Automotive Fuel Filter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

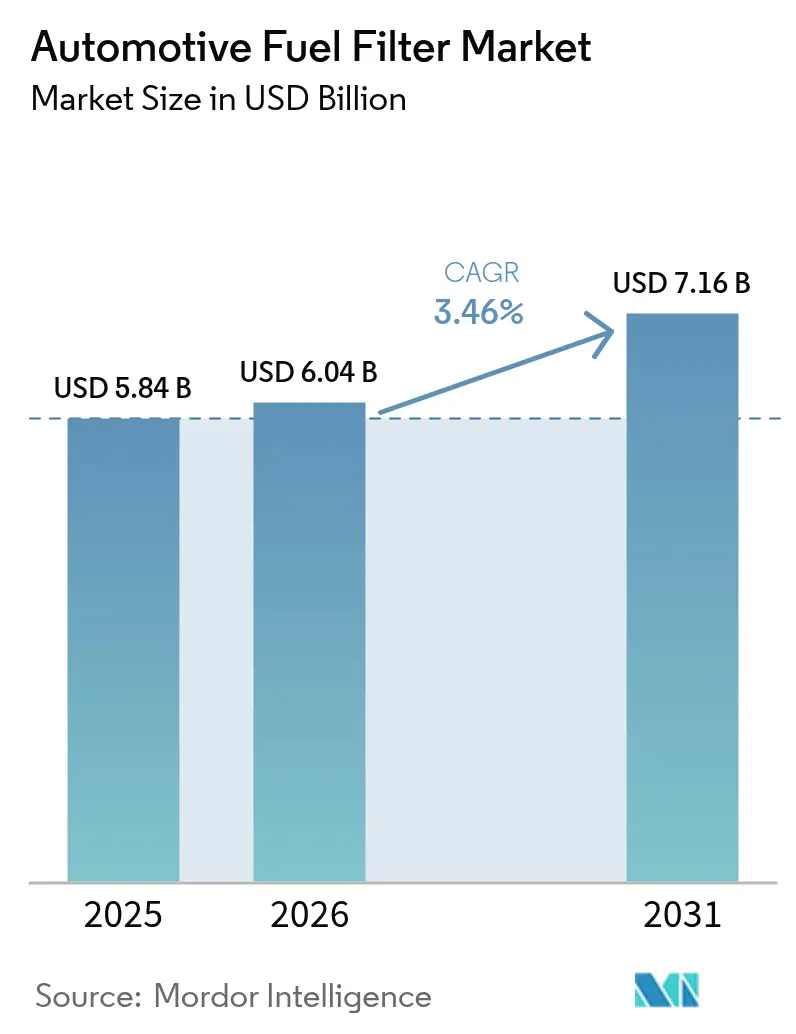

| Market Size (2026) | USD 6.04 Billion |

| Market Size (2031) | USD 7.16 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

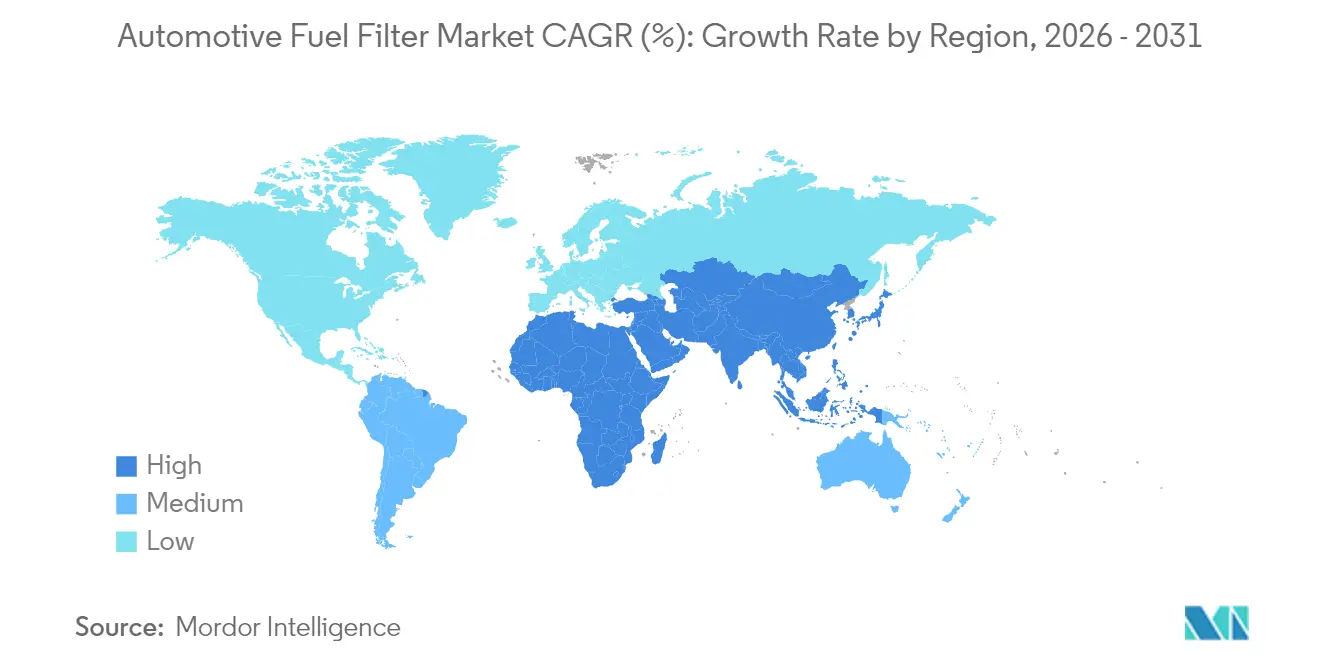

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

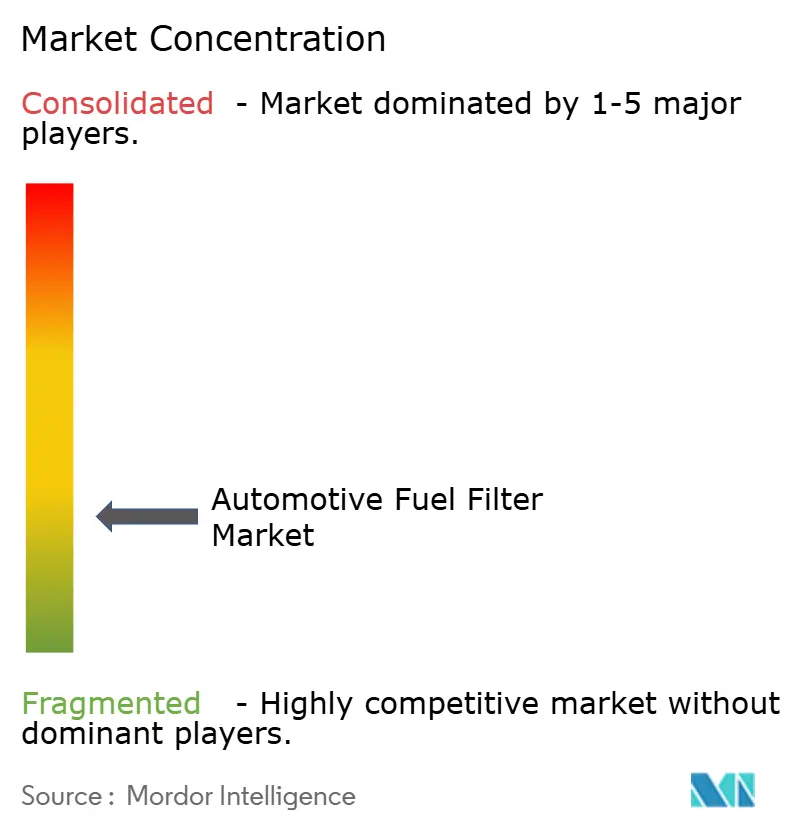

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Fuel Filter Market Analysis by Mordor Intelligence

The automotive fuel filter market size was valued at USD 5.84 billion in 2025 and estimated to grow from USD 6.04 billion in 2026 to reach USD 7.16 billion by 2031, at a CAGR of 3.46% during the forecast period (2026-2031). Global demand remains resilient as ageing vehicle fleets, stricter emission rules, and sustained production of internal-combustion vehicles in emerging economies offset the structural headwinds of electrification. Diesel applications preserve a sizeable revenue base because ultra-low-sulphur fuel legislation compels advanced water-separator designs, while bio-fuel blends and compressed natural gas create a parallel growth corridor for specialised filters. Rapid vehicle output in Asia-Pacific and Africa underpins original-equipment demand, whereas North America and Europe shift focus toward the replacement cycle. Digital retail, counterfeit risks, and sealed “lifetime” modules are reshaping competitive strategies across all tiers of the automotive fuel filter market.

Key Report Takeaways

- By fuel type, diesel held 47.82% of the automotive fuel filter market share in 2025; alternative fuels are projected to expand at a 8.87% CAGR through 2031.

- By filter media, cellulose led with 43.62% revenue share in 2025, while synthetic fibres are forecast to grow at 5.54% CAGR.

- By vehicle type, passenger cars commanded 54.05% of the automotive fuel filter market size in 2025, whereas light commercial vehicles are advancing at a 4.24% CAGR to 2031.

- By sales channel, the aftermarket segment controlled 70.12% of the automotive fuel filter market size in 2025 and is expected to post the quickest gains with a CAGR of 4.19% to 2031 as online platforms make replacement parts easier to source for workshops and DIY owners.

- By geography, Asia-Pacific dominated with 41.47% share in 2025; the Middle East & Africa region is on track for a 4.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Fuel Filter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Vehicle Parc Expanding Replacement Demand | +0.8% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Tighter Tail-Pipe Emission Norms | +0.6% | Europe, China, India with spillover to ASEAN | Medium term (2-4 years) |

| New-Vehicle Output in Asia-Pacific and Africa | +0.4% | APAC core, emerging Africa markets | Medium term (2-4 years) |

| Bio-Fuel Blends Requiring Compatibility Upgrades | +0.3% | Global, early adoption in EU and Brazil | Long term (≥ 4 years) |

| Ultra-Low-Sulphur Diesel Boosting Water-Separator Filter Demand | +0.2% | Global, regulatory-driven adoption | Short term (≤ 2 years) |

| Growth of High-Pressure GDI and CRDI Systems | +0.2% | Global, premium vehicle segments first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Global Vehicle Parc Expanding Replacement Demand

Global fleets are staying on the road for longer as household budgets tighten and new-car inventories fluctuate. Average passenger-car age in major OECD markets now exceeds 13 years, and extended maintenance schedules drive more frequent filter replacement to protect sensitive injectors. Light trucks and SUVs, which contain complex high-pressure fuel delivery systems, add to parts turnover. Dealers, independent garages, and e-commerce platforms leverage this aftermarket tailwind, enlarging the customer pool for the automotive fuel filter market. Parts distributors increasingly bundle fuel filters with other service kits to capture basket value and defend share in a price-sensitive environment.

Tighter Tail-Pipe Emission Norms Driving Advanced Filtration

Euro 6e rules took effect for new internal-combustion models in September 2023, and draft Euro 7 standards propose even lower particulate thresholds, forcing filter media to achieve sub-5-micron efficiency without sacrificing dirt-holding capacity. Comparable China VI and Bharat VI mandates require multi-stage filtration and robust water separation. Suppliers collaborate closely with engine OEMs to align filter specifications with after-treatment systems, while testing protocols have become stricter to validate durability across varying sulfur levels. Down-tier manufacturers face rising certification costs that may accelerate consolidation inside the automotive fuel filter market.

Rising New-Vehicle Output in Asia-Pacific and Africa

Vehicle production in India climbed to 31.03 million units during fiscal 2024-25 as investment incentives encouraged capacity additions. China still accounts for the world’s largest assembly volumes and eyes 35 million annual units by 2025, ensuring a large embedded base of combustion-engine cars through the decade. African markets such as Morocco, South Africa, and Egypt are scaling up localisation programmes, which strengthens demand for regionally supplied filters. Even with electric-vehicle momentum, policy frameworks in these regions still prioritise affordability and energy security, giving internal-combustion platforms a lengthy runway.

Surge in Bio-Fuel Blends Requiring Compatibility Upgrades

Fleet decarbonisation schemes in the European Union and the United States push transport operators to adopt biodiesel blends above B20; the U.S. Energy Policy Act provides compliance credits for such usage.[1]Alternative Fuels Data Center, “Biodiesel Blends,” afdc.energy.gov Higher ester content, however, elevates filter-blocking tendencies and accelerates media degradation. Manufacturers respond with hydrophobic synthetic layers, larger pleat surface areas, and in-line pre-heaters to relieve pressure-drop surges during cold starts. Engineering teams also trial ethanol co-solvent strategies to mitigate microbial growth in storage tanks. These efforts widen the product mix in the automotive fuel filter market and open premium-price niches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Penetration Cannibalising ICE Filter Volumes | -0.9% | Global, led by China, EU, California | Medium term (2-4 years) |

| Volatile Steel and Polymer Input Prices | -0.4% | Global manufacturing centers | Short term (≤ 2 years) |

| OEM Shift Toward Sealed "Lifetime" Fuel Modules | -0.3% | Developed markets, premium segments | Long term (≥ 4 years) |

| Proliferation of Counterfeit Low-Cost Filters | -0.2% | APAC, MEA, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating EV Penetration Cannibalizing ICE Filter Volumes

Battery-electric vehicles eliminate the need for fuel filtration, and their share of world car sales is projected to reach 50% by 2030. As manufacturers convert assembly lines and governments introduce zero-emission mandates, the serviceable market for fuel filters in mature regions declines. Workshops that once relied on high-margin replacement parts now pivot toward battery diagnostics and software updates. The automotive fuel filter market, therefore, grows largely where electrification rollouts are slower or where hybrid powertrains still incorporate auxiliary fuel modules.

Volatile Steel and Polymer Input Prices Squeezing Margins

Housing caps, endplates, and synthetic membranes depend on steel, aluminium, and engineering plastics whose spot prices fluctuate widely on commodity exchanges. Cost spikes compress gross margins for suppliers that operate on multi-year supply contracts with OEMs. Smaller firms struggle to secure hedged volumes and often absorb inflation rather than pass it on. The ability to substitute recycled or bio-based resins remains constrained by performance thresholds that must withstand high-pressure gasoline direct injection. This volatility narrows profit pools and raises the hurdle rate for capacity expansion inside the automotive fuel filter market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Diesel Dominance Amid Rising Alternative Blends

Diesel applications generated the highest revenue in 2025, holding 47.82% of the automotive fuel filter market share because trucks, off-highway machinery, and many SUVs require robust water-separator technology. Growth is sustained by ultra-low-sulfur mandates that expose tanks to condensation and microbial contamination. Fleet operators prize filters that trap particles down to 2 microns while collecting free water. Engineers are adapting elastomers and sealants to resist ester-induced swelling and methane-specific contaminants. Alternative fuels represent the fastest-growing segment at 8.87% CAGR through 2031. CNG buses in India and municipal fleets in Brazil underpin early volume, yet the segment’s technical requirements differ sharply from diesel, leading to specialised SKUs that command premium pricing.

The gasoline category, although pressured by electric-vehicle uptake, retains importance in ageing car parks across North America and parts of Europe where average mileage remains high. High-pressure gasoline direct injection systems demand sub-5-micron filtration and chemical resistance to ethanol. Suppliers see steady replenishment orders from independent workshops that align filter swaps with scheduled oil changes, reinforcing aftermarket stickiness. Diesel manufacturers also innovate around selective catalytic reduction, embedding sensors to alert operators when differential pressure rises beyond specification. This diagnostic trend ensures consistent pull-through for replacement parts and supports overall revenue stability in the automotive fuel filter market.

By Filter Media: Cellulose Leadership Tested by Synthetic Innovation

Cellulose remained the most widely used medium, contributing 43.62% of 2025 revenue thanks to low production cost and abundant feedstock. Yet its innate hydrophilicity and limited temperature resistance challenge its suitability for bio-fuel blends. Producers therefore coat cellulose fibres with hydrophobic agents while boosting pleat counts to raise dirt-holding capacity. Synthetic composites, polyester, polypropylene, and multi-layer nanofibers form the fastest-growing cohort at a 5.54% CAGR. These media achieve longer service intervals, lower differential pressure, and compatibility with aggressive fuel chemistries. Water-separator cartridges increasingly incorporate dual-zone designs, pairing a pleated synthetic layer with a coalescing fleece that forces micro-droplets to form larger beads before drainage.

Suppliers invest in plasma treatment and surface grafting to tailor fibre polarity. One widely adopted method bonds fluorinated silanes onto polyester, achieving water contact angles above 150° and resisting surfactant-rich diesel. In premium segments, melt-blown nanofibre layers augment base media to block particles below 1 micron, essential for ultra-high-pressure common-rail diesel pumps. Fabricators with in-house melt-blown assets gain scale advantages because they capture more value from vertically integrated membrane production.

By Vehicle Type: Passenger Cars Lead, Commercial Fleets Accelerate

Passenger cars, especially crossover SUVs, accounted for 54.05% of the automotive fuel filter market size in 2025 as consumer preference shifted toward larger, higher-output engines requiring substantial filtration capacity. Sport-utility platforms expose filters to greater vibration and extended idling, accelerating wear and driving earlier replacement intervals. Light commercial vehicles grow fastest at 4.24% CAGR, propelled by e-commerce logistics and parcel-delivery services that prioritize uptime. Fleet managers increasingly adopt predictive maintenance platforms that track pressure drop and temperature to schedule pre-emptive filter changes, curbing unplanned downtime and bolstering consumption in the automotive fuel filter market.

Medium and heavy trucks maintain steady demand because freight volumes move in tandem with infrastructure spending. Many long-haul operators adopt biodiesel blends, opportunistically lowering carbon footprints while protecting total-cost-of-ownership, provided filters are compatible. Off-highway segments, agricultural tractors, construction equipment, and mining trucks demand reinforced housings that survive vibration and contamination levels far above on-road norms.

By Sales Channel: Aftermarket Leadership Drives Digital Transformation

The aftermarket segment holds 70.12% of sales in 2025 and is set to expand the quickest through 2031, with a CAGR of 4.19%. Ageing cars and trucks need more frequent filter changes, and owners now shop for those parts online instead of relying only on local distributors. Digital storefronts let workshops and do-it-yourself motorists search by vehicle identification number, compare brands in seconds, and receive next-day delivery. This convenience, combined with competitive pricing and wider product ranges, keeps the aftermarket firmly in front. The original-equipment (OEM) channel still secures steady demand from new-vehicle production in Asia-Pacific and Africa, but its outlook is tempered by the growing use of sealed “lifetime” fuel modules that rarely require replacement.

E-commerce continues to reshape the broader parts landscape. Direct manufacturer-to-consumer platforms strengthen brand visibility, while established distributors build hybrid models that marry online catalogues with local pick-up points. Independent garages face rising complexity as fuel systems add sensors and tighter filtration tolerances, pushing some smaller shops to partner with larger retail chains for technical support and training. As platform data improves SKU forecasting and logistics efficiency, organised retailers gain scale advantages, leaving price-led niches and counterfeit products as the main competitive challenges in the aftermarket.

Geography Analysis

Asia-Pacific retained a commanding 41.47% share of the automotive fuel filter market in 2025, driven by prolific vehicle production across China, India, Thailand, and Indonesia. India’s Production Linked Incentive initiative has mobilized trillions of rupees in capex commitments, and policy planners expect component exports to follow similar trajectories. Local suppliers co-locate near OEM clusters to lower logistics costs and tap skilled labour pools. Even as China intensifies its new-energy-vehicle push, legacy gasoline and diesel platforms still dominate suburban and rural fleets, creating a steady replacement cycle. Domestic component brands strengthen export footprints into the Middle East, Eastern Europe, and South America, where their cost-to-performance ratio resonates.

The Middle East and Africa region is the fastest-growing territory, forecast at 4.98% CAGR through 2031. Gulf Cooperation Council states allocate hydrocarbons windfalls to road construction, freight corridors, and public-transport modernisation, which enlarges the rolling stock of buses and commercial trucks. Low ambient humidity often accelerates fuel tank condensation, elevating the importance of reliable water-separation features. Importers source filters from Europe and Asia but increasingly explore onshore assembly to stimulate jobs and shorten lead times. Sub-Saharan Africa’s young vehicle parc, coupled with lenient emission schedules, allows conventional diesel to remain prevalent, cushioning the automotive fuel filter market against electric encroachment.

North America and Europe exhibit modest growth as electrification incentives and sealed modules shrink volumes. Nevertheless, stringent particulate regulations and widespread adoption of gasoline direct injection force premium media upgrades, preserving average selling prices. Workshops promote bundled service packages to offset declining unit demand. Remanufactured filter programs gain popularity among eco-conscious drivers who seek lower environmental footprints without compromising warranty.

Regulatory Landscape

Vehicle-emissions and type-approval frameworks shape automotive fuel-filter specifications by tightening durability and in-use conformity requirements for ICE platforms. In the European Union, Implementing Regulation (EU) 2025/1706 (issued July 2025) sets procedures and test methodologies for exhaust and evaporative emission type-approval under Regulation (EU) 2024/1257, which strengthens the need for stable filtration performance over longer compliance periods and across varied duty cycles.

In the United States, the Environmental Protection Agency (EPA) advanced rulemaking activity in 2026 across light-duty and heavy-duty segments, including a May 2026 proposal in its Tier 3 and Tier 4 reconsideration (Part 1) and June 2026 updates to heavy-duty highway engine compliance provisions for MY 2027 and later. UNECE alignment also continues through regulations that reference updates tied to UN Regulation No. 83, and ISO standards used in filtration testing and validation, raising expectations for documentation, validation cycles, and repeatability for both OEM supply and qualified aftermarket parts.

Value Chain Analysis

The automotive fuel filter value chain starts with upstream suppliers of steel and aluminum housings, engineering polymers, elastomers, and engineered media (cellulose, glass fiber, and synthetic nonwovens). Media converters and Tier suppliers then pleat, treat, and assemble elements into in-line filters or integrated modules that include water separation and sensor provisions. Advanced media treatments, including hydrophobic coatings, coalescing layers, and multi-layer composites, are a key value-add step, particularly for diesel water-separator designs and for compatibility with higher bio-fuel blends.

Downstream, OEM demand is concentrated around vehicle assembly clusters, and suppliers increasingly co-locate near plants in major production regions such as Asia-Pacific (China, India, Thailand, and Indonesia) to reduce logistics costs and speed up engineering changes. The aftermarket remains the larger sales channel in this report scope, with multi-tier distribution through organized retailers, independent garages, and online platforms. In this segment, SKU matching, packaging authentication, and returns handling influence service levels and brand preference amid counterfeit risks and price competition.

Competitive Landscape

The automotive fuel filter market shows moderate fragmentation. Technology differentiation, rather than sheer scale, defines competitive edge. Leading firms allocate double-digit R&D budgets toward nanofiber membranes, coalescing rings, and sensor-integrated housings that furnish real-time clogging alerts. Mid-sized players specialise in regional niches, for example, agriculture in Europe or heavy-duty trucking in North America, to insulate themselves from price wars.

Counterfeit products remain the chief disruptor. Customs raids have uncovered large shipments of imitation cartridges bearing forged logos and inferior filter paper. Brand owners partner with e-commerce marketplaces to delist infringing offers and educate consumers on verification steps. Litigation and public-awareness campaigns slowly curtail the appetite for fakes, yet price-sensitive buyers still take risks. Companies that embed NFC chips or tamper-evident holograms into packaging record lower warranty claims and higher customer satisfaction scores.

Strategic moves cluster around capacity investments, joint ventures, and sustainability. Several tier-one suppliers retrofit lines to handle recycled polymers, reducing carbon footprints and meeting OEM scope-3 targets. Others establish technical centres in India and Brazil to tailor media formulations to local fuel chemistries, shortening development cycles. Patent filings concentrate on hydrophobic treatments, dual-stage cartridges, and smart modules compatible with over-the-air diagnostics that integrate seamlessly into fleet-management software suites.

Automotive Fuel Filter Industry Leaders

Denso Corp

MAHLE GmbH

MANN+HUMMEL

Robert Bosch GmbH

Donaldson Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrating in premium media and architecture upgrades tied to tighter particulate control needs, high-pressure injection systems (GDI and common-rail diesel), and fuel-chemistry variability from bio-fuel blending. Recent industry activity points to multi-layer and nanofiber media moving from development into commercialization, including Gessner Filtration highlighting a 3-layer fuel-filter media concept (micro-glass fiber, meltblown, and cellulose) and KOMAI introducing a nanofiber-based diesel fuel filter for high-pressure common-rail applications (January 2026). Both developments align with the shift toward finer filtration without sacrificing dirt-holding capacity.

Supply-chain regionalization and engineering localization also support OEM and aftermarket programs. In India, MANN+HUMMEL inaugurated a Global Technology and Innovation Center in Tumkur, Karnataka, alongside capacity actions in Pune (reported May 2026), supporting faster localization of filtration designs for regional fuel conditions and the local vehicle parc. In North America, Premium Guard Inc. completed Phase 2 acquisition of First Brands Group assets and consolidated manufacturing at the Albion, Illinois facility (June 2026), which reinforces shorter lead times and broader private-label and branded aftermarket coverage as online channels expand parts availability.

Recent Industry Developments

- July 2026: MANN+HUMMEL inaugurated its Global Technology and Innovation Center in Tumkur, Karnataka, described as its largest development hub outside Germany. The move strengthens localized engineering and validation capacity in a major vehicle-production region, supporting faster iteration of filter media, module designs, and application coverage for both OEM and aftermarket programs.

- February 2025: MANN+HUMMEL introduced a patented disassembly tool for the MANN-FILTER PU 10 023/1 z KIT used on models such as the Ford Ranger, enabling quicker and cleaner maintenance. Easier serviceability supports workshop throughput and helps defend branded aftermarket share as filtration modules become more integrated and access can be harder.

- December 2024: Uno Minda introduced a new aftermarket range covering filters including fuel filters for commercial vehicles. The expansion widens product availability in price-sensitive channels and increases competitive intensity in replacement demand tied to high-utilization fleets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from fuel filters used in on-road vehicles to remove contaminants from fuel before it reaches the engine, across OEM fitment and replacement demand in the aftermarket.

Scope exclusions: We exclude filters sold for off-highway equipment, marine engines, and stationary industrial engines.

Segmentation Overview

- By Fuel Type

- Gasoline

- Diesel

- Alternative Fuels

- By Filter Media

- Cellulose

- Synthetic (Glass and Polyester)

- Multi-layer Composites

- Water-Separator / Coalescer Elements

- By Vehicle Type

- Passenger Cars

- Hatchback

- Sedan

- Sport Utility Vehicle

- Multi-Purpose Vehicle

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Two-Wheelers

- Off-Highway

- Agricultural Machinery

- Construction and Mining Machinery

- Passenger Cars

- By Sales Channel

- OEM

- Aftermarket

- Organized Retailers

- Independent Garages

- Online Platforms

- Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To build the first structure of the model, we start with publicly available indicators that explain vehicle activity and replacement needs. Common inputs include road vehicle production and registrations from sources such as OICA, fuel quality and transport statistics from the International Energy Agency, and trade flows for filtration-related parts from UN Comtrade.

We also review government emissions and fuel standards publications (such as EPA and the European Commission), plus customs and tariff classification notes to reduce category mix-ups. Company annual reports, investor decks, and credible auto parts association pages are used to understand channel mix and typical replacement intervals, and then a paid subscription for company financials and news helps confirm scale and recent plant or sourcing changes. These listed sources are illustrative, and many other public and paid references are used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work is used to check what desk sources do not show clearly, especially average selling price movement, aftermarket replacement cycles by region, and how gasoline versus diesel demand is shifting in real orders. We speak with supply-chain, sales, and product leaders across major vehicle producing regions so assumptions on channel split, filter media mix, and commercial vehicle usage are corrected before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 44% |

| Mid tier: 46% | Functional/Unit leaders: 30% | EMEA: 34% |

| Smaller Players: 17% | Managers: 56% | Americas: 22% |

Market-Sizing & Forecasting

Market sizing is developed using a top-down build where vehicle parc, annual mileage patterns, and service interval norms are used to reconstruct the addressable replacement pool, which is then translated into value using region-wise price bands. To keep this grounded, we corroborate totals with selective bottom-up approximations, such as sampled channel checks on filter ASPs and a supplier-side roll up for a few high-volume countries, and then adjust for gaps where coverage is uneven.

Key inputs that guide the model include passenger and commercial vehicle production trends, in-use vehicle parc growth, the share of gasoline versus diesel vehicles in circulation, replacement frequency differences between OEM and aftermarket, and material mix shifts (cellulose versus synthetic media) that change pricing. For forecasting, scenario analysis is applied around vehicle production outlook, fuel-type transition pace, and aftermarket demand resilience, and those paths are aligned to the consensus heard from interviewees before the final 5-year curve is locked.

Data Validation & Update Cycle

Outputs are checked against independent signals, like region-level vehicle parc direction, known aftermarket share patterns, and observed price changes in filtration components, and then inconsistencies are investigated until the driver is explained. When a country or channel shows an unusual swing, we re-check the input series and may re-contact respondents to confirm whether it is a timing issue, a pricing shift, or a real demand change.

Each estimate goes through multi-step internal reviews where assumptions, unit logic, and currency treatment are inspected before sign-off. The report is refreshed annually, and interim updates are triggered when there are material events such as a sharp production correction, major emissions policy changes, or meaningful price inflation, and a final pre-release pass is completed so clients receive the most current view.

Mordor Intelligence's Automotive Fuel Filter Market Estimate Compared With Other Published Estimates

Published market values for automotive fuel filters often do not match because the boundaries are not always the same, and because price and volume assumptions are refreshed at different times. Differences also come from whether the sizing leans more on OEM production numbers or on aftermarket replacement behavior.

By tracking vehicle parc by region and channel and then refreshing price bands and replacement intervals through interviews, Mordor Intelligence keeps the counted revenue tied to on-road vehicle demand and avoids mixing in adjacent filtration products that sit outside fuel filters.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.04 B (2026) | |

| Global Consultancy A | USD 4.65 B (2025) | Uses a different base year and a broader product structure that can shift value between fuel filters and nearby filter categories, and the channel pricing and replacement intervals are not clearly tied back to an in-use vehicle parc build. |

| Industry Publisher B | USD 2.77 B (2024) | Heavier reliance on a narrower demand pool and earlier-year pricing, which can understate the value impact of synthetic media mix and aftermarket price dispersion across regions. |

The spread in the table mainly comes from timing, scope edges, and how replacement demand is converted into value through price and interval logic. When the same in-use vehicle base and channel behavior are used consistently, the resulting market size becomes easier to trace and repeat, which is what we aim to deliver in this report.

Key Questions Answered in the Report

What is the current value of the automotive fuel filter market?

The market is valued at USD 6.04 billion in 2026 and is projected to reach USD 7.16 billion by 2031.

Which region leads the global demand for fuel filters?

Asia-Pacific holds 41.47% of global revenue, benefiting from large-scale vehicle production in China and India.

Why are diesel filters still important despite electrification?

Trucks, off-highway machinery, and many SUVs continue to rely on diesel engines that require advanced water-separator filters to comply with ultra-low-sulfur fuel standards

How quickly is the online aftermarket growing?

Online channels are forecast to expand at a 4.61% CAGR as digital platforms simplify SKU matching and accelerate delivery.

Which filter media type is gaining share fastest?

Synthetic composites are growing at a 5.54% CAGR because they deliver longer service intervals and withstand aggressive bio-fuel chemistries.

Page last updated on: