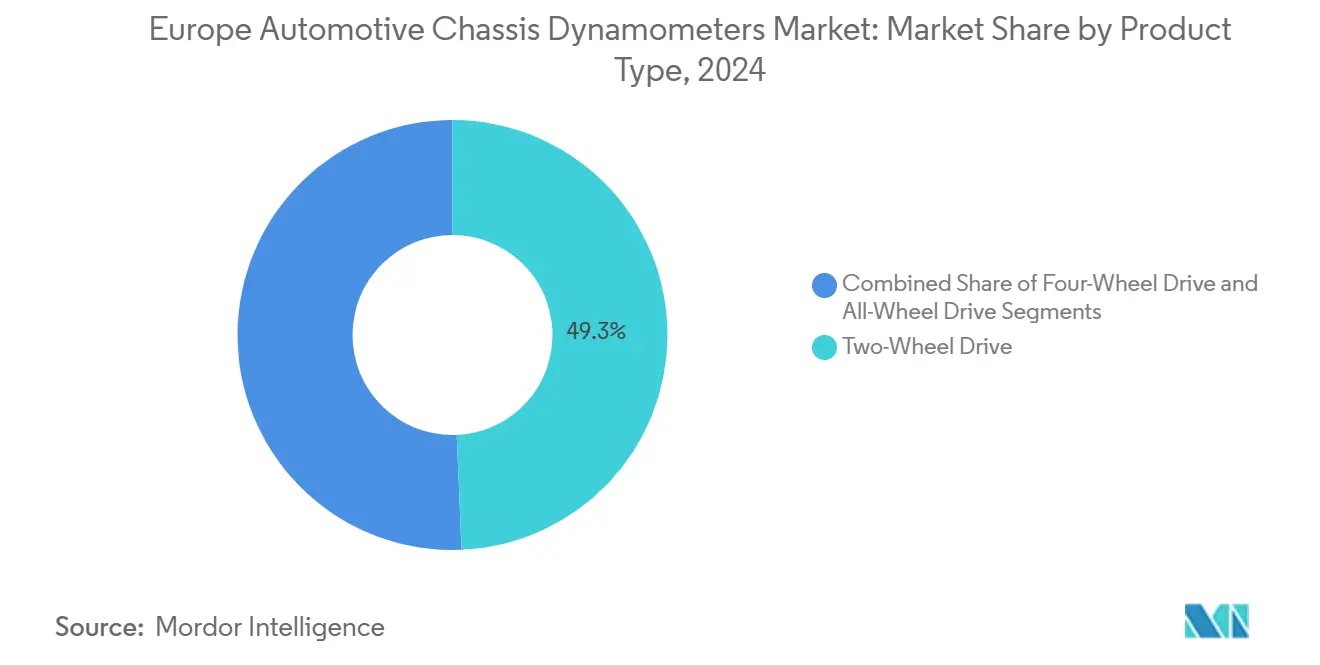

- By product type, two-wheel drive systems held 49.33% of the European automotive chassis dynamometer market share in 2024, while all-wheel drive configurations are forecast to expand at a 4.54% CAGR to 2030.

- By application, emissions testing accounted for a 35.82% share of the European automotive chassis dynamometer market size in 2024 and electric & autonomous component testing is advancing at a 16.09% CAGR through 2030.

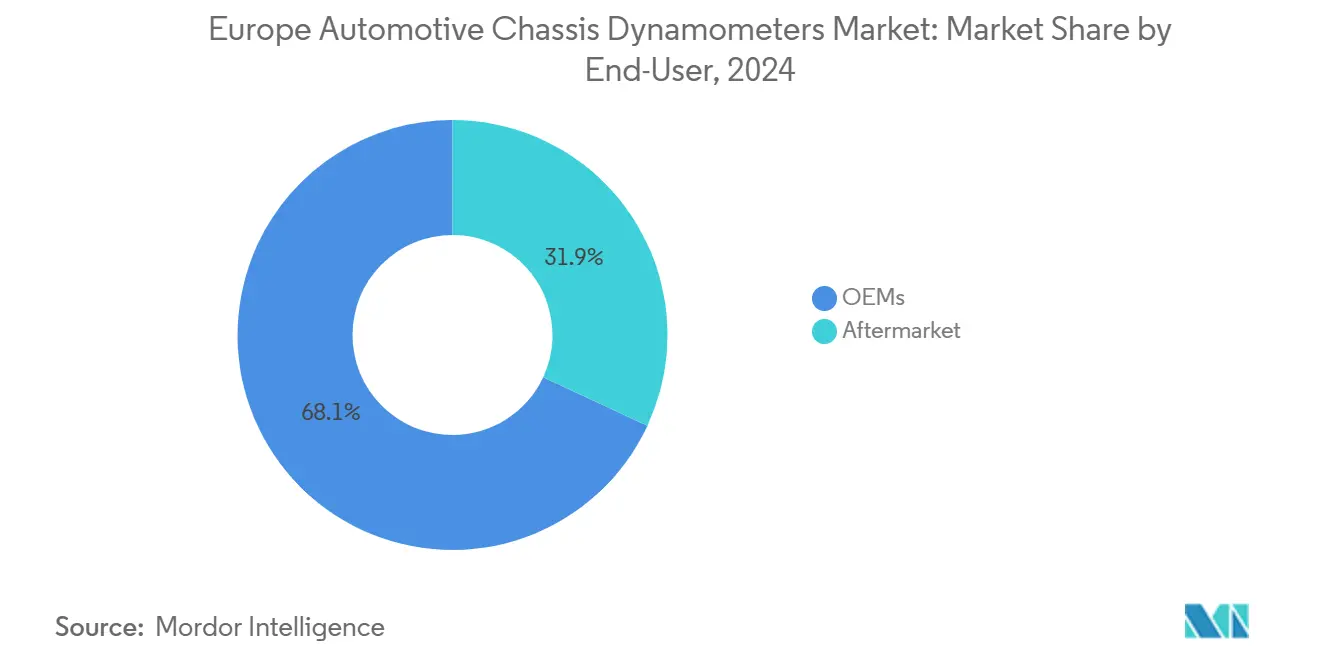

- By end-user, OEMs led with 68.06% revenue share in 2024; the aftermarket segment records the highest projected CAGR at 3.63% to 2030.

- By propulsion type, internal-combustion vehicles captured 58.34% of the European automotive chassis dynamometer market share in 2024, whereas battery-electric vehicles are set to grow at a 14.42% CAGR between 2025-2030.

- By country, Germany commanded 41.04% revenue share in 2024, while the Netherlands is forecast to post the fastest 4.85% CAGR through 2030.

Competitive positioning in Europe includes both locally based firms and those operating across multiple regions. The market landscape in the global automotive chassis dynamometers industry research shows how these players are arranged internationally.

Europe Automotive Chassis Dynamometers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Euro 7 and WLTP Compliance Deadlines | +1.3% | Germany, France, Italy, Spain, Netherlands | Medium term (2-4 years) |

| EV/HEV Model Launches | +1.1% | Germany, Netherlands, France, UK | Short term (≤ 2 years) |

| In-House R&D Lab Expansion | +0.7% | Germany, UK, Spain, Italy | Long term (≥ 4 years) |

| Outsourced Testing Demand | +0.6% | Germany, France, Netherlands, Spain | Medium term (2-4 years) |

| Cloud-Linked Dyno Analytics | +0.4% | Germany, Netherlands, UK, France | Long term (≥ 4 years) |

| Low-Inertia Dynos | +0.3% | Germany, Netherlands, France, UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Euro 7 and WLTP Compliance Deadlines

The November 2026 Euro 7 start date for new vehicle types compels OEMs and suppliers to install high-precision chassis dynamometers that can validate 8-year/160,000 km durability and real-driving-emissions metrics[1]European Parliament, “Development of Euro 7 Emission Standards for Cars, Vans, Lorries and Buses,” europarl.europa.eu. Laboratories must integrate enhanced data-acquisition hardware to meet on-board-monitoring and battery-durability verification needs. Germany’s automakers are allocating a large share of the EUR 320 billion 2025-2029 R&D budget to test-cell modernization[2]Verband der Automobilindustrie, “VDA-Präsidentin Müller fordert Mentalitäts- und Politikwechsel,” vda.de. Tier-1 suppliers face identical validation obligations, widening the European automotive chassis dynamometer market addressable base. WLTP protocol complexity favors facilities with certified metrology talent, reinforcing demand for advanced dynamometers throughout the European automotive chassis dynamometer market.

Surge in EV/HEV Model Launches and Test-Cell Upgrades

European battery-electric registrations in Germany rose significantly in January 2025, driving rapid retrofits of existing test cells to accommodate regenerative-brake, thermal-management, and power-electronics assessments. HORIBA’s Vehicle Test Cell platform combines emissions, energy-consumption, and component validation in a single cycle, signaling the new benchmark for integrated solutions. Hybrid validation multiplies complexity by requiring seamless transitions between combustion and electric modes. Simulation-center investments by automakers such as Škoda confirm escalating capital intensity and regulation-agnostic test design. As the European automotive chassis dynamometer market adapts, hardware-in-the-loop interfaces are becoming standard for assessing autonomous functions within power-train tests.

OEM In-House R&D Lab Expansion Programs

To protect intellectual property and shorten iteration loops, OEMs continue shifting validation in-house. New proprietary facilities equipped with multi-axle, low-inertia rigs accelerate Euro 7 certification, reduce third-party lead-times, and allow confidential work on next-generation battery-management algorithms. German groups account for the largest share of the EUR 320 billion R&D pipeline, although increasing overseas allocations raise concerns about domestic capacity utilization. Internal labs can compress development cycles by up to 30%, underpinning the European automotive chassis dynamometer market as OEMs enlarge captive testing networks across the continent.

Outsourced Testing Demand from Tier-1 Suppliers

Component manufacturers unwilling to invest EUR 3-5 million for all-wheel-drive cells opt for pay-per-use test centers offering certified compliance services. Independent providers supply cutting-edge cloud analytics and AI-driven automation, features unattainable for smaller suppliers. This outsourcing model optimizes capital deployment and grants access to multi-OEM platforms without compromising scalability, generating a parallel growth track inside the European automotive chassis dynamometer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX of AWD Chassis | -0.9% | Germany, UK, France, Italy | Short term (≤ 2 years) |

| Shrinking ICE Vehicle Pipeline | -0.7% | Germany, Spain, Italy, France | Medium term (2-4 years) |

| Energy-Price Volatility | -0.4% | Germany, Netherlands, UK, Spain | Short term (≤ 2 years) |

| WLTP-Certified Metrology Talent Scarcity | -0.4% | Germany, France, UK, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX of AWD Chassis Dynamometers

All-wheel-drive rigs cost EUR 3-5 million versus EUR 1-2 million for 2WD setups, deterring smaller facilities and delaying return-on-investment. Volatile European electricity prices, which have swung 40-60% since 2022, further strain budgeting accuracy[3]European Commission, “Report on Energy Prices and Costs in Europe,” eur-lex.europa.eu. Extended commissioning cycles and rapid power-train evolution make equipment obsolescence a genuine risk. These combined factors dampen procurement velocity in the European automotive chassis dynamometer market.

Shrinking ICE Vehicle Pipeline

With forecasts placing electric cars at 70% of new-car sales by 2030, legacy dynamometer capacity focused on combustion engines faces underutilization. Operators must support ICE programs during the sunset phase and simultaneously fund EV-specific upgrades, elevating fixed-cost burdens. The transition magnifies stranded-asset risk yet does not remove the need for emissions testing of hybrids, resulting in a complex capacity-planning puzzle across the European automotive chassis dynamometer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Demand Consolidates Around AWD Precision

Two-wheel drive units retained the largest 49.33% share of the European automotive chassis dynamometer market in 2024, a position rooted in the high volume of front-wheel-drive passenger cars. However, the European automotive chassis dynamometer market size for all-wheel-drive rigs is projected to expand at a 4.54% CAGR, reflecting premium EV platform proliferation, performance benchmarking, and traction-control algorithm validation.

Electric motors deliver instant torque and require dynamometers with tighter rotational-speed tolerance, faster response, and low inertia. Facilities such as Škoda’s 300 kW simulation center illustrate the trend toward high-speed, high-torque testing conditions. Four-wheel drive equipment still serves niche commercial and sports-car segments, but AWD’s technology requirements elevate average selling prices and catalyze software-defined enhancements like cloud-linked telemetry. Consequently, suppliers targeting the European automotive chassis dynamometer market focus R&D on scalable AWD architectures that preserve upgradability as EV power-train designs evolve.

By Application: Electrification Reorders Spending Priorities

Emissions testing retained a 35.82% share of the European automotive chassis dynamometer market size in 2024 because Euro 7 conformity assessments dominate near-term laboratory schedules. Yet electric & autonomous component validation is accelerating at a 16.09% CAGR, signaling a decisive pivot toward battery, inverter, and ADAS performance verification. Integrated test cells such as HORIBA’s facility capture simultaneous energy-consumption and emissions data, bridging ICE and EV requirements within the European automotive chassis dynamometer market.

Hardware-in-the-loop setups for radar and lidar validation require precise speed-synchronization between dynamometer rollers and virtual environments. Research & development applications benefit from cross-discipline convergence, compelling test-bench suppliers to offer modular platforms that address propulsion, thermal, and electronic systems in one environment. As electrification broadens, investments migrate from tailpipe emission analyzers toward high-voltage safety systems, regenerative-brake simulators, and battery-cycling add-ons.

By End-User: OEM Control Shapes Utilization Pattern

OEMs dominated with 68.06% revenue contribution to the European automotive chassis dynamometer market in 2024, mirroring their strategic choice to bring advanced validation in-house. Captive laboratories protect intellectual property, particularly battery-management software and fast-charging algorithms, while compressing development lead-times. The aftermarket and independent test-service segment grows at 3.63% CAGR as Tier-1s and smaller assemblers prefer variable-cost testing over fixed, high-CAPEX assets.

Providers differentiate via cloud dashboards, flexible vehicle-class coverage, and regulatory advisory expertise, ensuring their relevance within the European automotive chassis dynamometer market. OEM internalization remains capital-intensive, prompting some manufacturers to co-invest with academic or public-sector entities to share cost and talent pools. The coexistence of captive and outsourced models preserves healthy demand diversity for equipment vendors.

By Propulsion Type: Battery-Electric Acceleration Reconfigures Workloads

Internal-combustion vehicles still generated 58.34% of the European automotive chassis dynamometer market share in 2024, supported by the need to certify hybrid power-trains under Euro 7. The European automotive chassis dynamometer market size for battery-electric vehicle (BEV) testing is set to rise at a robust 14.42% CAGR as BEV registrations surge and drivetrain architectures standardize around multi-motor AWD layouts. BEV validation introduces unique requirements: regenerative-braking load reversal, battery-temperature conditioning, and high-torque launch simulations.

Hybrid electric modules further complicate profiles by toggling between engine and motor propulsion within a single cycle, demanding seamless control-strategy verification. Fuel-cell vehicles remain a small but sophisticated niche, necessitating hydrogen-safety enclosures and exhaust-water management. Collectively, shifting propulsion patterns compel testing centers to invest in versatile, software-upgradable rigs, sustaining momentum for suppliers active in the European automotive chassis dynamometer market.

Geography Analysis

Germany contributed 41.04% of revenue in 2024, underpinning the European automotive chassis dynamometer market through deep manufacturing, intensive R&D, and leadership in premium EV platforms. High-profile investments, such as EUR 650 million for BMW’s Munich EV conversion, coupled with federal-state funding for battery-cell research, ensure Germany remains the benchmark for advanced testing demand. The robust Tier-1 ecosystem likewise channels component-validation spending into domestic laboratories, reinforcing Germany’s anchor role in the European automotive chassis dynamometer market.

The Netherlands delivers the fastest 4.85% CAGR owing to its sustainability ethos and push for smart manufacturing that leverages additive techniques and AI-driven design. Dutch facilities favor energy-efficient dynamometers and circular-economy compliant procurement, setting a model that other mid-sized European states may emulate as they upgrade to Euro 7 standards. This policy-technology mix enlarges the regional footprint of the European automotive chassis dynamometer market while creating niches for modular, scalable solutions.

The United Kingdom, Spain, Italy, and France maintain mature, regulation-aligned testing capacities. The UK enhances climatic and high-voltage test coverage; Spain and Italy navigate energy-price volatility that elevates operating costs; France harnesses automotive-heritage competencies to preserve compliance leadership. The Rest-of-Europe cluster, including Sweden’s electromobility laboratory initiative, injects specialized demand for next-generation test environments. Collectively these geographies sustain balanced growth and margin resiliency within the broader European automotive chassis dynamometer market.

Mordor Intelligence tracks the automotive chassis dynamometers market with additional country-level coverage spanning China, Japan, India, United States, and South Korea, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The European automotive chassis dynamometer market is moderately concentrated. The top three suppliers—HORIBA Ltd, AVL List GmbH, and MAHA—collectively account for a significant share of installed-base revenue, a share founded on decades of combustion-engine expertise now repurposed for electrification. Barriers to entry include multimillion-euro R&D cycles, stringent accuracy certifications, and service-network breadth.

Competition centers on platform flexibility and data-analytics integration. HORIBA’s Vehicle Test Cell demonstrates a shift toward turnkey, software-centric solutions that minimize re-tooling between ICE and BEV programs. AVL leverages double-digit annual R&D allocations to introduce cloud-linked dynamometer controls that enable over-the-air calibration, while MAHA emphasizes mechanical robustness for high-torque commercial-vehicle evaluations.

Emerging entrants pursue low-inertia roller designs for regenerative-brake simulation and AI-guided test-sequence generation. White-space opportunities exist in modular, containerized test cells deployable to satellite R&D hubs, potentially lowering capital barriers for fast-growing EV startups. Supply-chain strategy therefore combines core electromechanical engineering with digital-service ecosystems, sustaining competitive dynamism inside the European automotive chassis dynamometer market.

Europe Automotive Chassis Dynamometers Industry Leaders

HORIBA Ltd

AVL List GmbH

MAHA Maschinenbau Haldenwang

Mustang Advanced Engineering

Taylor Dynamometer

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hyundai Motor Group expanded testing and R&D facilities at Nürburgring to accelerate EV and high-performance validation.

- July 2024: Cummins Inc. opened its Darlington power-train test facility featuring multi-energy dynamometers supporting Euro 7 and Stage 6 compliance.

Europe Automotive Chassis Dynamometers Market Report Scope

| Two-Wheel Drive |

| Four-Wheel Drive |

| All-Wheel Drive |

| Powertrain Testing |

| Emissions Testing |

| Fuel Efficiency Analysis |

| Electric and Autonomous Component Testing |

| Research and Development |

| Others |

| OEMs |

| Aftermarket |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| Germany |

| United Kingdom |

| Spain |

| Italy |

| France |

| Netherlands |

| Rest of Europe |

| By Product Type | Two-Wheel Drive |

| Four-Wheel Drive | |

| All-Wheel Drive | |

| By Application | Powertrain Testing |

| Emissions Testing | |

| Fuel Efficiency Analysis | |

| Electric and Autonomous Component Testing | |

| Research and Development | |

| Others | |

| By End-User | OEMs |

| Aftermarket | |

| By Propulsion Type | Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| Fuel-Cell Electric Vehicles | |

| By Country | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the European automotive chassis dynamometer market in 2025?

The market stands at USD 115.54 million in 2025.

What is the expected CAGR for European chassis dynamometers to 2030?

A CAGR of 3.72% is forecast through 2030.

Which country accounts for the largest share of demand?

Germany holds 41.04% of revenue in 2024.

Which product configuration is growing fastest?

All-wheel drive systems are projected to expand at a 4.54% CAGR.

Why are electric vehicles reshaping test-cell investments?

BEV validation needs regenerative-brake, thermal-management, and high-voltage safety testing, driving new equipment demand.

Page last updated on: