India Automotive Air Filters Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

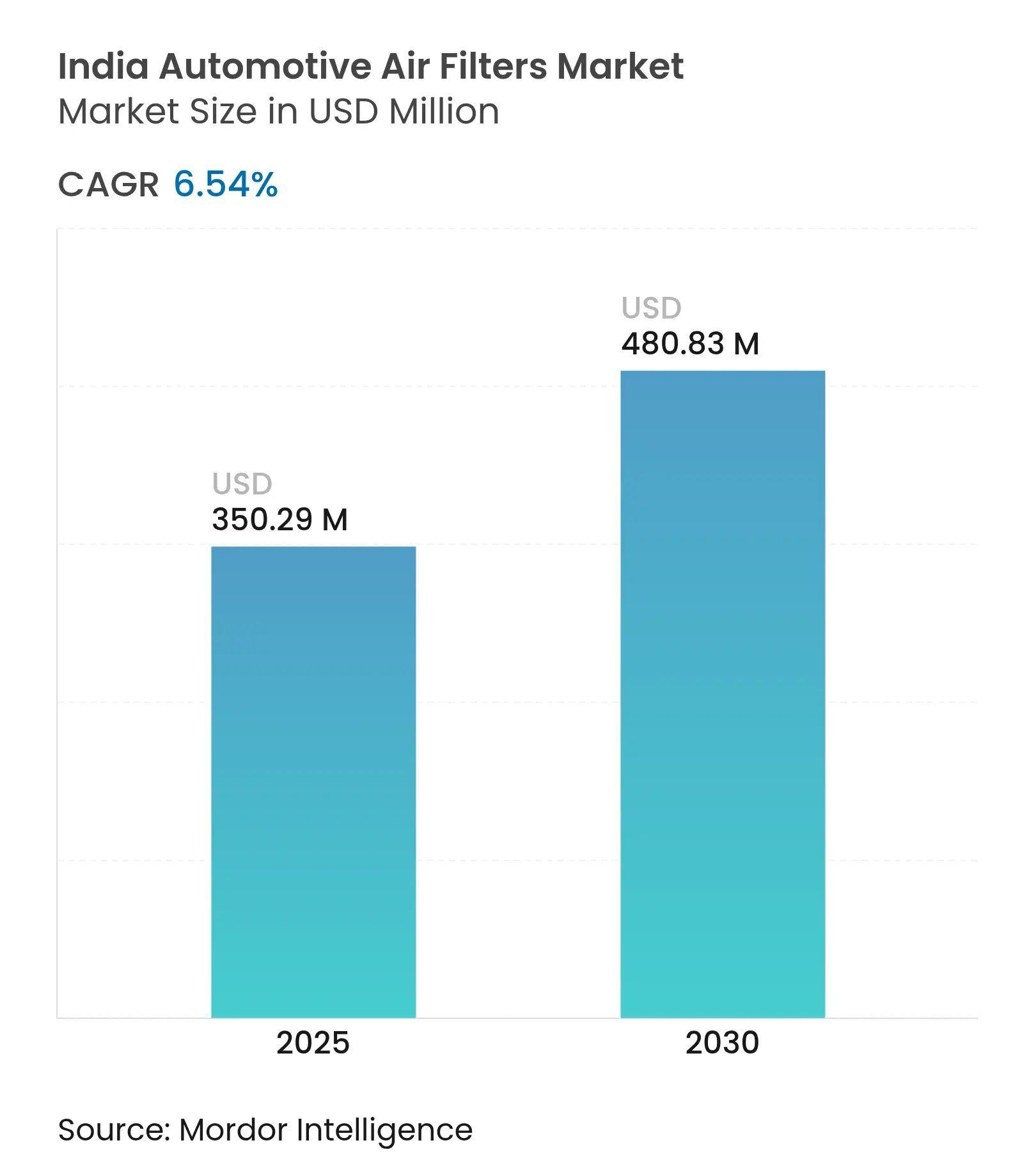

| Market Size (2025) | USD 350.29 Million |

| Market Size (2030) | USD 480.83 Million |

| Growth Rate (2025 - 2030) | 6.54 % CAGR |

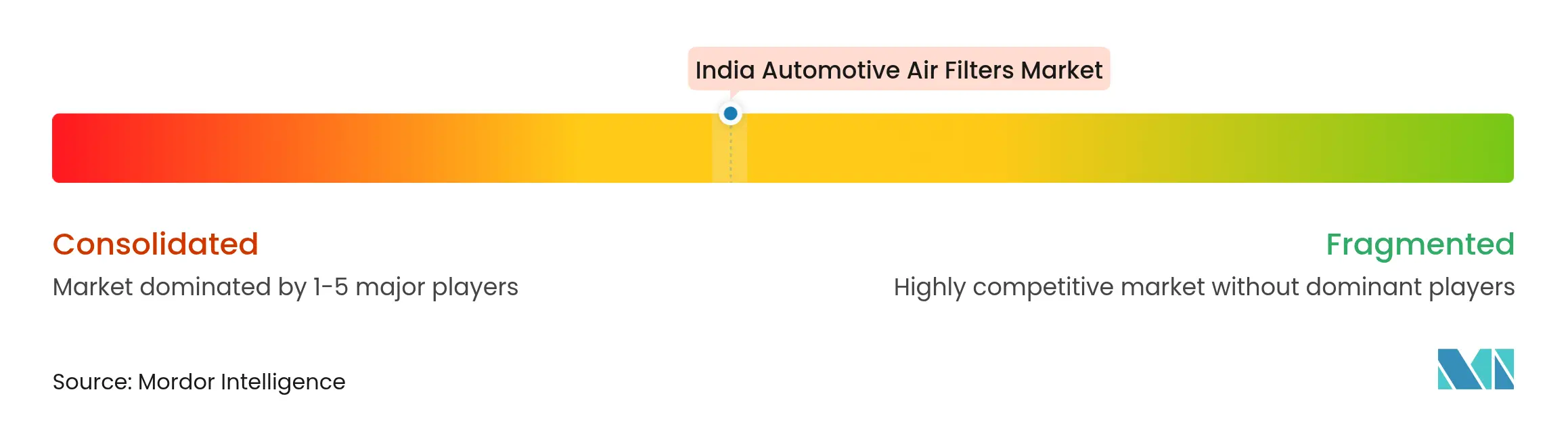

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

India Automotive Air Filters Market Analysis by Mordor Intelligence

The India automotive air filters market size is valued at USD 350.29 million in 2025 and is forecast to reach USD 480.83 million in 2030, advancing at a 6.54% CAGR during the forecast period. The government’s localization push through Production Linked Incentive schemes, and the continual introduction of BS-VI compliant models, all reinforce demand. Premium cabin filters are gaining traction as urban consumers prioritize in-cabin air quality, while OEMs balance longer-life parts with the need to protect complex after-treatment systems. The electrification of fleets will gradually curb demand for intake filters, yet it simultaneously opens revenue streams for advanced cabin and battery thermal-management filtration. Rising replacement cycles in high-utilization fleets and dust-intensive agricultural zones further broaden the India automotive air filters market opportunity.

Key Report Takeaways

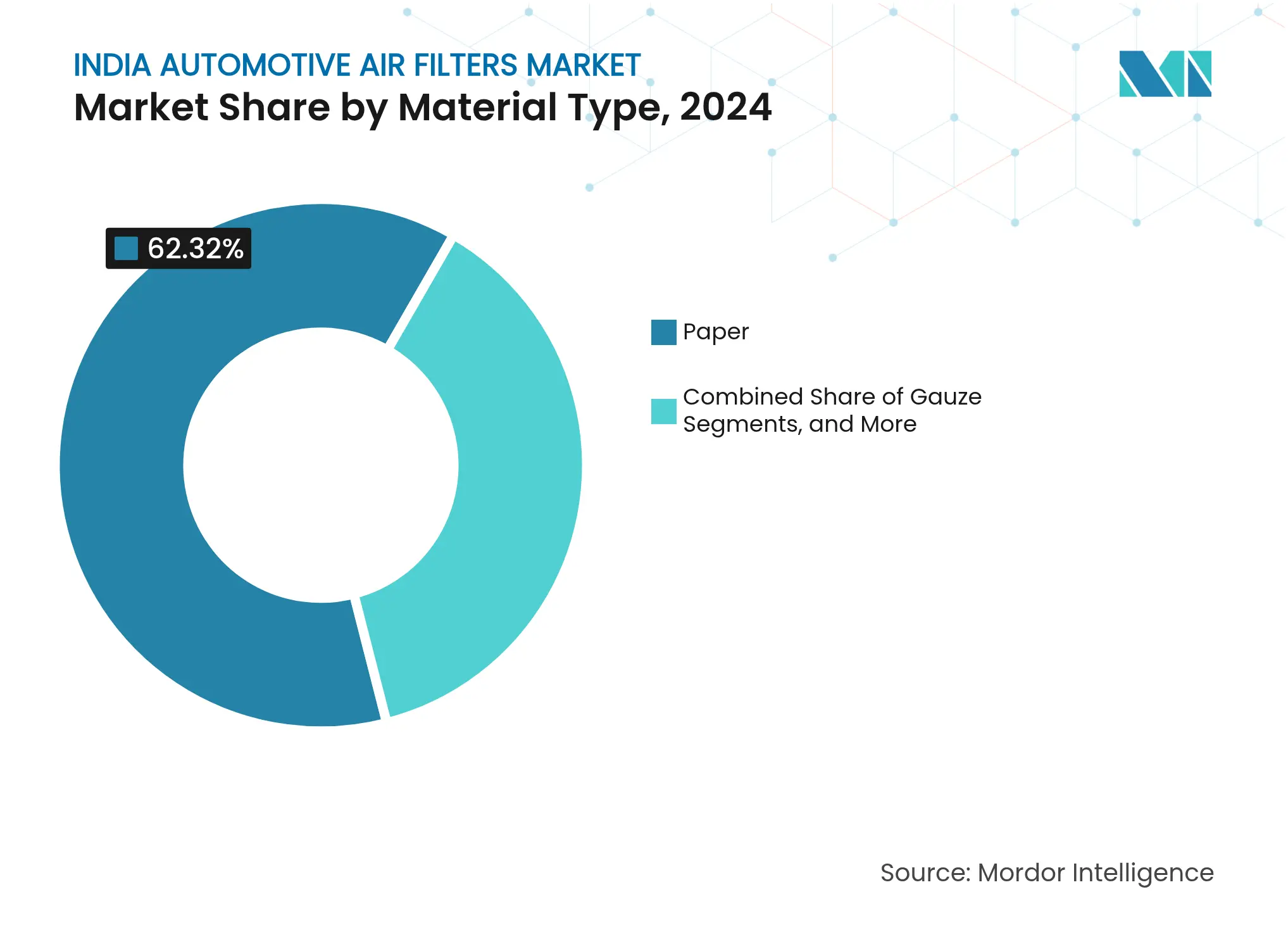

- By material type, paper filters captured 62.32% of the India automotive air filters market share in 2024, while nanofiber filters are projected to post the fastest 7.37% CAGR through 2030.

- By filter type, intake elements accounted for 56.38% of the India automotive air filters market share in 2024; cabin filters are poised to grow at a 6.38% CAGR to 2030.

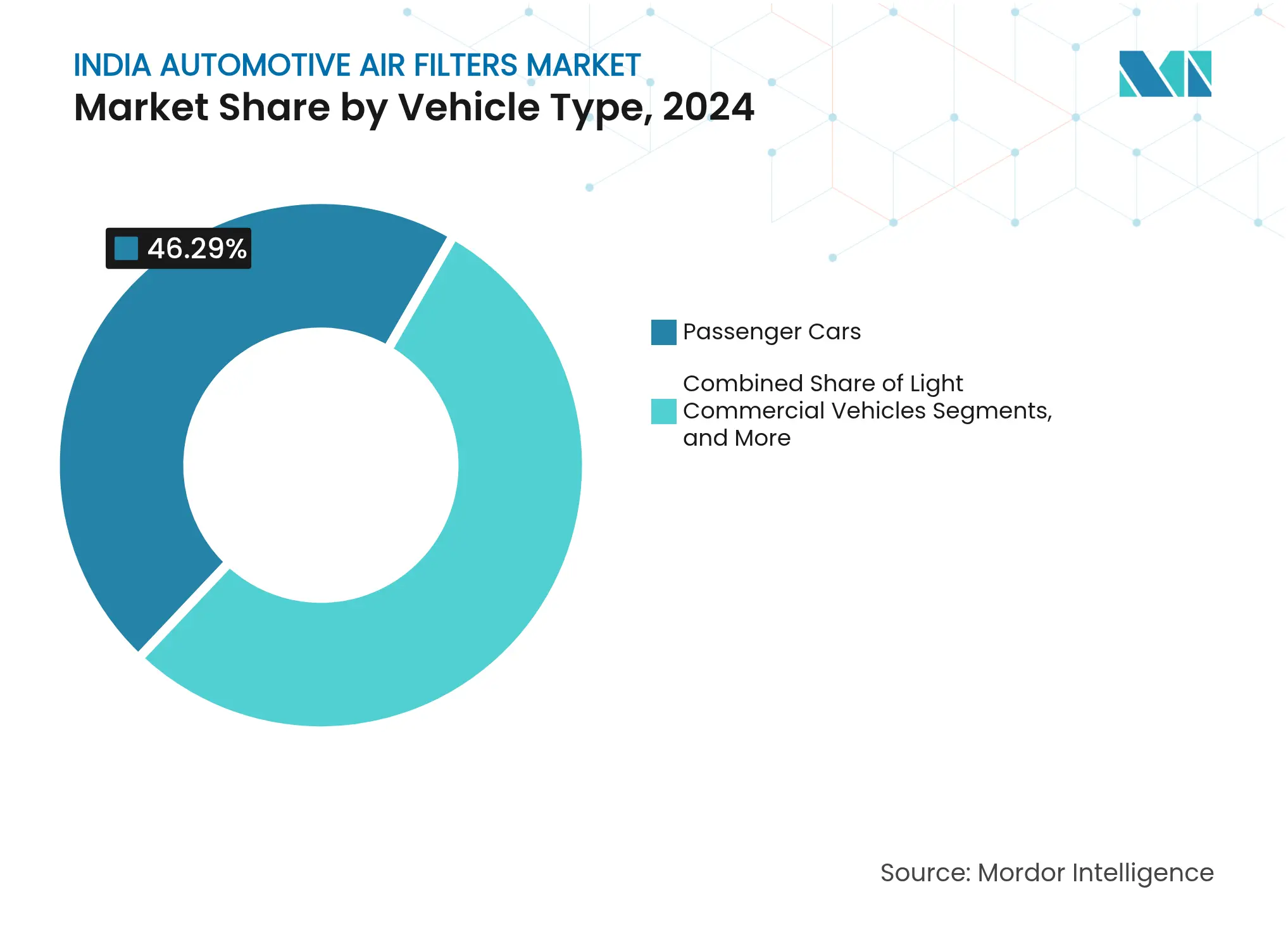

- By vehicle type, passenger cars held 46.29% of the India automotive air filters market share in 2024, whereas two-wheelers are expected to register the highest 7.49% CAGR through the forecast period.

- By sales channel, OEM fitment represented 63.72% of the India automotive air filters market share in 2024, while the aftermarket segment is anticipated to advance at an 8.22% CAGR during 2025-2030.

- By region, West India led 33.64% of the India automotive air filters market share in 2024; East and North-East India are forecast to expand at a 7.68% CAGR through 2030.

India Automotive Air Filters Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid Adoption of BS-VI Emission Norms Rapid Adoption of BS-VI Emission Norms | +1.2% | National; early gains in NCR, Mumbai, Chennai | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:National; early gains in NCR, Mumbai, Chennai | Impact Timeline:Medium term (2-4 years) |

Rising Consumer Preference for In-Cabin Air Quality Rising Consumer Preference for In-Cabin Air Quality | +0.9% | Delhi-NCR, Mumbai, Bangalore, Chennai | Medium term (2-4 years) | |||

Boom In Shared-Mobility and Subscription Fleets Boom In Shared-Mobility and Subscription Fleets | +0.8% | Urban centers; Mumbai–Pune, Bangalore, NCR | Short term (≤ 2 years) | |||

OEM Push Toward Longer-Life Service Parts OEM Push Toward Longer-Life Service Parts | +0.7% | Urban and semi-urban corridors | Short term (≤ 2 years) | |||

Surge in E-Commerce Two-Wheeler Deliveries Surge in E-Commerce Two-Wheeler Deliveries | +0.6% | Tamil Nadu, Maharashtra, Gujarat | Long term (≥ 4 years) | |||

Growing Agro-Machinery Use in Dusty Belts Growing Agro-Machinery Use in Dusty Belts | +0.5% | Punjab, Haryana, Uttar Pradesh, Maharashtra | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Adoption of BS-VI Emission Norms

Bharat Stage VI standards mandate ultralow-sulfur fuel and advanced particulate controls, lifting filtration performance requirements across power-trains. OEM launches of compliant models before the April 2020 deadline cemented demand for high-efficiency intake and cabin filters[1]“India’s Leap to BS-VI,”, Clean Air Coalition, ccacoalition.org. On-board diagnostic upgrades in BS-VI Stage 2 heighten sensor-protection needs, turning reliable air filtration into a critical safeguard for catalytic converters and diesel particulate filters. Suppliers have responded with multilayer synthetic media that preserve airflow while trapping sub-micron particles. Anticipated BS-VII rules, likely after 2026, will extend real-time emissions monitoring and push filtration specifications even higher, sustaining premium filter volume despite ICE market maturity. The regulatory glide-path, therefore, forms a durable growth floor for the Indian automotive air filters market.

Rising Consumer Preference for In-Cabin Air Quality

AQI readings above 400 in North Indian metros have transformed cabin filters from comfort add-ons into safety necessities. Honda’s Anti-Virus Charcoal Filter uses multilayer activated-carbon media plus herbal extract coatings to neutralize allergens, bacteria, and odors[2]“Anti Virus Charcoal Filter Launch,”, Honda Cars India, hondacarindia.com. BMW’s nanofiber solution captures ultrafine particles down to 100 nm, offering 40% higher filtration efficiency than conventional media. Enhanced sensor-based HVAC systems alert drivers when filter performance degrades, effectively tightening replacement cycles and expanding India's automotive air filter market size.

Boom in Shared-Mobility and Subscription Fleets

Shared mobility vehicles average 8-12 operating hours daily, triple the usage of privately owned cars. Elevated duty cycles shorten replacement intervals and guarantee repeat aftermarket sales. Fleet operators centralize maintenance and often insist on genuine parts to limit unscheduled downtime, giving OEM-linked suppliers a direct route to high-volume accounts. Subscription models concentrate demand in professional fleet workshops, where purchase decisions emphasize proven durability over initial cost. Even as electric models enter these fleets, cabin filter demand persists, supporting revenue diversification.

Surge in E-Commerce Two-Wheeler Deliveries

Delivery riders cover 100–150 km daily, facing continuous stop-start traffic that accelerates filter fouling. Tata Motors noted that e-commerce accounts for up to 10% of its medium—and heavy-duty vehicle sales, underscoring last-mile growth momentum[3]“FY 2024 Annual Report,”, Tata Motors, tatamotors.com. Fleet managers deploy premium filters to safeguard fuel-injection systems from urban soot, accepting higher upfront costs in exchange for fewer engine failures. As delivery platforms scale into smaller towns, two-wheeler replacement demand will permeate Tier-2 markets and incrementally boost the Indian automotive air filters market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Slow Electrification of Two-Wheelers Slow Electrification of Two-Wheelers | -0.9% | Urban centers; expanding Tier-2 cities | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:Urban centers; expanding Tier-2 cities | Impact Timeline:Medium term (2-4 years) |

Shift Toward Washable / Lifetime Filters Shift Toward Washable / Lifetime Filters | -0.7% | Urban premium segments | Medium term (2-4 years) | |||

Counterfeit Low-Cost Filters in Unorganized Aftermarket Counterfeit Low-Cost Filters in Unorganized Aftermarket | -0.6% | Rural and semi-urban markets | Short term (≤ 2 years) | |||

Lengthening Service Intervals for ICE Vehicles Lengthening Service Intervals for ICE Vehicles | -0.5% | National | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Slow Electrification of Two-Wheelers Dampening Intake Filter Demand

The rise of electric two-wheelers is transforming the aftermarket landscape as these vehicles eliminate the need for traditional engine-air filtration systems. The adoption is concentrated in major urban centers with developed charging infrastructure. However, declining battery prices and government subsidies indicate wider adoption potential, particularly by 2030.

The gradual phase-out of internal combustion scooters is reducing the demand for intake filters, especially in high-volume segments. However, this reduction is partially balanced by increased demand for advanced cabin filtration systems in electric cargo models, where air quality and driver comfort have become key priorities. This transition represents a fundamental shift in component demand across the two-wheeler market.

Counterfeit Low-Cost Filters in the Unorganized Aftermarket

Counterfeit filtration parts pose a significant challenge in rural markets, where price-sensitive customers choose lower-cost alternatives. These non-genuine components use inferior filter media and have inadequate sealing, which allows unfiltered dust to enter engines and increases the risk of early wear. Although industry surveys indicate counterfeit parts represent a minor portion of the aftermarket, filtration components face higher counterfeiting rates.

Segment Analysis

By Material Type: Nanofiber Innovation Drives Premium Shift

Paper filters dominated and captured 62.32% of the India automotive air filters market share in 2024 because of low cost and entrenched OEM fitment. The Indian automotive air filters market size for paper media is projected to inch forward at low single-digit growth, sustained by first-time owners in cost-sensitive segments. In parallel, nanofiber variants are forecast to post a 7.37% CAGR through 2030, as buyers in metros upgrade for PM2.5 protection.

Electrospun nanofibers under one μm diameter create tortuous flow paths that seize ultrafine particulates while keeping pressure drop minimal. MANN+HUMMEL’s 2024 roll-out of nanofiber cabin filters priced about 2–3 times standard units signals commercial readiness. Scaling output should narrow the cost gap and allow nanofiber adoption in compact cars and popular scooters, sustaining double-digit segment gains through 2030.

Note: Segment shares of all individual segments available upon report purchase

By Filter Type: Cabin Filters Gain Momentum Amid Health Concerns

Intake elements delivered 56.38% of the India automotive air filters market share in 2024, owing to universal combustion-engine use. Still, growing urban pollution and post-pandemic hygiene awareness propel cabin filters at a 6.38% CAGR to 2030. The Indian automotive air filters market size for cabin applications is expected to surpass intake replacements in passenger cars by the end of the decade.

OEMs now baseline particulate and odor-removal capabilities even in compact cars, while premium brands upgrade to antiviral and nanofiber media. Integrated air-quality sensors that trigger filter change reminders create an electronic pathway to lock in recurring sales. Aftermarket players exploit this window with direct-to-consumer e-commerce kits featuring plug-and-play filters for quick DIY swaps.

By Vehicle Type: Two-Wheeler Surge Reflects Urban Mobility Shift

Passenger cars accounted for 46.29% of the India automotive air filters market share in 2024, yet two-wheelers are forecast to expand faster at 7.49% CAGR through 2030. Higher usage rates in last-mile delivery multiply per-vehicle replacement events, raising the India automotive air filters market size attributable to scooters and motorcycles.

Commercial vehicle demand is equally linked to e-commerce logistics, where rigid replacement schedules and heavy loading cycles heighten filter stress. Agricultural and construction off-highway equipment will continue to require multi-stage systems to cope with severe dust, keeping specialized suppliers well occupied despite modest volume scales.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: Aftermarket Momentum Builds on Service Expansion

OEM networks secured 63.72% of the India automotive air filters market share in 2024 via bundling during new-vehicle sales and warranty servicing. However, the aftermarket will outpace at an 8.22% CAGR through 2030, owing to increased vehicle parc aging into second ownership. Digital platforms that ship filters nationwide within 24 hours broaden reach into Tier-3 towns, democratizing access to branded parts.

Counterfeit threats persist, but QR-code tracing and OEM-authorized web stores help consumers verify authenticity. Fleet operators leverage predictive analytics to schedule bulk replacement, sidestepping stock-outs and gaining volume discounts, thereby tilting more share toward organized aftermarket suppliers.

Geography Analysis

West India remained the most significant contributor, with 33.64% of the India automotive air filters market share in 2024, given Maharashtra’s Pune-Pimpri-Chinchwad and Aurangabad clusters, which host marquee OEMs and tier-1 suppliers. Access to Mumbai and JNPT ports streamlines inbound raw-material logistics and finished-goods exports, reinforcing supplier localization incentives. Enabling state policies and a deep ancillary base assure West India stays the anchor of the Indian automotive air filters market.

East and North-East India will log the fastest 7.68% CAGR through 2030 as infrastructure upgrades and industrial corridors entice OEMs to diversify capacity. New component parks in West Bengal and Odisha, as well as lower land costs, position the region as a strategic expansion arena for filter manufacturers seeking greenfield sites. Government freight-corridor projects will progressively address logistics gaps, narrowing time-to-market disadvantages and helping the Indian automotive air filters market penetrate underserved territories.

South India continues to benefit from Tamil Nadu’s “Detroit of Asia” status and Karnataka’s electronics ecosystem. Export-oriented production lines demand filters that meet global emission and durability norms, stimulating higher per-unit value. North India, anchored by the National Capital Region, supplies sizeable volumes but records moderate growth as market maturity tempers incremental gains.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Competition is moderate; MANN+HUMMEL couples nanofiber R&D with localized production to serve domestic and export OEM plants. Mahle, Bosch, and Donaldson maintain specialized portfolios for heavy-duty and off-highway segments.

Strategic thrusts focus on in-house media development, IATF 16949 compliance, and proximity manufacturing to meet value-addition norms under Make-in-India guidelines. Private-equity backing of component consolidation—illustrated by Carlyle’s USD 400 million platform for precision machinists—signals impending M&A that can reshape the structure of the Indian automotive air filters industry. Suppliers also invest in sensor-driven predictive maintenance to offer service packages rather than stand-alone parts, positioning themselves as lifecycle partners to fleets.

Electric-vehicle filtration needs—battery thermal-management micro-filters and odor-control cabin inserts—represent the next competitive battleground. Firms that translate ICE filtration know-how into EV applications are poised to capture early-mover advantage while hedging against long-term volume-erosion risks in intake filters.

India Automotive Air Filters Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Uno Minda, a Tier 1 supplier of automotive solutions to Original Equipment Manufacturers (OEMs), introduced a new range of cabin air filters for the Indian aftermarket. This product launch addresses air pollution concerns in metropolitan, Tier 1, and Tier 2 cities, where air quality poses health risks.

- March 2024: Hengst Filtration inaugurated its cutting-edge state-of-the-art facility in Yelahanka, Bengaluru. The move addresses the surging demand for filtration systems in industries such as automotive, hydraulics, healthcare, and industrial sectors.

Table of Contents for India Automotive Air Filters Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid Adoption of BS-VI Emission Norms

- 4.2.2Boom in Shared-Mobility and Subscription Fleets

- 4.2.3Rising Consumer Preference For In-Cabin Air-Quality

- 4.2.4OEM Push Toward Longer-Life Service Parts

- 4.2.5Surge in E-Commerce Two-Wheeler Deliveries

- 4.2.6Growing Agro-Machinery Usage in Dusty Rural Belts

- 4.3Market Restraints

- 4.3.1Shift Toward Washable / Lifetime Filters

- 4.3.2Lengthening Service Intervals for ICE Vehicles

- 4.3.3Slow Electrification of Two-Wheelers Dampening Intake Filter Demand

- 4.3.4Counterfeit Low-Cost Filters in the Unorganized Aftermarket

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape (AIS-137, BS-VI, OBD-II)

- 4.6Technological Outlook (nanofiber, electro-static media)

- 4.7Porter's Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Emission Regulation Impact Analysis

5. Market Size and Growth Forecasts (Value (USD))

- 5.1By Material Type

- 5.1.1Paper

- 5.1.2Gauze

- 5.1.3Foam

- 5.1.4Nanofiber

- 5.1.5Other Materials

- 5.2By Filter Type

- 5.2.1Intake Filters

- 5.2.2Cabin Filters

- 5.2.3Crankcase Ventilation Filters

- 5.3By Vehicle Type

- 5.3.1Passenger Cars

- 5.3.2Light Commercial Vehicles

- 5.3.3Heavy Commercial Vehicles

- 5.3.4Two-Wheelers

- 5.3.5Off-Highway Vehicles

- 5.4By Sales Channel

- 5.4.1Original Equipment Manufacturer (OEM)

- 5.4.2Aftermarket

- 5.5By Region

- 5.5.1North India

- 5.5.2West India

- 5.5.3South India

- 5.5.4East and North-East India

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1MANN+HUMMEL

- 6.4.2MAHLE GmbH

- 6.4.3Donaldson Company, Inc.

- 6.4.4Robert Bosch GmbH

- 6.4.5Elofic Industries Limited

- 6.4.6Fleetguard Filters Private Limited

- 6.4.7 Zenith Auto Industries (P) Ltd.

- 6.4.8K&N Engineering, Inc.

- 6.4.9AL Group LTD

- 6.4.10Allena Auto Industries Pvt Ltd

- 6.4.11S&B Filters, Inc.

- 6.4.12 TORAY INDUSTRIES, INC.

7. Market Opportunities and Future Outlook

India Automotive Air Filters Market Report Scope

An automotive air filter is a vital component in a vehicle's air intake system, designed to clean and filter incoming air by trapping contaminants like dust and dirt, ensuring that only clean, oxygen-rich air enters the engine's combustion chamber.

The Indian automotive airfilters market is segmented by material type, type, vehicle type, and sales channel. By material type, the market is segmented into paper air filters, gauze air filters, foam air filters, and other material types. By type, the market is segmented into intake filters and cabin filters. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By sales channel, the market is segmented into OEMs and aftermarkets. The report offers market size and forecasts for all the above segments in terms of value (USD).