Market Overview

| Study Period | 2019 - 2031 |

|---|---|

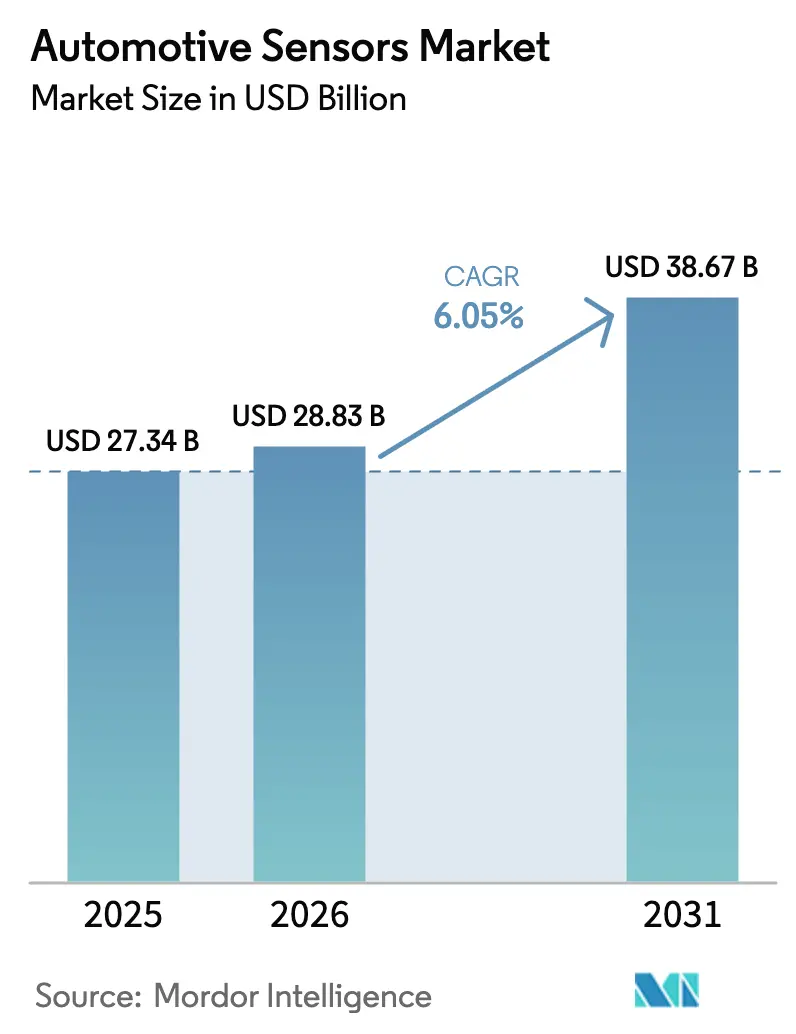

| Market Size (2026) | USD 28.83 Billion |

| Market Size (2031) | USD 38.67 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

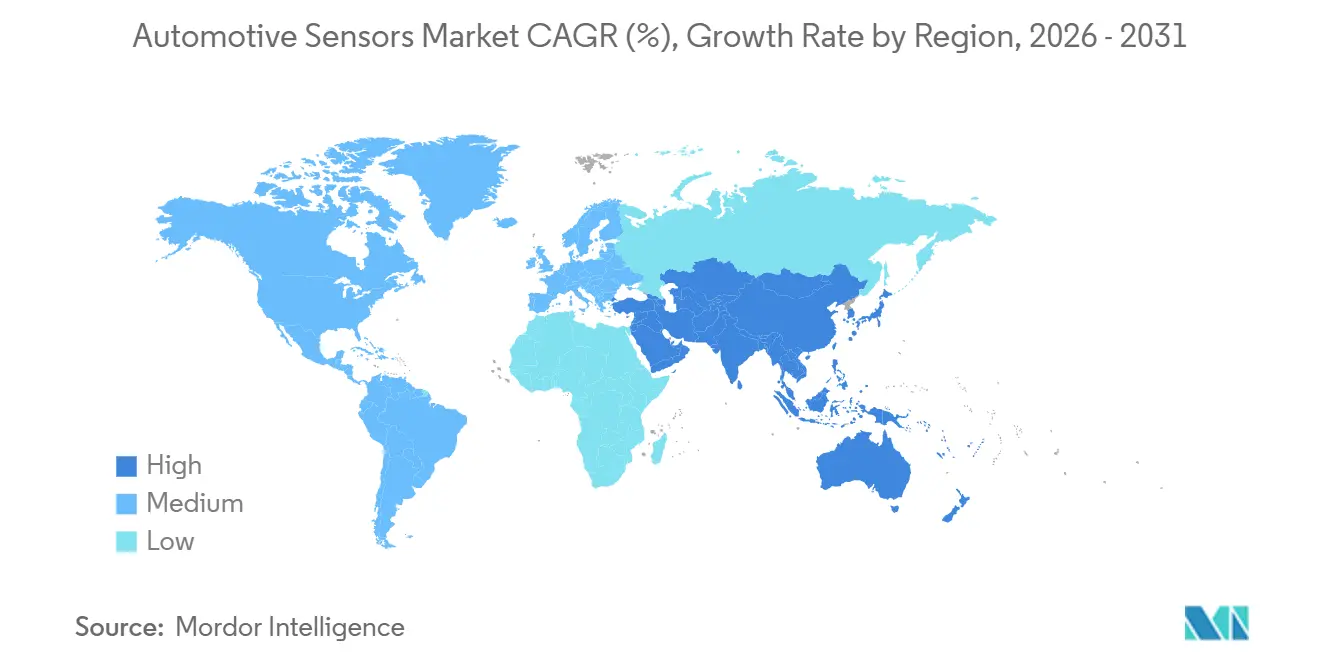

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Sensors Market Analysis by Mordor Intelligence

The automotive sensor market size was valued at USD 27.34 billion in 2025 and estimated to grow from USD 28.83 billion in 2026 to reach USD 38.67 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031). Solid growth reflects the rising sensor content per vehicle, as Euro 7 on-board monitoring and the United States' automatic-emergency-braking rules make redundant detection arrays mainstream, even in entry-level trims. Inertial measurement units (IMUs) remain pivotal because electronic stability control and Level 2+ ADAS now ship standard on 60% of North American light vehicles, while real-time battery-temperature sensing is scaling with fast-charging 800-volt platforms. Falling Micro-Electro-Mechanical Systems (MEMS) average selling prices (ASPs) accelerate adoption in sub-USD 15,000 cars sold across India and Southeast Asia, helping the automotive sensor market penetrate cost-sensitive tiers. Meanwhile, usage-based insurance programs that utilize accelerometers and GPS are increasing telematics volume and generating recurring data service revenues for fleet operators.

Key Report Takeaways

- By type, inertial sensors led the automotive sensors market, accounting for 28.13% of the share in 2025, and are projected to grow at a 6.47% CAGR through 2031.

- By application, the powertrain segment held 40.55% of the automotive sensors market size in 2025, while telematics recorded the fastest growth rate of 8.86% through 2031.

- By vehicle type, passenger cars accounted for 71.18% of the revenue share in 2025; commercial vehicles are expected to expand at a 7.15% CAGR through 2031.

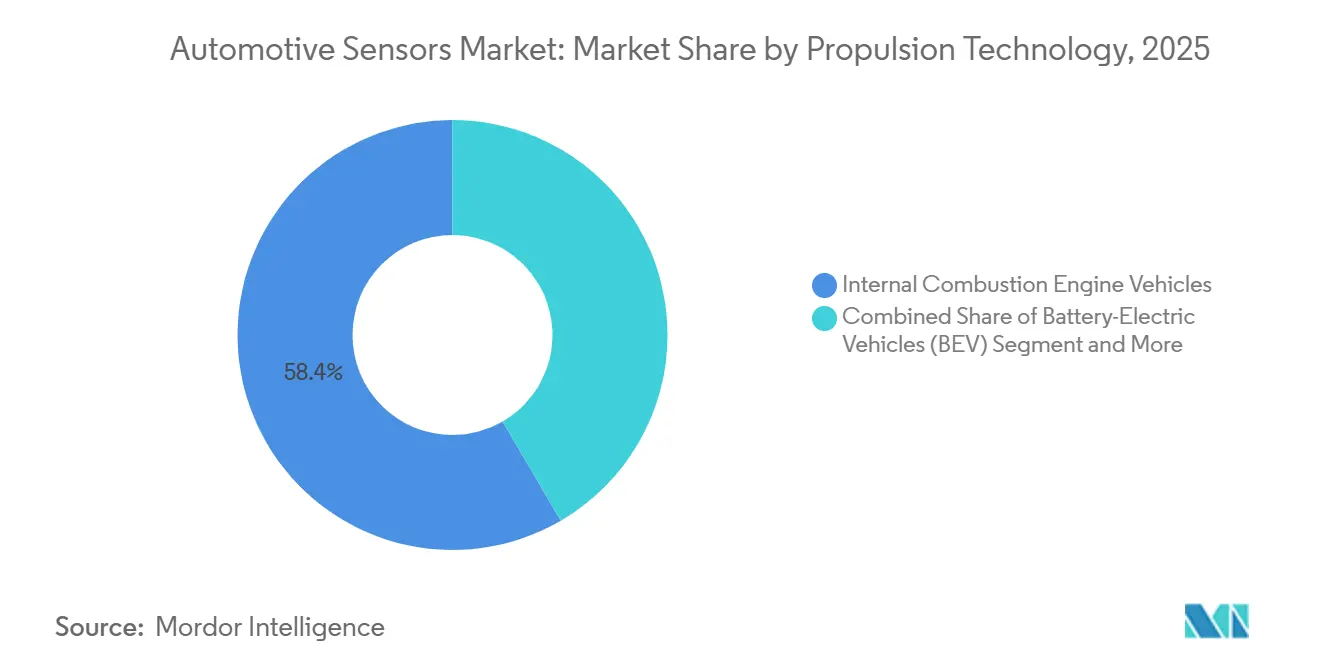

- By propulsion technology, internal combustion engine vehicles held 58.40% of the automotive sensors market size in 2025; fuel-cell electric cars are projected to grow at a 24.50% CAGR to 2031.

- By sales channel, OEM-fitted sensors dominated with an 88.20% share in 2025; the aftermarket segment is expected to advance at a 12.40% CAGR through 2031.

- By geography, the Asia-Pacific region captured a 42.30% revenue share in 2025 and is projected to advance at a 9.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Automotive Sensors Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS and Autonomous-Driving Sensors | +1.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| EV Thermal-Battery Sensing Boom | +1.5% | Asia-Pacific core, expanding to North America | Medium term (2-4 years) |

| Emission and Safety Mandates for Pressure/Gas Sensors | +1.2% | Global, strongest in Europe and China | Short term (≤ 2 years) |

| Falling MEMS ASP Driving Adoption | +0.9% | Global, cost-sensitive markets first | Long term (≥ 4 years) |

| OTA-Ready Self-Diagnostic Sensors | +0.6% | Premium markets, gradual mainstream | Long term (≥ 4 years) |

| Usage-Based Insurance Telematics Demand | +0.4% | North America and Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ADAS and Autonomous-Driving Sensor Proliferation

New regulations mandate that United States light vehicles include automatic emergency braking systems capable of detecting pedestrians at night, requiring manufacturers to enhance their forward-looking sensor suites [1]“Federal Motor Vehicle Safety Standard No. 127 Automatic Emergency Braking,”, National Highway Traffic Safety Administration, nhtsa.gov. Approvals for advanced driving systems, such as highway certifications, necessitate triple-redundant clusters, significantly increasing perception hardware costs. The transition from single-technology systems to hybrid radar-camera architectures is becoming more prominent with advancements in imaging-radar programs. However, research continues to highlight false-positive rates in current systems, emphasizing the need for higher-resolution lidar and thermal imaging. Additionally, updates to functional-safety standards are broadening audits to include cybersecurity, which extends validation processes but strengthens vendor positions in the market.

Electric Vehicle (EV) Thermal-Battery Sensing Boom

Global production of battery-electric vehicles has increased significantly, with each car incorporating multiple temperature probes across cells and coolant loops to prevent thermal runaway incidents. China's updated standards require real-time monitoring at the cell level, resulting in a notable increase in sensor counts compared to earlier models. Research from the European Union's Joint Research Centre highlights that distributed thermal sensing can substantially reduce catastrophic failures during crash scenarios [2]“Thermal Runaway Mitigation in Li-Ion Packs,”, Joint Research Centre, ec.europa.eu. In response to these developments, STMicroelectronics introduced advanced MEMS thermistors designed for high-voltage packs. Despite the growing share of pure electric vehicles, the demand for thermal sensors remains strong, particularly with the use of dual-zone cooling in plug-in hybrids. Additionally, updated standards now require tests for thermal-propagation resistance, emphasizing the importance of co-located pressure and temperature devices.

Emission and Safety Mandates Driving Pressure/Gas Sensors

The Euro 7 regulations will soon come into effect for new cars, introducing stricter particulate and NOx thresholds compared to the previous standards. This change requires the adoption of advanced zirconia sensors. Similarly, the United States Environmental Protection Agency (USEPA) is implementing new standards that significantly reduce particulate limits, driving the need for dual-sensor configurations in diesel vehicles. In addition, China is fully enforcing its updated standards, which align closely with Euro 6d-ISC-FCM, further expanding the global market for addressable sensors. Bosch has developed a particulate-matter module that uses laser scattering technology to predict filter regeneration, enhancing service intervals. Suppliers with expertise in ceramic substrates, such as Continental and NGK NTK, are now benefiting from higher pricing due to their specialized knowledge.

Falling Micro-Electro-Mechanical Systems (MEMS) ASP Enabling Mass Adoption

The average selling prices for automotive-grade accelerometers have declined due to increased die output from advanced wafer lines. This price reduction has enabled the adoption of electronic stability control and tire-pressure monitoring in India’s affordable automotive segment, driven by new safety mandates. Bosch’s six-axis accelerometer has been introduced at a significantly lower cost compared to its predecessor. Additionally, STMicroelectronics’ accelerometer, featuring on-chip machine-learning capabilities, has reduced microcontroller overhead, facilitating predictive maintenance in fleet telematics. In North America, affordable aftermarket kits have become widely available, driving replacement demand as original sensors near the end of their battery life.

Restraints Impact Analysis of Automotive Sensors Market*

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensor Costs in Mass-Market Vehicles | -1.1% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Wafer-Supply Volatility | -0.8% | Global, concentrated in Asia-Pacific | Medium term (2-4 years) |

| ADAS Liability Delays | -0.5% | North America and Europe primarily | Medium term (2-4 years) |

| Privacy Limits on Data Monetization | -0.3% | Europe and select jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Wafer-Supply Volatility

Automotive-grade lead times remain significantly higher than pre-pandemic levels, causing delays in new-model launches [3]“Global Semiconductor Equipment Outlook 2025,”, SEMI, semi.org. While new fabs by Intel and Taiwan Semiconductor Manufacturing Company (TSMC) in Arizona are expected to enhance domestic capacity, the automotive qualification process is delaying substantial volume relief. Europe's Chips Act aims to increase the region's share of the semiconductor market. However, foundries continue to prioritize logic nodes, leaving sensor-specific production lines limited. Tier-1 suppliers are increasing inventory buffers, which is straining working capital and reducing returns. This approach places smaller vendors with weaker financial resources at a disadvantage. Consequently, dual-sourcing strategies are now widely adopted, even for long-life AEC-Q100 components.

Sensor Cost Pressure on Mass-Market Vehicles

Manufacturers targeting affordable retail prices are reducing sensor sets, limiting ADAS features to higher trims, and slowing their expansion into emerging markets. Original equipment manufacturers (OEMs) in Latin America are pushing for significant price reductions on sensor modules, which has negatively impacted tier-1 gross margins and restricted R&D budgets. High-voltage current sensors required for advanced electric vehicles are more expensive than their standard counterparts, delaying their adoption outside premium brands. The aftermarket is also experiencing intense pricing pressure, with generic tire-pressure monitoring replacements significantly undercutting OEM parts. To maintain market share, suppliers are increasingly offering bundled calibration services and extended warranties, shifting their focus from hardware margins to service revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Sensors Market Segment Analysis

By Type:

Inertial Dominance Anchors Stability and NavigationInertial devices commanded 28.13% of the 2025 revenue within the automotive sensor market size and are expected to advance at a 6.47% CAGR to 2031 as global electronic stability control and sensor-fusion stacks standardize on six-axis IMUs. Bosch's SMI240 and Murata's steer-by-wire gyroscopes exemplify the industry's shift toward ASIL D-certified firmware, enabling minimal drift and withstanding extreme shocks. Temperature sensors, with multiple units in each electric vehicle battery pack, adeptly manage rapid thermal gradients during fast charging. Pressure modules play a crucial role, from monitoring tire pressure to regenerating diesel particulate filters in compliance with evolving standards. While commoditized speed sensors are vital for anti-lock braking systems and traction control, Hall-effect current transducers, designed for high-voltage packs, are carving out lucrative niches for companies like Allegro and Melexis.

The sensor landscape also features level, position, and gas sensors. Although ultrasonic parking aids may soon be overshadowed by high-resolution cameras, throttle-position and crankshaft sensors are poised to remain relevant, bolstered by a significant global fleet of internal combustion vehicles. Gas sensors, particularly those for NOx and particulate detection, are experiencing a resurgence in demand due to stricter regulations, granting companies like Continental and NGK NTK enhanced pricing leverage. In anticipation of updated standards, suppliers are integrating cybersecurity features into next-gen sensor chips, not only distinguishing their premium products but also bolstering the overall automotive sensor market.

By Application:

Powertrain Dominance Faces Telematics DisruptionPowertrain modules retained 40.55% of the revenue in 2025, due to the continued demand for oxygen, manifold-pressure, and crankshaft sensors, which are still required on internal-combustion engines. Yet telematics sensors represent the fastest-growing slice of the automotive sensor market, with an 8.86% CAGR driven by usage-based insurance and fleet analytics that monetize accelerometer, GPS, and cellular data.

As overall vehicle production rises, so too do body electronics, devices responding to rain, ambient light, and occupancy. Meanwhile, as smartphone-based access becomes more prevalent, vehicle security modules see a corresponding uptick. While the share of powertrains may wane due to the phasing out of exhaust-gas sensors in EVs, the introduction of voltage and thermal sensing in battery-management systems offers a counterbalance to this decline. Predictive-maintenance data harnessed from telematics has demonstrated its ability to reduce fleet downtime, underscoring the economic rationale for investing in sensors. Responding to the need for enhanced safety, ISO 26262 now requires telematics modules to have redundant signal paths. This addition, while raising the bill of materials, guarantees a fail-silent operation even during connectivity disruptions.

By Vehicle Type:

Commercial Fleets Accelerate Sensor AdoptionPassenger cars accounted for 71.18% of 2025 demand, reflecting widespread mandates for anti-lock braking systems, electronic stability control, and tire-pressure monitoring systems across 90% of global production. Commercial vehicles, however, are forecasted to grow at a 7.15% CAGR, the fastest within the automotive sensor industry, as fleets seek to lower their total cost of ownership through telematics and predictive maintenance.

Heavy-duty NOx standards, which are expected to be implemented in 2027 in the United States, require the use of dual sensors. Meanwhile, European rules add lane-keeping and emergency braking capabilities to new trucks, embedding inertia and perception hardware typically reserved for premium passenger cars. China’s 450,000 new-energy commercial vehicles delivered in 2024 carry mandatory thermal-runaway detection arrays. The installed commercial fleet is also older; average truck age tops 12 years in North America, so aftermarket retrofits for blind-spot and tire-pressure detection enlarge lifetime sensor revenue.

By Propulsion Technology:

FCEV’s Explosive TrajectoryInternal-combustion platforms still accounted for 58.40% of 2025 shipments; however, their share is expected to decline as battery-electric and plug-in hybrid vehicles gain market share. Battery-electric vehicles require dense current, voltage, and thermal arrays, raising content per unit. Plug-in hybrids remain relevant in Asia and North America, sustaining dual sensor sets for engine and battery. Fuel-cell electric vehicles are projected to post a 24.50% CAGR, the highest within the automotive sensor market, although from a low base, as hydrogen refueling stations surpassed 1,000 worldwide in 2024.

Toyota's Mirai and Hyundai's NEXO are equipped with hydrogen leak detectors, high-pressure transducers, and stack humidity monitors. These features comply with ISO standards for hydrogen safety. Due to the stringent safety requirements for hydrogen, fuel-cell electric vehicles (FCEVs) incorporate more sensors compared to battery electric vehicles. However, the impact on overall revenue remains limited until production volumes reach a significant scale.

By Sales Channel:

Aftermarket Gains Retrofit MomentumOriginal-equipment fitment accounted for 88.20% of 2025 revenue, underscoring the manufacturer's control over safety-critical modules. The aftermarket is expected to grow at a 12.40% CAGR through 2031 as collision-repair shops invest USD 30,000–50,000 in calibration rigs to meet insurer requirements after windshield or bumper replacement. Bosch’s 2024 automated ADAS alignment system cuts calibration time by two-thirds and anchors share in high-volume United States service chains.

Tire-pressure monitoring batteries have a predictable replacement cycle. In North America, where vehicles are typically older, sales of oxygen and mass-airflow sensors are strong. Recent regulations in Europe are expected to expand the aftermarket by granting independent shops access to diagnostic tools. While the aftermarket is poised for growth, the automotive sensor market will continue to have an OEM-focused structure, as integrated radar and lidar clusters, due to their calibration complexities and associated liabilities, remain under the control of original equipment manufacturers.

Geography Analysis

APAC Automotive Sensors Market

The Asia-Pacific led the automotive sensor market with 42.30% revenue in 2025 and is forecasted to grow at a 9.10% CAGR through 2031. China's new-energy vehicle sales, now mandated to include cell-level thermal monitoring under updated regulations, have propelled the market. In India, a production-linked incentive is facilitating local MEMS assembly and reducing import bills for tier-2 suppliers. In Japan, ADAS penetration has increased significantly, driven by the use of imaging sensors from DENSO and Sony. Meanwhile, South Korea's Samsung and SK Hynix are expanding their regional MEMS foundry capacity.

North America and Europe Automotive Sensors Market

While North America and Europe account for a significant share of shipments, their growth is expected to slow as vehicle production stabilizes and sensor usage in premium trims nears saturation. The United States Infrastructure Investment and Jobs Act is backing public charging points, which is likely to boost the demand for sensors in EV chargers. With stricter thresholds for NOx and particulates, companies such as Continental and Bosch are experiencing a consistent demand for gas sensors. Both North America and Europe are striving for semiconductor independence, as evident from Intel's investments in Arizona and the European Chips Act. However, the automotive sector's qualification process lags behind consumer electronics, leading to a continued reliance on Asian production.

MEA and South America Automotive Sensors Market

South America and the Middle East and Africa, which account for a smaller share of the market, are poised for faster growth. Brazil's incentives are bolstering the adoption of ESC and TPMS. Turkey's export vehicles, now equipped with EU-compliant ADAS, are driving local demand for sensors. Despite smaller production volumes, South Africa's adoption of stricter diesel regulations and the Gulf Cooperation Council's luxury fleet are both increasing the sensor count per vehicle. Argentina, while banking on currency stability for recovery, still presents an aftermarket opportunity due to its aging vehicle fleet.

Competitive Landscape

In the automotive sensor market, Bosch, DENSO, and Continental command a significant share of market revenues. Their positions span multiple stages, from wafer fabrication to module validation. Reflecting the industry's capital intensity, Bosch is investing in a new fabrication plant. As the industry pivots toward software-defined vehicles, Tier-1 suppliers are co-developing sensor platforms with OEMs and protecting aftermarket positions through calibration services and extended warranties.

In this evolving landscape, niche opportunities are attracting specialists. Allegro MicroSystems and Melexis supply application-specific current and magnetic-position ICs for advanced vehicle systems, and faster design cycles can provide an advantage over broader-line suppliers. Solid-state lidar companies such as Luminar and Aeva are also pursuing more direct OEM engagement, which can simplify supply chains and alter profit distribution. Patent filings in sensor fusion are increasing, with emphasis on software that differentiates performance as hardware becomes more standardized.

With updated standards, cybersecurity is becoming more important in sensor nodes. While this increases compliance costs, it can strengthen the position of suppliers with embedded security intellectual property. OEMs are also increasingly procuring semiconductors directly from vendors such as Infineon and STMicroelectronics, integrating components in-house and increasing pressure on traditional module suppliers. For smaller entrants, rigorous validation requirements and long design-win cycles continue to favor companies with strong balance sheets and global support capabilities.

Automotive Sensors Industry Leaders

Continental AG

NXP Semiconductors NV

Robert Bosch GmbH

Infineon Technologies AG

DENSO Corporation

- *Disclaimer: Major Players sorted in no particular order

Automotive Sensors Market Companies Covered in this Report

- Robert Bosch GmbH

- DENSO Corporation

- Continental AG

- Infineon Technologies AG

- NXP Semiconductors NV

- Sensata Technologies PLC

- Texas Instruments Inc.

- Analog Devices Inc.

- Aptiv PLC

- ST Microelectronics NV

- Valeo SA

- Honeywell International Inc.

- Allegro MicroSystems LLC

- Murata Manufacturing Co.

- ON Semiconductor Corporation

- TE Connectivity Ltd.

- Autoliv Inc.

Recent Industry Developments in Automotive Sensors Market

- October 2025: OMNIVISION, a global frontrunner in semiconductor technology, has unveiled its latest automotive image sensor: the OX08D20 8-megapixel (MP) CMOS, featuring TheiaCel™ technology. This cutting-edge sensor enhances the widely used OX08D10, tailored for exterior cameras in advanced driver assistance systems (ADAS) and autonomous driving (AD).

- October 2025: Sony Semiconductor Solutions announced the IMX828, the first CMOS image sensor for automotive applications to feature a MIPI A-PHY interface integrated directly into the chip.

- April 2025: Infineon Technologies acquired Marvell’s Automotive Ethernet unit for USD 2.5 billion to integrate networking with microcontroller portfolios.

Automotive Sensors Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the automotive sensors market as the revenue generated from factory-installed and replacement devices that detect temperature, pressure, speed, level or position, magnetic fields, gases, and inertial motion, converting those signals for electronic control units across passenger cars and commercial vehicles.

Scope Exclusions: stand-alone aftermarket gadgets lacking ECU integration and sensors used solely on production test benches lie outside our estimate.

Segments Covered in This Report

- By Type

- Temperature Sensors

- Pressure Sensors

- Speed Sensors

- Level / Position Sensors

- Magnetic Sensors

- Gas Sensors

- Inertial Sensors

- By Application

- Powertrain

- Body Electronics

- Vehicle Security Systems

- Telematics

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- By Propulsion Technology

- Internal Combustion Engine (ICE) Vehicles

- Battery-Electric Vehicles (BEV)

- Plug-in Hybrid Vehicles (PHEV)

- Fuel-cell Electric Vehicles (FCEV)

- By Sales Channel

- OEM-fitted Sensors

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Turkey

- Gulf Cooperation Council (GCC)

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We interview design engineers at sensor makers, Tier-1 module integrators, and vehicle procurement managers across North America, Europe, and Asia Pacific. These dialogues validate sensor content per vehicle, regional pricing dispersion, and regulation-driven demand inflections, closing gaps that desk work leaves open.

Desk Research

We begin with openly available statistics from bodies such as the International Organization of Motor Vehicle Manufacturers, ACEA, NHTSA, the IEA Global EV Outlook, JEITA, and UN Comtrade, which together provide yearly vehicle production, power-train mix, and trade flows. Company 10-Ks, investor decks, peer-reviewed journals, and respected trade press then clarify technology adoption curves and average selling-price shifts. Paid resources, including Marklines vehicle output dashboards and D&B Hoovers supplier financials, help Mordor analysts align market shares with actual revenue trails. The sources cited are illustrative, and many additional public and subscription feeds inform the baseline.

Market-Sizing & Forecasting

Starting with regional vehicle assemblies, electrification rates, and mandated ADAS fitment, the team constructs top-down demand pools that are multiplied by sensor-content buckets. Supplier revenue samples and channel checks supply selective bottom-up roll-ups that temper outliers. Key variables tracked include global production volumes, BEV and PHEV penetration, ADAS penetration levels, MEMS sensor ASP trends, and milestones such as Euro 7. Multivariate regression, supported by scenario analysis for policy timing, projects each driver. Where supplier disclosure is thin, volumes are interpolated from capacity utilization histories before final reconciliation.

Data Validation & Update Cycle

Outputs undergo two-step analyst review, in which anomalies against independent series or prior editions are flagged and resolved. Reports refresh annually, with interim updates triggered by major regulatory or technology events, ensuring clients receive the latest vetted view.

How Mordor Intelligence's Automotive Sensors Market Size Compares to Other Published Estimates

Published estimates often diverge because firms vary in the sensor families, retrofit channels, and ASP dynamics they include, and in how quickly they assume ADAS penetration will rise.

Key gap drivers for others include bundling high-value AD sensing hardware with traditional devices, applying blanket price uplifts without regional mix calibration, or omitting replacement demand entirely.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.83 B (2025) | Mordor Intelligence | - |

| USD 30.80 B (2023) | Global Consultancy A | Merges LiDAR and radar modules our scope treats separately |

| USD 43.30 B (2024) | Data Publication B | Uses single global ASP uplift without regional or power-train adjustment |

| USD 11.87 B (2024) | Industry Journal C | Counts only chassis-mounted sensors, excluding aftermarket replacement |

The comparison shows that by anchoring scope to OE and aftermarket flows, grounding prices in verified supplier data, and refreshing assumptions each year, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can confidently rely on.

Key Questions Answered in the Report

What is the current value of the automotive sensor market?

The automotive sensor market size was USD 28.83 billion in 2026 and is forecast to reach USD 38.67 billion by 2031.

Which sensor type holds the largest share?

Inertial devices such as accelerometers and gyroscopes led with 28.13% share in 2025 and are advancing at a 6.47% CAGR.

Which region is expanding the fastest?

Asia-Pacific is growing at 9.10% CAGR through 2031, driven by China’s electric-vehicle production surge and India’s localization push.

How will fuel-cell vehicles affect sensor demand?

Fuel-cell electric vehicles are set for a 24.50% CAGR to 2031, adding hydrogen-specific leak and pressure sensors that raise content per vehicle.

Why is the aftermarket growing quicker than OEM fitment?

Collision-repair ADAS calibration and predictable TPMS battery replacements are boosting aftermarket revenues at a 12.40% CAGR.

Page last updated on: