North America Automotive Airfilters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

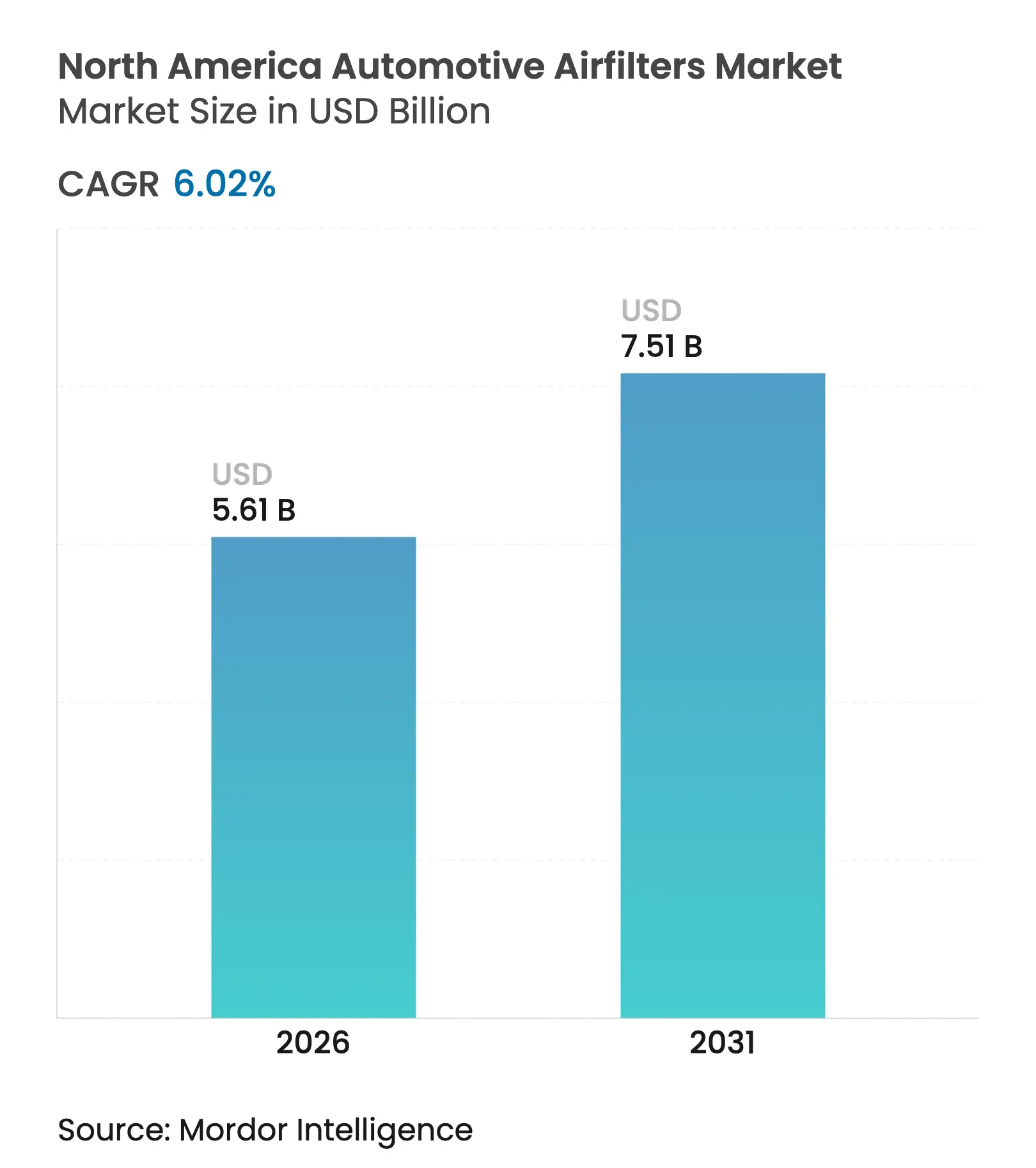

| Market Size (2026) | USD 5.61 Billion |

| Market Size (2031) | USD 7.51 Billion |

| Growth Rate (2026 - 2031) | 6.02 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Automotive Airfilters Market Analysis by Mordor Intelligence

The North America Automotive Air Filters market size was valued at USD 5.29 billion in 2025 and estimated to grow from USD 5.61 billion in 2026 to reach USD 7.51 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031). Robust replacement demand from an ageing vehicle parc, tightening U.S.–Canada particulate and NOx limits, and migration toward premium cabin filtration underpin this steady expansion of the North America automotive air filters market. Cabin filters now dominate unit volumes because wildfire smoke episodes, urban smog, and prolonged daily commutes convert filtration from a maintenance chore into a health safeguard. Nanofiber media adoption accelerates as regulators press for higher filtration efficiency without airflow penalties, while online retail reshapes route-to-market economics by giving consumers transparent pricing and choice. At the same time, the rising share of battery electric vehicles erodes long-term engine-intake filter volumes, forcing suppliers to pivot toward HEPA cabin, thermal-management, and smart-sensor products within the North American automotive air filters market.

Key Report Takeaways

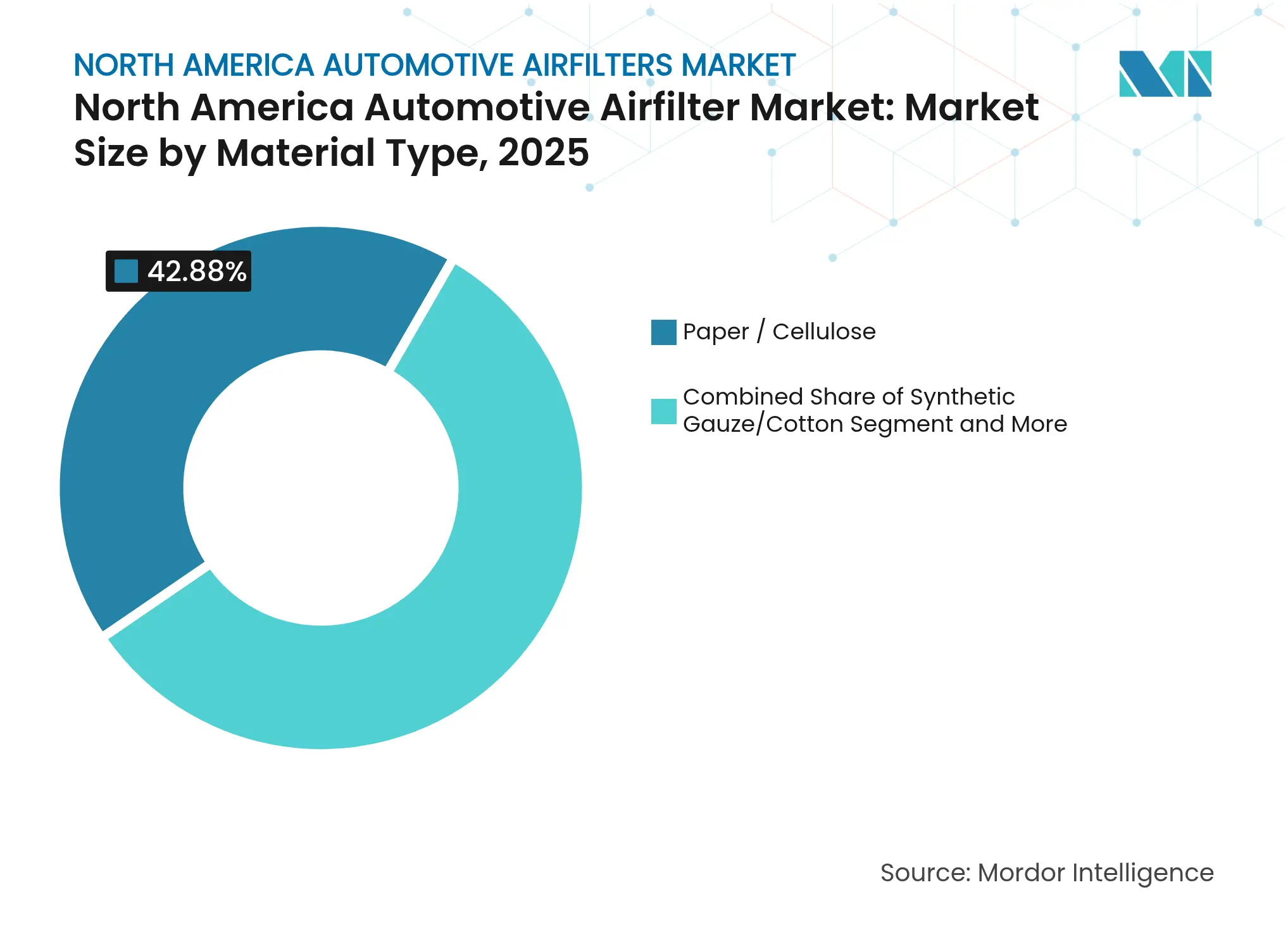

- By material type, paper/cellulose commanded a 42.88% share of the North American automotive air filters market in 2025, while nanofiber composites are projected to grow at an 8.03% CAGR between 2026 and 2031.

- By filter type, cabin filters held 54.62% of the North America automotive air filters market share in 2025 and are expanding at a 7.29% CAGR to 2031.

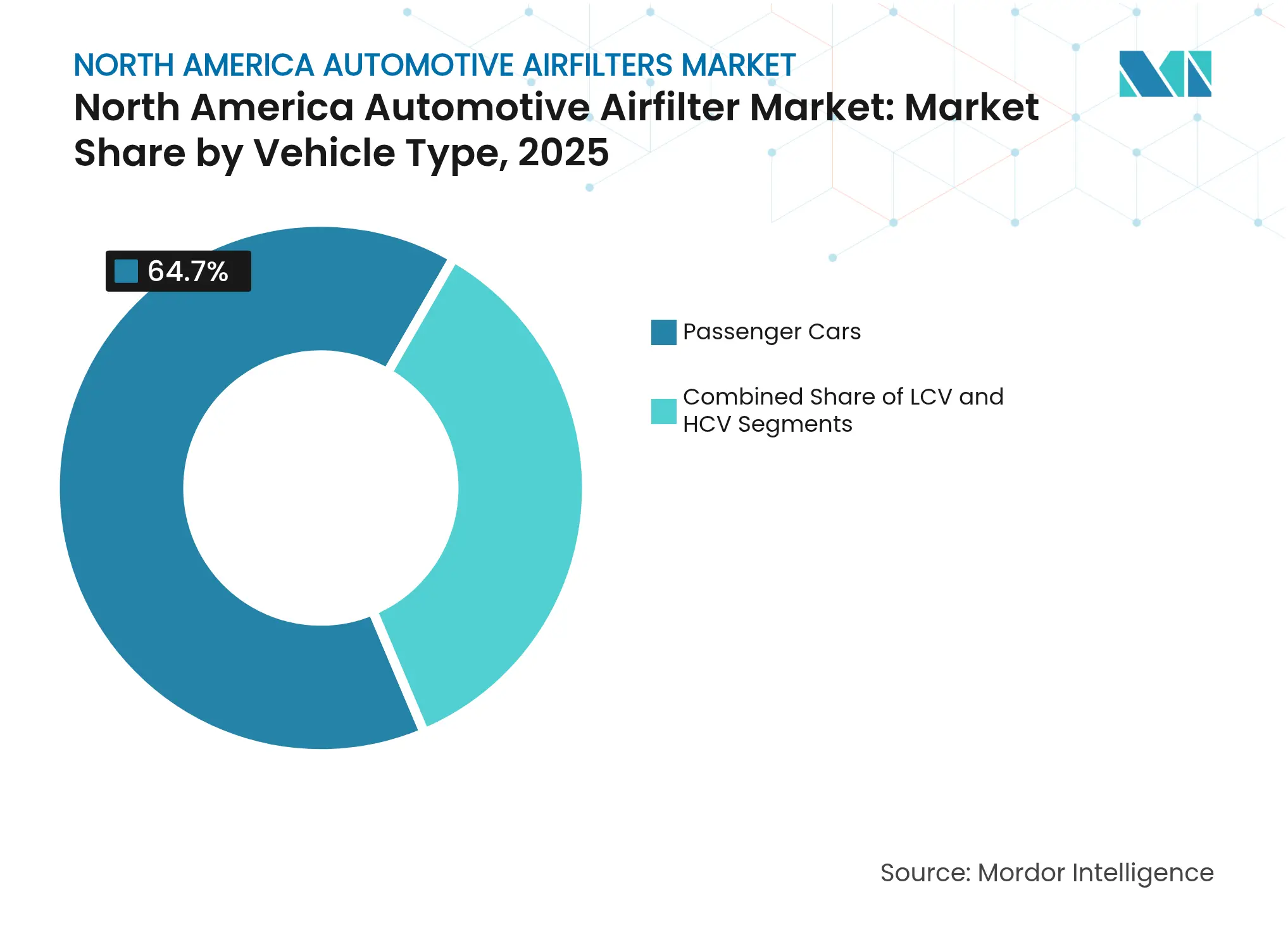

- By vehicle type, passenger cars led with 64.70% revenue share in 2025; light commercial vehicles are forecast to post the fastest 7.02% CAGR through 2031.

- By sales channel, the aftermarket accounted for 61.08% of the North America automotive air filters market in 2025, whereas online retail is set to grow at a 9.42% CAGR to 2031.

- By country, the United States dominated with a 73.85% market share in 2025; Mexico is projected to record the highest 7.38% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Automotive Airfilters Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Ageing Light-Vehicle Parc Ageing Light-Vehicle Parc | +1.5% | North America-wide, rural areas higher | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.5% | Geographic Relevance:North America-wide, rural areas higher | Impact Timeline:Long term (≥ 4 years) |

Stricter U.S.–Canada Emission Norms Stricter U.S.–Canada Emission Norms | +1.2% | United States, California leading | Medium term (2-4 years) | |||

Rapid Cabin-Air Quality Awareness Rapid Cabin-Air Quality Awareness | +0.8% | Western North America, British Columbia | Short term (≤ 2 years) | |||

EV/HV Platforms With HEPA Cabin Filters EV/HV Platforms With HEPA Cabin Filters | +0.7% | California, Quebec, urban centers | Medium term (2-4 years) | |||

OEM Shift Toward Nanofiber Engine OEM Shift Toward Nanofiber Engine | +0.6% | North America, Mexico manufacturing hubs | Medium term (2-4 years | |||

Integration of IoT Predictive Replacement Apps Integration of IoT Predictive Replacement Apps | +0.4% | Tech-forward metropolitan areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Stricter U.S.–Canada PM & NOx Emission Norms Drive Filter Upgrade Cycles

U.S. EPA light- and medium-duty standards for model years 2027-2032 push fleet average CO₂ targets to 85 g/mile, compelling automakers to specify higher-efficiency engines and cabin media that capture finer particulates without throttling airflow.[1]“Multi-Pollutant Emissions Standards for Model Years 2027-2032,”, United States Environmental Protection Agency, epa.govCalifornia’s Advanced Clean Cars II waiver, approved in December 2024, further tightens regional benchmarks that sooner or later cascade across the North American automotive air filters market.[2]“California Waiver for Advanced Clean Cars II,”, United States Environmental Protection Agency, epa.gov Nanofiber composites benefit by delivering the required capture efficiency with lower pressure drop, preserving fuel economy. Suppliers capable of documenting filtration performance under the tougher PM2.5 limit of 9 µg/m³ secure pricing power, whereas legacy cellulose lines suffer margin compression. Heavy-duty standards effective from 2027 raise durability and warranty thresholds, nudging light-duty buyers to perceive long-life filters as baseline value, reinforcing premium tiers within the North America automotive air filters market.

Rapid Cabin-Air Quality Awareness Post-Wildfire Seasons

Record wildfire smoke in 2024 blanketed California, Oregon, and British Columbia for weeks, pushing particulate readings above health-alert thresholds and igniting consumer demand for HEPA-grade cabin filters. State policy reviews now mandate high-efficiency filtration for buildings exposed to smoke plumes.[3]“State Policies on Wildfire Smoke Indoor Air Quality,”, Environmental Law Institute, eli.orgThat same mindset spills onto driveways: commuters treat vehicles as rolling shelters and seek filters with viral, allergen, and smoke removal claims. Mass-market OEMs respond by offering multi-layer cabin cartridges once limited to luxury trims, while aftermarket players package retrofit kits for older models. Promotional campaigns highlight World Health Organization PM2.5 guidance and children’s respiratory health to justify a premium upsell. The feedback loop tightens as navigation apps overlay smoke maps, nudging drivers to activate recirculation and reminding them to change filters. This human-health narrative cements Cabin Media as the North American automotive air filter market's heartbeat.

EV/HV Platforms Adopting Dedicated HEPA Cabin Filters

Electric and hybrid vehicles reach North American roads in larger volumes each quarter, and their silent cabins give engineers a clean canvas to spotlight air purity. Automakers install HEPA systems rated to medical-device standards and advertise pollen and virus removal claims as showroom differentiators. The National Renewable Energy Laboratory projects an extra 3.9 million plug-in vehicles by 2032. Although BEVs delete engine-intake filters, the higher unit value of HEPA modules offsets volume loss, supporting revenue resilience across the North America automotive air filters market. Suppliers with automotive-qualified HEPA media and low-noise blower integration seize early-mover advantage. Municipal incentives in Quebec and California accelerate this trend, ensuring medium-term lift despite engine-filter attrition.

Integration of IoT-Enabled Smart Filters With Predictive Replacement Apps

Connected filters embed RFID tags or Bluetooth sensors that measure differential pressure over time, transmitting remaining life estimates to phone apps and fleet dashboards. Pilot programs in tech-forward cities such as Austin, Seattle, and Toronto demonstrate 5% fuel-economy gains when fleets replace clogged filters proactively. Data monetization opens subscription revenue for filter makers, and API links to e-commerce storefronts streamline next-day replenishment. Insurance companies studying telematics tie clean cabin air to driver alertness, foreshadowing premium discounts that could widen adoption. The result is an emerging digital ecosystem that solidifies long-term share for suppliers investing in firmware and cloud platforms rather than raw media alone.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

BEV Adoption BEV Adoption | -1.8% | California, Quebec, urban centers | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:California, Quebec, urban centers | Impact Timeline:Long term (≥ 4 years) |

Washable Cotton Gauze Filters Washable Cotton Gauze Filters | -0.9% | Performance enthusiast markets, Southwest U.S. | Medium term (2-4 years) | |||

Polypropylene & Cellulose Pulp Price Polypropylene & Cellulose Pulp Price | -0.7% | Global supply chains, North America manufacturing | Short term (≤ 2 years) | |||

Counterfeit E-commerce Filters Counterfeit E-commerce Filters | -0.5% | Online retail channels, price-sensitive segments | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Long-Life Washable Cotton Gauze Filters Cannibalizing Replacements

Reusable cotton-gauze filters marketed by performance brands extend service life from 12 months to nearly 5 years. Enthusiasts appreciate airflow gains and sustainability messaging, especially in desert states where dust traditionally forces frequent swaps. Retailers emphasize 50,000-mile warranties and lifetime cost savings, pulling value away from conventional paper lines. Mainstream uptake remains capped by a higher upfront price and the messy oil-recharge process that can foul mass-airflow sensors. Nevertheless, even modest conversion rates shave volumes in the aftermarket segment of the North America automotive air filters market. Manufacturers counter by launching drop-in washable cabin filters with antimicrobial linings, recapturing revenue while aligning with circular-economy goals.

BEV Adoption: Eliminating Engine-Intake Filter Demand By 2035

Zero-emission regulations could push BEVs to 50% of new sales by 2030 in leading regions, stripping half of the traditional engine-filter volume out of the North America automotive air filters market. Suppliers brace for a structural shift from high-volume, low-margin intake filters to higher-value but lower-volume cabin and battery-thermal media. The timeline is uneven: rural and vocational fleets retain diesel and gasoline engines beyond 2040, but coastal states cut demand sharply earlier. Hence, diversified product roadmaps and investment in HEPA, odor-adsorption, and liquid-coolant filtration become existential, not optional, for incumbents.

Segment Analysis

By Material Type: Nanofiber Innovation Challenges Traditional Media

Nanofiber composites held a modest slice in 2025 yet are on course for 8.03% CAGR, the fastest of any material, as regulators focus on PM2.5 capture. While Paper/Cellulose still accounts for 42.88% of the North American automotive air filters market, paper and cellulose struggle to meet new efficiency targets without thickening pleats that choke airflow. Electrospun nanofibers remove 99.9998% of 300-500 nm particles at low pressure drop, a metric validated in Macromolecular Materials and Engineering studies. Suppliers blend nanofiber coatings with cellulose cores to keep costs palatable and to use existing production lines. Sustainability pressures add complexity: plant-based polymers and recycled cellulose draw R&D funding as OEMs pursue carbon-neutral supply chains. Graphene-oxide-reinforced cellulose nanofibers delivered 99.98% capture in laboratory tests while biodegrading in soil, signaling pathways for future mainstream deployment.

Price volatility in polypropylene and pulp hampers smaller firms with weak hedging strategies, pushing them toward contract manufacturing or specialty niches. Vertically integrated multinationals with pulp plantations and resin plants enjoy cost leverage and can experiment with hybrid stacks mixing melt-blown, spunbond and electrospun layers. Over 2026-2031, nanofiber adoption trickles down from turbo-gasoline SUVs into light commercial vans, raising the North America automotive air filters market size captured by the material from single digits to mid-teens by decade’s end.

Note: Segment shares of all individual segments available upon report purchase

By Filter Type: Cabin Filters Drive Market Evolution

Cabin filters already control 54.62% of revenue. They are fighting engine-intake filters for every incremental dollar, a rare instance where a comfort feature outranks a drivetrain component in the North America automotive air filters market. Cabin units grow 7.29% CAGR, boosted by wildfire smoke, pandemics, and HEPA positioning. Engine filters remain essential for sold internal-combustion vehicles but confront longer service intervals and gradual volume attrition as BEVs scale. Research from the U.S. Department of Energy sets energy factors for air cleaners, indirectly nudging automotive engineers toward higher CADR (clean air delivery rate) targets. Automotive cabins copy home-air-purifier marketing language: multi-layer particulate-carbon-antimicrobial stacks, smartphone-controlled recirculation, and LED life indicators. Suppliers differentiate by impregnating activated carbon with copper or silver ions, promising viral inactivation within minutes, a claim validated by ISO 18184 tests. This technology shift cements cabin filters as the North America automotive air filter market's economic growth engine.

Despite the glamour around HEPA, mass-market vehicles continue to ship with particulate-only cabin filters that comply with cost ceilings. The aftermarket fills the gap: 30% of replacement cabin filters sold online in 2025 carry carbon or HEPA upgrades. As a result, distributors watch average selling price climb while the volume mix changes, improving margin contribution even as BEVs delete engine filters.

By Vehicle Type: Commercial segments outpace passenger cars

Light commercial vehicles (LCVs) are rising at 7.02% CAGR, paced by e-commerce and last-mile delivery that ratchet daily mileage and dust exposure higher than passenger cars. Mexico’s production surge to 3.99 million units in 2024 strengthens LCV supply into the United States and Canada, swelling OEM filter volumes embedded in exports. The North American automotive air filters market size for LCVs is projected to expand by 7.02% annually as fleets prioritize high-efficiency media that stretch service intervals and protect turbo-diesel injectors. Heavy commercial trucks, construction equipment, and off-highway machinery form a smaller base yet consume oversized filters frequently, contributing steady aftermarket cash flow cushions cyclical dips in light-vehicle demand.

Passenger cars still generate 64.70% of the revenue, but plateauing miles driven, improved seal designs, and rising BEV share flatten their filter replacement curve. Fleet electrification programs for ride-hailing, rental, and corporate mobility trim engine filter purchases but spark new cabin-pure-air packages that preserve spend per vehicle. Therefore, a revenue mix shift rather than outright collapse typifies the medium-term picture in the North America automotive air filters market.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: Online Retail Disrupts Traditional Distribution

The aftermarket dominates at 61.08% share due to the ageing car parc, yet online retail’s 9.42% CAGR is where narrative excitement lies. Pure-play marketplaces leverage shared logistics and algorithmic pricing to undercut brick-and-mortar rivals by 12-15%, cannibalizing walk-in traffic. Counterfeit filters infiltrate these channels, prompting brand owners to add scannable QR codes, tamper-evident seals, and online warranty registration to safeguard their reputation.

Authorized dealer service retains business from warranty-bound vehicles and lease returns that must use OEM parts. Yet even dealers integrate e-commerce portals for click-and-collect convenience, blurring channel boundaries. Smart-filter subscriptions and over-the-air lifespan alerts could unlock recurring revenue; early adopters report 25% repurchase rates inside 18 months. The dynamic underscores why digital mastery becomes as critical as media science for future winners in the North America automotive air filters market.

Geography Analysis

The United States anchors the North American automotive air filters market with a 73.85% share in 2025, underpinned by a 275 million-vehicle parc and nationwide service infrastructure. California’s leadership on CARB LEV III and Advanced Clean Cars II acts as a bellwether, pushing OEMs to standardize higher-efficiency filters across all states rather than run dual specifications. Wildfire-prone western states fuel cabin-filter upgrades, while southeastern markets with humid climates focus on mold-resistant antimicrobial media. Donaldson Company booked USD 2.25 billion in fiscal-year 2024 Mobile Solutions sales, much of it channelled through U.S. distributors, demonstrating local manufacturing’s pull on filter volumes. However, early BEV adoption, especially in California and Washington, erodes long-term engine-filter units, compelling suppliers to pivot toward HEPA and HVAC auxiliary filters.

Mexico represents the fastest-growing node at 7.38% CAGR to 2031. Nearshoring boosts production as OEMs hedge supply-chain risk and capitalize on USMCA tariff advantages. New plants in Guanajuato and Coahuila integrate nanofiber media supply onsite to feed turbo-gasoline exports. Domestic aftermarket culture matures as the national fleet ages and safety inspections proliferate, creating incremental replacement demand beyond factory fitments. Filter makers eye joint ventures and greenfield plants to dodge cross-border freight and currency volatility. Still, political stability, energy costs and enforcement of counterfeit crackdowns will dictate how completely Mexico transforms into a self-sustaining pillar of the North America automotive air filters market.

Canada contributes a stable, modest slice where growth comes mostly from replacement cycles and rising HEPA awareness in metro corridors such as Toronto, Montreal, and Vancouver. Provincial incentives accelerate EV uptake, reducing engine-filter demand yet amplifying HEPA cabin upgrades. Harsh winters and salted roads necessitate robust seals and corrosion-resistant housings. Alignment with U.S. emission rules simplifies product homologation, allowing manufacturers to pool inventory across the border. Canadian buyers, highly attuned to sustainability, test recyclable filter frames and washable cabin inserts, but premium pricing restricts uptake outside urban zones. As a result, Canada functions as a niche testbed for green material innovation within the wider North America automotive air filters market

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The North America automotive air filters market displays moderate fragmentation, no single player controls market, yet the top quintet secures meaningful economies of scale. Donaldson and Mann+Hummel leverage engineering depth and vertically integrated media lines to win OEM platforms and high-margin aftermarket SKUs. Donaldson’s FY 2024 sustainability program cut greenhouse gases 18% versus a 2021 baseline, a credential that resonates with automakers setting Scope 3 targets. Mann+Hummel’s MyAirShield nanofiber range feeds premium cabin demand, while Parker-Hannifin cross-sells filtration to mobility and industrial customers via a diversified base. Performance brands K&N and AIRAID blur into mainstream, promoting washable cotton-gauze products that cannibalize conventional replacement cycles.

Counterfeit infiltration through online channels erodes trust; the Automotive Anti-Counterfeiting Council coordinates takedowns, but the cat-and-mouse dynamic persists. Suppliers deploy serialized labels and blockchain registries, adding cost but preserving brand equity. Investment now tilts toward electrospun nanofibers, antimicrobial coatings, and IoT sensor integration, areas where smaller disruptors can leapfrog legacy tooling barriers. Subscription-direct startups package filters with smartphone reminders, courting tech-savvy drivers reluctant to queue at parts counters. Incumbents retaliate by launching direct-to-consumer portals or partnering with e-grocers to insert filters in next-day delivery networks. The contest mixes material science, digital commerce, and sustainability narratives as firms jockey for a share in the evolving North America automotive air filter market.

North America Automotive Airfilters Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: The EPA granted California’s waiver for Advanced Clean Cars II, cementing stricter emissions and accelerating filter-performance upgrades.

- April 2024: The EPA finalized multi-pollutant standards for MY 2027-2032 light vehicles, lowering CO₂ and PM limits and indirectly boosting high-efficiency filter adoption.

- January 2024: The Environmental Law Institute released a report on state wildfire-smoke mitigation policies, underscoring the pivot to high-efficiency filtration in mobile environments.

Table of Contents for North America Automotive Airfilters Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Stricter U.S.-Canada PM & NOx emission norms (EPA Tier-3, CARB LEV III)

- 4.2.2Rapid cabin-air quality awareness post-wildfire seasons

- 4.2.3Ageing light-vehicle parc greater than 12.5 yrs fueling aftermarket volumes

- 4.2.4EV/HV platforms adopting dedicated HEPA cabin filters

- 4.2.5Integration of IoT-enabled smart filters with predictive replacement apps

- 4.2.6OEM shift toward low-restriction nanofiber engine media for turbo-gasoline SUVs

- 4.3Market Restraints

- 4.3.1Long-life washable cotton gauze filters cannibalising replacements

- 4.3.2BEV adoption eliminating engine-intake filter demand by ~2035

- 4.3.3Polypropylene & cellulose pulp price volatility squeezing margins

- 4.3.4Proliferation of counterfeit e-commerce filters undermining branded share

- 4.4Value/Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1By Material Type

- 5.1.1Paper/Cellulose

- 5.1.2Synthetic Gauze/Cotton

- 5.1.3Foam

- 5.1.4Nanofiber Composite

- 5.1.5Others (Activated Carbon, Metal Mesh)

- 5.2By Filter Type

- 5.2.1Intake (Engine) Air Filters

- 5.2.2Cabin Air Filters

- 5.3By Vehicle Type

- 5.3.1Passenger Cars

- 5.3.2Light Commercial Vehicles (LCV)

- 5.3.3Medium and Heavy Commercial Vehicles (MHCV)

- 5.4By Sales Channel

- 5.4.1OEM

- 5.4.2Aftermarket

- 5.4.2.1Independent Aftermarket

- 5.4.2.2Authorized Service Centers

- 5.4.2.3Online Retail

- 5.5By Country

- 5.5.1United States

- 5.5.2Canada

- 5.5.3Mexico

- 5.5.4Rest of North America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1Mann+Hummel

- 6.4.2Donaldson Company

- 6.4.3Purolator Filters LLC

- 6.4.4K&N Engineering

- 6.4.5AIRAID (Truck Hero)

- 6.4.6S&B Filters Inc.

- 6.4.7Mahle GmbH

- 6.4.8Bosch Automotive Aftermarket

- 6.4.9Denso Corporation

- 6.4.10Cummins Filtration

- 6.4.11Fram Group

- 6.4.12Clarcor (Part of Parker-Hannifin)

- 6.4.13ACDelco (GM)

- 6.4.14AFE Power

- 6.4.15Wix Filters

- 6.4.16Sogefi Group

- 6.4.17H&V (Engineered Media)

- 6.4.18Roki Co., Ltd.

- 6.4.19Champion Laboratories

- 6.4.20Luber-finer

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Material Type

- Paper/Cellulose

- Synthetic Gauze/Cotton

- Foam

- Nanofiber Composite

- Others (Activated Carbon, Metal Mesh)

- Paper/Cellulose

- By Filter Type

- Intake (Engine) Air Filters

- Cabin Air Filters

- Intake (Engine) Air Filters

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Medium and Heavy Commercial Vehicles (MHCV)

- Passenger Cars

- By Sales Channel

- OEM

- Aftermarket

- Independent Aftermarket

- Authorized Service Centers

- Online Retail

- Independent Aftermarket

- OEM

- By Country

- United States

- Canada

- Mexico

- Rest of North America

- United States

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our North America Automotive Airfilters Baseline Stands Firm

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 5.29 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 0.96 B (2024) | Regional Consultancy A | Tracks only replacement cabin filters and excludes medium/heavy trucks | ||

USD 6.18 B (2024) | Industry Journal B | Uses shipment values without adjusting for distributor margins or aftermarket mark-ups |