Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

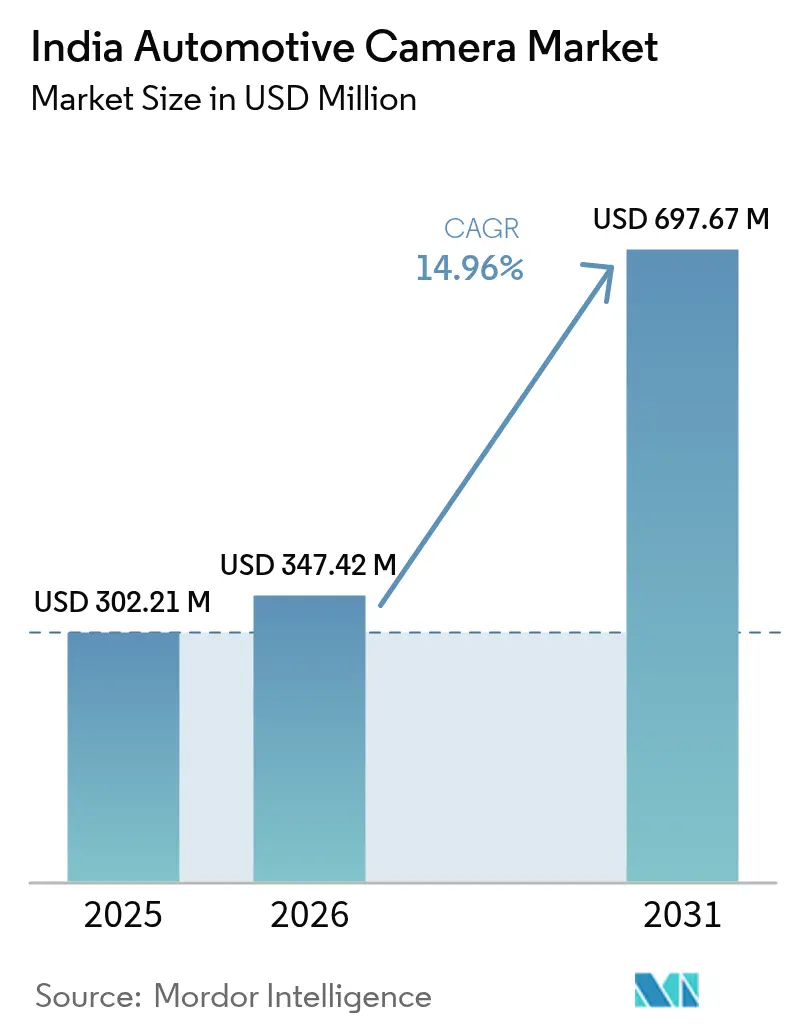

| Base Year Market Size (2025) | USD 302.21 Million |

| Market Size (2026) | USD 347.42 Million |

| Market Size (2031) | USD 697.67 Million |

| Growth Rate (2026 - 2031) | 14.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Camera Market Analysis by Mordor Intelligence

The India automotive camera market size was valued at USD 302.21 million in 2025 and estimated to grow from USD 347.42 million in 2026 to reach USD 697.67 million by 2031, at a CAGR of 14.96% during the forecast period (2026-2031). This robust growth rests on a blend of safety regulations, manufacturing incentives, and consumer demand that makes India an important production and adoption hub for vehicle-mounted cameras. Stricter AIS-150 and Bharat NCAP rules, the premium hatchback and SUV boom, and lower CMOS costs keep volumes rising even in price-sensitive segments. OEMs lead adoption because integrated cameras streamline compliance, while localization policies reduce currency and logistics risks. Competitive intensity remains balanced as global Tier-1s partner with Indian suppliers to deepen local content and weather foreign-exchange swings.

Key Report Takeaways

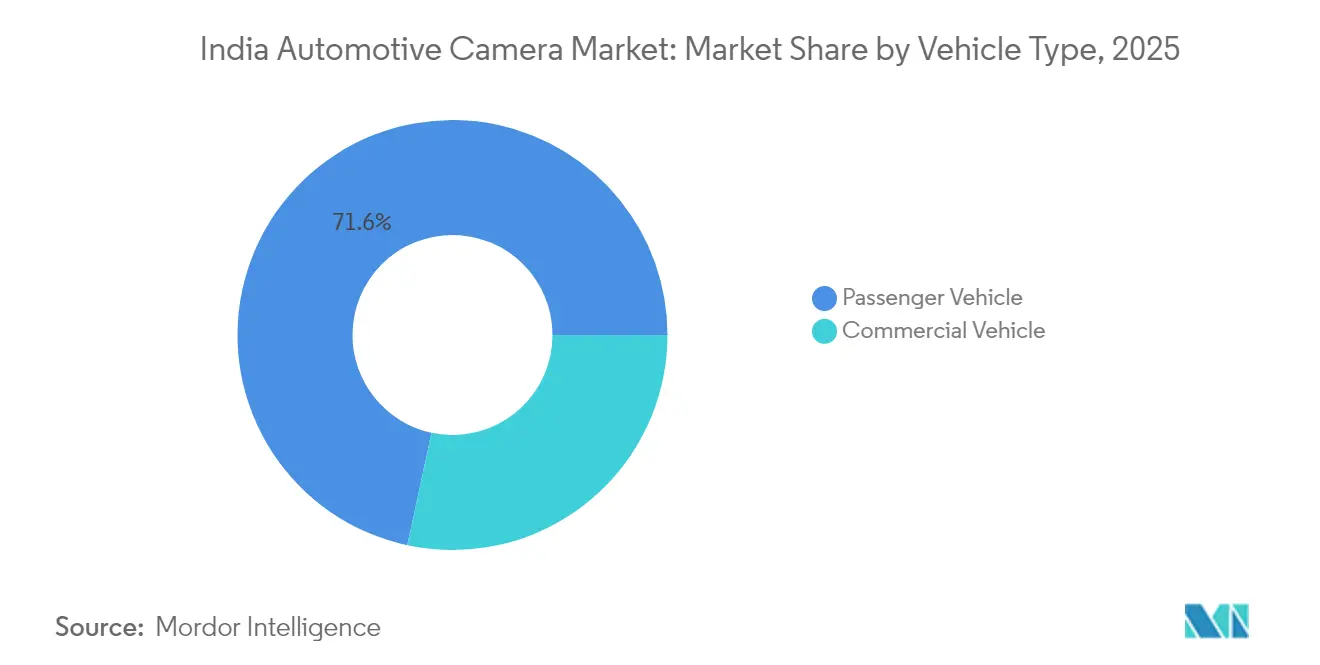

- By vehicle type, passenger vehicles led the Indian automotive camera market with 71.63% of the share in 2025, while commercial vehicles are projected to expand at a 16.98% CAGR through 2031.

- By camera type, viewing cameras captured 62.74% of the Indian automotive camera market in 2025; sensing cameras are forecast to grow at an 18.12% CAGR between 2026 and 2031.

- By application, parking and surround-view systems accounted for 56.95% of the Indian automotive camera market in 2025, whereas ADAS applications are set to advance at a 17.29% CAGR to 2031.

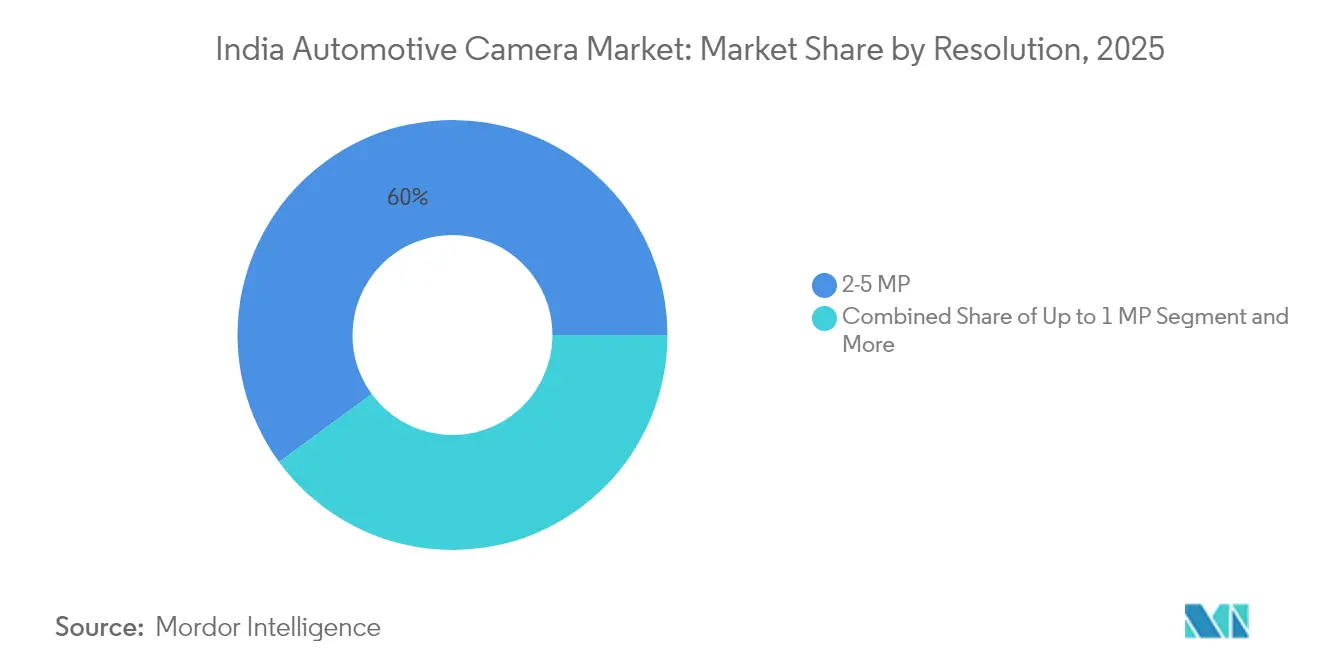

- By resolution, the 2–5 MP segment held 60.05% of the Indian automotive camera market in 2025, while cameras above 5 MP are expected to post a 16.85% CAGR over the next five years.

- By sales channel, OEM-fit solutions dominated the Indian automotive camera market, with 80.62% of the market in 2025; the aftermarket segment is anticipated to record a 15.84% CAGR through 2031.

- By mounting location, rear-view modules comprised 51.21% of the Indian automotive camera market in 2025, whereas front-view cameras are poised for a 16.72% CAGR during 2026-2031.

- By region, North India commanded 36.29% of the Indian automotive camera market in 2025, while South India is projected to log a 16.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Automotive Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter AIS-150 and Bharat NCAP Safety Mandates | +3.2% | National, early lead in North and West | Medium term (2-4 years) |

| Rising Demand for Parking-Assist and ADAS | +2.8% | Metro and Tier-1 urban centers | Short term (≤ 2 years) |

| Volume Growth in Premium Hatchbacks and SUVs | +2.4% | National, strongest in North and West | Medium term (2-4 years) |

| Declining CMOS Costs and Localized Supply Chains | +2.1% | Manufacturing hubs in South and West | Long term (≥ 4 years) |

| PLI Incentives for Domestic Camera Modules | +1.9% | South, West, selective North | Long term (≥ 4 years) |

| Usage-Based Insurance Analytics | +1.3% | Urban markets nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter AIS-150 and Bharat NCAP Safety Mandates

Regulatory frameworks reshape the Indian automotive camera market as AIS-150 compels electronic stability control and advanced braking across vehicle categories beginning 2026. Bharat NCAP scores tie directly to camera-enabled ADAS, prompting Mahindra, Hyundai, and Tata to add Level 2 functions in mid-tier trims to secure higher ratings[1]“Bharat NCAP to Drive Safer Vehicles,”, Press Information Bureau, pib.gov.in. Phased timelines help firms spread investment, yet small OEMs grapple with certification costs that ultimately favor suppliers holding proven safety credentials. Consumer awareness grows as NCAP star labels appear in showroom marketing, reinforcing camera demand nationwide.

Rising Demand for Parking-Assist and Surround-View Features

As urban areas grapple with congestion and dwindling parking spaces, there's a rising interest in camera-based driver assistance systems. Technologies like parking aids and surround-view cameras are in high demand, especially in premium vehicles that now boast sophisticated multi-camera setups for navigating tight city streets. Meanwhile, budget-friendly rear-view cameras are making waves in the aftermarket, with many drivers opting to enhance older vehicles for improved visibility. The surge in parking-related insurance claims underscores the growing consumer reliance on these visual aids, solidifying their presence across various vehicle segments.

Declining CMOS Camera Costs and Localized Supply Chains

Falling module costs, driven by lower semiconductor prices and increased production, enable automakers to add camera systems to affordable vehicles. This is making advanced safety and convenience features more common in entry-level models. Manufacturers are shortening delivery timelines and qualifying for government production-linked incentives through strategic partnerships. For instance, Motherson Sumi Systems’ Vision Systems division is increasing local content. By localizing more components, these collaborations boost supply chain efficiency and competitiveness in a market increasingly influenced by policy-driven manufacturing goals[2]“Annual Report 2025,”, Motherson Group, motherson.com. Deep localization softens forex shocks and nurtures supplier ecosystems in Karnataka, Tamil Nadu, and Maharashtra, where production clusters thrive.

Usage-Based Insurance Analytics Leveraging Camera Data

Insurers tap real-time driving footage for risk scoring, offering premium cuts of 10-15% to fleets installing cameras. The Insurance Regulatory and Development Authority now endorses usage-based products, sparking interest among logistics fleets that see dual gains in safety and insurance savings. Privacy rules under the Digital Personal Data Protection Act 2023 mandate informed consent, pushing suppliers to build secure data protocols that garner trust without dampening growth potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-Front Cost Premiums in Sub-INR 10-Lakh Cars | -1.8% | National, sharpest in rural and semi-urban markets | Short term (≤ 2 years) |

| Harsh Climatic and Road-Dust Conditions | -1.4% | North and West during monsoon and dust-storm seasons | Medium term (2-4 years) |

| FX-Linked Import Dependence on Image Sensors | -1.1% | Nationwide with tight supply-chain concentration | Medium term (2-4 years) |

| Consumer Privacy Concerns on In-Cabin Monitoring | -0.9% | Urban clusters with greater privacy awareness | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Harsh Climatic and Road-Dust Conditions Impairing Sensors

Indian summers top 50 °C, monsoons bring torrents, and seasonal dust storms coat windscreens. These extreme fog lenses cause condensation in housings and degrade electronics[3]“Environmental Stress on Automotive Cameras,”, IEEE, ieeexplore.ieee.org. Owners often ignore frequent cleaning, leading to image loss that erodes trust. Suppliers respond with rugged IP-rated units and hydrophobic coatings, inflating bills of material and lengthening test cycles at dedicated climatic chambers.

Consumer Privacy Concerns on In-Cabin Monitoring

Driver-facing cameras enable fatigue detection and insurance analytics, yet raise personal-data questions. Urban buyers, especially in tech-savvy cities, hesitate to accept always-on monitoring, slowing adoption in passenger cars. The Digital Personal Data Protection Act enforces consent and data-storage limits, so suppliers must include robust opt-in workflows and edge-processing features that avoid cloud upload when possible, adding design complexity and cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Dominance Drives Market Expansion

Passenger models generated 71.63% of 2025 revenue, underscoring the Indian automotive camera market's focus on consumer safety features. Commercial fleets, however, will post a 16.98% CAGR as electrification rules and logistics digitization spur mandatory monitoring. Passenger-car demand matches rising disposable income and technology differentiation, while fleet operators chase lower insurance premiums and accident liability reductions.

Commercial sales cycles are longer, yet telematics-linked discounts yield rapid ROI. OEM line-fit solutions simplify compliance and warranty management for both segments, although retrofits still appeal to budget-minded transporters upgrading legacy trucks. Passenger car camera take-rates escalate with every model refresh, driven by competitive launches from Mahindra, Hyundai, and Tata that now bundle basic ADAS under INR 20 lakh (~ USD 22,500).

By Camera Type: Sensing Technology Acceleration

Viewing units held 62.74% of shipments in 2025 as consumers prioritized parking ease. Sensing cameras will advance at an 18.12% CAGR through 2031, fueled by stereo configurations supporting lane-keeping and collision avoidance. Mono setups dominate entry-level builds thanks to lower cost, while stereo platforms emerge in premium crossovers touting Level 2 assistance.

The Indian automotive camera market size for sensing modules gains as processors drop in price and vision algorithms run efficiently on vehicle controllers. Upgrade complexity introduces calibration service revenue for workshops and gives software-centric suppliers a fresh edge. Viewing cameras remain relevant but cede share as NCAP-driven active safety rules migrate from premium to mid-range trims.

By Application: ADAS Emerges as Growth Leader

Parking and surround-view held a 56.95% share in 2025 because maneuvering hazards remain top of mind for city drivers. Still, ADAS will rise at a 17.29% CAGR as OEMs advance collision warning, auto emergency braking, and lane-departure systems to satisfy star-rating norms.

Driver monitoring gains fleet traction, though privacy sensitivity tempers private-car uptake. The application mix underlines an evolution from passive viewing toward active risk prevention, moving the Indian automotive camera market toward higher value content with incremental software revenue streams.

By Resolution: Higher Definition Drives Premium Adoption

Cameras rated 2-5 MP owned 60.05% of 2025 volumes, balancing clarity and cost. Units above 5 MP will climb 16.85% CAGR because ADAS logic needs crisp data at a longer range. Sub-1 MP parts fade except in bargain rear-view kits for small cars.

High-definition images require stronger SoCs and thermal design margins, and chipmakers now offer automotive-grade ISP packages. Production lines upgrade optics and clean-room processes to meet tighter tolerances, gradually lowering per-unit deltas and spreading HD adoption down the price ladder.

By Sales Channel: OEM Integration Dominates

OEM-fit captured 80.62% of 2025 shipments, proving in-plant integration wins on warranty and calibration quality. Aftermarket kits will still clock 15.84% CAGR, mainly rear-view sets sold through accessory chains to owners wanting budget compliance.

Complex ADAS retrofits stay niche because they need network access, coding, and precise alignment that only factories guarantee. As OEMs standardize cameras in mid trims, economies of scale narrow the price gap to aftermarket, further consolidating share.

By Mounting Location: Front-View Systems Gain Momentum

Rear-view modules kept a 51.21% share in 2025, aided by parking and heavy-vehicle rules. Front-view units will log 16.72% CAGR alongside ADAS growth that mandates forward recognition. Side-view and interior placements fill blind-spot monitoring and driver-fatigue niches, respectively, but remain smaller layers of the Indian automotive camera market.

Front sensors demand aerodynamic housings and heated lens keepers for monsoon resilience, inviting specialist component makers. Interior cameras face privacy scrutiny but win favor with commercial fleets where compliance outweighs concerns.

Geography Analysis

North India generated 36.29% of 2025 turnover thanks to clusters in Haryana and Uttar Pradesh that host major OEMs such as Maruti Suzuki and Honda. Proximity to the National Capital Region speeds design iterations and brings supplier density that trims logistics expenses. Seasonal dust storms and temperature swings test camera robustness, yet robust service networks limit downtime.

South India will outpace all regions at a 16.63% CAGR through 2031. Karnataka’s electronics belt and Tamil Nadu’s auto corridor attract camera R&D investment, anchored by engineering talent from local institutes. Bangalore and Chennai act as validation hubs where global Tier-1s tune ADAS algorithms for Indian roads, reinforcing the Indian automotive camera market position as an export-capable tech center.

West India leverages Maharashtra’s manufacturing base and Gujarat’s port access to secure component flow and finished-vehicle exports. State incentives lure new factories, and a vast supplier pool supports complex camera assemblies. East and North-East zones remain small today, but rising vehicle ownership and highway expansion will open fresh lanes for camera vendors eyeing underserved territories.

Competitive Landscape

The Indian automotive camera market is moderately concentrated, as the top five players command near-45% revenue. Bosch, Continental, and Valeo apply decades of ADAS expertise and leverage partnerships for local production. Bosch’s memorandum with Tata Electronics underscores deeper semiconductor roots. At the same time, Continental’s new Aumovio identity spotlights software-defined vehicles and camera-centric safety. Valeo scales its Fish-Eye architecture for compact cars to meet cost targets.

Domestic majors seize PLI funds to close technology gaps. Motherson Sumi Systems pushes localized content and eye-tracking modules, whereas Uno Minda broadens electronics capacity for EV and ICE lines. Competitive levers include harsher climate validation, lower total cost, and faster homologation cycles. White space remains in fleet-oriented driver monitoring and retrofit twins for the insurance market. Technology convergence invites chipmakers and smartphone camera suppliers that offer advanced imaging IP, spurring alliances like Magna’s tie-up with NVIDIA aimed at high-compute ADAS roadmaps.

Regulatory certifications enable certain suppliers to deliver NCAP-compliant systems punctually, giving them a competitive edge. This differentiation often relegates smaller entrants to niche positions or tier-2 roles, as they may lack the resources or expertise to meet stringent certification requirements.

India Automotive Camera Industry Leaders

Continental AG

Magna International Inc

Robert Bosch GmbH

Valeo SA

Autoliv Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tata Electronics and Bosch inked an MoU to explore collaborative manufacturing of automotive electronics, such as camera modules, tailored for Indian initiatives. This partnership aims to leverage Bosch's expertise in automotive technology and Tata Electronics' manufacturing capabilities to support the growing demand for advanced automotive electronics in India. The collaboration is expected to contribute to the development of localized solutions, aligning with the Indian government's push for self-reliance in manufacturing under the "Make in India" initiative.

- January 2024: Maruti Suzuki is set to invest a whopping INR 3.5 billion in Gujarat, marking the establishment of its second automobile plant. With an ambitious annual capacity of 1 million units, the new facility is slated to commence operations in the fiscal year 2028-29. This move will effectively double Maruti Suzuki's production capacity in Gujarat to a robust 2 million units annually. Notably, this expansion is largely fueled by a rising demand for features, such as car cameras, across Maruti's diverse model lineup, rather than any production delays.

India Automotive Camera Market Report Scope

India automotive camera market covers the latest trends and technological development in the automotive camera market, demand for the vehicle type, camera type, application type, and share of major players.

By Vehicle Type

| Passenger Vehicle | Hatchback |

| Sedan | |

| Sport Utility Vehicle and Multi-Purpose Vehicle | |

| Commercial Vehicle | Light Commercial Vehicle |

| Medium and Heavy Commercial Vehicle |

By Camera Type

| Viewing Camera | |

| Sensing Camera | Mono |

| Stereo |

By Application

| ADAS |

| Parking & Surround View |

| Driver Monitoring |

By Resolution

| Up to 1 MP |

| 2-5 MP |

| Above 5 MP |

By Sales Channel

| OEM-Fit |

| Aftermarket |

By Mounting Location

| Front View |

| Rear View |

| Side View |

| Interior/In-Cabin |

By Region

| North |

| South |

| West |

| East & North-East |

| By Vehicle Type | Passenger Vehicle | Hatchback |

| Sedan | ||

| Sport Utility Vehicle and Multi-Purpose Vehicle | ||

| Commercial Vehicle | Light Commercial Vehicle | |

| Medium and Heavy Commercial Vehicle | ||

| By Camera Type | Viewing Camera | |

| Sensing Camera | Mono | |

| Stereo | ||

| By Application | ADAS | |

| Parking & Surround View | ||

| Driver Monitoring | ||

| By Resolution | Up to 1 MP | |

| 2-5 MP | ||

| Above 5 MP | ||

| By Sales Channel | OEM-Fit | |

| Aftermarket | ||

| By Mounting Location | Front View | |

| Rear View | ||

| Side View | ||

| Interior/In-Cabin | ||

| By Region | North | |

| South | ||

| West | ||

| East & North-East | ||

Key Questions Answered in the Report

What is the 2026 value of the India automotive camera market?

The market is valued at USD 347.42 million in 2026.

How fast will revenue grow through 2031?

Revenue is projected to rise to USD 697.67 million, reflecting a 14.96% CAGR during 2026-2031.

Which camera type is gaining ground the quickest?

Sensing cameras will expand at an 18.12% CAGR through 2031.

Which region is the fastest-growing market?

South India is on track for a 16.63% CAGR thanks to strong electronics ecosystems.

Which vehicle class uses the most cameras today?

Passenger cars account for 71.63% of 2025 shipments.

Page last updated on: