Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

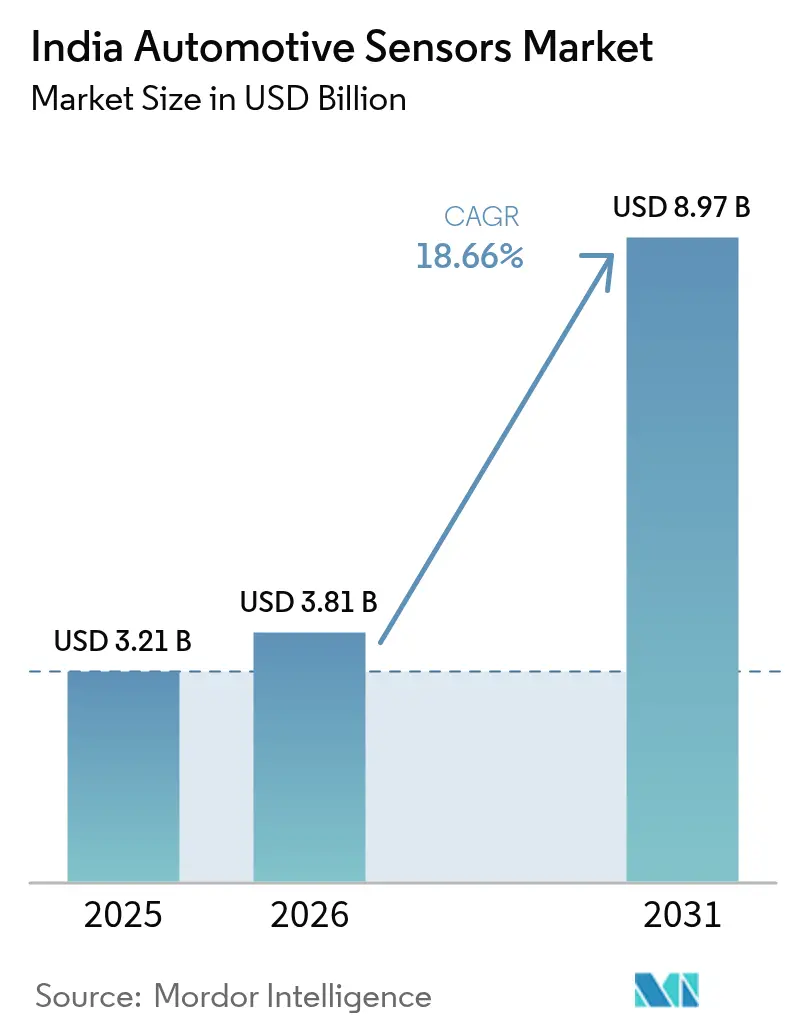

| Base Year Market Size (2025) | USD 3.21 Billion |

| Market Size (2026) | USD 3.81 Billion |

| Market Size (2031) | USD 8.97 Billion |

| Growth Rate (2026 - 2031) | 18.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Sensors Market Analysis by Mordor Intelligence

The India Automotive Sensors Market size was valued at USD 3.21 billion in 2025 and estimated to grow from USD 3.81 billion in 2026 to reach USD 8.97 billion by 2031, at a CAGR of 18.66% during the forecast period (2026-2031). Regulatory mandates, electrification of two- and three-wheelers, and supply-chain localization initiatives are together propelling the India automotive sensors market toward its strongest multi-year expansion on record. Steady enforcement of AIS-145 safety standards obliges OEMs to embed radar, camera, and pressure sensors across commercial and passenger platforms. Parallel growth in electric-vehicle production, led by two-wheeler volumes that grew significantly in FY2025, increases sensor content per vehicle by three-fifth. Government Production Linked Incentive (PLI) and SPECS programs encourage domestic MEMS fabrication, trimming landed costs and shortening lead times. Global suppliers, concerned about China-centric risk, have begun reallocating capital toward India, reinforcing the long-term competitiveness of the India automotive sensors market[1]“AIS-145 Automotive Standards Amendment,” Ministry of Road Transport & Highways, morth.gov.in.

Key Report Takeaways

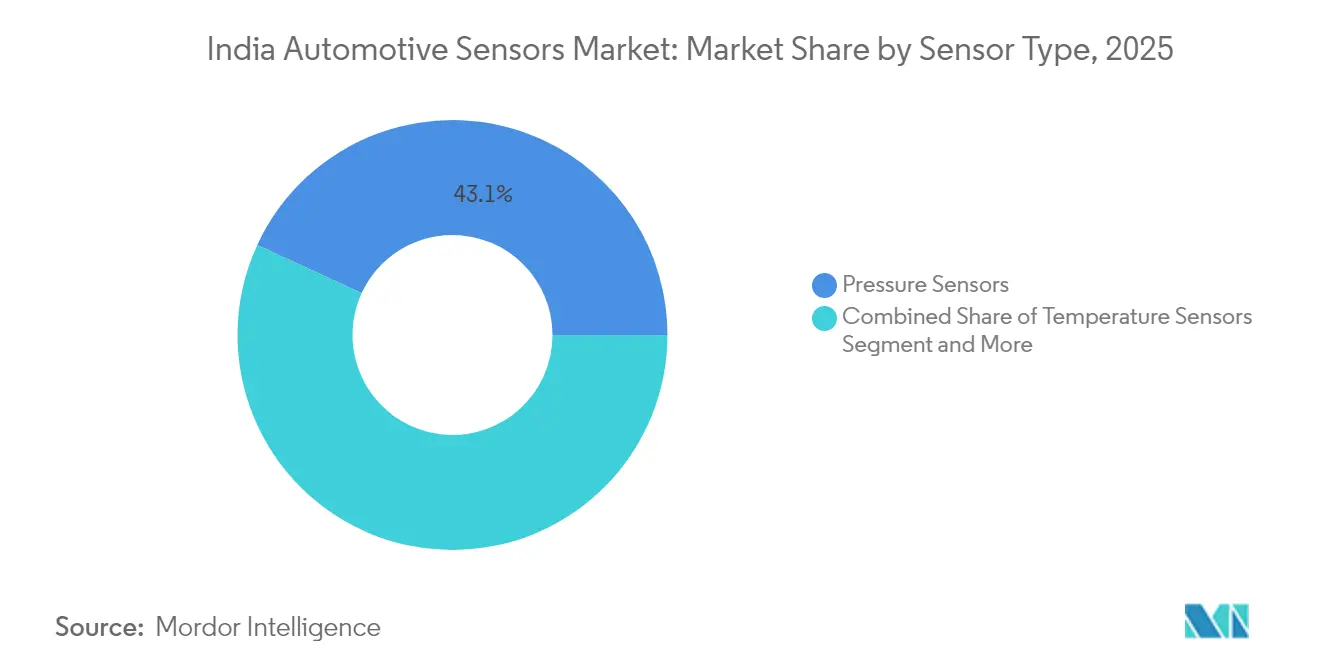

- By sensor type, pressure sensors captured 43.12% of the India automotive sensors market share in 2025, whereas electro-optical sensors are poised to grow at an 18.79% CAGR through 2031.

- By vehicle drivetrain, internal combustion engine vehicles held a 62.58% share of the India automotive sensors market in 2025, while electric vehicles registered the fastest 18.71% CAGR to 2031.

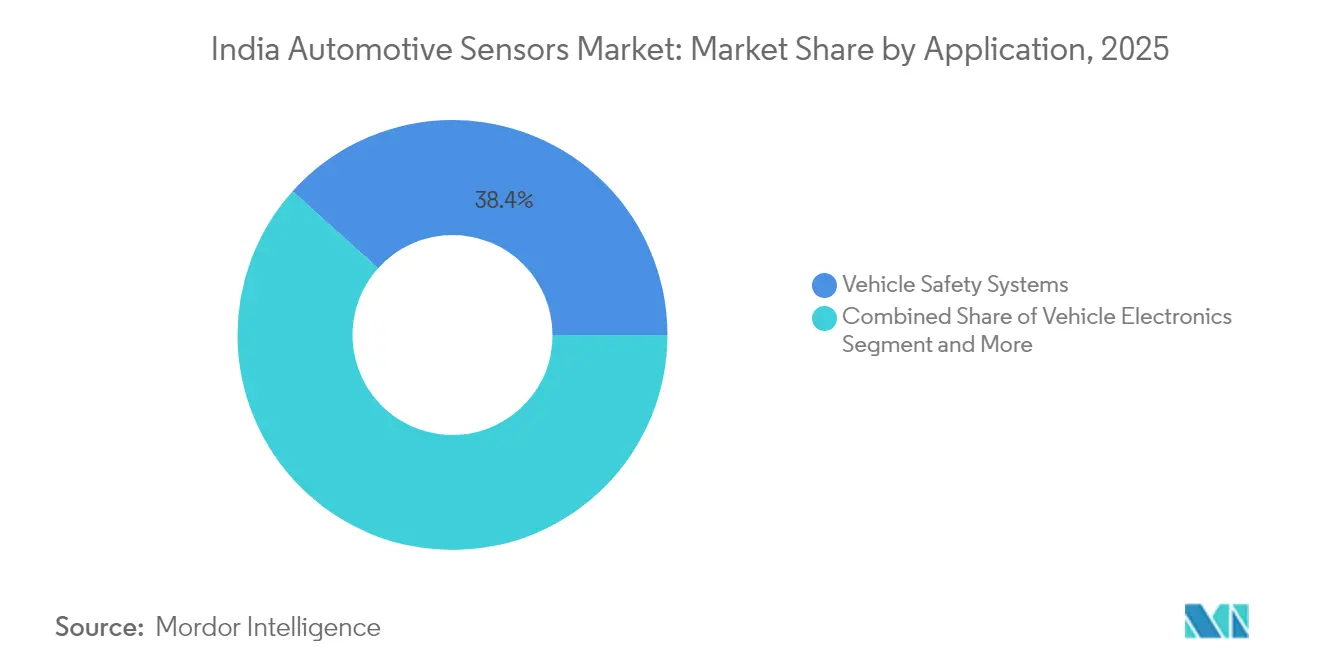

- By application, vehicle safety systems accounted for 38.35% of the India automotive sensors market share in 2025 and are advancing at an 18.74% CAGR through 2031.

- By vehicle type, passenger cars led with 56.72% of the India automotive sensors market share in 2025; two-wheelers are projected to expand at an 18.80% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Automotive Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory ADAS and TPMS Regulations | +4.2% | National, with early adoption in commercial vehicle segments | Medium term (2-4 years) |

| Rapid Electrification Of India's Two- & Three-Wheeler Fleet | +3.8% | National, concentrated in urban centers and delivery ecosystems | Short term (≤ 2 years) |

| PLI & SPECS Incentives | +2.9% | Manufacturing hubs in Gujarat, Tamil Nadu, Karnataka | Long term (≥ 4 years) |

| OEM-Led Shift To Domain/Zone E-E Architectures | +2.1% | Tier-1 cities and premium vehicle segments initially | Medium term (2-4 years) |

| Ultra-Low-Cost 8-Bit MCUs Enabling Sensor Fusion | +1.7% | National, targeting cost-sensitive passenger car segment | Short term (≤ 2 years) |

| Usage-Based-Insurance (UBI) Adoption | +1.4% | Urban markets with high insurance penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory ADAS & TPMS Regulations Post-AIS-145

Ministry of Road Transport and Highways (MoRTH) has proposed amendments to the Central Motor Vehicles Rules (CMVR), which obliges vehicles exceeding eight seats to integrate advanced emergency braking, lane departure, and driver-drowsiness warning systems from April 2026. Traditionally late adopters, commercial fleets must now deploy radar, camera, and inertial sensors across platforms. TPMS rules augment demand for wheel-mounted pressure sensors that generate a continuing aftermarket. The regulation coincides with a vehicle scrappage program that cycles older trucks out of service, accelerating new sensor uptake. Suppliers able to certify ISO 26262 compliance and functional-safety performance are likely to capture premium contracts.

Rapid Electrification of India’s Two- & Three-Wheeler Fleet

Electric two-wheeler sales surged to 1.14 million units in FY2025, and the segment now integrates up to 20 sensors per vehicle versus 8 in comparable ICE models. Battery-thermal, cell-voltage, and motor-position sensors dominate the bill of materials, while regenerative braking systems add torque and wheel-speed sensing. Three-wheelers accounted for more than half of new registrations in 2024, concentrating demand in urban last-mile networks. Price-sensitive OEMs favor domestically packaged MEMS devices to contain costs, spurring capacity additions at new Indian fabs.

PLI & SPECS Incentives Localising MEMS Sensor Production

Value-addition thresholds doubled to two-fifths, nudging global vendors to commit to clean-room investments. Micron and Tata’s chip projects promise a domestic supply of automotive-grade substrates. Local silicon-carbide development further lessens import dependence for high-temperature pressure and exhaust-gas sensors, strengthening the Indian automotive sensors market[2]“PLI Scheme Guidelines for Automobile and Auto Components,” Department for Promotion of Industry & Internal Trade, dpiit.gov.in .

OEM-Led Shift to Domain/Zone E-E Architectures

Continental and Infineon pilot zone-controller designs that aggregate inputs from up to 12 sensor domains, trimming wiring weight and cost. Centralized compute enables over-the-air updates that can unlock new sensor-driven features after sale. Infineon’s TRAVEO T2G MCU line supplies the processing bandwidth for real-time camera-radar fusion, positioning India as a development base for software-defined vehicles. Domestic tier-1s benefit through joint-engineering programs to tailor firmware to local road conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-Sensitive OEM Pricing | -2.8% | National, particularly affecting mass-market vehicle segments | Short term (≤ 2 years) |

| Lag In Tier-II Wafer-Level Packaging Capacity | -1.9% | Manufacturing clusters lacking advanced packaging infrastructure | Medium term (2-4 years) |

| Fragmented After-Sales Service Network | -1.5% | Rural and Tier-II/III cities with limited automotive service infrastructure | Long term (≥ 4 years) |

| Import Duties On Sensor-Grade Silicon Wafers | -1.2% | National, with higher impact on cost-sensitive domestic manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-Sensitive OEM Pricing and Razor-Thin Supplier Margins

Six leading automakers controlled the majority of domestic sales in FY2024, creating monopsony power that compels vendors to price sensors more than one-fifth below global averages. Electric models add 3–4 times more sensor content yet must hold retail prices flat to win mass-market acceptance. Higher logistics and energy costs render Indian parts costlier than Mexican equivalents, squeezing exporter profit. Sustained margin pressure limits R&D budgets, delaying next-generation sensor rollouts.

Lag in Tier-II Wafer-Level Packaging Capacity

India’s focus on front-end fabs leaves a gap in automotive-grade back-end assembly and testing. Dependence on Southeast Asian OSAT plants extends lead times by up to 20 days and inflates landed costs by one-tenth. Import duties on specialty substrates elevate BOM prices, and capacity clashes with smartphone sensors during demand spikes. Without rapid packaging expansion, the Indian automotive sensors industry faces supply-chain exposure that could curtail near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Pressure Sensors Lead Despite Electro-Optical Surge

Pressure sensors dominated the India automotive sensors market in 2025 with a 43.12% share, largely due to mandatory TPMS adoption and widespread engine-management use cases. This legacy base ensures steady volume even as electric powertrains add battery-coolant monitoring and brake-pressure sensing. Electro-optical sensors, including cameras and infrared modules, log the fastest 18.79% CAGR through 2031 as ADAS features cascade into mid-segment models. Temperature and speed sensors continue incremental gains tied to Bharat Stage VI emission control and anti-lock braking mandates.

Electromagnetic devices capture share through proximity and position applications such as e-axle monitoring and automated parking assist. Emerging inertial and gas sensors populate the “other” category, where cabin-air-quality and vehicle-dynamics functions highlight rising customer expectations. Domestic players like Sona Comstar now prototype short-range radar for blind-spot detection, underlining India’s shift from commodity sensing to advanced perception modules within the India automotive sensors market.

By Vehicle Drive-Train: ICE Dominance Yields to EV Momentum

Internal-combustion platforms held 62.58% of India automotive sensors market size in 2025, buoyed by established fueling infrastructure and slower rural electrification. Electric vehicles lead growth at an 18.71% CAGR as two- and three-wheelers proliferate in cities. EVs integrate three-fifths more sensors per unit, spanning battery voltage, pack temperature, and high-voltage isolation monitoring. Hybrid variants, though niche, layer both ICE and EV sensing, representing the most complex bill of materials.

ICE vehicles nonetheless sustain high sensor content through particulate-filter monitoring and advanced fuel-injection control demanded by BS-VI norms. As charging networks widen and battery prices fall, OEMs project EV volumes to top one-fifth of new registrations by 2030, creating a structural pivot for suppliers focused on drivetrain-specific sensors within the India automotive sensors market.

By Application: Safety Systems Drive Growth Across All Segments

Safety-system installations accounted for 38.35% of India automotive sensors market size in 2025 and are set to post an 18.74% CAGR to 2031. Radar, camera, ultrasonic, and driver-monitoring units underpin emergency braking and lane-keeping functions stipulated under AIS-145. Engine and drivetrain uses retain significant volume through exhaust-gas, knock, and transmission sensors that remain mandatory across ICE and hybrid fleets.

Vehicle electronics applications spanning infotainment, HVAC, and body electronics grow steadily as usage-based insurance and telematics platforms demand additional motion and environmental sensing. Emerging predictive maintenance and cabin wellness features further diversify sales channels, ensuring that sensor suppliers serve multiple value pools within the Indian automotive sensors market.

By Vehicle Type: Passenger Cars Lead While Two-Wheelers Accelerate

Passenger cars delivered 56.72% of the India automotive sensors market share in 2025 due to higher per-vehicle sensor counts and growing premiumization. Two-wheelers register the fastest 18.80% CAGR, reflecting electrification and adoption of safety tech such as ABS and TPMS in scooters and motorcycles. Light-commercial-vehicle uptake benefits from e-commerce logistics, while heavy trucks integrate ADAS and telematics for fleet efficiency.

Two-wheeler electrification compels OEMs to integrate battery-management and motor-position sensors previously absent from low-cost models. Marquardt’s domestic battery-BMS rollout illustrates vendor adaptation to this swift shift in the India automotive sensors market.

Geography Analysis

Concentration in Tamil Nadu, Karnataka, Gujarat, and Maharashtra anchors the India automotive sensors market, supported by OEM hubs in Chennai, Bengaluru, Pune, and Sanand. These clusters supply both domestic and export demand, with total vehicle output growing drastically in 2024. State-level incentives such as Tamil Nadu’s EV policy and Gujarat’s semiconductor subsidies accelerate sensor adoption by reducing capex for tier-1 suppliers.

Second-tier regions, including Telangana and Andhra Pradesh, are courting investments through land-cost rebates and power-tariff concessions. Localization under the Atmanirbhar Bharat initiative enabled crores of substitution of imports in 2024, though a simultaneous rise in high-value electronic imports underscores ongoing reliance on foreign wafer fabrication. Export competitiveness is improving, with component shipments targeted to grow exponentially by 2030.

The India Semiconductor Mission’s placement of advanced fabs in Gujarat and Assam promises upstream supply security for sensor manufacturers. Closer material sources lower logistics cost and cut cycle times, making the India automotive sensors market attractive for global design wins. Urban aftermarket demand clusters in Delhi-NCR, Mumbai, and Bengaluru ensure broad geographic distribution of service revenue streams.

Competitive Landscape

The India automotive sensors market shows moderate concentration: multinational leaders dominate high-tech niches, while local firms compete in volume segments. Bosch, Continental, DENSO, and Infineon employ global R&D assets to deliver radar, lidar, and 3-axis MEMS gyros that meet ISO 26262 and ASIL-B/C levels. Simultaneously, they localize packaging and calibration to pare down costs for mass-segment cars.

Domestic contenders such as Awesense Five and Axiro Semiconductor enter with cost-optimized pressure and temperature sensors, leveraging PLI benefits to narrow the technology gap. Strategic partnerships are multiplying: Infineon is evaluating wafer-fab collaboration with Tata Group, and Continental is co-developing zone-controller firmware with Indian engineering centers. Suppliers differentiate through speed-to-market, price tiers, and functional-safety certification, forging a two-tier structure across the India automotive sensors market.

White-space opportunities arise in telematics and predictive-maintenance sensors, where telecom carriers and SaaS providers seek integrated hardware-software bundles. The confluence of EV growth, ADAS mandates, and semiconductor localization intensifies competition, but the large and diversified demand base sustains room for incumbents and newcomers alike.

India Automotive Sensors Industry Leaders

Continental AG

DENSO Corporation

Aptiv

Robert Bosch

Hyundai Mobis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bosch committed EUR 2.5 billion to artificial-intelligence R&D through 2027, applying AI to assisted-driving sensor suites for global and Indian platforms.

- April 2025: Axiro Semiconductor inaugurated a USD 36 million RF-design center in Bengaluru to support automotive and IoT sensor chipsets.

- March 2025: The Government of India expanded the automotive PLI budget, in which automobiles and auto components jump from INR 346.87 crore to INR 2,818.85 crore for FY 2025-26, aiming to deepen domestic supply chains for advanced sensors.

India Automotive Sensors Market Report Scope

The India Automotive Sensors Market covers the latest trends and technological development of sensors in India, demand by Sensor type, vehicle drive-train, application and market share of major sensor players across the country.

By Sensor Type

| Pressure Sensors |

| Temperature Sensors |

| Speed Sensors |

| Electro-Optical Sensors |

| Electro-Magnetic Sensors |

| Other Sensors |

By Vehicle Drive-train

| ICE Vehicles |

| Electric Vehicles |

By Application

| Engine & Drivetrain |

| Vehicle Electronics |

| Vehicle Safety Systems |

| Other Applications |

By Vehicle Type

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| By Sensor Type | Pressure Sensors |

| Temperature Sensors | |

| Speed Sensors | |

| Electro-Optical Sensors | |

| Electro-Magnetic Sensors | |

| Other Sensors | |

| By Vehicle Drive-train | ICE Vehicles |

| Electric Vehicles | |

| By Application | Engine & Drivetrain |

| Vehicle Electronics | |

| Vehicle Safety Systems | |

| Other Applications | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles |

Key Questions Answered in the Report

How large is the India automotive sensors market in 2026?

The India automotive sensors market size is USD 3.81 billion in 2026.

What CAGR is projected for automotive sensors in India through 2031?

The market is expected to advance at an 18.66% CAGR to 2031.

Which sensor type currently leads volume sales?

Pressure sensors lead with a 43.12% share in 2025.

Which drive-train category is growing fastest for sensor demand?

Electric vehicles show the fastest 18.71% CAGR through 2031.

What regulation is most influential for safety-sensor uptake?

The AIS-145 standard mandating ADAS and TPMS features starting April 2026.

How will localization incentives affect sensor supply chains?

PLI and SPECS subsidies encourage domestic MEMS fabrication, lowering costs and lead times for sensor suppliers.

Page last updated on: